Neocloud rally incoming...

It'll be even more aggressive this time.

> Just had a reasonable (and healthy) pullback the last couple of weeks

> Received many more catalysts, including $NBIS and $CRWV being included in the Nasdaq-100

We have until June 22nd before Nasdaq rebalance takes effect. Gives us exactly one week to plant our seeds before the real run begins.

Our thesis has gotten much stronger with these validations. Companies like $BTDR, $CIFR, $CLSK, $HUT, $IREN, $KEEL, $MARA, $WULF, $SLNH, and many more will benefit.

And there seems to be a few names that have pretty high asymmetry relative to its competitors...

Will share my research soon.

Obsidian trading journal = a system that studies every trade you make.

Works while you sleep.

Every pattern identified. Every edge validated. Every mistake documented so it never costs you twice.

After 30 days it knows your trading better than you do.

After 90 days it is preventing losses your past positions already predicted.

The people who build this tonight will never trade the same way again.

Read this and Bookmark it now.

si recién empezás con Claude Code, estos son los conceptos que más importan:

1) Agent Loop

2) Memory

3) Skills

4) Subagents

5) MCP

6) Hooks

entender los fundamentos te va a ayudar a aprovecharlo al máximo.

La corrupción y vileza de @DuniaLudlow son símbolo de Morena.

Sabe que @CitlaHM goza de la perversidad de golpear con bajeza:

Publica fotos de los hijos menores de edad de @AlessandraRdlv y muestra su mezquindad.

Con lo niños NO, @CitlaHM

$SPCX firmó con $GOOG un deal de USD 920M mensuales por cómputo. Y esto cambia la matemática del IPO del 12 de junio

Te explico qué pasó y qué significa sencillo👇

El deal según el filing oficial presentado el 3 de Junio

Google le paga a SpaceX USD 920M por mes desde octubre 2026 hasta junio 2029

A cambio accede a capacidad de cómputo de aproximadamente 110.000 GPUs NVIDIA en los data centers COLOSSUS

El contrato tiene cláusulas duras: si SpaceX no entrega los GPUs comprometidos antes del 30 de septiembre 2026, Google puede cancelar inmediatamente. Y desde 2027 cualquiera de las dos partes puede salir con 90 días de aviso

Ahora sumemos todo

- Anthropic ya pagaba USD 1.25B mensuales (deal hasta mayo 2029)

- Google suma USD 920M mensuales (hasta junio 2029)

Total: USD 2.17B por mes = USD 26B anuales de compute-as-a-service

Revenue contratado combinado: cerca de USD 75B hasta 2029

Para dimensionar: SpaceX facturó USD 18.7B en TODO 2025. Solo estos dos contratos le garantizan más de un año entero de facturación actual, por adelantado

Por qué esto es enorme para la empresa:

1) Valida los economics de COLOSSUS por segunda vez

Cuando Anthropic firmó, algunos dijeron "es un solo cliente, puede irse en 90 días". Ahora Google (que tiene sus propios data centers y sus propios chips TPU) decide alquilar cómputo a SpaceX

Si la empresa con la MAYOR infraestructura de cómputo propia del planeta te alquila capacidad, tus economics son competitivos. Punto

2) Diversifica el riesgo de cliente único

Era el riesgo más serio del segmento AI: dependencia total de Anthropic. Ahora hay dos clientes ancla, los dos de primera línea mundial

3) El segmento AI deja de ser solo promesa

Con USD 26B anuales contratados, el segmento que perdía USD 6.4B operativos en 2025 tiene un puente concreto hacia la rentabilidad

Por qué esto es enorme para el sector

Confirma la tesis del cuello de botella energético: en EEUU la red eléctrica no da abasto para los data centers de IA

Los hyperscalers prefieren alquilar capacidad ya construida antes que esperar 3 años por conexiones a la red. El que tiene gigavatios disponibles HOY tiene pricing power

Y SpaceX construyó COLOSSUS 1 en 122 días contra los 730 días promedio de la industria. Esa velocidad de construcción es el moat que nadie está valuando

La lectura crítica (porque siempre hay una)

El timing es demasiado perfecto: el deal se firmó el 5 de junio, el IPO es el 12 de junio

