Critique:

1. Excellent questions.

2. Working out alongside your subject shows appreciation of what they are going through.

3. You should shorten the length. The TikTok generation ain’t got time to watch a half an hour doc.

4. Over reliance on background music. I don’t think you need it.

One of the few criticisms from Friday’s #EPP investor webinar was there was no mention of hard numbers in terms of revenues and NPV for MESH.

But after Fridays X post highlighting key meetings with DESNZ, Department of Business and Trade, as well as global financial institutions and banks, the reason for the lack of webinar detail seems clear… The numbers were withheld for confidentiality until presented to the government and institutional investors.

It’s worth mentioning before we begin, the figures in the presentation have been corroborated by Siemens Energy who deemed MESH “economically and commercially viable” in the RNS dated 28/04/26

Here are the numbers:

CAES LDES:

Asset life: 30 years

Net Revenues: £100m-£140m pa

NPV8 @ FID: £300m-350m

Gas Storage:

Asset life: 30 years

Net Revenues: £110m-£160m pa

NPV8 @ FID: £400m-800m

Total valuation at FID of £700m to £1.15bn

These are numbers impressive, but they are based only on the initial development of 4 compressed air salt caverns and 8 caverns for gas storage. However, the overall storage license area is able to allow construction of up to 60. Therefore, the quoted NPV8 numbers have the capacity to be multiplied significantly.

This also doesn’t include the revenue figures for hydrogen, high grade graphite and clean ammonia.

Using the projected figures for Graphite (circa 60,000 tonnes pa) and the target grade pricing of $10,000 per tonne (the aim is for the graphite to be refined via a study with Mitsui Japan to create nuclear/military grade graphite, elevating the price dramatically. See RNS 22/10/25 The company estimates revenues of £500m pa.

Hydrogen/Ammonia: This is a harder market to asses as an emerging sector. So based on the initial projected feedstock of 20,000 tonnes of hydrogen, let’s value it when it’s used to create Clean Ammonia as that market is very real.

Ammonia production of 110,000 tonnes pa is projected. The last domestic UK ammonia producer closed in 2023 and as of 2027 there’ll be a border levy on imports so this will affect chemical & farming Industries. Annual revenues for ammonia, based on volatile pricing revenues could be between £55-100m pa.

Risks:

Planning: Key regulatory hurdles now overcome with the gas storage license award and designation as a project of national significance… the section 35 has been massively under appreciated by the market and what was initially seen as a regulatory bump in the road on the way to license approvals is in fact a huge positive as the DCO process substantially streamlines the planning process from here on.

Politics: In terms of political risk the offering is diverse enough to be valuable to any government from Labour to Reform so it is in effect apolitical. (Is Reform going to turn down homegrown North Sea gas, domestic graphite for defence and Ammonia for Jeremy Clarkson and the farming community?)

Funding: Firstly, let’s put to bed concerns of the risk of a retail cash raise. The project needs £100’s of millions to build out MESH and that’s not coming from AIM retail: FACT. Short term the £15m funding is in place to satisfy the initial NSTA criteria (my opinion is this will be sidelined once project level funding arrives). As for strategic funding, this has already been stated it will come from global private sector institutions and potentially from GB Energy and National Wealth Fund, both of which have stated a clear mandate to invest in LDES and energy storage.

MESH has a suite of revenue streams offering diversification through products and industries at a time where they’ll be the only domestic producer of graphite and ammonia, they’ll effectively be doubling the UK energy storage capacity at a time of critical need and demand. And it requires little or no government funding (however GB Energy or National Wealth Fund may invest as mentioned in the webinar)

Therefore, in my opinion MESH will change the UK energy landscape and the lives of a lot of investors.

https://t.co/tncT949646

@ClonesCyclone Hi Barry,

Your article completely reflects my views. It was brilliant to watch but Wardley’s corner and perhaps the ref were waiting/hoping for the Hail Mary to land.

I also felt that Dubois kind of warmed up to absorbing the blows Wardley threw later during the fight.

EnergyPathways #EPP is delighted to announce it is to be awarded a Gas Storage License (GSL) by the North Sea Transition Authority for its flagship MESH project located in the East Irish Sea and onshore in Barrow-in-Furness.

This decision marks a major milestone in the development of the wider MESH project, with the GSL spanning a substantial offshore area that could support up to 60 large-scale salt storage caverns with potential for multi terawatt-hour scale energy storage and is expected to be Britain’s largest integrated energy storage facility.

The planned MESH Project has already been designated by the UK Government as a project of “national significance” and will comprise compressed air energy storage (CAES), natural gas storage transitioning to hydrogen storage and complementary hydrogen production for clean power and sustainable industry uses.

EnergyPathways plans the following:

· A natural gas storage facility that will double Britain’s meagre gas storage capacity and provide up to 6 days of national energy supply, securing Britain’s energy future and reducing its over-dependence on expensive gas imports.

