Thank you @MikeCrapo for asking the tough questions to @GaryGensler but I you showed your tell commissioner. You went white when asked about Mmtlp and you pretending not to know know the #MMTLP ticker was hilarious. You have been informed earlier this month. Pathetic!

⚠️Not Legal Advice

What if DTCC fails to turn over information?

Adverse Inference

The doctrine is essentially:

“The party who failed to produce evidence cannot benefit from the absence of that evidence.”

For example, if the Trustee presents:

Nasdaq order data

FINRA short-sale data

Broker-dealer records

ShareIntel analysis

Trading patterns

Expert testimony

and shows those sources point toward a conclusion…

Then the absence of DTCC records may actually strengthen the Trustee’s position.

A court could effectively conclude:

“The Trustee’s reconstruction is the best available evidence because the more complete records were not produced.”

That’s very different from automatically accepting the estimate, but the practical result can sometimes be similar.

📣📣DTCC IS TRYING TO RUN OUT THE CLOCK ⏰️

MMAT MMTLP Bankruptcy subpoenaed the DTCC over a year ago. They still have not fully complied with the records that were requested in the subpoena.

The Trustee has contacted them many times.

Now, a hearing is set for tomorrow, June 16th, 2026, at 9.30 am.

Let's see what the Judge has to say about their noncompliance.

If you have nothing to hide, supplying the records shouldn't be a problem.

DTCC IS HIDING THE CRIME‼️

📌 Updated June 13, 2026

MMAT / MMTLP / TRCH

Meta Materials Inc. Chapter 7 Bankruptcy

The next key dates are now on the board.

Most important:

🚨 June 16 — 9:30 AM PT

Remote Zoom hearing regarding DTCC subpoena compliance and protective order administration.

This does not mean the Court has ruled against DTCC yet.

It means the Trustee successfully got the issue placed on an expedited schedule after raising concerns about outstanding production and time-sensitive discovery.

The focus remains the data.

And the clock is still ticking.

#MMTLP #MMAT #TRCH #DTCC #FINRA

📌 MMAT | MMTLP | TRCH

Meta Materials Inc. Bankruptcy

Case No. 24-50792-gs (Chapter 7)

Document No. 2870

Filed: June 12, 2026

⚖️ Summary:

Judge Gary Spraker granted the Trustee’s request for shortened time, allowing an expedited hearing regarding DTCC subpoena compliance and protective order administration. The order does not decide the DTCC dispute itself—it simply puts the matter before the Court on an accelerated schedule.

🚨 HEARING SCHEDULED:

📅 June 16, 2026 💥

🕤 9:30 AM PT

💻 Remote Zoom Hearing

⚠️ Not Legal Advice. For informational and entertainment purposes only.

MMAT MMTLP TRCH

🚨WHY DOESN’T THE TRUSTEE PURSUE A MOTION TO COMPEL?🤔

⚠️ Not legal advice - for discussion purposes.

A motion to compel usually works best when:

•The court knows exactly what is missing.

•The producing party (DTCC) has had a chance to explain why it hasn’t produced it.

•The judge understands any technical, confidentiality, or protective-order issues.

•The moving party can show a clear record of efforts to resolve the dispute.

The Trustee is essentially telling Judge Spraker:

“We’ve been working on this for over a year, exchanged 40+ emails, production is still incomplete, we’re running into statute-of-limitations concerns, and we need the Court involved now.”

Then she specifically states one of her goals is:

“…set a schedule and parameters for any motion to compel, if necessary.”

⸻

The filing identifies three objectives:

1️⃣ Force DTCC to explain itself

The Trustee wants:

“concrete information from DTCC about a date by which it will produce the Correspondent Clearing Data”

In plain English:

“Tell us exactly when we’re getting the data.”

⸻

2️⃣ Resolve Protective Order Problems

The Trustee specifically references:

“ECF No. 2601”

which is the protective-order framework.

That suggests there may still be disagreements regarding:

confidentiality designations

who can view data

how it can be stored

how it can be used in litigation

A status conference is often faster than filing a lengthy compel motion when the dispute may be procedural rather than outright refusal. ⬅️

⸻

3️⃣ Prepare for a Motion to Compel

The filing expressly says:

“set a schedule and parameters for any motion to compel, if necessary”

That tells me the Trustee has not yet concluded DTCC is refusing outright.

Instead:

Current Position

Production incomplete ✔️

Delays occurring ✔️

Missing data identified ✔️

Court intervention needed ✔️

But

Not yet at “DTCC has definitively refused to comply.”

⸻

Why This Might Be Strategically Better

If the Trustee files a motion to compel today, DTCC could respond:

“We’re still producing.”

“We’re working through confidentiality issues.”