SpaceX necesitaba revenue contratado para justificar la valuación target de USD 1.75T. Conseguir USD 30B adicionales firmados una semana antes del pricing no es casualidad, es ingeniería de IPO

Y las cláusulas de salida siguen ahí: ambos contratos pueden cancelarse con 90 días de aviso desde 2027. Son USD 26B anuales que pueden evaporarse si COLOSSUS deja de ser competitivo

Cómo queda la valuación

En mi análisis del SOTP (suma de las partes) el segmento AI valía USD 350B en el escenario base. Con Google sumado, ese piso sube a USD 400-450B

El base case total pasa de USD 810B a aproximadamente USD 900B y zona atractiva de compra en 850B - 1.2T

A USD 1.75T (target del filing): el deal lo hace más defendible. El precio queda entre mi escenario bull (USD 1.300B) y mega-bull (USD 2.000B)

A USD 2.5T (precio pre-IPO en mercados privados): sigue sin cerrar. Incluso con Google adentro, el precio está por encima del escenario donde TODO sale perfecto

Mi conclusión

El deal con Google es la mejor noticia del prospecto desde el contrato con Anthropic. Sube el piso, valida el modelo, diversifica el riesgo

Pero no convierte una valuación agresiva en una valuación razonable. A USD 2.5T seguís pagando hoy lo que ARK Invest (la casa más bullish del mercado) proyecta para 2030

La empresa mejora. El precio sigue siendo el problema

Nada de lo que dije es recomendación de inversión. Es un análisis puramente educativo sobre el nuevo filing de SpaceX antes de su IPO del 12 de junio. Tienen análisis completo del balance en el tweet citado

Abrazo a todos

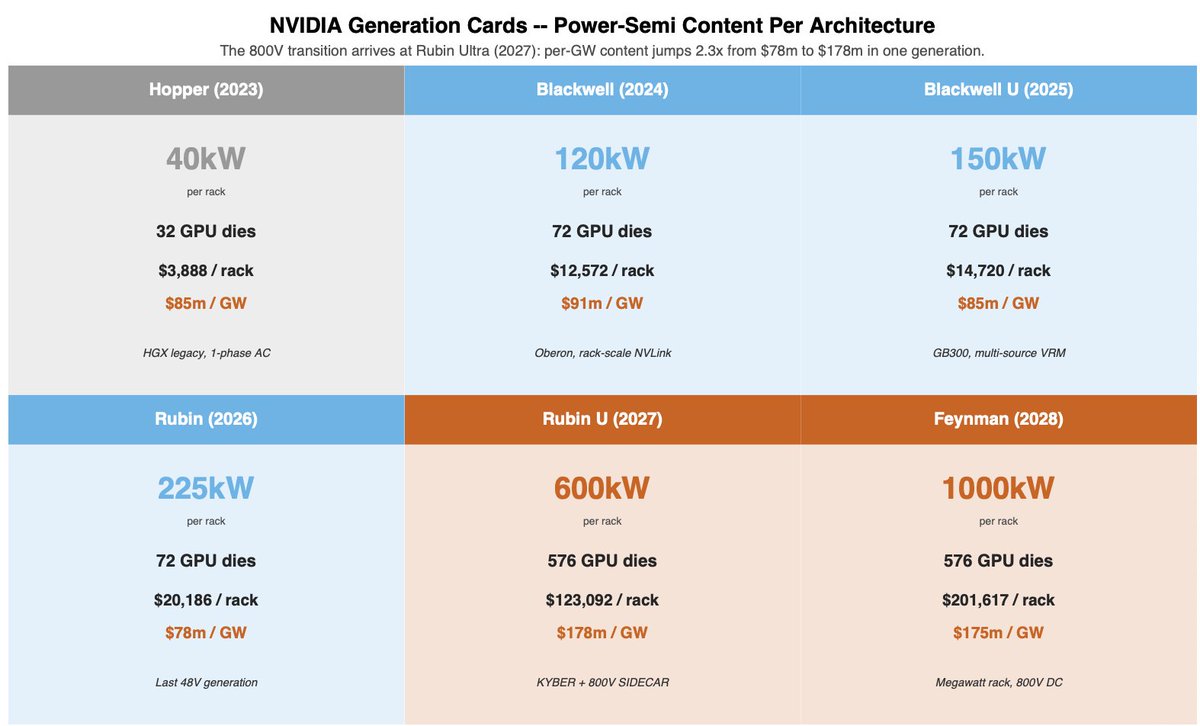

From 2023 to 2026 $NVDA kept adding more GPUs to each rack but the underlying power system stayed the same. Think of it like adding more appliances to your house without rewiring anything. You can do it up to a point.

