My friends at North Central Animal Shelter have one girl hamster: Sauce! She is a happy cutie. She is a grayish white & a very adventurous fun loving girl. Staff love to watch her play & explore. Let’s find this cute girl named Sauce a rescue or forever home…Call 1-888-452-7381 #adopt

🚨 This trader extracts $4,800+/month on @PolymarketTrade with zero bots, zero alpha-leaks

Broke down the full strategy end-to-end.

REAL entries. REAL results.

He doesn't guess direction.

He exploits structural inefficiencies.

STRATEGY [3 mechanics]:

15-min BTC/ETH arbitrage

YES + NO < $0.97 → buy both sides

Math guarantees resolution at $1.00

No predictions. Purely mechanical edge.

Range spread betting

Limit orders across price ranges

One correct range → 300-900% ROI

Market-making on high-odds markets

Sell NO on <4% events: depegs, black swans

Entry 0.96–0.98. Win rate: 94%+

Win rate: 74% · Positions: 12 · P&L: +$4,830

Edge is not bet size — it is mechanics.

While others guess, the system prints.

My friends were popping bottles on a Friday night. I was in a dark room debugging a Python script for regional crop yields.

"You’re seriously betting on... rainfall data?" they laughed.

I didn't explain. Most people trade on "vibes" or whatever the top reply on a news thread says.

They see a 30¢ share and think it's a bargain. I see a 30¢ share and realize the market is blind to the LMSR algorithm.

The Logarithmic Market Scoring Rule is the secret engine of prediction markets. It’s the same logic that helps LLMs predict the next token, repurposed to price human belief.

The math is elegant, cold, and profitable:

C(q) = b * ln(Σ e^(qi / b))

95% of traders have never seen this equation.They don't understand that b (the liquidity parameter) dictates exactly how much the price moves per dollar.

The Play:

- Market Price: 0.28 (28% probability)

- My Model: 0.49 (49% probability)

-Edge: 21 cents per share.

While they were debating politics, I was hunting the delta.

Market resolved. +$5,800 profit while I slept.

The real alpha isn't "knowing" what will happen. It's knowing that the market’s pricing mechanism is lagging behind the raw data.

Most people play the player. I play the formula.

500$ → 500k$

I’ve been digging into this OpenClaw + Gemini 3.1 Flash setup for 15min BTC markets. Is the new release actually broken, or is this just the ultimate execution?

Let’s break down the mechanics of this profile:

> https://t.co/HkUUKaO3JJ

The "Cheat Code" isn't the model - it's the new Pluggable Context Engine. Old systems couldn't process wallet data fast enough. This new stack (GPT-5.4 + Gemini 3.1) allows for near-instant ingestion of @Polymarket on-chain flows.

The bot doesn't guess the direction. It follows the "Smart Money" then immediate-hedges:

Monitor: Tracks the Top 50 Polymarket wallets.

Trigger: If 3+ whales enter the same position within 10s.

Execution: Bot enters 2.3s before the price moves.

The Lock: Immediately buys the opposite side (hedge).

Example of a single cycle:

Whale buys YES @ 41¢

Bot catches it @ 42¢

Price pumps to 68¢ (Whale impact)

Bot buys NO @ 54¢ Total Cost: $0.96 | Payout: $1.00 | Profit: 4% Locked. Zero directional risk. Pure arbitrage on whale flow.

Executed: 187 hedged pairs

Avg Profit: 4.2% per cycle

Start: $800

Finish: $14,200

Biggest Single Cycle: +$890

The mentions of GPT-5.4 feel like a massive flex (or a hallucination of the future), but the logic is sound. Using LLM agents with high-speed context windows to front-run prediction markets is the new frontier.

If you aren't looking at pluggable context engines for your bots, you're playing a 2024 game in a 2026 world.