“The Trustee never asked the Court for assistance before filing.”

By requesting a status conference first, the Trustee creates a record showing:

cooperation

patience

multiple follow-ups

attempts to resolve informally

urgency because of limitations concerns

That record makes a later motion to compel much stronger.

⸻

⏰⏰⏰⏰⏰⏰⏰⏰⏰⏰⏰⏰⏰⏰

This paragraph is probably the biggest headline:

“Continued delay in DTCC’s production of the Correspondent Clearing Data risks prejudice to the estate, including exposure to statutes-of-limitations constraints on potential litigation…”

That is unusually direct. 🎯

The Trustee is essentially telling Judge Spraker:

🚨 “I may have claims to investigate, but I need this DTCC data before limitations periods become a problem.”

That is stronger language than we’ve seen in many prior filings. 👀

⸻

This filing may signal:

Near-Term

The Trustee wants Judge Spraker to quickly get DTCC and the Trustee’s team in front of him and explain:

What has been produced?

What remains outstanding?

Why is it outstanding?

When will it be produced?

Next Step

If DTCC cannot provide satisfactory answers or a firm production schedule, then a formal Motion to Compel becomes much more likely.

In other words:

📌 This filing looks less like an alternative to a motion to compel and more like the Trustee positioning herself to file one with maximum leverage if DTCC still doesn’t deliver. 💥

Not legal advice — just an interpretation of the docket and bankruptcy procedure. ⚖️📄

MMTLP NBH MMAT Meta Materials #SECfraud#FINRAfraud#FOIAdenials

Well, well, well, the hits continue to drop from the SEC.

Peirce’s Speech Quietly Confirms the Core MMTLP Thesis.

Her remarks, especially on statutory limits, overreach, 15c2‑11 misuse, CAT failures, and inconsistent enforcement, directly support the legal and factual arguments that:

1. MMTLP trading should never have been allowed.

2. The halt was executed without statutory authority.

3. FINRA and the SEC selectively applied rules to cover prior failures.

4. FOIA stonewalling is part of a broader pattern of opacity she criticizes.

5. The SEC’s own Commissioner believes the agency has exceeded its authority in exactly the ways MMTLP exposed.

This speech is not just philosophically aligned, it is factually aligned with the regulatory failures at the heart of MMTLP.

Maybe we may now have a commissioner that will state "We need to fix it!" A Nearly 30 years and we don't know how to address the MMTLP fiasco created by FINRA and the SEC.

What say you?

I say focus on the work! There is so much out there.

Focus...

https://t.co/e1iOfvsGHU

Intersting, I was just asked to provide such a list of people at the @SECgov I thought were COMPLICIT in The MMTLP Fiasco and the WEAPONIZATION of the FEDERAL AGENCY against innocent citizen investors.

They cannot stop what is coming...#LockIn

MMTLP MMAT TRCH NBH

MMTLP MMAT TRCH NBH

Maybe one should FOIA the communications of MS. Karina Dorin...

"Karina Dorin is a Staff Attorney in the Division of Corporation Finance at the U.S. Securities and Exchange Commission (SEC). In her role within the Office of Energy and Transportation, she is responsible for reviewing corporate filings, such as registration statements and prospectuses, to ensure compliance with federal securities laws."

MIGHT the responses tell us what she said to NBH to get them to withdraw the S-1 Sub Rights Offering the FIF Member Firms were so afraid of....hmmm.

Anyone investigating The MMTLP Fiasco may surely want to interview MS. DORIN in addition to David Saltiel, Erik Gerding and Karl Hiller. #RICO #Conspiracy

@SECGov@USTreasury@SecScottBessent@DirectorPulte@FBIDirectorKash

They cannot stop what is coming...

Funny thing about the NewCo S1 comment record.🤔

SEC feedback looks pretty cordial, right up until the FIF

expresses concern.

🚨After that?

Different story.🚨

Draw your own conclusions.