Rubin Ultra in 2027 hits that point.

576 GPU dies per rack pulling 600 kilowatts is physically impossible to run on the old wiring. So NVIDIA splits the rack into two separate units. One rack holds all the GPUs. A dedicated sidecar rack next to it handles all the power conversion at 800 volts DC.

In the old system a 5kW power supply unit cost around $95 of semiconductor content. In the new 800V sidecar each unit is rated at 30kW and costs around $880 of semiconductor content.

The per-unit cost goes up nearly 10x because the chips required to handle 800V cannot be made from regular silicon. You need silicon carbide and gallium nitride, which are more advanced and more expensive materials.

Multiply that across an entire rack and you go from $20,186 of power semiconductors per rack at Rubin to $123,092 at Rubin Ultra.

That gap does not go to $NVDA. It does not go to the companies building the racks. It goes entirely to the chip companies supplying the power semiconductors.

Full report dropping Monday covering every name positioned for it. $IFX $MPWR $VICR $NVTS $STM $ON $TXN $ADI $POWI $DIOD $WOLF $AOSL

$IREN: The cloud market's dark horse

I bet most $IREN bulls are starting to get increasingly exhausted by the price action. I certainly am.

However, as long-term investors, we should see day-to-day price action as nothing more than noise.

$IREN is particularly "noisy," which makes it an especially difficult hold. Yet in times like these, it's important to step back and refocus on the company's fundamentals rather than let price action sway one's emotions.

And the way I see it, $IREN's competitive standing is rapidly improving.

I recently came across an interesting research report by Goldman Sachs that highlighted the discrepancy between planned data center capacity and realized capacity.

Out of the ~18 GW planned to be commissioned over the past 6 quarters, only about ~11 GW actually got built.

Not only is the gap between planned and realized capacity rapidly widening, but the rate at which new capacity is coming online has actually declined over the past couple of quarters.

Much of this discrepancy comes down to power continuing to be a major bottleneck.

As grids get more and more constrained with lead times reaching 5+ years, many developers are moving toward behind-the-meter (BTM) generation (on site power generation), circumventing the need for grid connectivity.

Yet that comes with its own set of problems and bottlenecks. The end result is an increasing amount of delays and outright project cancellations.

This industry backdrop plays directly into the hands of $IREN, which now has 5.8 GW of secured grid-connected power across global jurisdictions.

The only reason the industry is switching toward BTM is that it's the only option if you don't want to wait in multi-year queues to secure grid connections. But don't get it twisted, grid-connected power remains the preferred option.

$IREN is in a unique position to capitalize on this structural bottleneck and become one of the few cloud providers that can actually bring on 5+ GW of compute capacity over the coming years.

I'd even go as far as saying that this structural advantage is the primary reason the $NVDA partnership came to be.

While $NVDA undoubtedly remains king of the hill, even they face a real dilemma that could cause cracks in their growth trajectory.

On the supply side, they have to come to terms with the fact that the gap between planned and realized data center capacity is widening, while the trend of new capacity coming online is actually decelerating.

This is the issue I just flagged, and it could act as a potential growth bottleneck for $NVDA, since fewer builds means fewer GPU sales.

Layered on top of this is the demand side. It's perfectly clear that demand for $NVDA's AI hardware remains insatiable. However, when looking closer, it's also apparent that competition is increasing.

Pretty much every hyperscaler is working on their custom chips (TPU, Trainium, Maia, MTIA), and not exclusively for internal use cases anymore, but increasingly to service the compute needs of large AI labs. Anthropic alone has signed deals worth billions for Google TPU and AWS Trainium capacity.

Then you obviously have the likes of AMD and Cerebras directly competing against the AI giant, trying to claim market share.

Taken in aggregate, these two issues could gradually lead to a growth problem for $NVDA if not addressed.

