Top Tweets for #ACLD

#SME #ACLD #AeleaCommodities

Aelea Commodities H2 FY26 Earnings Conference Call Highlights

👉 FY27 & Future Outlook:

▫️ Management expects continued growth momentum in FY27 with similar trajectory to FY26 (no specific numbers were guided due to regulatory constraints).

💠 Growth to be driven by deeper value-chain integration (farm-gate and origin-level sourcing), improved RCN quality mix, higher recovery rates (targeting better whole vs. pieces ratio), and initial contribution from Phase II (CNSL oil extraction + rooftop solar already operational).

💠 EBITDA margins expected to sustain/expand around 10-11% industry levels; deeper sourcing improves margins but increases short-term finance costs (which are expected to remain elevated or rise further in absolute terms as scale grows).

▫️ Long-term 2037 Vision (10-year strategy):

💠 Cashew processing capacity scale-up to 1,000 MTPD (from current 140 MTPD)

💠Focus on full value chain — food (kernels + value-added), fuel (biofuels, CNSL), feed, and fertility (by-products like biochar, activated carbon).

💠 Expansion into other nuts & fruits (almonds, walnuts, dates, pistachios, makhana) with significant processing capacities and 50% targeted towards retail/value-added/institutional segments; plan for ~100 premium retail stores (mostly franchise).

💠 Green energy & sustainability push via Aelea Green Energy Ltd subsidiary: biodiesel, bioethanol, green thermal power, soil amendments, bio met coke, green steam, etc.

💠Plans to enter “three whites” (rice, sugar, wheat) later in the decade with Africa-linked and India-centric value-added focus.

💠 ESG angle: ~3,000 direct + 50,000 indirect jobs (rural & women-focused), major reduction in carbon emissions/logistics, closed-loop water systems, and certified sustainable biofuels.

👉 Current Projects, Capacity & Future Pipeline:

▫️ Current Operations:

💠Unit II (Surat) at healthy ~94-95% capacity utilisation in FY26.

💠Processed ~16,000 tonnes RCN in H2 FY26 (similar in H1).

💠Sourcing mix ~95% African origins (60-65% through direct/sea-transit level via merchant traders), ~5% local.

▫️ Phase II (CNSL oil extraction facility ~50 MTPD + solar):

💠Construction largely complete; rooftop solar already executed and contributing savings; ground-mounted solar pending government approvals (policy changes).

💠Commercial benefits (power cost savings + CNSL revenue) expected from H2 FY27.

💠CNSL to primarily boost bottom line (target ~10% EBITDA margin on this product) rather than top line.

▫️ Unit III / Phase III:

💠Land acquisition completed; focus on Cardanol, Bio Charcoal, and De-oil Cake production.

💠Preparatory work ongoing with emphasis on renewable energy integration and by-product valorisation.

💠Expected post-stabilisation of Phase II; capex to be incurred in later part of FY27 / FY28.

💠 Two wholly-owned subsidiaries incorporated: Aelea Green Energy Limited (renewable & sustainable energy) and Aelea Nuts & Fruits Limited (food processing, FMCG, value-added agri products).

▫️ Branded Retail & Exports:

💠Continued expansion of branded portfolio across retail & e-commerce (currently ~1% of sales via B2C consumer pouches).

💠Focus remains primarily institutional/B2B for better margins and visibility, though organic B2C growth is planned as part of the 2037 basket approach.

👉 Other Notable Points:

▫️ Finance cost rose sharply (from ~₹2 Cr to ~₹8 Cr) due to deliberate deeper value-chain sourcing (better margins but reduced supplier credit).

💠Inventory increased with scale (expected to rise further).

💠Working capital intensive business due to commodity nature and value-chain expansion.

▫️ Strategic & Operational Highlights:

💠FSSC 22000 certification obtained for Surat facility (boosting export readiness).

💠Multiple awards including Fairdeal Filaments MSME Entrepreneurship Award, Gold Membership from NDFC, CFO Vault Excellence in Cost Optimization, and MSME Star Stories 2025. CRISIL outlook revised to BBB/Stable.

💠 Management emphasis on conservative yet aggressive growth, “giving hand” philosophy, and long-term survival + compounding (reflected in logo symbolism).

▫️ Q&A Key Takeaways:

💠Margins in FY26 aligned with guidance (10-11% EBITDA); no major hiccups beyond expected finance cost increase from value-chain deepening.

💠B2C currently minimal (1%); no heavy ad spend planned — focus on organic/profitable growth and multi-product basket.

💠Geopolitical tensions (Red Sea etc.) caused longer transit times but no major price impact yet; management monitoring closely.

💠Recovery mix averaged ~63% wholes / 37% pieces; kernel realisation ~₹590-595/kg.

💠No immediate dilution or excessive debt concerns; back-to-back hedging model for inventory.