Some new FOIA docs tell the story…🧨🧨🧨

$MMTLP #MMTLParmy $MMAT

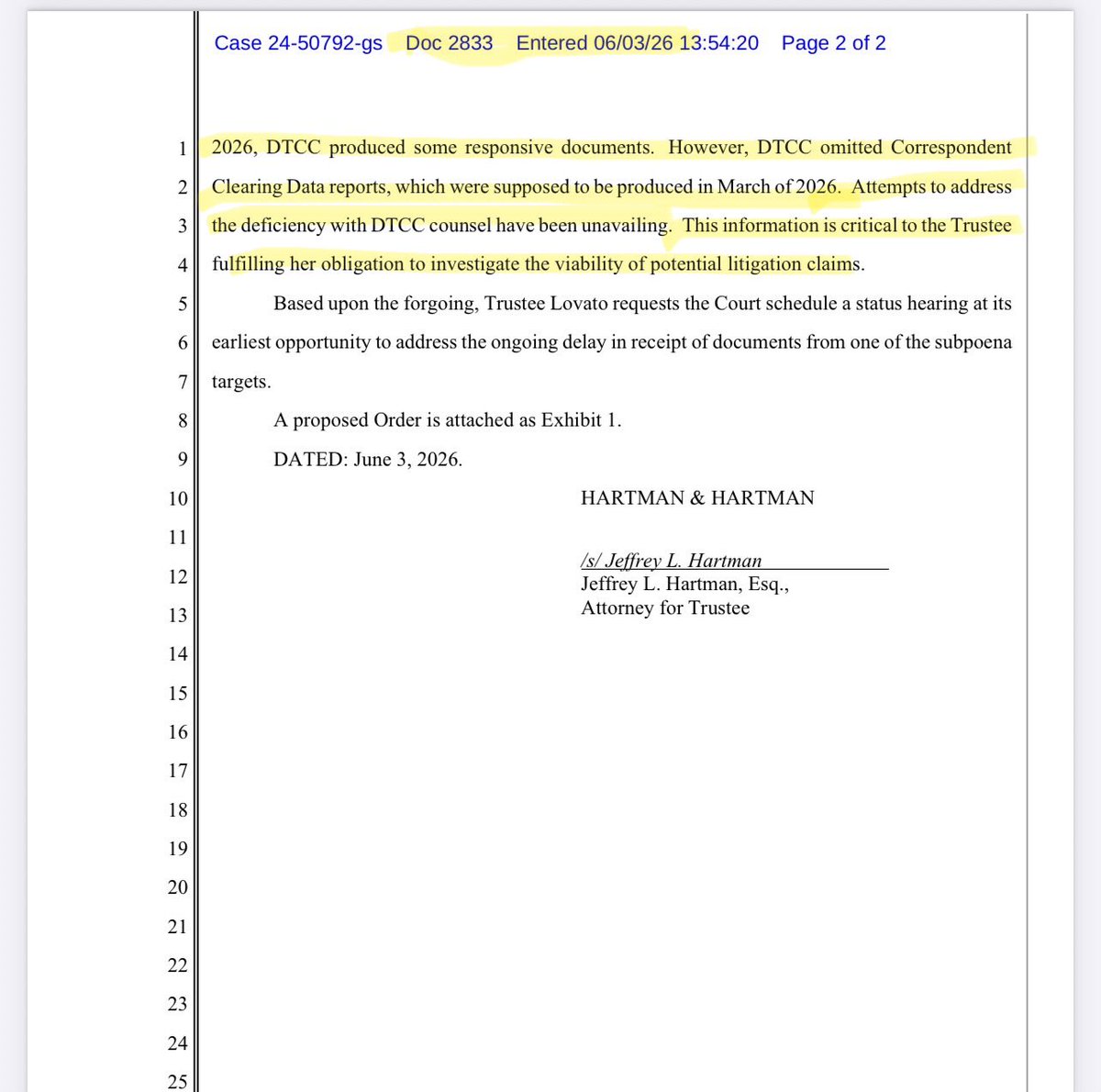

🦋 MMAT | Meta Materials Inc.

Case No. 24-50792-gs (Chapter 7)

📅 Filed: June 3, 2026

📄 Docket No. 2833 – Ex Parte Application to Set Status Hearing

⚖️ Layman’s Summary

Trustee Christina Lovato is asking Judge Spraker to schedule a status hearing because DTCC has allegedly not provided all of the subpoenaed records the Trustee believes were due months ago.

🔥 Key Quote

“DTCC omitted Correspondent Clearing Data reports, which were supposed to be produced in March of 2026.”

🚨 Why It Matters

The Trustee tells the Court:

“This information is critical to the Trustee fulfilling her obligation to investigate the viability of potential litigation claims.”

In plain English:

👉 The Trustee believes important DTCC data is still missing.

👉 Efforts to resolve the issue privately have failed.

👉 The missing information is important to determining whether litigation claims exist.

👉 The Trustee wants the Court involved to move the process forward.

📌 Bottom Line

This filing suggests the MMAT investigation is still active, the Trustee is still seeking additional DTCC records, and she believes those records are important to evaluating potential legal claims.

⚠️ Not Legal Advice.

Keeping the FLAME alive for #MMTLPfiasco

Seems that the mouth pieces for Wall Street are feeling the flames...

Good.

