The basket has delivered a pretty solid return so far.

Considering the starting date was April 27, I think the performance has been quite respectable.

You can view the basket here: https://t.co/ipGwtqK3Em

$INTC appointed former SK Hynix CEO Seok-Hee Lee as Executive Vice President of Intel Foundry.

The hire adds more foundry leadership depth as Intel tries to scale its contract chip manufacturing business and compete more directly with $TSM and Samsung.

Intel Foundry: Externally Disclosed & Inferred Pipeline

*Note* This is a speculative bull case construction, not company confirmed; every line carries meaningful estimate risk. However, these are my estimates on Intel Foundry customer pipeline.

1. CONFIRMED: Apple low-end M-series on 18A. I size this at ~$0.3–0.5B of revenue annualized. Apple’s base remains overwhelmingly TSMC, so any Intel allocation starts small.

2. SPECULATIVE: Broader M-series migration to IFS. Conditional, multi-year. If a first SKU succeeds, a wider shift is conceivable; I see this as incremental revenue at ~$1.5–2.5B at maturity, heavily probability-weighted down.

3. SPECULATIVE: Merchant AI-accelerator wins. One mid-scale custom-silicon program on 18AP (hyperscaler or neocloud). ~$1–2B incremental at run-rate… BUT does not include ASIC design services which i assume will be part of the deal and have no way to estimate how much revenue it could be.

4. CONFIRMED: Terafab (Tesla/SpaceX) on 14A . Musk has indicated 14A for the full-scale Terafab. But this is Tesla/SpaceX-led capacity, not an Intel licensing annuity, so Intel’s take is process-IP/enablement and structurally fuzzy. Placeholder ~$0.2–0.4B/yr.

5. CONFIRMED: Advanced packaging + logic-tile supply for Google TPU. The most credible “big” line item. I see this as a serious multi-year program at ~$3–6B cumulative over three years, assuming it displaces incumbent packaging supply.

6. SPECULATIVE: Feynman packaging & I/O dies. Combined advanced-packaging and 18AP/14A I/O die content of ~$1–2B.

7. SPECULATIVE: Possible EMIB-T adoption by Nvidia and a co-designed x86 collaboration. No public basis but consider it a low probability, high payoff possibility.

Much of Dwarkesh's argument hinges on this statment which *was* accurate but will be increasingly inaccurate on a go forward basis imo:

“American labs port across accelerators constantly. Anthropic's models are run on GPUs, they're run on Trainium, they're run on TPUs. There are so many things you can do, from distilling to a model that's well fit for your chips.”

As system level architectures diverge (torus vs. switched scale-up topologies, memory hierarchies, networking primitives), true portability is eroding. The Mi300 and Mi325 had roughly the same scale-up domain size as Hopper while Blackwell’s scale-up domain is 9x larger than the Mi355 scale-up domain, etc.

Many frontier models are now being explicitly co-designed for inference on specific hardware like GB300 racks. Codex on Cerebras is another example. Those models run less efficiently on other systems and the performance differentials will only widen. A model that runs well on Google’s torus topology will run less efficiently on Nvidia’s switched scale-up topology and vice versa - the data traffic is fundamentally different as a byproduct of the models being parallelized across the different topologies.

Google’s internal teams - and increasingly the Anthropic teams as they become the most important customer of almost every cloud - have the luxury of operating across the stack (models, chips, networking) - but that is not the case for the rest of the market and other prospective users. Anthropic is the exception, not the rule. To wit, Anthropic and Google allegedly have a mutual understanding where Anthropic can hire the TPU engineers they need every year to ensure that they can continue to get the most out of the TPU.

Given the overwhelming importance of cost per token to the economics of the labs, models will be run where they run best. Most extremely large MoE models will run best on GB300s given the importance of having a switched scale-up network like NVLink for MoE inference. When training was the dominant cost for labs and power was broadly available, labs were optimizing to minimize capex dollars. Model portability was a way to create leverage over suppliers. I think that drove a lot of the focus on portability.

Today, inference costs as measured by tokens per watt per dollar are everything. Inference is way more important than training costs (inference is effectively now part of training via RL). Labs are therefore now optimizing for inference. This means increasing co-design and higher go-forward switching costs for individual models between systems. I do think this explains why Anthropic and Nvidia came together: Anthropic needed Blackwells and Rubins to inference at least *some* of their models economically. And Mythos might just end up being released coincident with the availability of Rubins for inference.

TLDR: as labs shift their focus from training to inference, the costs of portability and the upside of co-design to maximize tokens per watt per dollar both rise. Portability is likely to begin decreasing as a result.

I think what I might have respectfully added to Jensen’s answer is that systems evolve under local selective pressures.

