🎉Three years of GBI: an honest reckoning

Anniversaries are good moments to celebrate. They are also good moments to admit what did not work.

In three years, we built the platform we wanted to build. We proved that goal-based investing works. We created a conflict-free advisory engine that connects portfolios to real life goals.

What we did not manage to do was move GBI into its next stage.

The gap had a name: partnerships and strategic capital.

GBI was never meant to remain only a B2C app. The engine we built could support family offices, advice-only robo-advisory models, and B2B platforms. But to get there, we needed the right partners or strategic investors.

We did not find them.

The main reason was simple: revenue.

Or rather, the deliberate absence of it.

GBI is free until CHF 100k of starting capital. That was a principle. We did not want to penalize smaller portfolios. But commercially, that principle is also a wall.

Most VCs want B2B, recurring revenue, fast monetization, and clean metrics. A free-until-CHF-100k, conflict-free, consumer-facing investment platform is not exactly VC catnip and👿more like garlic for vampires.

We would still make the same choice again. But we should have defined the first revenue path earlier.

With hindsight, the natural model was portfolio monitoring by subscription. But proper monitoring requires connecting real client accounts across Saxo, Interactive Brokers, Swissquote, banks, and custodians.

That is expensive. Operationally heavy. And hard to justify on top of a free product without a strategic partner.

So the revenue gap and the partner gap were really the same problem. Each was waiting for the other.

🎯Where do we go from here?

The engine is built. It is live. It works. The lesson is learned. Next, GBI is AI-ready. Goal onboarding can move naturally to an avatar-driven conversation because the hard part, the optimization engine underneath, already exists.

And we are bringing more of our modelling work to B2B: fair-value monitoring tools for FX, equities, rates, and commodities.

So, the honest three-year summary:

👉We built the engine.

👉We proved the method.

👉Yes, we missed the commercial bridge.

👉Now we know what bridge has to be built.

Some gaps are failures. Others are invitations. 💪

🙏Thanks to everyone who has supported us along the way and expect more to come!

🎉Three years of GBI: from principle to platform. Part 2 of 3 - what we built, and how we built it.

In our first article we described what we set out to fix. Here we want to be concrete about what we actually built, and be transparent about the method behind it, because the "how" matters as much as the "what."

👉 The platform https://t.co/uWsbV8zhXJ is live, openly available, and built entirely in Java on a serverless cloud architecture: real-time advice, low operating costs, conflict-free by design, and no pitch deck in sight. The advice is driven by your goal and your situation, not by what is most profitable for us to sell you.

👉 The engine underneath is dynamic asset allocation, built on the dynamic programming framework we explained in our recent blog articles (see comments). The objective is not to maximize expected wealth. It is to maximize the probability of actually reaching your goal. That distinction matters more than most people realize.

👉 Our early sketches, shared in this carousel, show how we translated that theory into practice from day one: an efficient surface mapping expected return against goal threshold and failure probability, with risk profiles already penciled in by hand. The strategies rest on roughly 250 SAA portfolios drawn from efficient frontiers, varying across goals, income category, and risk profile. We follow the tangency-portfolio logic of Tobin's separation theorem: a deliberately limited, carefully chosen asset set that keeps implementation lean, transaction costs low, and conflict of interest out by design. This is also where the conflict-free promise from our first article stops being a slogan and becomes engineering.

💪This is the part that is hard to fake. A polished interface is easy; a mathematically grounded allocation that adapts as your situation changes is not. That rigor is what turned our founding principles into something that works in practice.

👉 On performance: across all five risk profiles, GBI's dynamic rebalancing beat the passive benchmark over May 2023 to May 2026. Our default fully-hedged strategy already outperformed. But an optimized FX hedge, one that selectively hedges rather than hedging everything by default, would have added a further 0.2 to 0.85 percentage points on top for the Elevated, Medium, and Moderate profiles. Blanket hedging has a cost, and a more nuanced approach adds real value.

The chart in the carousel shows the full picture. We invite you to compare these numbers with any mandated solution or robo-advisory platform in Switzerland or abroad, and to judge for yourself.

Read the theory: links in the comments.

Past performance is not indicative of future results. Figures cumulative in CHF, before taxes.