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

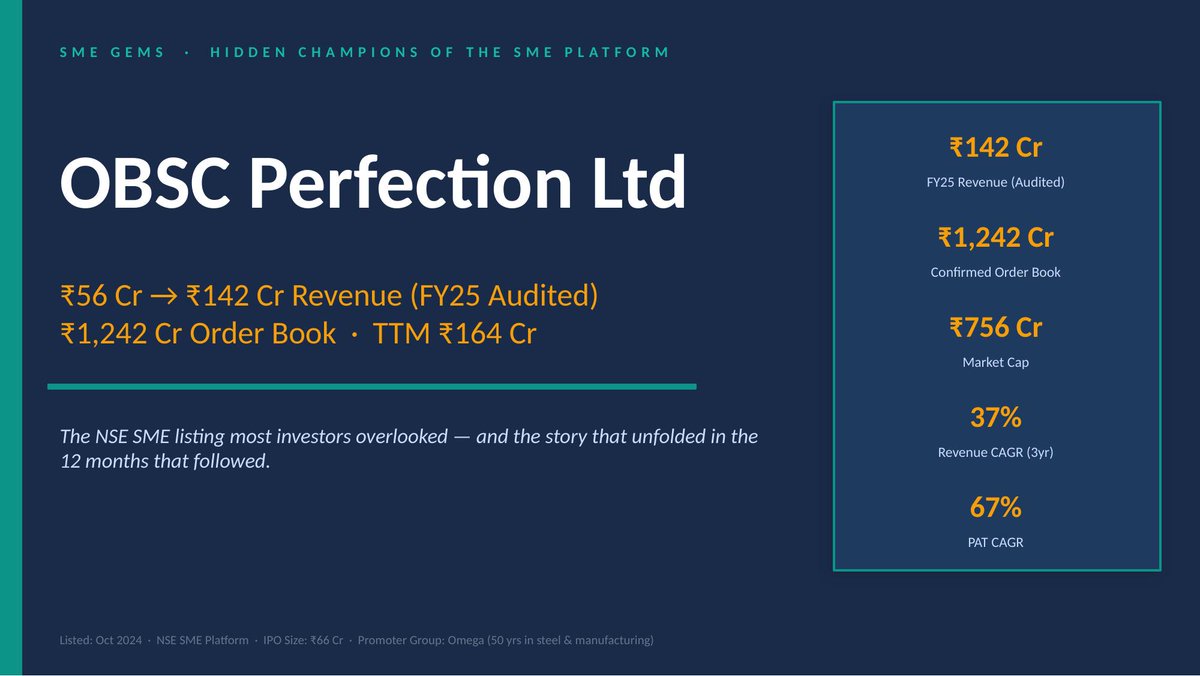

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

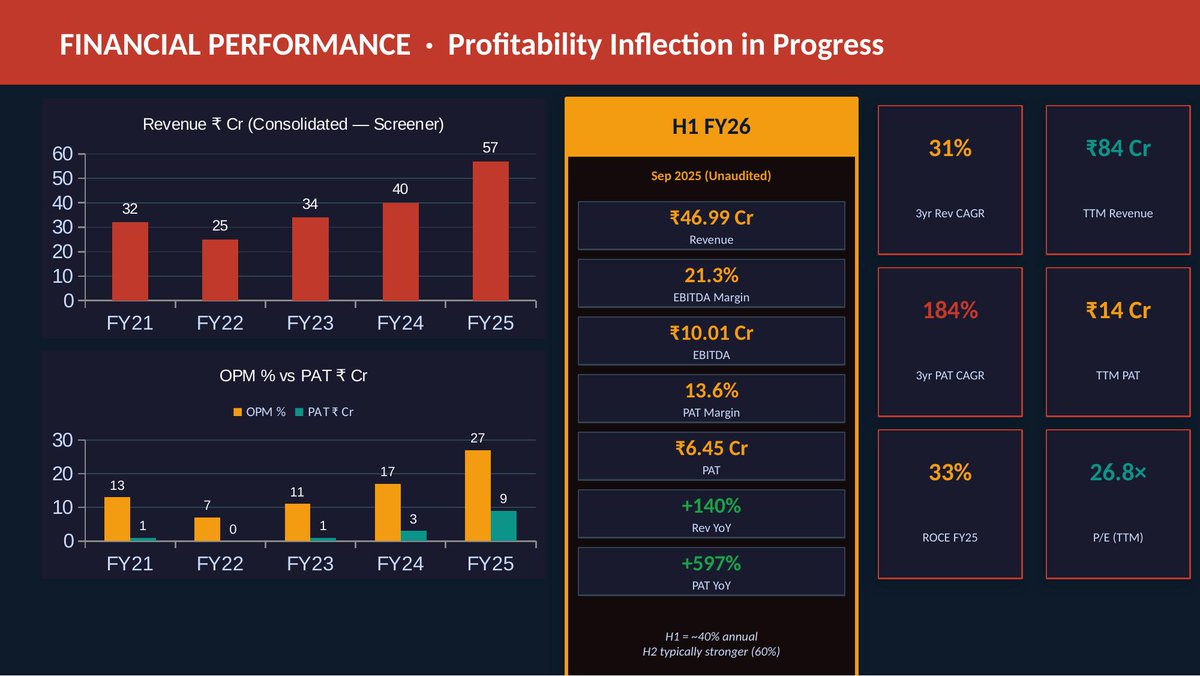

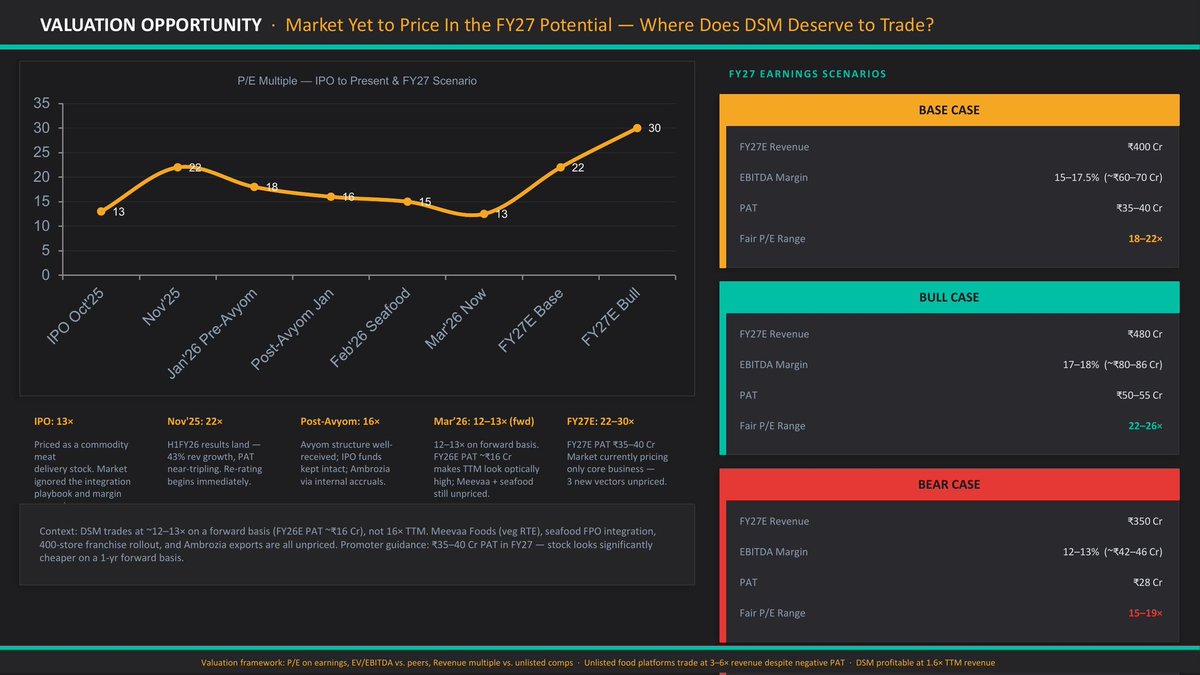

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 https://t.co/Sto1a1qHIQ

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

We are proud to announce that Dr. @balcar_lorenz has successfully defended his #PhD @MedUni_Wien on #coagulation, #bleeding, & #thrombosis in #acld

Congratulations 🥳🥳

Arihant Bharat Connect Conference March '26:

👉Day 1:

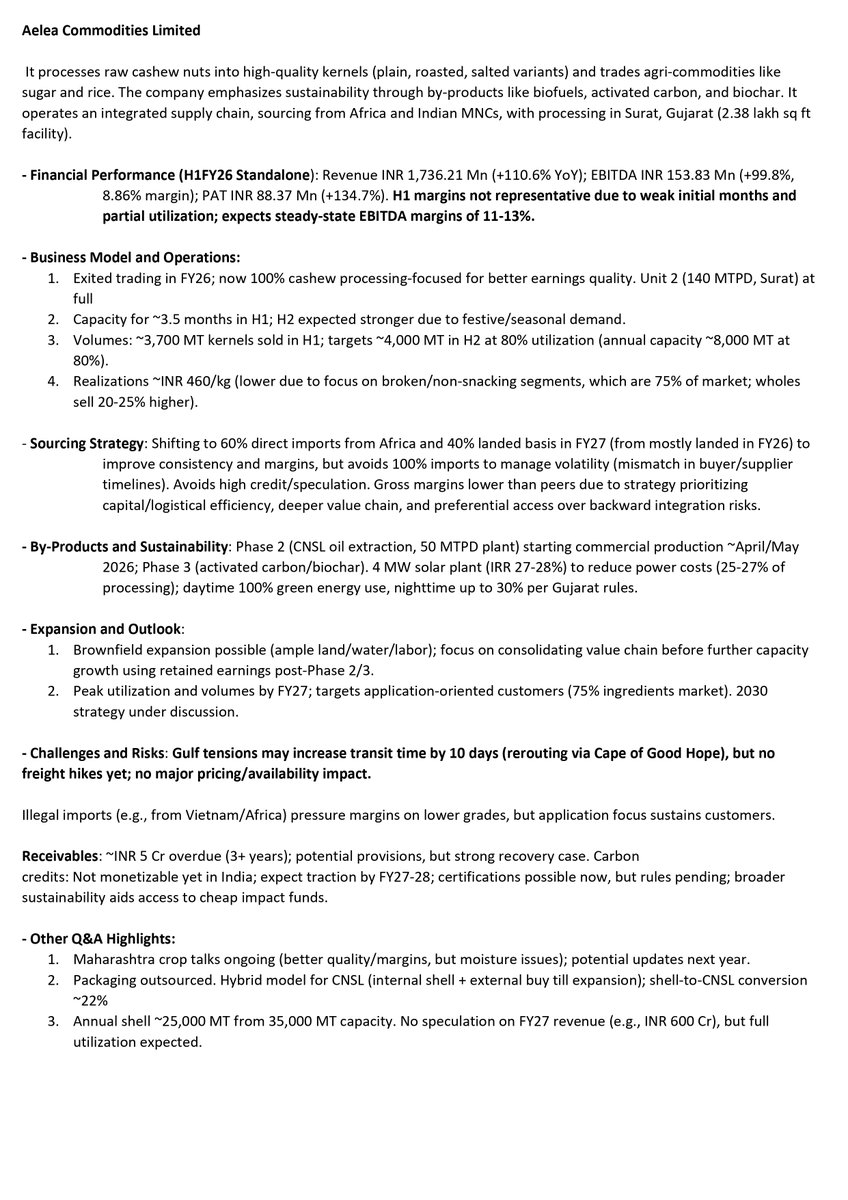

💠Aelea Commodities

💠Utssav CZ Gold Jewels

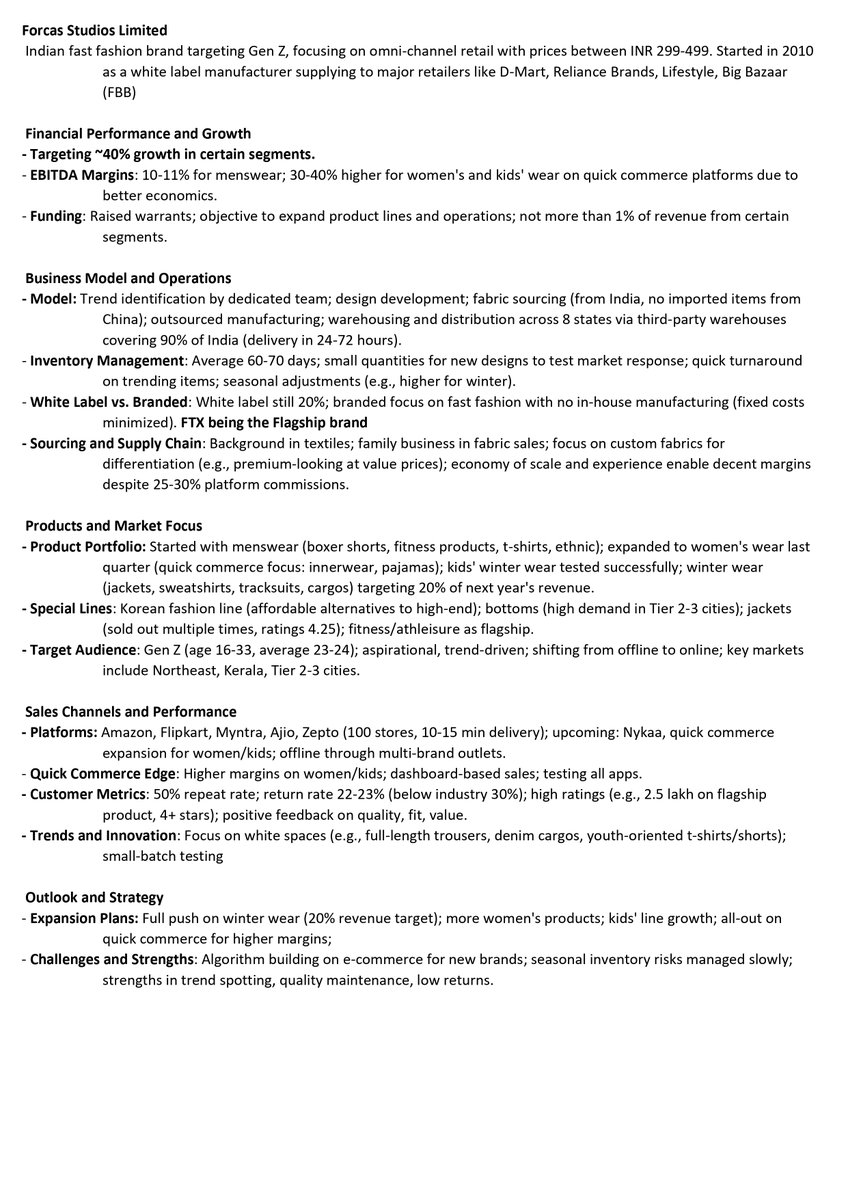

💠Forcas Studios

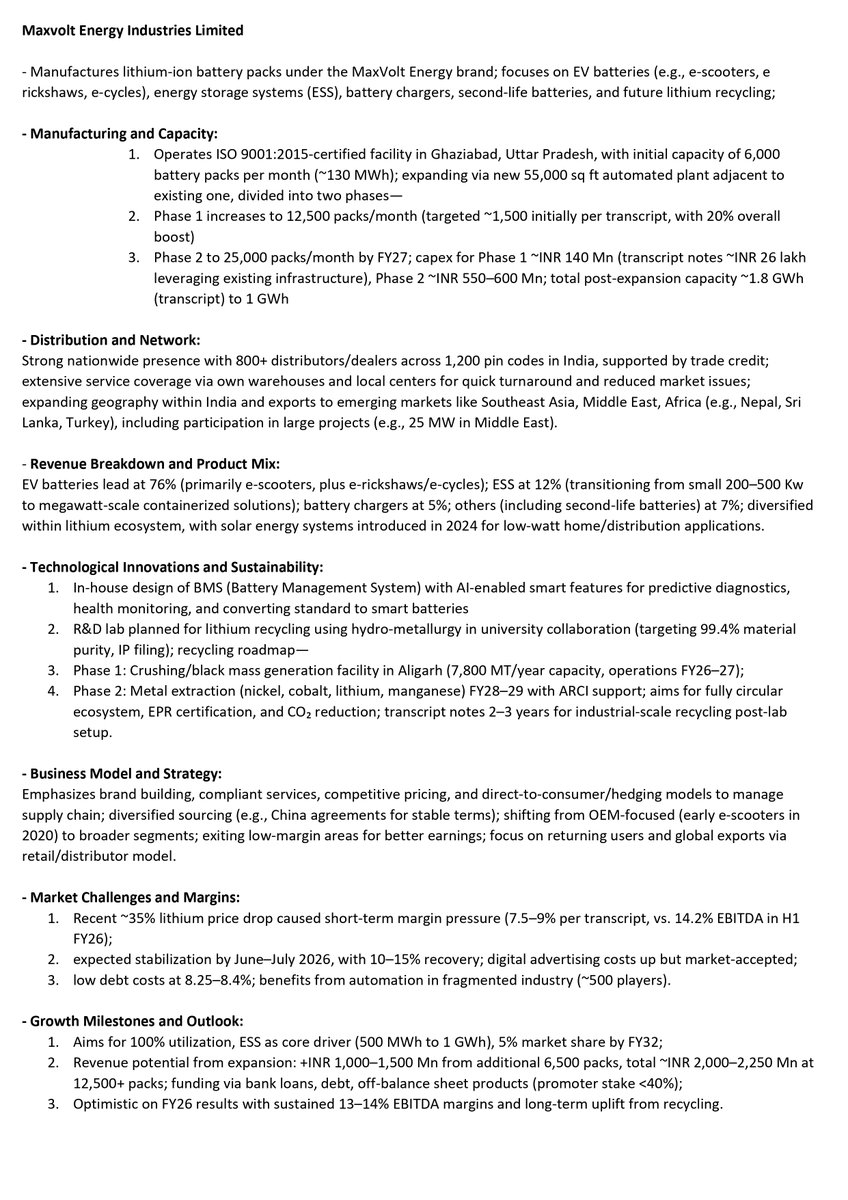

💠Maxvolt Energy Industries

💠AVP Infracon

#aelea #acld #utssav #forcas #avpinfra #avpinfracon #maxvolt #maxvoltenergy #utssavcz #bharatconnectconference #arihantcapital