This is exactly where $IREN comes in.

They've got the largest secured power portfolio of any neo-cloud at 5.8 GW and growing fast, they develop 100% of their data centers themselves, and they're not building competing silicon.

That makes them the most reliable demand outlet $NVDA can partner with at scale.

The Sweetwater partnership, positioning the 2 GW campus as a "flagship DSX deployment," isn't $NVDA doing $IREN a favor. It's $NVDA solving its two biggest problems at once.

I'm sure you know the popular saying that "history never repeats, but often rhymes." I think today's neo-cloud market is somewhat similar to the dot com era search engine war.

Back then, the front-runners leading the race were AltaVista, Excite, and Yahoo, while Google was a latecomer that ultimately came out on top.

Today, the vast majority of investors in this space are declaring either $CRWV or $NBIS the obvious winners in the race to become the next hyperscaler.

However, I believe the real dark horse that the mainstream doesn't give much credit to is $IREN.

I believe they have all the ingredients to leapfrog every competitor in a short amount of time, in large part due to their structural advantages and pursuing the right long-term strategy from the get go.

The asset-light model, which both $CRWV and $NBIS have been leaning into, doesn't work well in capital-intensive industries, at least not over the long run.

It's somewhat of an oxymoron, since it seems intuitive that one way to circumvent some of the CapEx burden is to outsource from colocation providers.

Yet that approach leaves you with less control, less flexibility, and ultimately higher costs in aggregate in the form of operating expenses (the landlord also has to earn $).

I studied the Bitcoin mining industry for years, and the asset-light model was once a popular strategy around the 2021 bull market. While it proved to be a strong growth lever, it ultimately ended up being a disaster for anyone who adopted it.

Companies like $MARA are the perfect example.

$MARA heavily adopted the asset-light model and grew to become the largest $BTC miner, yet ended up as one of the most unprofitable public miners of all, leading to significant value destruction for shareholders over time.

Once it became obvious that asset-light wasn't a sustainable strategy, $MARA tried to pivot away from it by increasing self-deployments. But developing infrastructure in-house is a much harder discipline to master, and you don't simply switch into it overnight.

$IREN ultimately won the mining race last cycle by doing the exact opposite of $MARA from the start.

They developed all of their data center infrastructure in-house, backed by a seemingly unlimited pipeline of secured power, which ended up making them the fastest growing and most profitable miner of all time.

While the cloud sector has significant differences from the mining industry, the primary drawbacks of the asset-light model carry over.

Over time, it will become obvious to Wall Street and the broader market that this strategy sounds great in theory, but in practice leads to a stack of operational issues and severe margin compression.

Out of the two current front-runners, $CRWV and $NBIS, I think Nebius will do better. They've at least started moving toward a more diversified mix of self-owned capacity rather than purely relying on hosted colocation, which is the right direction even if they're still early in that pivot.

That said, as the $MARA example showed, developing in-house gigawatt projects at scale is not something you learn overnight.

It's clear to me that a player like $IREN, which has been building this discipline from day one, has the most realistic pathway toward sustained, profitable growth in this space.

In my view, $IREN is the dark horse that will end up winning the race. Thus overthinking today’s price action wouldn't do me any favors.

Cheers guys, have a great weekend! ✌️

Anthropic engineer:

"You're not supposed to prompt Claude. You're supposed to build a system that prompts itself."

this is one of the best workflows I've seen in a long time

in this video he breaks down exactly how most people are using Claude:

- the 14% you lose to CLAUDE.md before typing a word

- the plugins that 95% of users have never installed

- the caching setup that keeps it at 95% hit rate and almost free

- why starting every chat from zero is the slowest way to use Claude

if you've been using Claude for more than a month and never left the chat window, you've been using one project when you could be running a team of them

instead of another show tonight, watch this

make sure to bookmark it before it gets lost in your feed

full guide in the article below

El mejor momento para aprender a desplegar tu propia infraestructura de IA fue hace 2 años.

El segundo mejor momento es ahora.

Los servicios en la nube van a subir precios en cuanto la gente dependa de ellos.

Ya lo hicieron antes.

La alternativa siempre estuvo en GitHub.

Casi nadie miraba.