#GoalBasedInvesting #WealthTech #AssetAllocation #FamilyOffice #QuantFinance

Article 1: What We Had in Mind

Three years of GBI. Here is the real story

Three years. It's hard to believe how fast they went. Three years ago we launched the first (and, to the best of our knowledge, still the only) openly available https://t.co/uWsbV8zhXJ platform to the world, and today we get to look back at a journey we're genuinely proud of.

The aim was clear from day one: show that it is possible to build a highly scalable solution that is free of conflicts of interest, that solves genuinely complex investment problems, and that tackles the major malpractices which have put investors at a disadvantage for decades. Ambitious? Absolutely. And that is exactly why it has been so much fun.

To celebrate, and to keep ourselves honest, we are publishing three articles that lay out what we had in mind, what we achieved and how, and, just as importantly, where we need to be realistic about what could have gone better (i.e. where we fell short).

We start today with what we had in mind. From the very beginning it was clear what we wanted to achieve, and it was nothing less than to correct what is not working in finance and, to be more precise, in financial advice:

Advice should be goal-oriented. If you plan to invest, invest with a plan. A portfolio only makes sense in relation to what it is meant to fund; a number on a screen is not a goal.

Investments should be tailored to each individual. The goal of buying a house requires a different plan than the goal of paying back a mortgage. Two people with the same risk questionnaire but different objectives should not end up with the same portfolio.

Costs should never put small pockets at a disadvantage. No ad valorem pricing. A smaller risk budget should not subsidize the system: lower-risk profiles deserve lower fees than aggressive, high-risk profiles, not a flat percentage that quietly penalizes the careful saver.

We should be on your side, especially while you are still building. For investors early in their wealth journey, advice should be about helping them grow, not about what can be extracted along the way. That means caring about which assets you hold, not where you hold them, and removing by default the conflicts of interest that are baked into traditional advice.

These four principles were never marketing slogans. They were design constraints: the rules we held ourselves to before writing a single line of allocation logic. And so the tool was developed step by step, and here we are, with:

a platform that lets you save for a goal, manage debt repayment, and plan your retirement;

a platform that is free of charge up to CHF 100k;

a platform that expands the investment universe as your investment capital grows.

So how was the adoption? Let's be honest about this too. Professional investors and B2B users loved the platform; first-time investors reacted very differently. What looks to us like a straightforward solution can feel, to people with little or no financial experience, too ambitious and too difficult to understand, and the step towards actually implementing it is often the hardest one. That realization led us to build an educational platform at https://t.co/Ch0a47dIJa, which we are now developing further into a video portal that lets you consume financial education on demand.

In the next article, we go deeper: the engineering behind the platform, the results across risk profiles, and the mathematics that makes it all work.

https://t.co/bH240VnLtL

#GoalBasedInvesting #WealthManagement #FinancialAdvice #Fintech #Switzerland #Investing #Familyoffice

Was Schach mit deiner Anlagestrategie zu tun hat?

Dynamische Programmierung klingt nach Informatik – ist aber eines der mächtigsten Werkzeuge, um unter Unsicherheit optimale Entscheidungen über die Zeit zu treffen.

Stell dir ein Schachbrett vor: Du startest links und bewegst dich Spalte für Spalte nach rechts. Jede Entscheidung bringt dich mit gewissen Wahrscheinlichkeiten in ein neues Feld. Am Ende zählt deine Position. Wie spielst du optimal?

Der Trick: rückwärts denken. Man beginnt beim letzten Schritt, bestimmt dort die beste Entscheidung und arbeitet sich Schritt für Schritt zur Gegenwart vor. Man muss die Zukunft also nicht erraten – man lässt sich von ihr sagen, was die Gegenwart tun sollte.

Genau dieselbe Logik steckt hinter Asset Allocation:

→ Die Bewegung nach rechts = der Lauf der Zeit

→ Die Felder = dein Vermögensniveau zu jedem Zeitpunkt

→ Die möglichen Züge = die Portfolios, die du wählen kannst

→ Das Ziel = dein gewünschtes Endvermögen

Die entscheidende Frage lautet damit: Welches Portfolio solltest du angesichts deines aktuellen Vermögens, deiner Risikotoleranz und deines Horizonts heute wählen, um dein Ziel zu erreichen?

