Macroeconomia: Crédito bancário, Inflação, Pol. Monetária e Nível de atividade. Economista e Mestre em Economia pelo IE-UFRJ. MBA em Finanças pelo Coppead-UFRJ.

How do economists estimate an interest rate that exists only in theory? Our blog explores various approaches to modeling the “just-right” real interest rate that would prevail at full employment and 2% inflation https://t.co/NH0t3FdNz7

1/ Aprovação do governo Lula sai de 43% para 46% (+3pp) e desaprovação sai de 52% para 49% (-3pp) em um mês, segundo pesquisa Genial/Quaest. O saldo negativo que era de -9pp, agora é de -3pp.

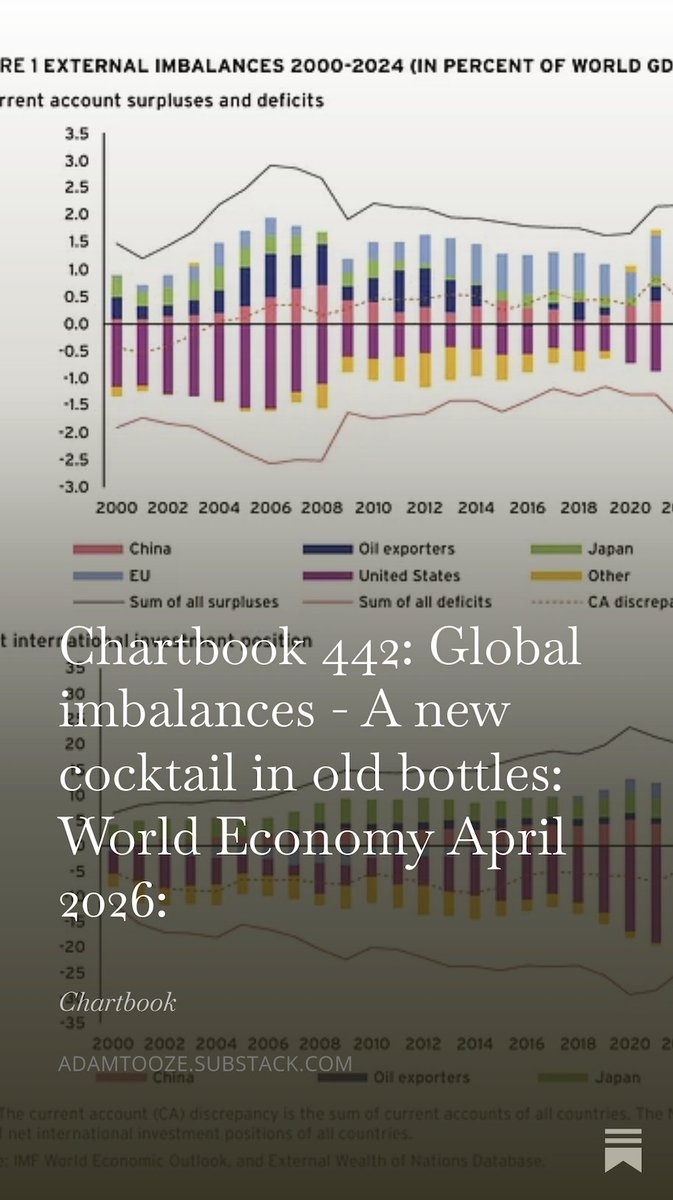

Global imbalances - April 2026. A new cocktail in old bottles.

The latest Chartbook newsletter just dropped.