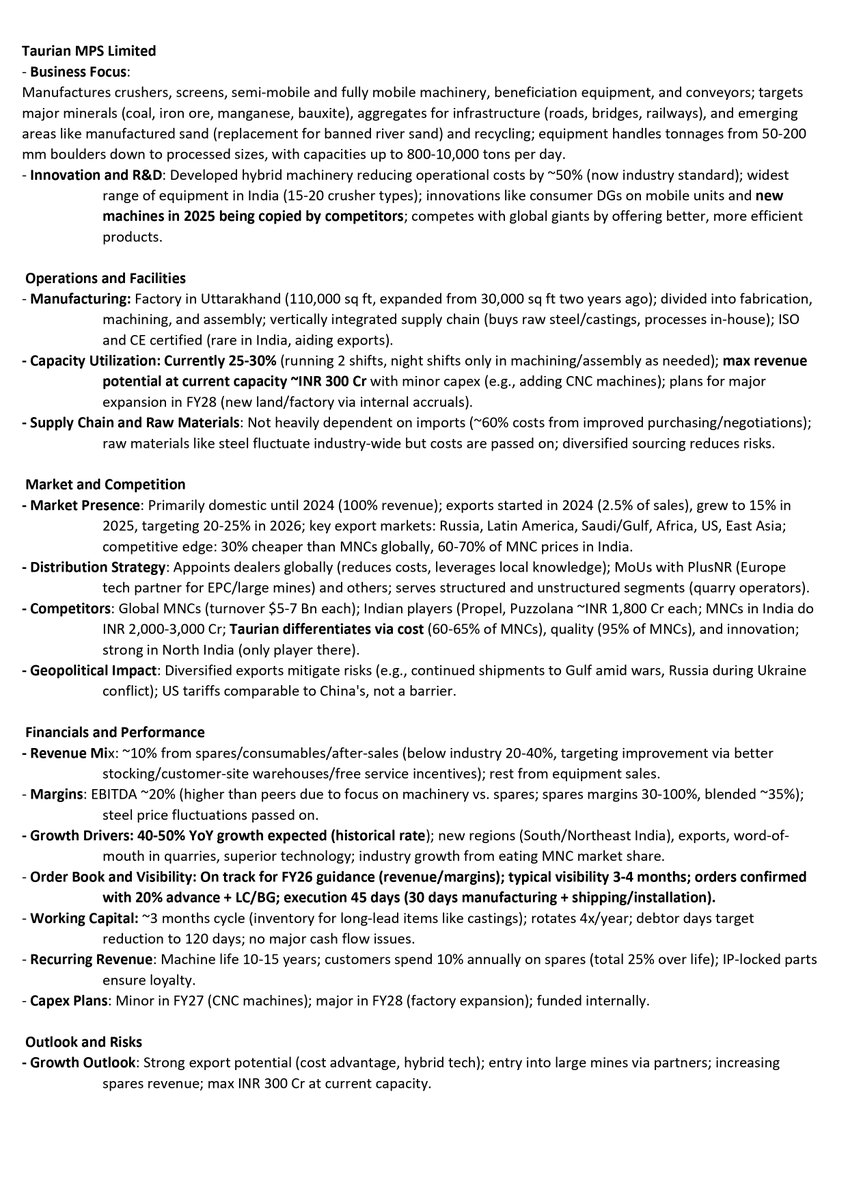

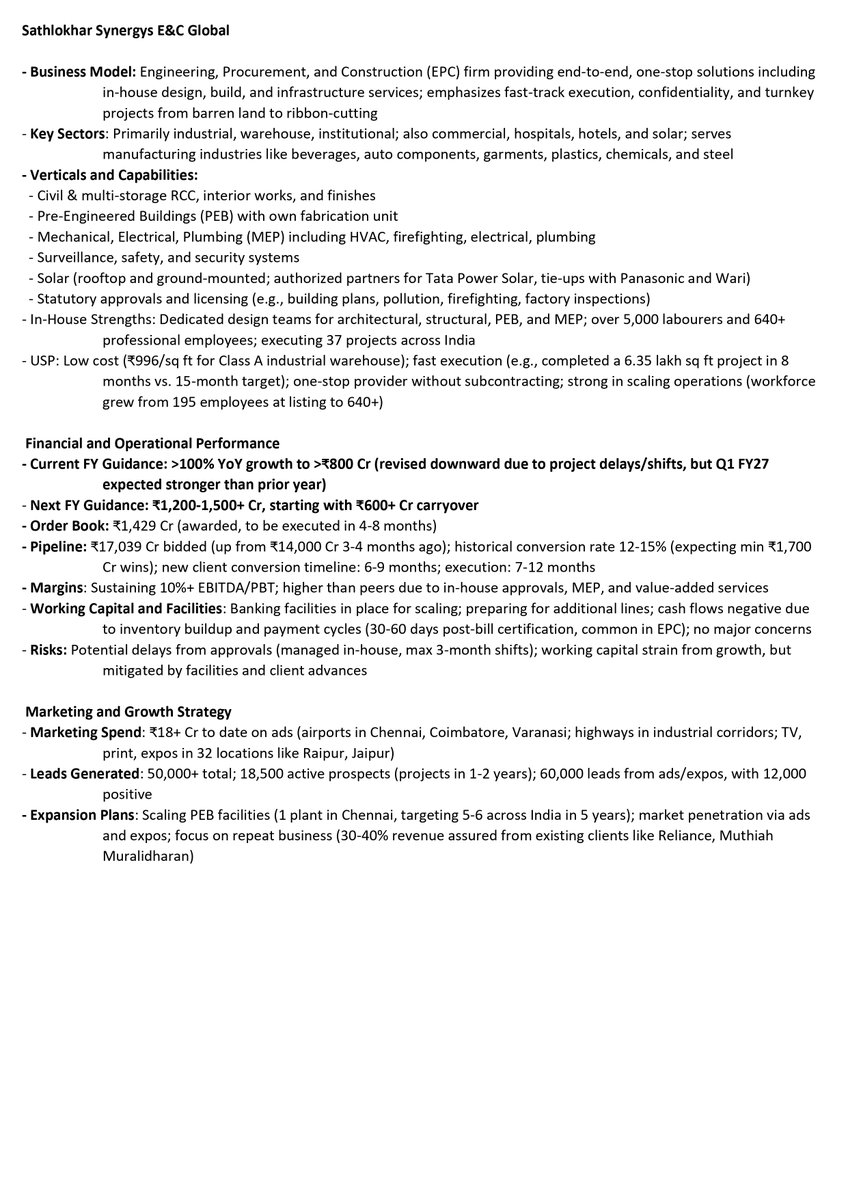

Arihant Bharat Connect Conference March '26:

👉Day 1:

💠Sathlokar Synergys E&C Global

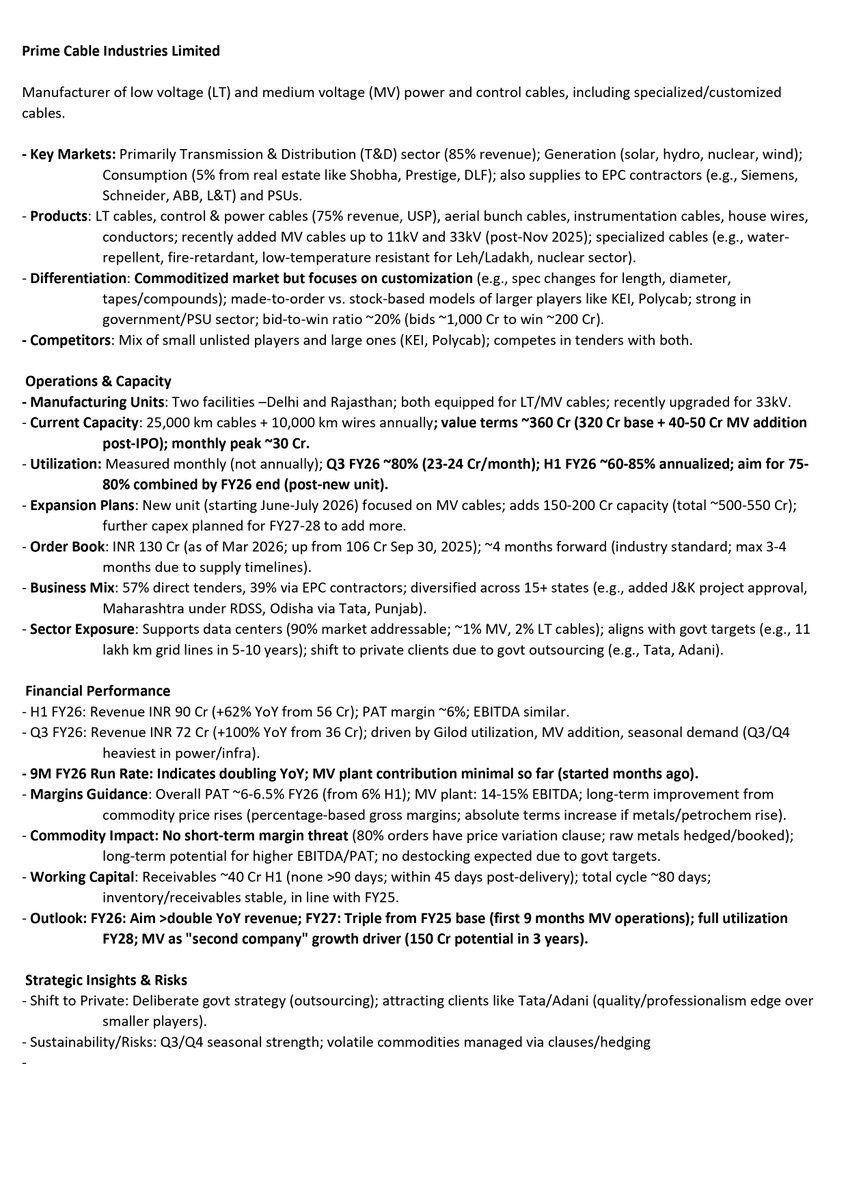

💠Prime Cable Industries

💠Taurian MPS

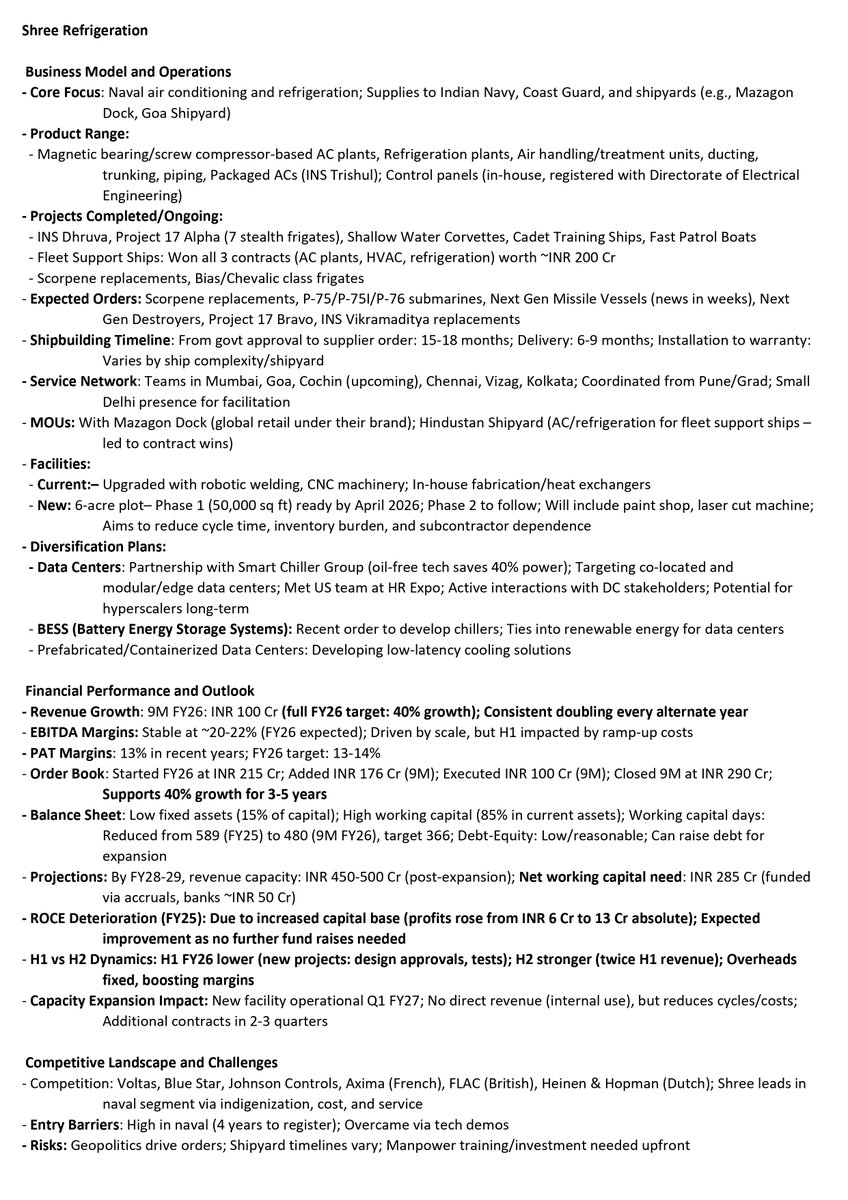

💠Shree Refrigerations

💠Silkflex Polymers

💠Classic Electrodes

💠TBI Corn

💠Dar Credit & Capital

#sathlokar #ssegl #primecab #primecableindustries #taurian #taurianmps #shreeref #shreerefrigerations #silkflex #classiceil #tbi #tbicorn #dccl #darcreditandcapital #bharatconnectconference #arihantcapital

Thanks to all the speakers - great range of really engaging talks - clinical service developed and research @basl_events @BASLedu #palliativehepatology #ACLD

There’s still time to register! @basl_events

Annual BASL palliative hepatology SIG meeting 🙌🏼

11th December 2025

Birmingham

Multiprofessional

Free attendance

Hybrid F2F and online

Contact [email protected]

#ACLD #palliativehepatology #cirrhosis

@TerryYip12 @CMH_journal @CUHKGI @CUHKMedicine @VWSWong @wonglaihung @JimmyLaiCT @JinXinrui_Dawn Nice work @TerryYip12 !

Dr. Hartl @hartl_md also found that #LowT3 was associated with #ACLF and #Mortality in a #cirrhosis #ACLD cohort including - but not limited to - MASLD patients:

https://t.co/tsz9b2oLIc

Really looking forward to the #BASL Palliative Hepatology annual SIG meeting in Birmingham - hybrid - details below - there’s still time to register to attend! Fantastic speakers, lots of experience and research updates #palliativehepatology #ACLD

Registration open:

contact [email protected] to join - Limited places available.