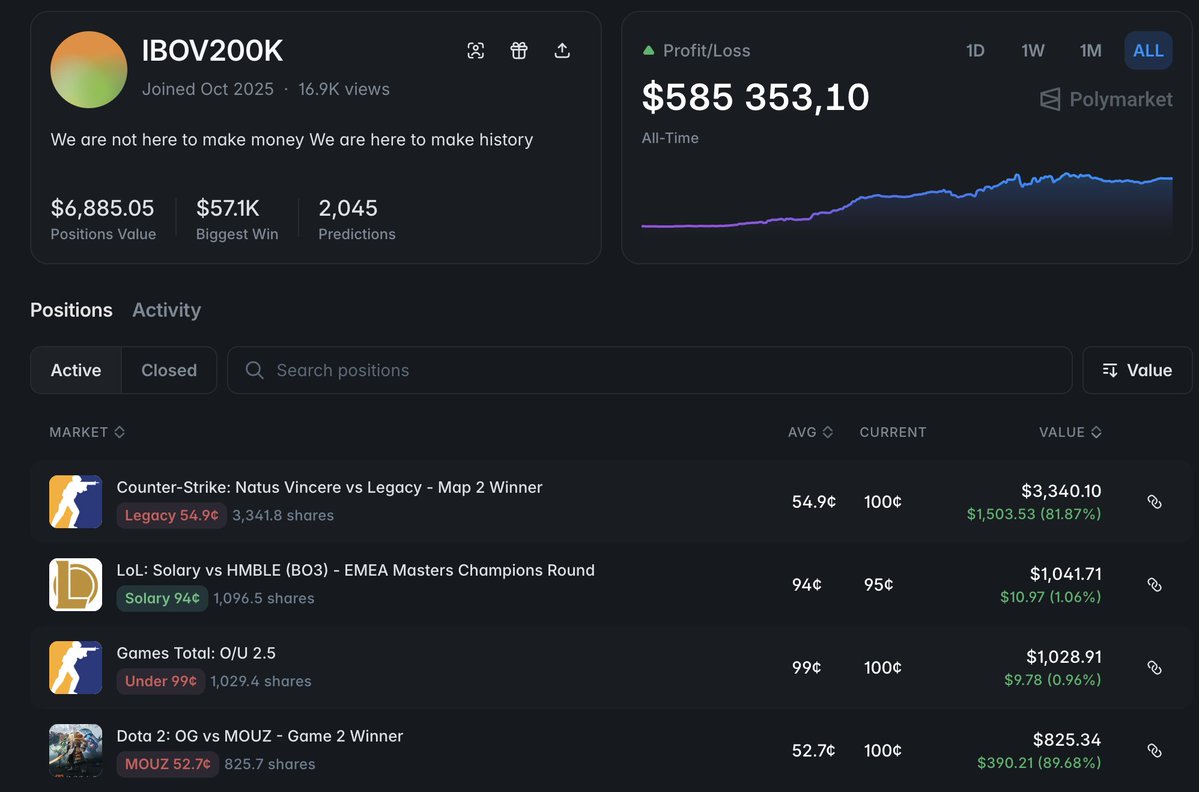

How I quanting a Goldman Sachs formula to extraction $400k on @Polymarket

Most people look at a price of 0.44 and ask "Is this cheap or expensive?"

I look at 0.44 and calculate the theoretical price.

Here is the alpha you’re missing:

Every market on Polymarket is actually a binary option. And binary options have a "fair value" based on math, not vibes.

I applied the Black-Scholes model for digital option.

The Formula: V = e^(-r * T) * N(d2)

Where d2 is: d2 = (ln(S / K) + (r - (sigma^2) / 2) * T) / (sigma * sqrt(T))

The Trade Breakdown:

Market Price: 0.44

Black-Scholes Model: 0.61

The Gap: The market was underpricing the probability by 39%.

I entered with a "small" $800 position. Market resolved at 0.98. Total: +$31,400 from a single play.

That’s the difference between a "trader" and a mathematician.

Profile that use such strategy:

> https://t.co/GvoMMCx9jw