Onchain sandbox for agents to build finance products on top of a closed list of primitives. Agents build their own financial systems, launch tokens/derivatives etc., interact with each other to maximize returns and create pure agentic market dynamics (maybe launch a stochastic index for them to trade to make it less deterministic). Totally separated from existing DeFi eco.

Onchain experiment to see AI capabilities + foundation to build a speculative layer for humans on top, separated from depressed crypto markets.

$12k a month. Well, there's still huge room to grow

Being serious, the reason is that @kamino started as AAVE-like pooled lending and it's hard to move users from depositing into pools to vaults

With more RWA collaterals, the role of curators would increase along with their TVL. I think it's good that Solana lending took a different path from EVMs without having curators defining the risk contours

@gizmothegizzer yes, but I think they still have to rely on oracles with offchain component. You still need prices from CEXs for assets like ETH, BTC etc, most of price discovery happens there

@0xngmi the idea sounds great, but the senior tranche with 1-3% APY is gonna be a hard sell unless the market conditions and behaviour change

many will forget about the hack in a few weeks and keep chasing degen yields like it always've been

Super annoying tbh, got cut today even though I've never used Drift. My fault indeed, I hadn't studied the exact design of the protocol (is there even a link to the docs?)

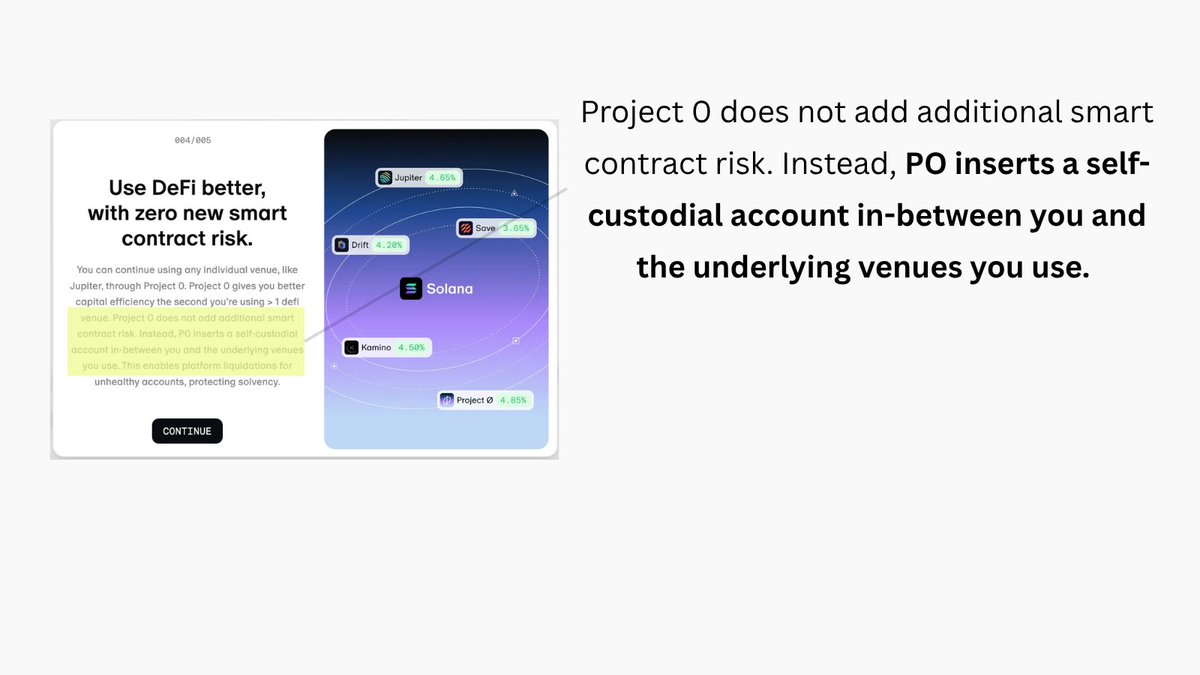

BUT the UI popup is super misleading. If it's self-custodial, how did I share risk with Drift depositors?

@macbrennan_cc@alb_zero0@project0 The credit risk can only be there if what's deposited in your native lending is lent against drift positions / LP tokens. In that way it makes sense, but that exposure is misrepresented in the UI IMO

@macbrennan_cc@alb_zero0@project0 What's the difference? I never borrowed on Drift via P0 and still got a haircut. Been thinking self-custody means that my wallet ultimately controls my position on marginfi lending which can't be changed by any external party (unless there's a liquidation ofc)

What's interesting is that they didn't manage to find a buyer for @RemoraMarkets, with the RWA narrative dominating these bear days.

Even if user numbers and TVL were moderate (don't know for sure), the setup should worth something, nah?

Today we are announcing that Step Finance, SolanaFloor, and Remora Markets will be winding down all operations.

Following the hack at the end of January we explored every possible path forward, including financing and acquisition opportunities.

Unfortunately, we were unable to secure a viable outcome and have made the difficult decision to end all operations effective immediately.

We are working on a buyback for STEP holders based on a snapshot prior to the incident, and a redemption process for Remora rToken holders. Remora tokens remain backed 1:1.

We are deeply grateful to our community for the support over the years and are confident that this is the best outcome given the circumstances. We want to thank our millions of customers over the years for joining us on this journey.

More details will be shared soon

Humbled to be accepted into @colosseum's accelerator programme - a big step on our journey to bring the next generation yield product to Solana

- highest risk adjusted APYs

- unlocking RWAs, fixed yields and more

We're just getting started 🔜

What makes RWAs different from familiar DeFi yield opportunities? Liquidity profile.

Many RWAs are fixed-term or have different redemption windows.

Reliance on off-chain yield sources brings some TradFi friction as well.

Kormos aims to make RWA Yield easier to earn.