Next up, FINRA's former board member and Barack Obama's former White House counsel, Kathryn Ruemmler, along with former Clinton campaign and former SEC Chairman, Gary Gensler, ALL OF WHOM were on deck during this clear sabotage of META MATERIALS through the naked short selling of #MMTLP

@palikaras@busybrands@JunkSavvy@SECGov@EdMartinDOJ@PeterTicktin

Part 1 of 2

MMAT MMTLP NBH TRCH

⚖️ META MATERIALS (MMAT) Bankruptcy

Case No. 24-50792-gs

Document 2831

Filed June 2, 2026

Trustee Christina Lovato’s Response to Danielle Spears’ Motions

⚠️ Not Legal Advice

⸻

🦋 Two Quotes That MMAT / MMTLP / NBH Shareholders Will Likely Focus On

1️⃣ Shareholder List / Claims Agent / Shareholder Rights

From Page 6:

“The Trustee has requested a comprehensive list of shareholders from the transfer agent. Once that information has been received, the Trustee will determination [sic] next steps, i.e., incurring the expense to engage a claims agent. It is not the Trustee’s intention to prejudice the rights of any creditor or shareholder. At the appropriate time, the Trustee will seek authority to establish a bar date.”

Why This Matters

This is one of the clearest statements yet that:

✅ The Trustee is seeking a complete shareholder list.

✅ A claims agent is being considered.

✅ The Trustee expressly states she does not intend to prejudice shareholder rights.

✅ The Trustee anticipates eventually seeking a bar date process.

⸻

2️⃣ FINRA and the U3 Halt

From Page 7:

“FINRA and the U3 halt. This issue was a significant part of the Texas Litigation previously addressed. After more than a year and two opportunities to make her case against FINRA and others (including Greg McCabe), Ms. Spears’ case was dismissed with prejudice. What Ms. Spears ignores is that FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares. Ms. Spears apparently believes the Trustee and her professionals need her lay-person expertise.”

Why This Matters

Many shareholders have focused on FINRA and the December 2022 U3 halt.

The important takeaway here is not the criticism of Spears.

The significant statement is:

“FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares.”

That is a direct statement from the Trustee confirming that FINRA remains a discovery target in the MMAT investigation.

⸻

📝 Comprehensive Layman’s Summary

What Is This Filing?

This filing is Trustee Christina Lovato’s response asking Judge Gary Spraker to deny several motions filed by Danielle Spears before the June 16, 2026 hearing.

⸻

Trustee’s Core Position

The Trustee argues that individual shareholders cannot:

❌ Direct the investigation

❌ Demand investigative materials

❌ Control litigation decisions

❌ Force the Trustee to pursue particular claims

❌ Obtain internal work product or litigation strategy

The filing states:

“A putative shareholder cannot broadly intervene into, or seek to direct, a trustee’s administration of a chapter 7 estate.”

⸻

Standing

The Trustee acknowledges the Court previously ruled:

“Ms. Spears qualifies as a party in interest…”

However, the Trustee immediately notes:

“The Trustee reserves all rights to object to Ms. Spears’ standing.”

In plain English:

The Court recognized limited party-in-interest status, but the Trustee is not conceding broader rights.

⸻

Shareholder Notice

One of the most important sections of the filing concerns shareholder notice.

The Trustee states:

“There may be as many as 65,000 or more shareholders.”

The Trustee also confirms:

✔️ A comprehensive shareholder list has been requested.

✔️ A claims agent may be engaged.

✔️ Shareholder rights are not intended to be prejudiced.

✔️ A future bar date may be requested.

⸻

FINRA Discovery Continues

Another significant takeaway:

Despite the Texas litigation discussion, the Trustee specifically confirms that FINRA remains a source of discovery being pursued in connection with Meta Materials trading activity.

For shareholders closely following:

FINRA

MMTLP

U3 Halt

Trading records

Market activity

this paragraph confirms FINRA remains within the investigative scope.

See first comment for continuation.