Check it out here:

https://t.co/mMfEDcYvoJ

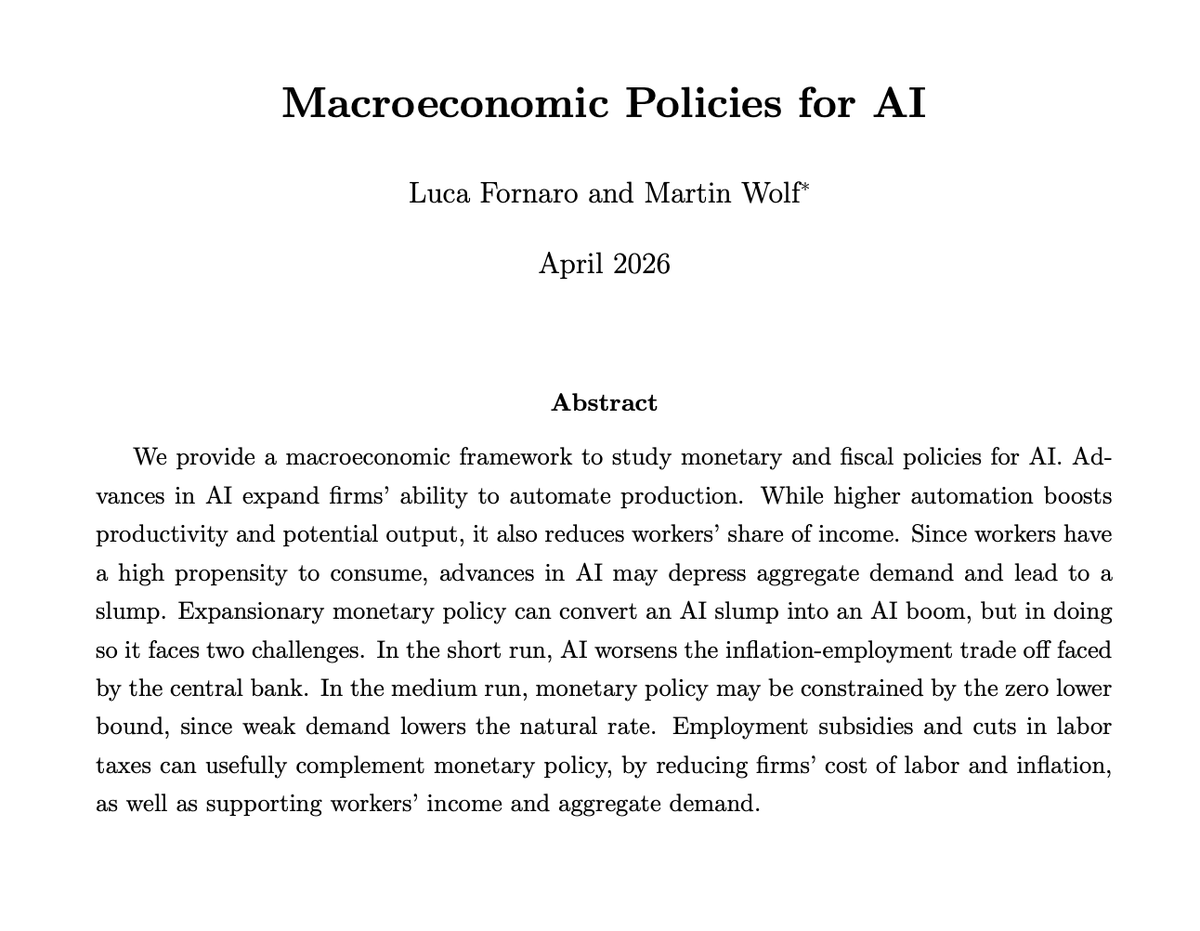

How will AI affect our economies? In this new paper, we argue that macroeconomic policies may determine whether we will face an AI slump or an AI boom. Spoiler: monetary policy alone may have a hard time sustaining an AI boom, employment subsidies/cuts in labor taxes can help.