Das Schöne daran: Unter den richtigen Annahmen lässt sich beweisen, dass eine optimale Strategie existiert – und ein Algorithmus findet sie. Kein Raten, kein Bauchgefühl.

Wer tiefer eintauchen möchte – inklusive Rasterspiel, Schritt-für-Schritt-Beispiel und der Verknüpfung zu Begriffen wie States, Control Set und Reward Function – findet die ganze Erklärung hier: https://t.co/udVBo3HhKZ

Du willst dynamische Programmierung in Aktion sehen? Definiere dein eigenes Anlageziel und erlebe, wie sich diese Mathematik in der Praxis anfühlt: https://t.co/63BWIRjAv1

#Geldanlage #Vermögensverwaltung #GoalBasedInvesting #Fintech

5/5: Unsere Einschätzung: Eher ja. Die Zinsprämie spiegelt Makro-Ungleichgewichte wider. Wahrscheinlich baut sich der Carry über einen schwächeren USD wieder ab. ➡️ Fazit: Hedging ist heute eine Makro-Entscheidung, keine reine Bewertungs-Frage mehr.

Wer mehr Details braucht, einfach melden📈 #FX #USDCHF #Macro #Investing #Schweiz

Die USD-Hedging-Story 2026 🧵

1/5: Währungsrisiken sind die grösste Unbekannte für Portfolios. Bei https://t.co/hP8jNE6mpZ haben wir seit dem Start konsequent auf USD-Hedging gesetzt – und das hat sich ausgezahlt. 💰 Aber: Die Spielregeln ändern sich gerade fundamental. Ein Blick auf unsere FX-Fair-Values: 👇

4/5: Die neue Kernfrage für 2026: Kann die Zinsdifferenz (USD > CHF), die man beim Hedging als Kosten zahlt, durch US-Inflation & schwächeres Realwachstum kompensiert werden? Sprich: Folgt nun eine weitere Phase der CHF-Überbewertung oder eine Abwertung?