https://t.co/Gyfx3HxEZM

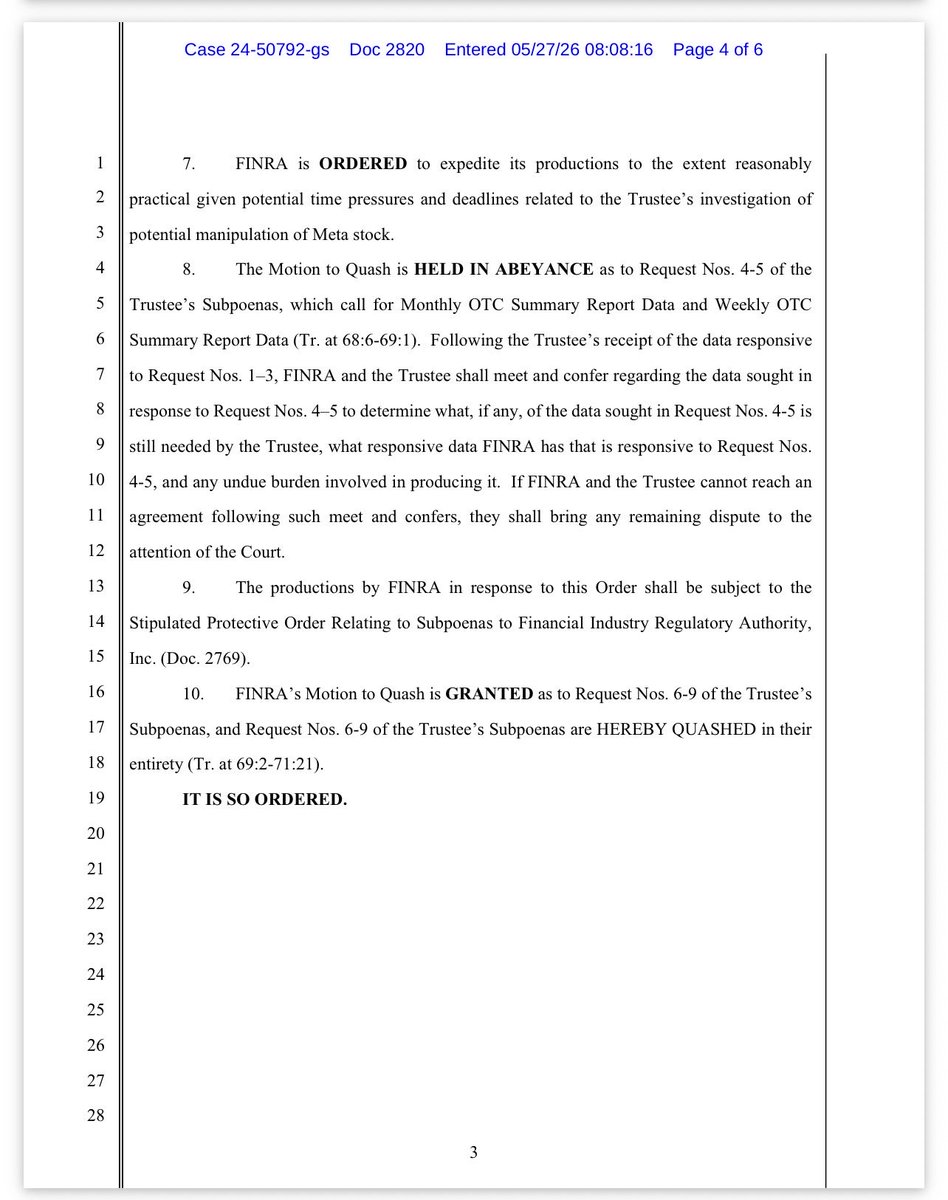

MMAT | In re Meta Materials Inc. | Case No. 24-50792-gs | Doc 2820 | Filed May 27, 2026

Order Granting in Part and Denying in Part FINRA’s Motion to Quash Trustee Subpoenas

⚠️ Not Legal Advice

The big picture

This is a major discovery win for the Chapter 7 Trustee.

Judge Spraker basically said:

“FINRA, you do have to turn over important trading/manipulation-related data. But there are limits, and the trustee has to pay certain production costs.”

This order is directly tied to the trustee’s investigation into potential manipulation of Meta stock (MMAT / TRCH / MMTLP).

⸻

What happened in plain English

FINRA tried to block the subpoenas

FINRA asked the court to either:

Kill the subpoenas entirely (motion to quash) OR

Narrow them significantly via protective order.

The judge said:

Not entirely. Some yes. Some no.

Hence:

“Granted in part, denied in part.”

⸻

What the Trustee WON 🥇

1) Short Interest Data — PRODUCE IT

FINRA must turn over reported short interest data.

That includes:

TRCH + MMAT

Sept. 21, 2020 → Aug. 21, 2024

MMTLP

June 28, 2021 → Dec. 14, 2022

Layman’s meaning:

This shows what broker-dealers were reporting as short positions.

This helps answer:

Was short interest unusually elevated?

Did reported short positions match actual market behavior?

Were there anomalies around key events?

⸻

2) TRF Data — HUGE 🧨

FINRA must produce Trade Reporting Facility (TRF) data.

Same date ranges.

This is likely one of the most important parts of the order.

Why?

TRF captures off-exchange / OTC reported trades, often associated with internalized trading / market maker activity.

Layman’s translation:

If the trustee is investigating alleged manipulation, this is where some of the most meaningful footprints could live.

Judge even ordered:

FINRA must expedite production due to time pressure.

That’s important.

⸻

3) Reg SHO Daily Short Sale Volume Data

FINRA must produce this too.