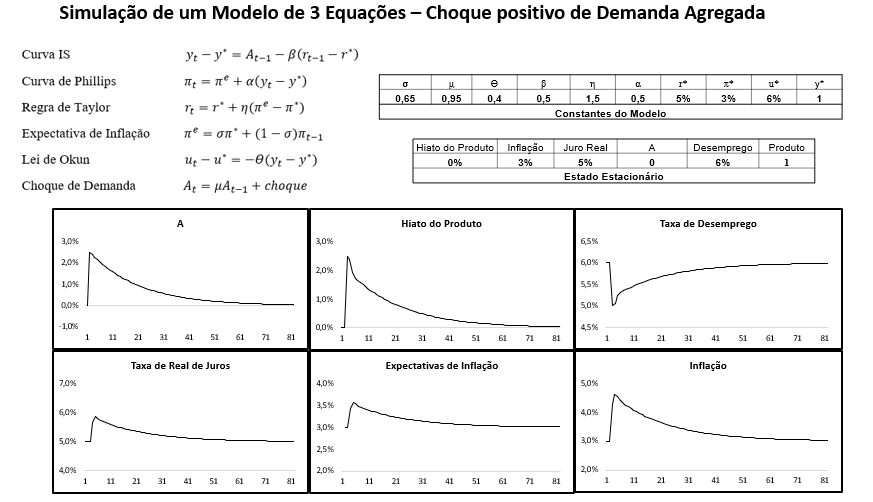

Com um modelinho macro deste tipo um aluno de segundo ano de graduação em Economia pode brincar de mudar os parâmetros e/ou os valores de equilíbrio das variáveis e, a partir de então, verificar o que acontece com as variáveis do sistema após um choque de Demanda Agregada.