The evolutionary pressure in America is a shortage of watts so it makes sense for Nvidia to optimize, as an American company, for power efficiency and tokens per watt and stay on copper as long as possible. China has a surfeit of watts. Chinese AI systems are already taking advantage of this with the Huawei Cloudmatrix 384 and Atlas SuperPoD having an optical scale-up domain that is much larger than anything offered by Nvidia today at the cost of *much* higher power consumption and much lower tokens per watt. The networking primitives for this Huawei system are very different than those for Nvidia’s systems and a model that runs well on Nvidia will not run well on that system and vice versa. This means that if a Chinese ecosystem gets momentum, Chinese models might stop running well on American hardware. And when Chinese models run best on American hardware, America is in a better position as this gives America a degree of leverage and control over Chinese AI that it risks losing to an all-Chinese alternative ecosystem.

This architectural fork makes porting and distillation less effective and strengthens the pro-American national security case for selling China deprecated GPUs imo.

Also I will attest that I did not wake up a loser this morning.

SpaceX a clôturé son premier jour de cotation à 2 100 milliards de dollars, +19%. Tout le monde regarde le chiffre. Personne ne regarde ce qu'il price réellement.

Laissez-moi vous dire ce que le marché vient d'acheter, et pourquoi je pense que cette boîte vaudra 30 à 50 trillions d'ici 5 ans.

D'abord, le symbole. Cette IPO est un référendum. D'un côté, 20 ans de discours sur la décroissance, la sobriété, la redistribution, la fin de l'histoire gérée par des comités. De l'autre, un homme qui a dit "je vais rendre l'humanité multiplanétaire", que tout le monde a traité de clown, et qui vient de créer la plus grosse entreprise cotée de l'histoire en partant d'un entrepôt à El Segundo. Le marché a voté. Le wokisme avait des départements RH, SpaceX avait des fusées. Les fusées ont gagné.

Ensuite, la mécanique économique, parce que c'est là que tout le monde se trompe. Les analystes valorisent SpaceX comme une entreprise de lancement plus Starlink. C'est comme valoriser Internet en 1995 sur le marché du fax. Starship ne réduit pas le coût du kilo en orbite de 20%, il le divise par 100. Et chaque fois dans l'histoire qu'un coût d'infrastructure est divisé par 100, ce n'est pas le marché existant qui grossit, ce sont des industries entières qui naissent. Le coût du calcul divisé par 100 a donné Internet, le smartphone, l'IA. Le coût de l'orbite divisé par 100 va donner une économie spatiale complète.

Faisons la liste de ce qui devient rentable quand le kilo en orbite coûte le prix d'un billet d'avion. Les data centers orbitaux, avec énergie solaire continue et refroidissement gratuit, au moment exact où l'IA fait exploser la demande énergétique terrestre. La fabrication en microgravité de semi-conducteurs, de fibres optiques, d'organes imprimés impossibles à produire sous gravité. Le tourisme orbital de masse, puis les hôtels lunaires, qui passeront du fantasme au business plan exactement comme la croisière de luxe au 20ème siècle. Le transport point à point terrestre, Paris-Tokyo en 40 minutes. L'industrie minière des astéroïdes, dont un seul corps de classe M contient plus de métaux que tout ce que l'humanité a extrait depuis le néolithique. Et Mars en ligne de mire, pas comme destination touristique, mais comme le plus grand projet d'infrastructure jamais entrepris, avec tout ce que ça implique de demande en énergie, matériaux, robotique, IA.

SpaceX ne participera pas à ces marchés. SpaceX possède le péage d'entrée de tous ces marchés. C'est AWS, mais pour la civilisation. Apple vaut 3 500 milliards en vendant des rectangles de verre sur une seule planète. Le premier monopole d'accès à une frontière infinie à 30 ou 50 trillions dans 5 ans, ce n'est pas de l'exubérance, c'est une simple règle de trois sur l'expansion du marché adressable.

Et maintenant, la partie que je préfère. Ce futur n'a pas besoin de bureaucrates. Il n'y a pas de comité consultatif en orbite. Pas de commission Théodule sur Mars. Chaque dollar de cette nouvelle économie sera créé par des ingénieurs, des techniciens, des soudeurs, des pilotes, des entrepreneurs. Les diplômés en gestion de la norme vont devoir apprendre un métier utile, et franchement, c'est une excellente nouvelle pour eux aussi : construire est infiniment plus fun que contrôler.

Parce que c'est ça, le vrai signal d'aujourd'hui. Pendant 50 ans on nous a vendu un futur rétréci : moins d'énergie, moins d'enfants, moins d'ambition, gérer le déclin proprement. Et là, d'un coup, le plus gros actif financier du monde est un pari sur l'abondance, l'expansion et l'aventure. Le pessimisme vient de passer en position vendeuse sur lui-même.

Le futur sera méga fun. Il y aura des hôtels avec vue sur la Terre, des honeymoons en orbite, des gamins qui diront "papa, c'était comment avant les fusées réutilisables" comme on dit "c'était comment avant Internet". Et quelque part dans les années 2030, un humain marchera sur Mars en livestream devant 5 milliards de personnes, et ce jour-là plus personne ne se souviendra du nom d'un seul de ses détracteurs.

Achetez de l'optimisme. C'est encore sous-valorisé.

@ContrarianCurse Time to power plus turbine orders < supply where the backlog was. Nuke would make sense but it’s still min 5 yrs if countries could deliver nuke powerplants as fast as China.