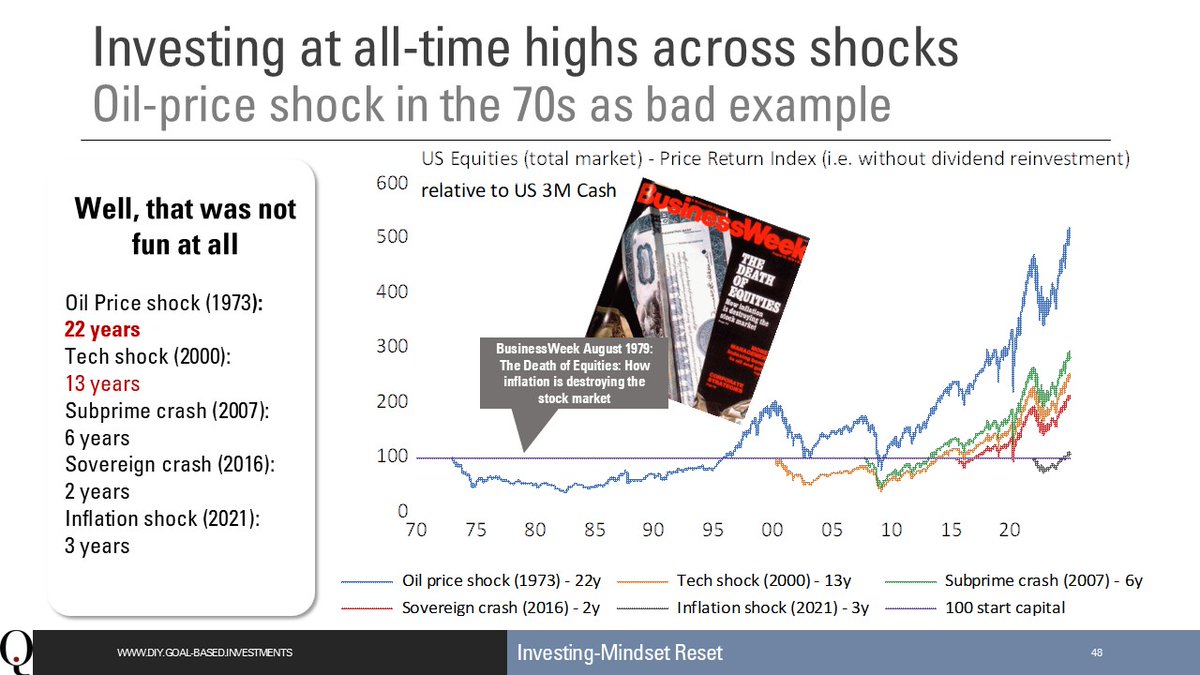

Now that markets seem to have caught their breath and calmed down, it’s the perfect time to zoom out and look at history. 👇

Here is what actually happened after the last major oil price shock—before you allow someone to tell you that "this time it's different."

If you look at the chart below, the reality is sobering. If you had the misfortune of investing at the all-time high just before the October 1973–January 1974 Oil Price Shock, it took a staggering 22 years for US Equities to break even relative to cash (looking at price returns).

It was utterly devastating for equity markets, and the recovery dragged on longer than any other modern crisis we track in this window. By August 1979 sentiment was so broken that BusinessWeek famously ran their cover story: "The Death of Equities: How inflation is destroying the stock market."

A few things stand out when we look back at that era:

The Stagflation Trap: The painful combination of surging inflation and rising unemployment created an economic puzzle that academic analysts are still debating today.

Faster Modern Recoveries: Notice how every major market crash that followed had a much quicker recovery: the 2000 Tech Shock (13 years), the 2007 Subprime Crash (6 years), and the 2016/2021 shocks (2 and 3 years, respectively).

True, today’s market structures, central bank toolkits, and economies are fundamentally different. But we shouldn’t jump to the comforting conclusion that things are simply "back to normal" just because politicians are taking to social media to speak their book and declare victory. History tells us that structural economic shifts take time to digest.

To be clear, my personal view is not that we are doomed to repeat this exact 22-year stagnation, nor is this a call to stay out of the market (our forecasts for this year are currently only slightly negative). Rather, it’s a reminder that investing is inherently risky. Investors should think twice before blindly accepting the comforting promise that "in the long run, everything will be fine", because as history shows, the "long run" can sometimes test your solvency and patience for decades.

And to be fair, the academic analysis of the 1970s usually overlooks one critical, highly disruptive exogenous shock: I happened to be born during that period. 😉

👇 P.S. This chart is a sneak peek from our https://t.co/82euPDlUN7 course. (Note: The course is currently only held in German).

#Markets #Investing #EconomicHistory #OilShock #MacroEconomics #WealthManagement #InvestmentStrategy #QIO

Valuation doesn’t matter—until it does. 👇 Chart below: Korea’s valuation in context.

It’s remarkable—and frankly, stunning—to watch how markets can stretch beyond sensible valuation levels for quarters, or even years. And no, this isn’t about using a simple P/E metric in isolation. We look at a chain of fair-value frameworks across time and contexts.

And because of this often valuation often feels irrelevant... right up until it suddenly becomes the only thing that matters.

Take Korea correction today for example. As the chart below shows (without todays move), it’s been one of the most expensive markets in the world—yet traditional fundamentals like future growth, inflation or financing conditions (both domestic and global) couldn’t explain the rally. But who cared? Markets kept climbing.

Now, that momentum appears to be fading—and in our view, there’s more room to the downside. Not because Korea is uniquely vulnerable, but because so much capital was pulled forward in anticipation of extraordinary gains. When that narrative shifts, money gets taken off the table. Fast.

Yes, I know—pundits and finfluencers love to say “you can’t time the market.” We would never recommend resting your investment thesis solely on valuation; after all, markets can remain irrational longer than you can remain solvent (i.e. employed), and fundamentals can occasionally catch up with the market (see the shadow values in the fair-value chart to gauge calibration uncertainty).

But you can illustrate it, you can interpret it, and you can step aside when levels reach extremes.