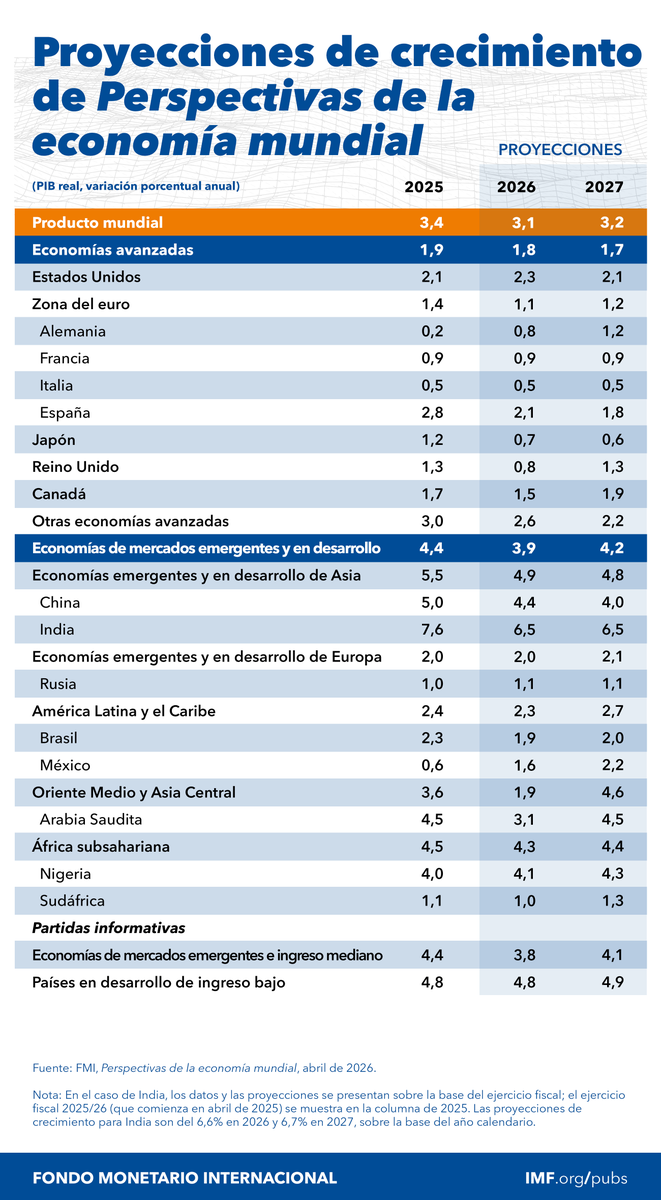

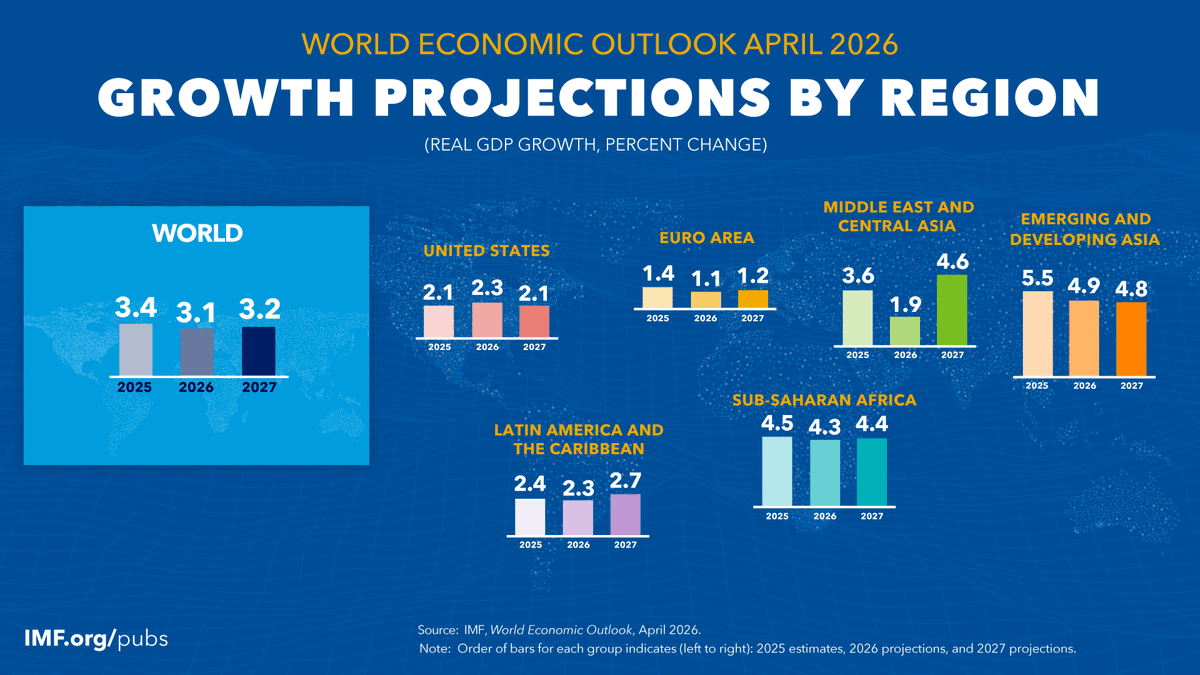

What’s ahead for the global economy in 2026? Growth is projected to slow to 3.1% in 2026. Inflation is set to rise to 4.4% before easing to 3.7% in 2027—a 0.6 percentage point upward revision relative to January, driven by higher commodity prices. https://t.co/5xMUE4sKMm

Super interesting!

