The AI Revolution is reshaping South Korea’s economy:

The value of South Korea’s exports rose to a record ~$270 billion in Q2 2026.

This comes as South Korea's exports jumped +59.5% YoY in June, an acceleration from the already strong +53.4% gain in May.

Semiconductor exports continue to lead the gains, surging +199.5% YoY, to $44.8 billion, driven by strong AI and data center investments.

Shipments of computer-related products soared +308.8%, while petroleum products rose +49.8%.

AI demand has made South Korea into an economic powerhouse.

Bloomberg: "The Silicon Data LLM Token Expenditure Index, which tracks what users pay for AI tokens, is down almost 20% from a high in May after nearly doubling since its inception in December. The gauge is the cleanest read anyone has on the $700 billion-plus capex boom that has done the sector’s heavy lifting. For stock investors, that could be flashing a warning that AI companies are losing pricing power with increasingly cost-sensitive customers, and that expectations for an eventual AI bonanza could prove misplaced.

'There are increasing reports that users of AI solutions, priced in tokens, are having to restrain unlimited use due to high costs,' said veteran investor Louis Navellier. 'The chatter that OpenAI is pushing back its IPO to next year is seen as a sign that, currently, profitability remains a problem.'"

As I warned back in my December report on "GenAI & Productivity" (https://t.co/kEx5Z4BbRz):

"GenAI appears to be transitioning tech giants from the most-profitable business models in history to business models more akin to industrials...Meanwhile, while there’s a lot of speculative fear about how a single LLM could rise to dominance and what that could mean for economic, societal, and political stability, we believe the bigger concern for investors today is how relative model parity could compromise pricing power. Tech giants have thrived on monopolies and duopolies for a decade or more. Now, they’re in an LLM arms race where it’s unclear when or even if ever leadership will be sustainable."

Learn more about Sage Road Research here: https://t.co/Wgwz2xmY1y. Interested in subscribing? Message me.

Bloomberg link: https://t.co/dmiMU860Oh

🚨The Buffett Indicator suggests US stocks have rarely been this expensive:

The ratio of total US stock market value to GDP is up to a record ~230%.

This is more than double the long-term average of 89%.

By comparison, the 2000 Dot-Com Bubble peaked at ~140%.

Nearly every major valuation metric for the S&P 500 now sits at or near a record high, with the price-to-earnings ratio probably the only exception.

Is the market priced for perfection?

The Economist: "Talkie, a model trained only on text from before 1931, thinks God is extremely important and is “very proud to be a citizen of Great Britain”. It is a bigger believer in law and order than any frontier model we tested."

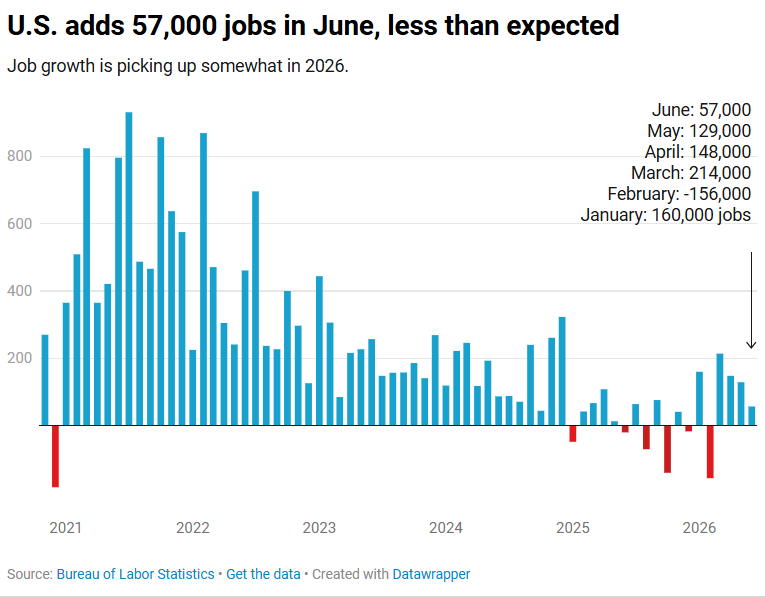

JUST IN: A disappointing jobs report. The US economy added 57,000 jobs in June (below expectations of 115k). Hospitality jobs decline by -61k. Plus, April and May were revised lower by -74,000.

The unemployment rate fell to 4.2% --> the lowest in a year, but mainly due to a big drop in people job hunting.

The bad news = Wages aren’t keeping up with inflation. Wage gains were 3.5% in the past year, which is below ~4% inflation.

From the FT: "The key lesson from the end of the dotcom bubble is that the main risk will probably come from deterioration in the cash flow of the AI sector’s prospective customers. So, investors should be more concerned about any deceleration in the earnings and cash flow of the potentially heavy AI user sectors, such as financials, manufacturers, media, transportation, education and healthcare."

As I've written often in one form or another in my reports since launching Sage Road almost a year ago (https://t.co/Wgwz2xnvR6), I believe the market’s myopic fixation on the builders of the AI revolution has led to widespread neglect of the beneficiaries of AI’s capabilities. This matters not only to understanding how ROI will manifest and define winners/losers across sectors, but also the willingness and ability of enterprises to subsidize extraordinary AI CAPEX.

FT link: https://t.co/edwWyBYrnX