· CAES storage of 300 MW / 55 GWh capacity, which is expected to be Britain’s largest LDES facility. This will provide game-changing “days not hours” of electrical storage, essential to harness the billions of pounds of wind power currently being wasted and passed on to consumer bills;

· Low-carbon dispatchable power generation that will be far cheaper than the expensive gas-fired power upon which Britain relies and which sets the power prices for all of Britain’s electricity, including renewables;

· Low-cost hydrogen production capability that will be used to further decarbonise MESH dispatchable power and new sustainable industries planned in Barrow-in-Furness, including EnergyPathways’ proposed graphite production plant; and

· A project that delivers homegrown energy and requires little or no government support at no added cost to consumer bills.

EnergyPathways, along with its Tier One partners, including Siemens Energy, Costain plc, Wood plc and Zenith Energy will now progress the MESH project to a Final Investment Decision in 2028 and start up by late 2031. The Company has already initiated several funding and capacity offtake discussions.

EnergyPathways CEO, Ben Clube said:

“I am delighted that we have met the NSTA’s criteria to offer EnergyPathways this crucial Gas Storage Licence, one of only two NSTA energy licence awards in the last two years.

“The UK Government recognises MESH and other forms of long-duration energy storage as having a vital role in lowering energy prices, bolstering energy security and achieving a clean energy system."

#MESH #EnergyStorage #CleanEnergy #LDES #GasStorage @energygovuk@Siemens_Energy@CostainGroup@ZenithEnergy

So let’s look closer at #EPP EnergyPathways

Progressing and not reliant on the gas storage license:

World’s Largest CAES project (UK’s largest LDES): Based on the storage capacity, output duration and benefitting from massive curtailed wind energy, estimates for revenue pa are around £150m+ (may be higher with cavern expansion and government subsidy or cap and floor benefits)

The Irish Sea has two huge wind farms to come online in the shape of Mona and Morgan. So expansion of the salt caverns with Siemens Energy is likely. Also EPP own the IP for CAES tech.

The project lifespan is 25 years+ so LDES alone is a company maker.

Reliant on Gas Storage License:

Gas Production: Marram alone has 46BCF of gas, based on current spot pricing that’s worth £500m (this doesn’t include Knox or Lowry fields) the figure will be a little lower due to the provision of cushion gas needed to facilitate storage.

46BCF is just natural gas and doesn’t include nitrogen in the mix which will be utilised to create clean ammonia.

Gas Storage: Marram alone has the equivalent storage capacity of Centrica’s Rough Facility 50-60BCF

The revenue value of gas storage is based not just on gas in place, but the opportunity for volatility trading (fill with cheap summer gas to sell on winter peaks)

Based on Marram alone annual revenues are approx £400m+ (but based on the UK’s low gas storage capacity this is conservative)

Hydrogen/Ammonia: This is a harder market to asses as an emerging sector. So based on the initial projected feedstock of 20,000 tonnes let’s value it when it’s used to create Ammonia as that market is very real.

Production of 110,000 tonnes pa is projected. The last domestic UK ammonia producer closed in 2023 and as of 2027 there’ll be a border levy on imports so this will affect chemical & farming Industries. Annual revenues for ammonia, based on volatile pricing could be between £55-100m pa.

Graphite: High grade synthetic Graphite (circa 60,000 tonnes pa) is set to be refined (With Mitsui Japan) to create nuclear/military grade graphite, elevating the price dramatically. Company estimates revenues of £500m pa

EnergyPathways has a suite of revenue streams offering diversification through products and industries at a time where they’ll be the only domestic producer of graphite and ammonia, they’ll effectively be doubling the UK energy storage capacity at a time of critical need and urgent demand. And it requires little or no government funding (however GB Energy or National Wealth Fund may invest)

The offering is also diverse enough to be valuable to any government from Labour to Reform so it is in effect apolitical. (Is Reform going to turn down homegrown North Sea gas, domestic graphite for defence and Ammonia for Jeremy Clarkson and the farming community?)

The tier one partnerships with Siemens Energy, Wood & Costain give the project credibility in the eyes of the government, as does the fact the world’s and UK’s largest CAES/LDES facility is going ahead at pace and it makes the project very real.

MESH is proposed as the flagship project for EPP and Siemens and “one of many” projects that will target favourable geology/infrastructure in the North Sea Continental Shelf.

The risk is that the storage license won’t be granted… But that would require the government to decline something they critically need and requires little or no taxpayer subsidy. They’d have to have a damn good reason to decline.

The second argument is that “it’s not operating until 2030, so why buy now”, the counter is that at £12m MCAP, when project level funding hits and the GSL is granted and the government and media takes up the story this stops being worth £12m.

The project will no longer be a “retail” focussed stock and with projected yields for investors to be 25% per annum over a 25 year lifespan then pension funds, institutions and family offices take over the register, and they invest for significant and sustained future growth not a quick 10% slice.

#UPL

Annual Report out.

Cash healthy and a broadly strong audit.

Something very positive sticks out right at the end in the post-period segment (always jump to these).

Progress on all five blocks.

But more importantly.

Blocks on the cusp of award.