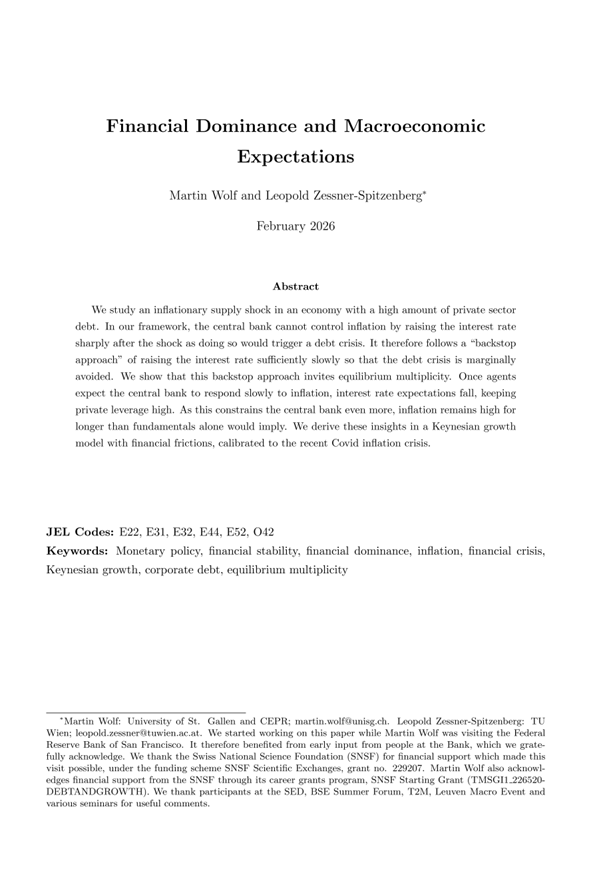

"Financial Dominance and Macroeconomic Expectations" by Martin Wolf and Leopold Zessner-Spitzenberg.

"We study an inflationary supply shock in an economy with a high amount of private sector debt. In our framework, the central bank cannot control inflation by raising the interest rate sharply after the shock as doing so would trigger a debt crisis. It therefore follows a “backstop approach” of raising the interest rate sufficiently slowly so that the debt crisis is marginally avoided. We show that this backstop approach invites equilibrium multiplicity. Once agents expect the central bank to respond slowly to inflation, interest rate expectations fall, keeping private leverage high. As this constrains the central bank even more, inflation remains high for longer than fundamentals alone would imply. We derive these insights in a Keynesian growth model with financial frictions, calibrated to the recent Covid inflation crisis."

https://t.co/cG11B8Nybz

@FtGraner@TonyVolpon@P_droMenezes@UOL A despesa acumulada em termos reais cresceu cerca de 15% entre 2023-2025. Mansueto falou que ‘deve crescer’ 20% em termos reais no acumulado dos 4 anos. E não ao ano.