#Markets #Valuation #Korea #Investing #Macro #RiskManagement

Die Pensionskassen-Wunde: Ein Weckruf und 5 Fehler, die wir abseits der Aktienquote beheben müssen

Die Diskussion um schrumpfende Renten in der Schweiz, wie sie jüngst in der SonntagsZeitung thematisiert wurde, ist ein wichtiger Weckruf. Die Wunde der Altersvorsorge schmerzt trotz unzähliger "Pflaster" weiter.

Ich stimme Armin Müller zu: Eine höhere Aktienallokation ist für eine sinnvolle Verwaltung von Altersvermögen zwingend notwendig. ABER: Alleine eine höhere Aktienquote wird die massgeblichen Probleme der zu geringen Renditeentwicklung nicht beheben. Wir sehen bei der Analyse von Pensionskassen (PKs) und privaten Vermögen immer wieder die gleichen fünf systemischen Fehler: Fünf Stellschrauben für nachhaltig bessere Renditen:

-) Zu viele Produkte: Niemand braucht mehr als 5 Produkte im Portfolio (Komplexität frisst Rendite)

-) Massiver CH Home-Bias: Der MSCI World fehlt oft als Kern der Anlagestrategie.

-) Falsche Hedging-Annahmen: Fokus auf Obligationen statt Aktien im Hedging – ein Ansatz, der von der Wissenschaft längst verworfen wurde.

-) Ineffiziente SAA: Einsatz der Efficient Frontier statt des Tangentialportfolios (bedeute viele Produkte bei wenig Rendite).

-) Zu hohe Gebühren: Alles über 0.25% p.a. ist für eine institutionelle Lösung inakzeptabel.

Diese Probleme werden besonders durch Anlagestrategien verschärft, bei denen Obligationen den grössten Anteil darstellen – oft mit negativen (foreign hedged) oder Null-Renditen (domestic).

👉 Die Kernfrage: Warum tritt dieses Problem quer über die Schweiz und bei so vielen PKs gleichzeitig auf? Ich glaube, es liegt an einer Handvoll von ALM-Beratungsunternehmen, welche die Arbeit im Anlagegeschäft primär als Risikominimierungsaufgabe wahrnehmen, anstatt den Fokus auf Renditeaussichten und Renditenmodellierungen zu legen.

Solange sich dieser Fokus nicht ändert, wird eine höhere Allokation in Aktien nur zu einem besseren Geschäft, aber nicht zu den wirklich nachhaltig besseren Renditen und Renten führen, die wir alle brauchen.

PS: Wer sehen möchte, dass es auch anders geht, kann unter 👉 https://t.co/63BWIRjAv1 seine eigene „private PK“ aufbauen und verwalten (oder mit unseren Kursen lernen wies geht). Für die meisten Nutzerinnen und Nutzer kostenlos – und falls wer einen gratis Testzugang brauchst, einfach melden.

#Altersvorsorge #Pensionskasse #Schweiz #Finanzen #Anlagestrategie #Rendite #BVG #Pensionskassen #Anlagen #Risiken

💡 Der gefährlichste Chart der Finanzwelt ist nicht falsch – es ist schlimmer.

Es ist die Illustrierung, welche jede Bank, jeder CIO und unzählige Finfluencer seit Jahren recyceln – sauber, simpel, beruhigend. Geliked von Tausenden auf LinkedIn, geliebt von Vertriebsteams rund um den Globus. Und genau das ist das Problem.

Kaum jemand hat je seinen Wahrheitsgehalt hinterfragt oder analysiert, was wirklich hinter den Zahlen und der Logik steckt. Für mich ist dieses Chart das Sinnbild dafür, was in der Finanzwelt schiefläuft.

Die Mathematik ist korrekt, die Logik nicht. In der Realität treten die besten und schlechtesten Tage oft nebeneinander auf – wer den einen verpasst, verpasst meist auch den anderen. Und nein, diese „besten Tage“ machen die Verluste kurz davor nicht wett.

🎯 Unsere Analyse zeigt: Selbst wer das ganze Jahr vor diesen „besten Tagen“ investiert war, hätte verloren – und zwar deutlich.

„Timing“ bedeutet nicht Raten, sondern Risikomanagement – die Disziplin, zu de-riskieren, wenn sich Bedingungen verschlechtern, und wieder zu investieren, wenn sie sich verbessern.

