180,000 U.S. homes face extreme risk from three natural disasters simultaneously.

New Orleans. Houston. 3 separate policies required — homeowners, windstorm, flood. 3 premiums. None on the listing.

Traditional listing sites don't show you this. But something exists that can.

Realtors have a name for it: attainability fatigue.

The monthly payment on a median Denver home is 87% higher than 2020 — and the conversation is still stuck on list price and mortgage rate.

There's more to what a home actually costs you.

https://t.co/k3Bk9TLJST

So we built Quoll Homes.

Not risk scores. Actual dollars — mortgage, insurance, property taxes, utilities — on every listing, with 10-year projections.

Search your market: https://t.co/jWlQ0Rur5r

#ClimateRisk#HomeBuying

In late 2025, Zillow quietly removed climate risk data from listings.

The official reason: to "adhere to varying MLS requirements."

What actually happened is worth understanding.

Here's the part that didn't get attention:

Risk scores alone were never the real answer.

Seeing "high fire risk" is financially ambiguous. Is that $200/yr in insurance? $4k/yr? Can the home even qualify for coverage?

Scores without $ don't help buyers make decisions.

The question isn't just "can I afford to buy this home?"

It's "can I afford to own it in year three? Year ten?"

Most home searches don't help buyers answer that.

https://t.co/jWlQ0RtTfT

#HomeBuying#ClimateRisk

By year 3, a $260,000 home in Tampa already costs more to own than a home that's $105,000 more expensive to buy.

The mortgage didn't change. Here's what did.

The mortgage on the Tampa home is $15,768/yr — and it never moves.

The variable costs started at $9,960/yr and reach $19,416 by year 10.

At purchase, the mortgage was 61% of total costs.

By year 10, it's 45%.

The home gets more expensive every year without anything going wrong

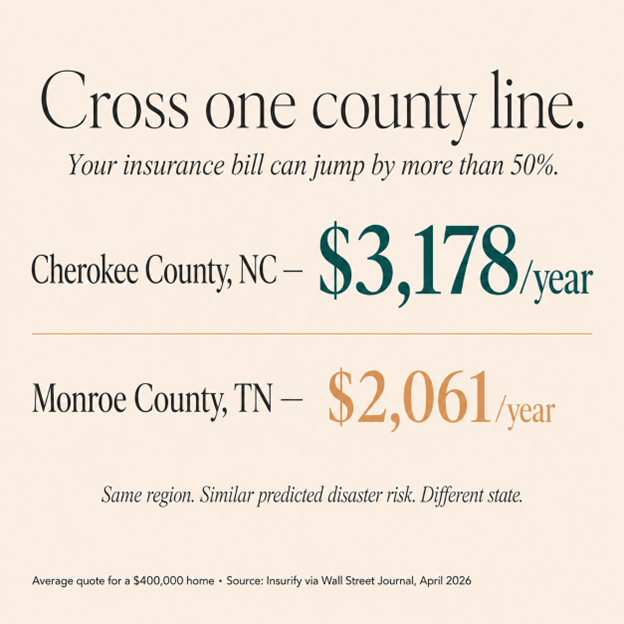

Home insurance is priced by address.

Cherokee County, NC and Monroe County, TN sit side by side. Similar disaster risk. The premium delta on a $400k home > $1,100 a year. Same region. Different state.

Averages don't tell buyers what they'll actually pay. The address does.

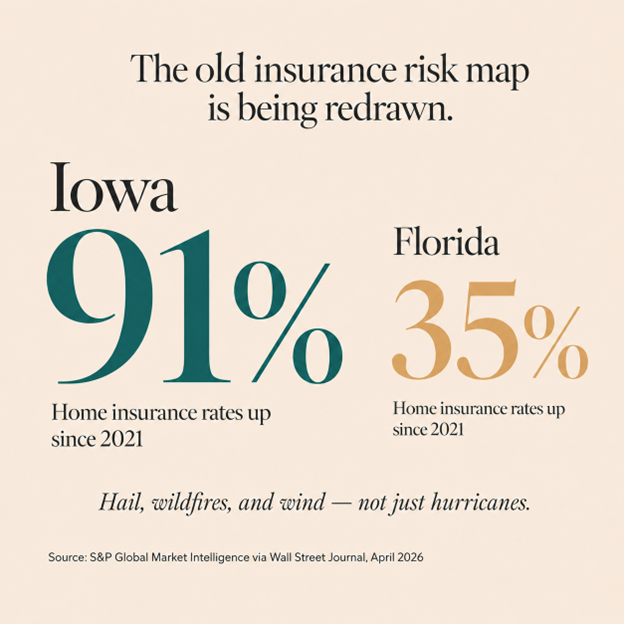

Since 2021, IA home insurance rates up 91%, FL up 35%.

The old assumption that coastal states pay most and inland states stay cheap is breaking down.

Common insurance cost assumptions by consumers today may be based on a risk map that no longer exists. #HomeInsurance#ClimateRisk

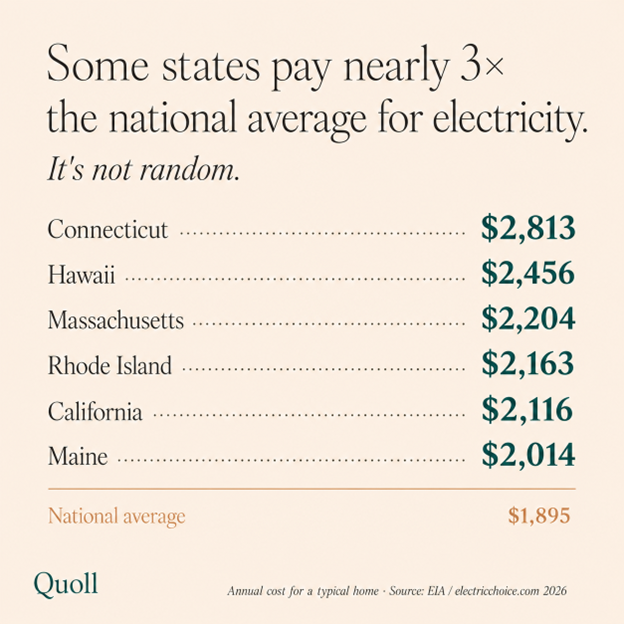

Some states pay nearly 3× the national avg for electricity — $1,895/yr nationally, up 30%+, with climate-related disasters driving grid hardening costs to ratepayers. California up 96% since 2014.

It doesn't show up in the listing when you're buying, but it'll cost you.

Climate risk isn’t just a repair or insurance story. It can become a market story too. In Hillsborough County (Tampa, FL area), homes are taking longer to sell than they were a few years ago, while disaster events have become part of the market backdrop.

A housing market needs enough earning power to support the place itself. Orlando, Miami and Tampa ranked among the bottom 5 big metros for median household income in 2024. When pay lags place costs, markets get harder to sustain.

Home value depends on the next buyer’s math. In places like Florida, wages are lagging while insurance and other climate-linked costs rise. When that math stops working for enough buyers, the buyer pool narrows before prices do. https://t.co/RJu223dWXO

A home can be affordable to buy and still costly to hold up. When specs get cut to lower the upfront price, the tradeoff can show up later in faster wear, more maintenance, and higher repair risk. How will it hold up?