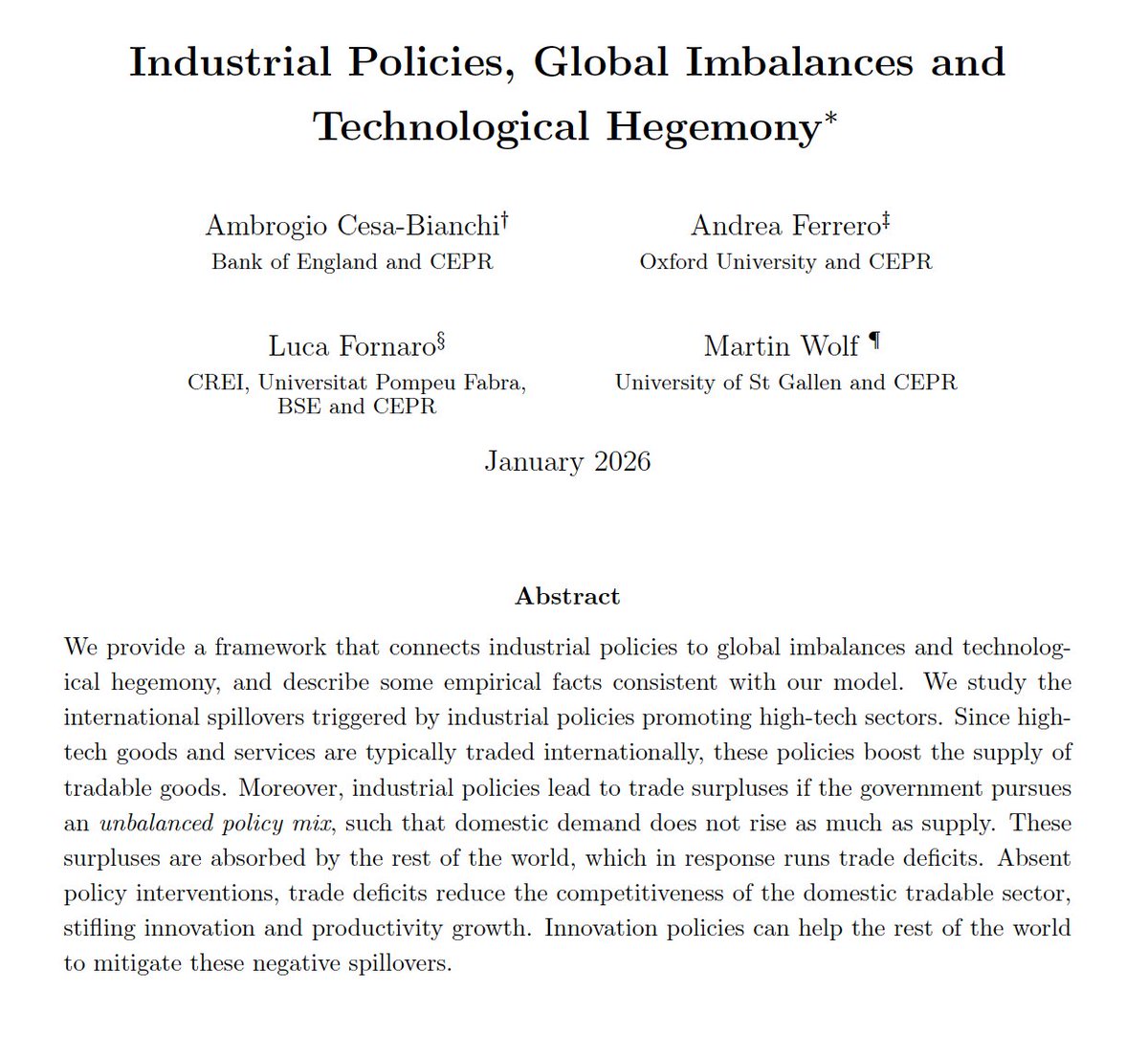

Industrial policies (IPs) are rarely connected to global imbalances. Yet, IPs are a key feature of many surplus countries. This new paper tackles three questions: Can IPs shape global imbalances? What are the spillovers to deficit countries? What policy responses are available?

In answer to some comments, and for those of you who are nerds: On the role of trade versus financial flows, see

/https://t.co/cdfABhBN4h

Discussion of what happens when investors want to reduce the share of dollar assets around p28. Dollar depreciation can be substantial.

Our January 2026 projections are in. So, what’s ahead for the global economy? Growth remains steady, supported by surging tech investment—especially in N. America & Asia—& favorable financial conditions. These tailwinds offset shifting trade policies & other uncertainties. https://t.co/zH3To1MItB