Das ist kein Glück. Das ist Prozess.

Ja, time in the market ist wichtig – aber nur, wenn man versteht, in welcher Marktphase man sich befindet.

Denn Nichtstun ist keine Strategie – es ist Kapitulation.

https://t.co/Ch0a47dIJa

Denn bevor wir Menschen befähigen können, mit Vertrauen zu investieren, müssen wir zuerst das korrigieren, was oft leichtfertig (oder manchmal sogar absichtlich) falsch vermittelt wird.

✨ Bildung vor Sales.

✨ Wahrheit vor Slogans.

Bleib dran – die nächsten Episoden folgen.

#Investieren #Vermögensaufbau #ETF #Finanzwissen #Schweiz

💡 Das grösste Risiko für Anleger:innen ist nicht der Markt. Es sind die Mythen, die ihnen erzählt werden.

Viel zu oft kursieren Charts und Slogans, die Investieren simpel und sicher erscheinen lassen – als würde das Risiko „verschwinden“, wenn man nur lange genug wartet.

#Investieren #Vermögensaufbau #ETF #Finanzwissen #Schweiz

Dieses Karussell ist Teil einer neuen Serie, in der wir solche Mythen aufgreifen. Nicht, um vom Investieren abzuhalten – sondern um das richtige Verständnis dafür zu schaffen, wie Märkte tatsächlich funktionieren.

🚀 Vom Anfänger zum Anleger in nur 5 Tagen! 💰 Viele haben Angst vor dem Investieren, weil es kompliziert erscheint. Aber das muss nicht sein! Unser DIY InvestorInnen Programm bringt dir in nur 5 Tagen das nötige Know-how, eine cleare Strategie und die Unterstützung, die du brauchst! 💪 Nach 5 Abenden bist du bereit, dein Geld für dich arbeiten zu lassen. Die Plätze sind begrenzt, sicher dir jetzt deinen Spot! 🔐mehr auf https://t.co/KY0vEYkC0l✨

💡🌱🎯 Aus euren Erfahrungen geboren – für eure Ziele gemacht: Unser DIY InvestorInnen Programm. https://t.co/KY0vEYkC0l

🚀 Launch unseres DIY InvestorInnen Programms

Wir dachten, dass Top-Technologie und unabhängige Beratung reichen, um den Einstieg ins Investieren zu erleichtern. Doch unsere Nutzerinnen und Nutzer haben uns gezeigt, dass Technologie allein nicht reicht, um die Hürden beim Investieren zu überwinden.

Aus diesem Grund gibt es nun das DIY InvestorInnen Programm – verständlich, praxisnah und direkt an ihren Bedürfnissen orientiert.

https://t.co/KY0vEYkC0l

In nur 5 Abenden lernst du Schritt für Schritt, wie du deine persönliche Anlagestrategie entwickelst und direkt umsetzt – ohne Vorwissen, ohne Fachjargon, aber mit klarer Anleitung.

🔍 Was uns von anderen Kursen unterscheidet:

Keine Theorie ohne Praxis: Am Ende des Programms hast du nicht nur Wissen, sondern dein eigenes Depot eröffnet und dein erstes Investment platziert.

Unabhängig & konfliktfrei: Wir verkaufen keine Produkte, wir zeigen dir, wie du selbstbestimmt investierst.

Umsetzungs-Garantie: Wir begleiten dich, bis deine Strategie steht – und falls du nicht zufrieden bist, bekommst du dein Geld zurück.

Erfahrung & Expertise: Über 20 Jahre Kapitalmarktforschung, preisgekrönt (Ethics in Finance Award Finalist) und in der Schweiz entwickelt.

🎁 Early Bird Angebot

Buche bis zum 15. September und sichere dir 10% Rabatt auf die Teilnahmegebühr.

📅 Kursdaten: 22.–26. September, jeweils ab 19:00 Uhr

👉 Plätze sind limitiert – reserviere dir jetzt deinen Spot!

#InvestierenLernen #Finanzbildung #SelbstbestimmtInvestieren #DIYInvestorInnenProgramm #Schweiz