Sofc and solar is obvious

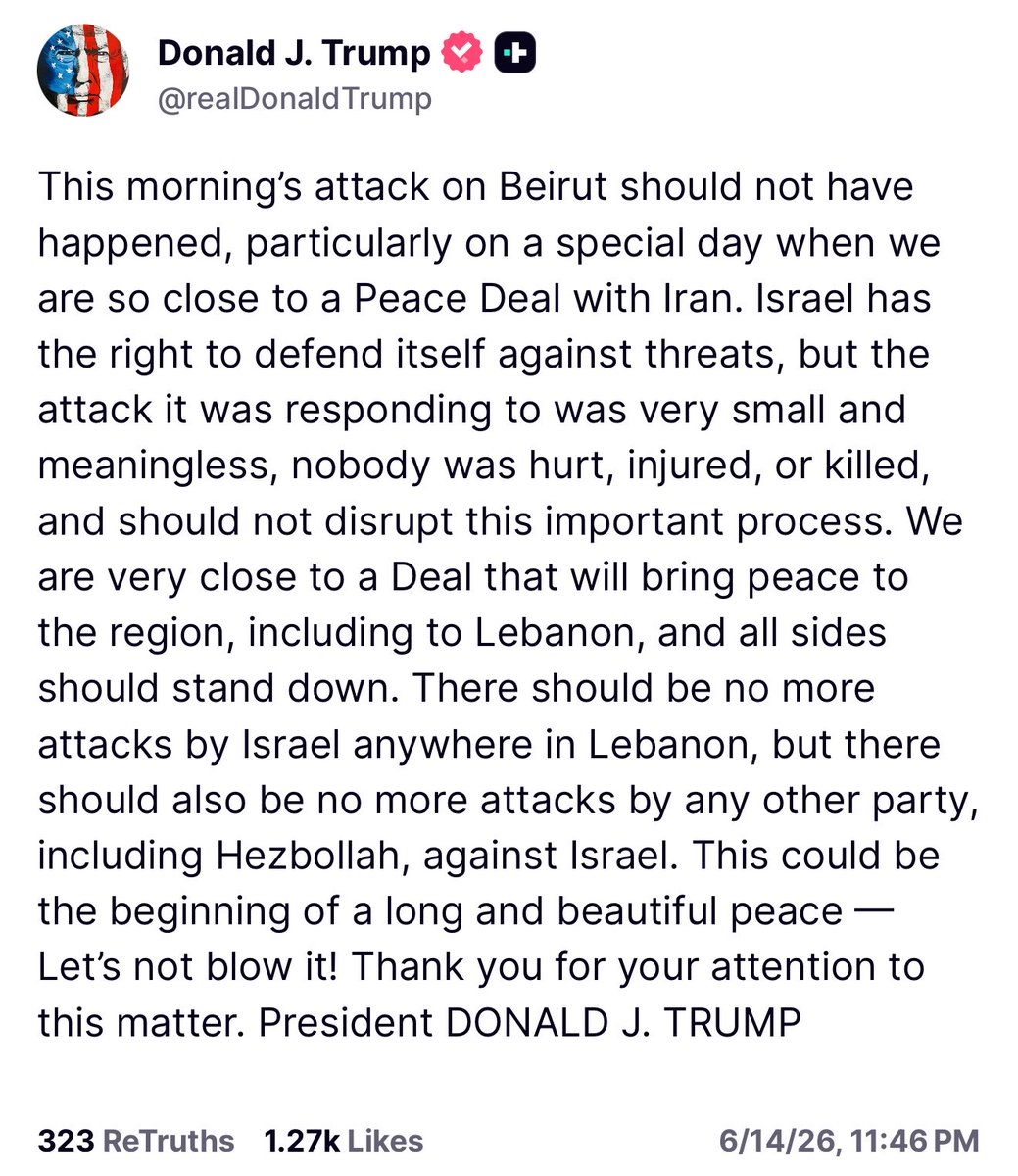

오늘 아침 베이루트에 대한 공격은 일어나서는 안 될 일이었습니다. 특히 우리가 이란과의 평화 협정에 이토록 가까이 다가선 특별한 날에는 더욱 그러합니다. 이스라엘은 위협에 맞서 스스로를 방어할 권리가 있지만, 이스라엘이 대응한 공격은 매우 사소하고 무의미한 것으로, 부상자도 사망자도 없었으며, 이 중요한 과정을 방해해서는 안 됩니다. 우리는 레바논을 포함한 이 지역에 평화를 가져올 협정에 매우 근접해 있으며, 모든 당사자들은 자제해야 합니다. 이스라엘은 레바논 어느 곳에서도 더 이상의 공격을 해서는 안 되며, 헤즈볼라를 포함한 어떤 다른 세력도 이스라엘에 대한 공격을 중단해야 합니다. 이것은 길고 아름다운 평화의 시작이 될 수 있습니다 - 이 기회를 날려버리지 맙시다! 이 사안에 관심을 가져주셔서 감사합니다.

도널드 J. 트럼프 대통령