Same date ranges.

This helps show:

Daily short sale activity

Short-sale patterns

Whether activity spiked during sensitive periods

Not proof of wrongdoing by itself.

But valuable puzzle pieces.

⸻

Timing priority (important) 👀

📆FINRA agreed to prioritize production in this order:

MMAT 2023

MMAT 2024

MMAT 2022

MMAT 2021

Then TRCH

Then MMTLP

Why that matters:

The trustee likely wants the most actionable data first given statute/time pressure.

⸻

Judge explicitly referenced manipulation investigation

This is a key line.

Judge ordered FINRA to move quickly because of:

“potential manipulation of Meta stock.”

That’s notable.

This is not a finding that manipulation occurred.

But it confirms the court recognizes the trustee’s investigation as legitimate and time-sensitive.

⸻

Requests put on HOLD (not denied yet)

Requests 4–5:

Monthly OTC Summary Report Data

Weekly OTC Summary Report Data

Judge said:

Let’s wait.

Reason:

The trustee may get enough from Requests 1–3 first.

If more is still needed, the parties must meet and confer.

If they still fight, they can come back to court.

Translation:

This door is still open.

⸻

What FINRA WON

Requests 6–9 were QUASHED entirely.

Meaning:

FINRA does NOT have to produce whatever those categories were seeking.

So this was not a total trustee sweep.

⸻

Costs — trustee pays

Because FINRA is a nonparty, Rule 45 cost protections apply.

Meaning:

If producing the data is expensive or burdensome:

the trustee pays the production costs.

This matters because FINRA had argued massive burden.

The judge basically said:

“Produce it—but the estate can shoulder the cost.”

⸻

Protective order remains in place

Anything produced stays under the existing protective order.

Meaning:

This data is not automatically public.

It’s controlled discovery material.

So no—this does not mean shareholders get to immediately see raw trading records.

They have this S1. Memorized they have only been reading it for 3 years and 4 months. The only thing that has changed is the fing financials that they fing requested on 2 different occasions costing the company millions of dollars in accounting and legal fees for a fing company that doesn’t fing trade. I want every shareholder to remember this shit when they consider any settlements well as the lost opportunity cost in the market for the past 3 years and 4 months of waiting on this approval for effectiveness. F the SEC AND F FINRA for this BS. I’ve held this in for over 3 years out of respect for all shareholders and for NBH. ITS OUR TURN TO EAT AT TROUGH AND WE ARE FING HUNGRY!!!

Just so you know Failure is not an option in this deal. If it was this game would have been over long ago. This fight has blue just begun. Hold my Beer….

Next Bridge Hydrocarbons Announces SEC Declares Effective its S-1 Registration Statement

Company prices and commences a public offering of 40 million shares

https://t.co/2hO7KuPeJJ

![kimkep4796's tweet photo. Part 1 of 2

MMAT MMTLP NBH TRCH

⚖️ META MATERIALS (MMAT) Bankruptcy

Case No. 24-50792-gs

Document 2831

Filed June 2, 2026

Trustee Christina Lovato’s Response to Danielle Spears’ Motions

⚠️ Not Legal Advice

⸻

🦋 Two Quotes That MMAT / MMTLP / NBH Shareholders Will Likely Focus On

1️⃣ Shareholder List / Claims Agent / Shareholder Rights

From Page 6:

“The Trustee has requested a comprehensive list of shareholders from the transfer agent. Once that information has been received, the Trustee will determination [sic] next steps, i.e., incurring the expense to engage a claims agent. It is not the Trustee’s intention to prejudice the rights of any creditor or shareholder. At the appropriate time, the Trustee will seek authority to establish a bar date.”

Why This Matters

This is one of the clearest statements yet that:

✅ The Trustee is seeking a complete shareholder list.

✅ A claims agent is being considered.

✅ The Trustee expressly states she does not intend to prejudice shareholder rights.

✅ The Trustee anticipates eventually seeking a bar date process.

⸻

2️⃣ FINRA and the U3 Halt

From Page 7:

“FINRA and the U3 halt. This issue was a significant part of the Texas Litigation previously addressed. After more than a year and two opportunities to make her case against FINRA and others (including Greg McCabe), Ms. Spears’ case was dismissed with prejudice. What Ms. Spears ignores is that FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares. Ms. Spears apparently believes the Trustee and her professionals need her lay-person expertise.”

Why This Matters

Many shareholders have focused on FINRA and the December 2022 U3 halt.

The important takeaway here is not the criticism of Spears.

The significant statement is:

“FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares.”

That is a direct statement from the Trustee confirming that FINRA remains a discovery target in the MMAT investigation.

⸻

📝 Comprehensive Layman’s Summary

What Is This Filing?