Date: Thursday 11th December

Time: 9:30AM - 4:00PM

Location: Austin Court, 80 Cambridge Street, Birmingham B1 2NP

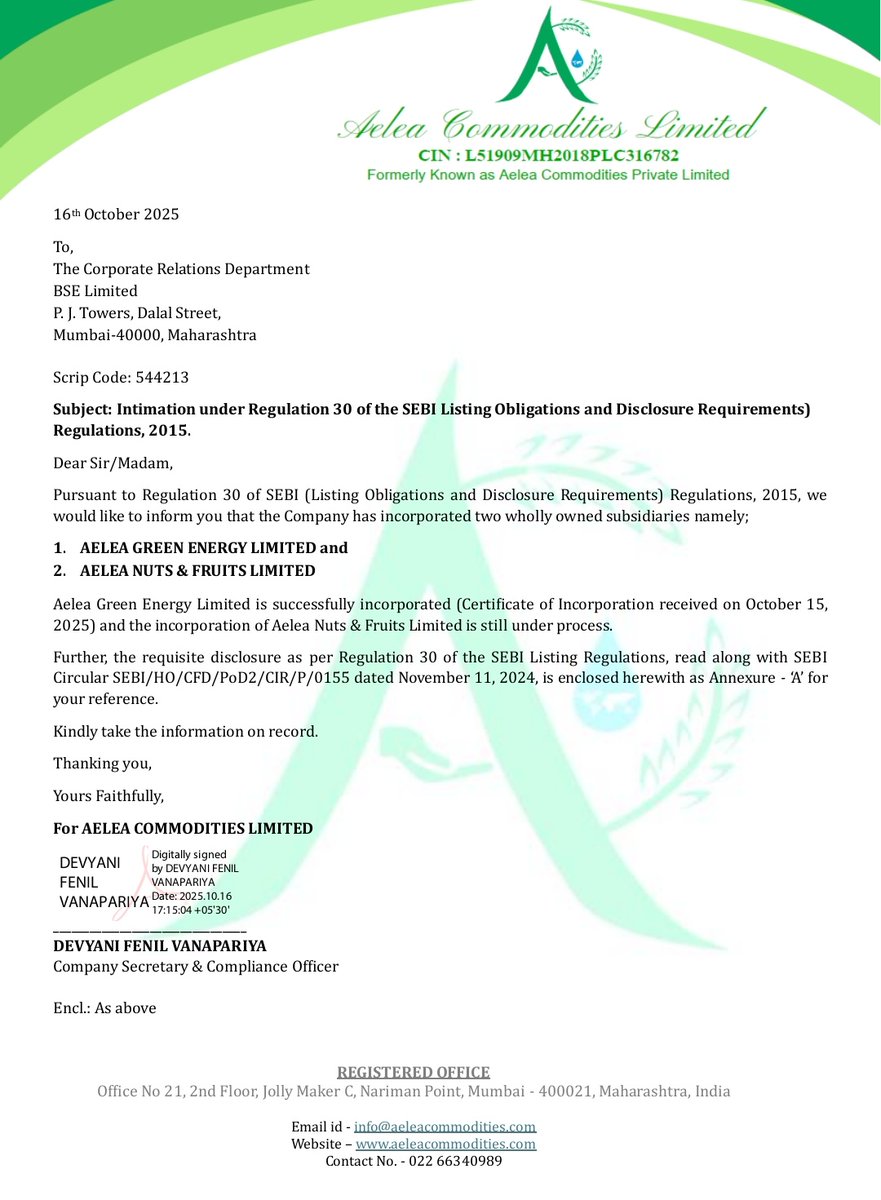

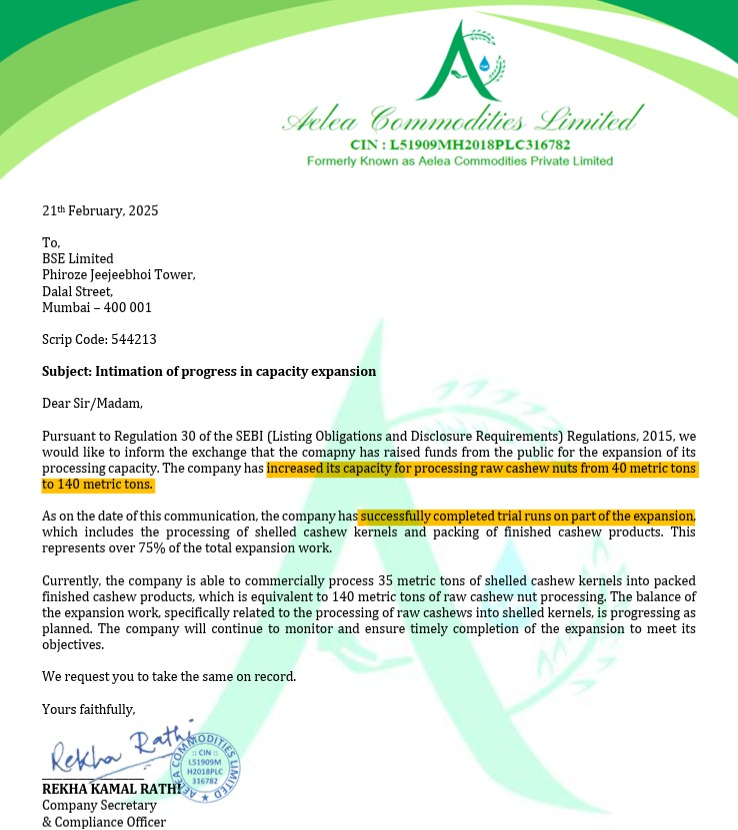

#SME #AeleaCommodities #ACLD #Aelea

Aelea Commodities H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️ Expecting to breach the ~400cr+ mark with H2 FY26 at full capacity, targeting H2 > H1 due to seasonality and utilization

💠No fixed top-line due to commodity price fluctuations (RCN prices down 17-18% in last 12 months).

💠No trading revenue in FY26

▫️EBITDA ~12-13% average margin annually; H1 at 8.9% (impacted by low Q1 utilization ~40 MTPD); H2 expected at 13-14%+ with leverage, covering Q1's near-negative EBITDA

💠Cost-plus model with back-to-back hedging minimizes some volatility; gross margins ~15% (H1 FY26) vs. 20% (H1 FY25) due to natural output variations (±3 days inventory risk)

💠Volumes: ~3.5 months at full 140 MTPD in H1; full H2 at 140 MTPD (adjusted for holidays)

💠Commodity prices (downward trajectory stabilizing); 6-7% annual consumption growth

💠New subsidiaries (Aelea Green Energy) to support by-product revenue streams for margin enhancement

👉Projects and pipeline:

▫️Current Processing Capacity:

💠Surat facility handled H1 volumes equivalent to ~3.5 months full run-rate; Utilization: 100% since July'25; latent demand absorbs output (no stockpile issues)

💠Input-Output: ~1 ton RCN yields 230 kg edible kernels, 70 kg shell (22% CNSL oil ~144 kg, balance de-oiled cake/charcoal 50-55% yield); shells/skins sold as scrap currently

💠By-Product: CNSL/De-oiled cake sold as-is; preparatory work advanced

▫️100% processing revenue; branded gaining B2C traction (retail/e-commerce). Targeting diversified mix

▫️ Recent announcements : Aelea Green Energy Ltd. (100% subsidiary): Handles renewable ecosystem, carbon credits (EU exports)

💠Aelea Nuts & Fruits Ltd. (under incorporation): Potential for value-added food lines