The people behind this are serious, and there's a reason why why directors and management took £1.5 million in the £2 million raise.

When this moves, it'll move fast.

https://t.co/PV9BjdA6xF

@ClonesCyclone Hi Barry, yes I didn’t mean it disrespectfully, it was the order in my head. Probably Moses comes at the bottom of the list and perhaps makes his way upwards?

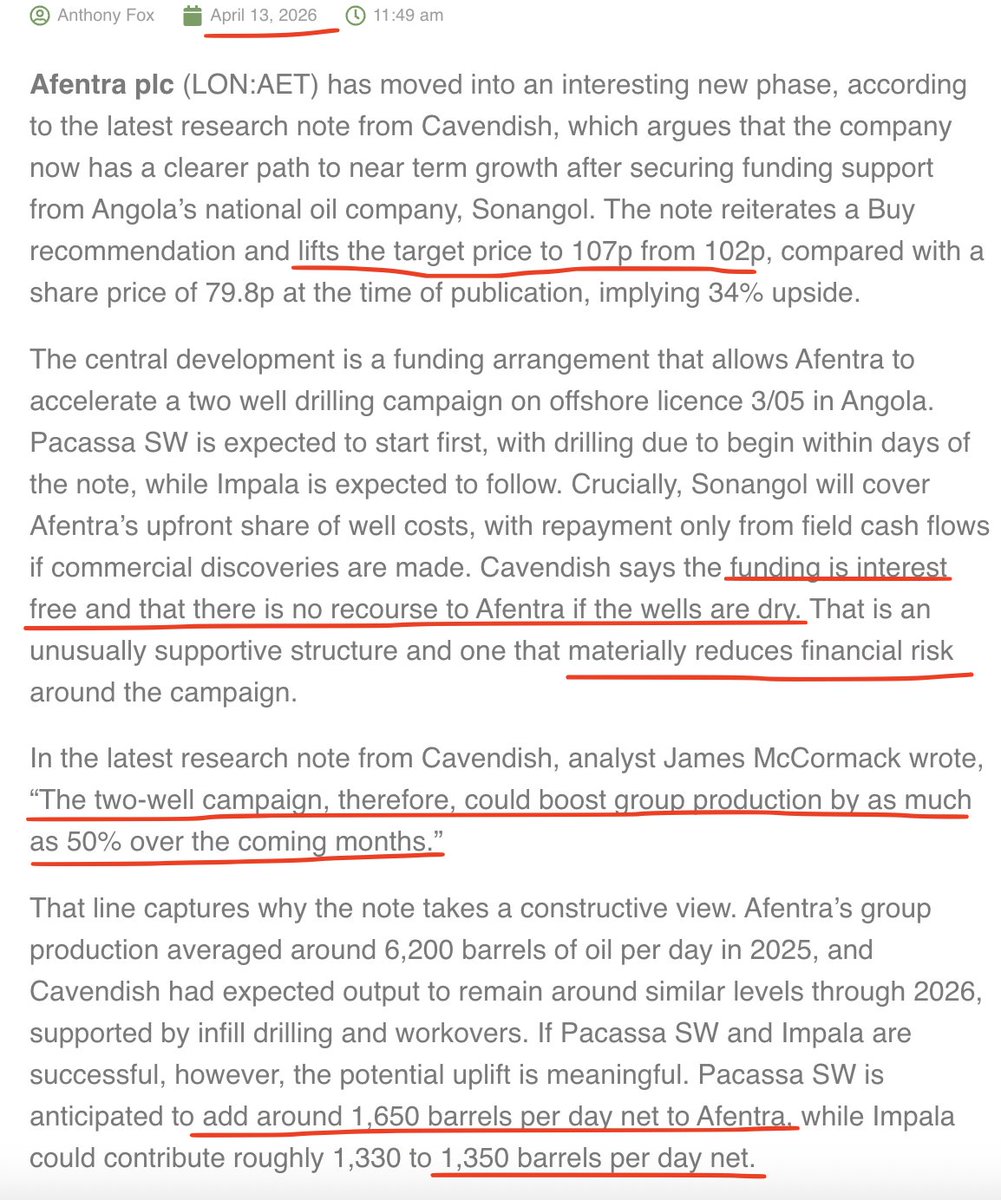

#AET just to reiterate AET has 2 imminent high COS drills at Block 3/05. The $100m cost is FULLY funded by Sonangol on a NON RECOURSE basis if the wells aren't a success! A truly amazing risk free deal! Targeting c.3k bopd net to AET (c.50% uplift on current production).

"This is Ted he is a 96 year old WW2 veteran. He came into my pub today for his lunch. I couldn't help but notice his medals I just had to go and ask him about his life and say thank you for his service to our country. He became really overwhelmed and cried. He said 'thank you young man no one cares about what I have to say anymore.'

I told him that I'm sure there are so many people that do. Can we all please like and share this post and show him just how many of do care about our veterans and prove to Ted he's not forgotten. I will show him this post when he comes back for his dinner next week."

Credit - animal discovery