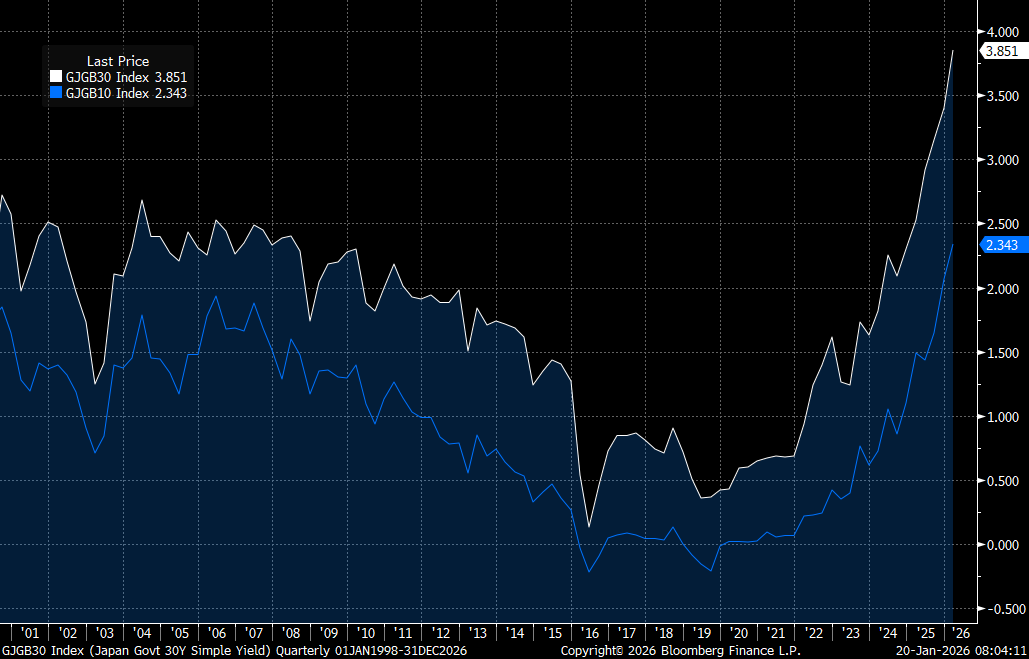

Is Japan’s bond shock signalling the end of global liquidity’s safety valve?

If markets have not been watching Japan, now is the moment. The relentless surge in long-dated JGB yields signals that one of the world’s most reliable liquidity backstops is fading, with consequences that extend well beyond Tokyo.

For decades, ultra-low Japanese yields have acted as a global liquidity anchor, encouraging capital to flow abroad in search of return and underpinning risk appetite across global bonds, equities, and credit. That anchor is now shifting, with Japan’s bond market seeing a sharp repricing, with 30-year JGB yields at 3.86% after jumping 25 basis points today and the 10-year rising 8 basis points to 2.34%. Both are modern records which are now accelerating.

The global implication matters more than the domestic politics. Higher JGB yields raise the opportunity cost of funding carry trades and overseas investments that for decades have relied on Japan as the world’s cheapest source of capital. As yields rise, capital is pulled back toward home, draining liquidity from global markets almost by definition. Policy options are limited: direct yield control would likely shift pressure straight to the currency, while more restrictive measures risk market distortion and loss of confidence. Whichever route the Bank of Japan takes, the outcome is the same — tighter global liquidity.

A Secretaria de Política Econômica do @MinFazenda divulgou a nova metodologia para estimar o PIB potencial e o hiato do produto, de autoria de Raquel Nadal, Lorena Brandão e equipe. O modelo incorpora, além do capital físico e humano, dois fatores naturais essenciais à economia brasileira: capacidade de geração de eletricidade e terra agriculturável. A abordagem também ajusta a taxa de participação considerando envelhecimento populacional e utiliza estimativas econométricas para determinar os pesos de cada fator, impondo retornos constantes de escala.

Os resultados mostram um PIB potencial mais estável e um hiato mais próximo de zero ao longo do tempo, quando comparados a outras estimativas. A medida da SPE também apresenta maior capacidade de prever núcleos de inflação sensíveis ao ciclo econômico. A análise revela ainda que, nos últimos anos, houve aumento relevante na produtividade do capital físico e retomada da produtividade total dos fatores, sustentando uma elevação gradual do crescimento potencial.

A metodologia reforça a importância de políticas voltadas à qualificação da força de trabalho, ao aumento da participação das mulheres no mercado e ao aproveitamento eficiente dos recursos naturais, elementos centrais para elevar o crescimento sustentável do país.

Links:

Relatório: https://t.co/9wFpRiDD9x

Apresentação: https://t.co/HAd97oHy46

Highly relevant! It's worth listening carefully to Jay Powell's speech at the Jackson Hole Symposium.

Let's highlight two elements in the speech:

"...with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance."

This might imply that Powell could support a 25 bps cut at the next meeting in September.

"...we returned to a framework of flexible inflation targeting and eliminated the "makeup" strategy. As it turned out, the idea of an intentional, moderate inflation overshoot had proved irrelevant."

It was unfortunate timing to adopt this "makeup" strategy. It is reasonable to eliminate it now.

The full speech can be found here:

https://t.co/6cAGWpWndy

YouTube:

https://t.co/lsSTuuymzl