▫️Pipeline:

▫️ Unit III Land acquired (~412,000 sq ft); integrate 4 MW solar for power (25-27% of processing costs; captive solar at 30-35% grid cost)

💠Total target: ~240 MTPD by FY27

💠Direct RCN sourcing from Africa (Côte d’Ivoire, Benin, Tanzania) + Indian MNCs; 65% imported crop

💠Unit III construction post-monsoon; solar orders placed. Capex Phase 1 complete

💠Phase 2: CNSL oil processing (Cardanol for automotive/chemicals)

💠Phase 3: Convert to biofuels, activated carbon, biochar (waste-to-wealth; export premiums via sustainability certifications)

💠Capex : Phase 2 ~20-30cr (internal accruals). IRR ~27-28% on solar (3-4 year payback, no subsidies). Construction resumes Q3 FY26; completion by FY26-end or Q1 FY27

💠Forward integration: Private labels, vegan/dairy-free innovations; CNSL in pharma/automotive

💠Export growth: 6-7% consumption rise; premium for certified green products. No volume targets shared

👉 Others :

▫️Financials: Q1 revenue ~50cr (at 40 MTPD), Q2 ~120cr; H2 monthly run-rate ~40cr

💠Borrowings reduced via supplier credit (enables scale without WC strain)

💠Tax rate higher in September due to deferred liabilities (final at FY-end)

▫️Sourcing & Risk Management: Continuous back-to-back buying/selling with 80-90 day inventory; natural product variations cause minor gross margin volatility

💠Track prices via dynamic factors (quality, moisture, origin)—no standard benchmark shared due to variability

▫️Competition & Differentiation: ~2,000 Indian processors (95% <10 MTPD, South/Maharashtra-heavy; low mechanization)

💠Differentiates being in Western India hub, 140 MTPD scale, AI-imported tech (China/Europe, not in Vietnam/Africa), integrated chain (kernels to biofuels)

Good #Q2FY26-15/10/25 till 6pm

Aelea Commodities

#ACLD

#Aelea

Comeback quarter

Good H1FY26

Rev at 173cr vs 87cr, H2 at 93cr

PBT at 12.4cr vs 6.8cr, H2 was a loss qtr

PAT at 8.7cr vs 5.5cr, H2 was a loss qtr

OCF at 23cr vs 9cr

Inventory at 90cr vs 49cr, H2 should be big

Oberoi Realty

#OberoiRlty

#OberoiRealty

Solid Q2FY26

Rev at 1779cr vs 1319c4, Q1 at 987cr

Other income at 65cr vs 38cr, Q1 at 86cr

PBT at 993cr vs 782cr, Q1 at 507cr

PAT at 760cr vs 589c4, Q1 at 421cr

Good QoQ and YoY uptick

OCF at 898cr vs 1506cr

KEI Industries

#KEIInd

#KEI

Good Q2FY26

Partially led by higher other income at 42cr vs 12cr

Rev at 2726cr vs 2283cr, Q1 at 2590cr

PBT at 277cr vs 207cr, Q1 at 263cr

PAT at 203cr vs 154cr, Q4 at 196cr

OCF at 383cr vs -308cr

Ador Welding

#Ador

#AdorWelding

Solid Q2FY26 on a lower base

Good recovery quarter with solid margin expansion QoQ and YoY

Rev at 281cr vs 269cr, Q1 at 252cr

PBT at 34cr vs 19cr, Q1 was a loss qtr

PAT at 25cr vs 7cr, Q1 was a loss qtr

OCF at 42cr vs 60cr

Tips Music

#TipsMusic

Growth rate reducing, down to 12-15% vs consistent 30s that company used to clock earlier

Rev at 89cr vs 81cr, Q1 at 88cr

PBT at 72cr vs 64cr, Q1 at 62cr

PAT at 53cr vs 48cr, Q1 at 46cr

OCF at 46cr vs 48cr

GTV Engineering

#GTVEngg

Rev at 25cr vs 24cr, Q1 at 17cr

Other income at 1.3cr vs 0.2cr

Good margin expansion

PBT at 4.6cr vs 1.6cr, Q1 at 2.7cr

PAT at 3.5cr vs 1.1cr, Q1 at 2cr

Good QoQ and YoY growth

OCF at 6.2cr vs 2.3cr

Huhtamaki India

#Huhtamaki

Rev down, margins expand well QoQ and YoY

Rev at 624cr vs 652cr, Q1 at 612cr

PBT at 49cr vs 14cr, Q1 at 33cr

PAT at 37cr vs 12cr Q1 at 25cr

Summit Securities

#SummitSec

Rev at 120cr vs 107cr, Q1 at 27cr

PBT at 118cr vs 106cr, Q1 at 27cr

National Fittings

#NatFittings

Rev at 24cr vs 19cr, Q1 at 21cr

PBT at 2.7cr vs 0.9cr, Q1 at 3.6cr

PAT at 1.8cr vs 0.8cr, Q1 at 2.6cr

OCF at 2.6cr

Decent:

#Ksolves

Good uptick QoQ,marked improvement

YoY degrowth continues in margine

#HDFCAMC

Lower mark to market gains this qtr

#HDFCLife

Expensive valns for these numbers

#KKCL

Decent rev uptick, margins down

@ViennaLiverNews Retreat Weekend 2025

Big Thanks 🙏 to all #VLSG & @LBG_research @CrgMotion Team Members for the great discussions & defining the Mission #2025 for the @MedUni_Wien program for #Cirrhosis #ACLD and #PortalHypertension

Most Popular Users

Elon Musk

@elonmusk

240.3M followers

Barack Obama

@barackobama

119.3M followers

Donald J. Trump

@realdonaldtrump

111.6M followers

Cristiano Ronaldo

@cristiano

109.6M followers

Narendra Modi

@narendramodi

106.9M followers

Rihanna

@rihanna

97.4M followers

NASA

@nasa

92.1M followers

Justin Bieber

@justinbieber

90.7M followers

KATY PERRY

@katyperry

87.2M followers

Taylor Swift

@taylorswift13

81M followers

Lady Gaga

@ladygaga

72.6M followers

Kim Kardashian

@kimkardashian

69.6M followers

Virat Kohli

@imvkohli

69.1M followers

YouTube

@youtube

68.6M followers

Bill Gates

@billgates

63.6M followers

The Ellen Show

@theellenshow

62.5M followers

CNN

@cnn

61.9M followers

Neymar Jr

@neymarjr

61.8M followers

X

@x

60.9M followers

Selena Gomez

@selenagomez

60.3M followers