This filing is Trustee Christina Lovato’s response asking Judge Gary Spraker to deny several motions filed by Danielle Spears before the June 16, 2026 hearing.

⸻

Trustee’s Core Position

The Trustee argues that individual shareholders cannot:

❌ Direct the investigation

❌ Demand investigative materials

❌ Control litigation decisions

❌ Force the Trustee to pursue particular claims

❌ Obtain internal work product or litigation strategy

The filing states:

“A putative shareholder cannot broadly intervene into, or seek to direct, a trustee’s administration of a chapter 7 estate.”

⸻

Standing

The Trustee acknowledges the Court previously ruled:

“Ms. Spears qualifies as a party in interest…”

However, the Trustee immediately notes:

“The Trustee reserves all rights to object to Ms. Spears’ standing.”

In plain English:

The Court recognized limited party-in-interest status, but the Trustee is not conceding broader rights.

⸻

Shareholder Notice

One of the most important sections of the filing concerns shareholder notice.

The Trustee states:

“There may be as many as 65,000 or more shareholders.”

The Trustee also confirms:

✔️ A comprehensive shareholder list has been requested.

✔️ A claims agent may be engaged.

✔️ Shareholder rights are not intended to be prejudiced.

✔️ A future bar date may be requested.

⸻

FINRA Discovery Continues

Another significant takeaway:

Despite the Texas litigation discussion, the Trustee specifically confirms that FINRA remains a source of discovery being pursued in connection with Meta Materials trading activity.

For shareholders closely following:

FINRA

MMTLP

U3 Halt

Trading records

Market activity

this paragraph confirms FINRA remains within the investigative scope.

See first comment for continuation.

https://t.co/Gyfx3HxEZM](https://pbs.twimg.com/media/HJ2Ii3xWkAA1qtF.jpg)

![kimkep4796's tweet photo. Part 1 of 2

MMAT MMTLP NBH TRCH

⚖️ META MATERIALS (MMAT) Bankruptcy

Case No. 24-50792-gs

Document 2831

Filed June 2, 2026

Trustee Christina Lovato’s Response to Danielle Spears’ Motions

⚠️ Not Legal Advice

⸻

🦋 Two Quotes That MMAT / MMTLP / NBH Shareholders Will Likely Focus On

1️⃣ Shareholder List / Claims Agent / Shareholder Rights

From Page 6:

“The Trustee has requested a comprehensive list of shareholders from the transfer agent. Once that information has been received, the Trustee will determination [sic] next steps, i.e., incurring the expense to engage a claims agent. It is not the Trustee’s intention to prejudice the rights of any creditor or shareholder. At the appropriate time, the Trustee will seek authority to establish a bar date.”

Why This Matters

This is one of the clearest statements yet that:

✅ The Trustee is seeking a complete shareholder list.

✅ A claims agent is being considered.

✅ The Trustee expressly states she does not intend to prejudice shareholder rights.

✅ The Trustee anticipates eventually seeking a bar date process.

⸻

2️⃣ FINRA and the U3 Halt

From Page 7:

“FINRA and the U3 halt. This issue was a significant part of the Texas Litigation previously addressed. After more than a year and two opportunities to make her case against FINRA and others (including Greg McCabe), Ms. Spears’ case was dismissed with prejudice. What Ms. Spears ignores is that FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares. Ms. Spears apparently believes the Trustee and her professionals need her lay-person expertise.”

Why This Matters

Many shareholders have focused on FINRA and the December 2022 U3 halt.

The important takeaway here is not the criticism of Spears.

The significant statement is:

“FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares.”

That is a direct statement from the Trustee confirming that FINRA remains a discovery target in the MMAT investigation.

⸻

📝 Comprehensive Layman’s Summary

What Is This Filing?

This filing is Trustee Christina Lovato’s response asking Judge Gary Spraker to deny several motions filed by Danielle Spears before the June 16, 2026 hearing.

⸻

Trustee’s Core Position

The Trustee argues that individual shareholders cannot:

❌ Direct the investigation

❌ Demand investigative materials

❌ Control litigation decisions

❌ Force the Trustee to pursue particular claims

❌ Obtain internal work product or litigation strategy

The filing states:

“A putative shareholder cannot broadly intervene into, or seek to direct, a trustee’s administration of a chapter 7 estate.”

⸻

Standing

The Trustee acknowledges the Court previously ruled:

“Ms. Spears qualifies as a party in interest…”

However, the Trustee immediately notes:

“The Trustee reserves all rights to object to Ms. Spears’ standing.”

In plain English:

The Court recognized limited party-in-interest status, but the Trustee is not conceding broader rights.

⸻

Shareholder Notice

One of the most important sections of the filing concerns shareholder notice.

The Trustee states:

“There may be as many as 65,000 or more shareholders.”

The Trustee also confirms:

✔️ A comprehensive shareholder list has been requested.

✔️ A claims agent may be engaged.

✔️ Shareholder rights are not intended to be prejudiced.

✔️ A future bar date may be requested.

⸻

FINRA Discovery Continues

Another significant takeaway:

Despite the Texas litigation discussion, the Trustee specifically confirms that FINRA remains a source of discovery being pursued in connection with Meta Materials trading activity.

For shareholders closely following:

FINRA

MMTLP

U3 Halt

Trading records

Market activity

this paragraph confirms FINRA remains within the investigative scope.

See first comment for continuation.

https://t.co/Gyfx3HxEZM](https://pbs.twimg.com/media/HJ2Ii3vWwAAtOu9.jpg)

![kimkep4796's tweet photo. Part 1 of 2

MMAT MMTLP NBH TRCH

⚖️ META MATERIALS (MMAT) Bankruptcy

Case No. 24-50792-gs

Document 2831

Filed June 2, 2026

Trustee Christina Lovato’s Response to Danielle Spears’ Motions

⚠️ Not Legal Advice

⸻

🦋 Two Quotes That MMAT / MMTLP / NBH Shareholders Will Likely Focus On

1️⃣ Shareholder List / Claims Agent / Shareholder Rights

From Page 6:

“The Trustee has requested a comprehensive list of shareholders from the transfer agent. Once that information has been received, the Trustee will determination [sic] next steps, i.e., incurring the expense to engage a claims agent. It is not the Trustee’s intention to prejudice the rights of any creditor or shareholder. At the appropriate time, the Trustee will seek authority to establish a bar date.”

Why This Matters

This is one of the clearest statements yet that:

✅ The Trustee is seeking a complete shareholder list.

✅ A claims agent is being considered.

✅ The Trustee expressly states she does not intend to prejudice shareholder rights.

✅ The Trustee anticipates eventually seeking a bar date process.

⸻

2️⃣ FINRA and the U3 Halt

From Page 7:

“FINRA and the U3 halt. This issue was a significant part of the Texas Litigation previously addressed. After more than a year and two opportunities to make her case against FINRA and others (including Greg McCabe), Ms. Spears’ case was dismissed with prejudice. What Ms. Spears ignores is that FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares. Ms. Spears apparently believes the Trustee and her professionals need her lay-person expertise.”

Why This Matters

Many shareholders have focused on FINRA and the December 2022 U3 halt.

The important takeaway here is not the criticism of Spears.

The significant statement is:

“FINRA is one of the non-parties from which the Trustee is seeking discovery related to the trading of Meta Materials shares.”

That is a direct statement from the Trustee confirming that FINRA remains a discovery target in the MMAT investigation.

⸻

📝 Comprehensive Layman’s Summary

What Is This Filing?

This filing is Trustee Christina Lovato’s response asking Judge Gary Spraker to deny several motions filed by Danielle Spears before the June 16, 2026 hearing.

⸻

Trustee’s Core Position

The Trustee argues that individual shareholders cannot:

❌ Direct the investigation

❌ Demand investigative materials

❌ Control litigation decisions

❌ Force the Trustee to pursue particular claims

❌ Obtain internal work product or litigation strategy

The filing states:

“A putative shareholder cannot broadly intervene into, or seek to direct, a trustee’s administration of a chapter 7 estate.”

⸻

Standing

The Trustee acknowledges the Court previously ruled:

“Ms. Spears qualifies as a party in interest…”

However, the Trustee immediately notes:

“The Trustee reserves all rights to object to Ms. Spears’ standing.”

In plain English:

The Court recognized limited party-in-interest status, but the Trustee is not conceding broader rights.

⸻

Shareholder Notice

One of the most important sections of the filing concerns shareholder notice.

The Trustee states:

“There may be as many as 65,000 or more shareholders.”

The Trustee also confirms:

✔️ A comprehensive shareholder list has been requested.

✔️ A claims agent may be engaged.

✔️ Shareholder rights are not intended to be prejudiced.

✔️ A future bar date may be requested.

⸻

FINRA Discovery Continues

Another significant takeaway:

Despite the Texas litigation discussion, the Trustee specifically confirms that FINRA remains a source of discovery being pursued in connection with Meta Materials trading activity.

For shareholders closely following:

FINRA

MMTLP

U3 Halt

Trading records

Market activity

this paragraph confirms FINRA remains within the investigative scope.

See first comment for continuation.

https://t.co/Gyfx3HxEZM](https://pbs.twimg.com/media/HJ2Ii4hXYAAvt7I.jpg)