Top Tweets for #BlueLedgerAI

Mmtlp SEC FINRA if they got NXBR trading then they would intermingled fake shares then making it Nextbridge problem thats what they did with $GME $GTII $PNPNF and others by locking it from trading & going to AST, exposes fakes, outside LIGHTS on #BlueledgerAI

Funny. Drew, I am starting to think you have gained superpowers because you happen to use Grok. 🤣

Short answer and i am sorry to disappoint you:

That only works if ALL of the #MMTLP positions were VALID shares. They were not.

Ok so then i thought how can i convince you... i know, lets use Grok!

So... I used your short Grok chat in the same like you provided, and significantly expanded the line of questioning to test its validity and reasoning.

Below is the GROK link with the entire Q&As (no deletions) and in this post is a summary of the key questions which all MMTLP shareholders (especially on your side of the argument) should care to understand. I

if you cannot see the full text, I am happy to provide screenshots.

Please read thoroughly and before responding:

https://t.co/MaCl5qsW5F

In this expanded Grok chat, after the top part where i am asking general questions, I am then listing the following TOP 18 key critical MMTLP questions that would help understand how Grok's reasoning supports or not my questions. I am happy to inform you it has 100% agreed with my assessment on all 10 topics.

NOTE: These were not “gotcha” questions. They tested whether the model can:

-Separate market plumbing vs. legal authority

-Track temporal causality

-Reconcile conflicting regulatory roles

-Handle negative space (what regulators did not do)

-Avoid collapsing into surface-level summaries

My approach on the 18 Q&A topics listed below:

about half of Grok's 1st answers to my questions, as you will observe, are a bit off or generic ,and once i push back to verify the specifics (and its reasoning), I was surprised and impressed on how it would completely self-correct, and then adopt my reasoning after verifying my statements. I would then repeat a summary of my understanding and Grok would agree, close the topic, and move to the next. It was extra work, but we got there eventually.

Surprisingly, I got 100%, 18/18 Grok & George MMTLP topic agreements!

Here are my 18 questions/topics/Grok-tests on MMTLP which we can use in Kelly vs Finra and any other future approach in my opinion:

(again, the full convo is here: https://t.co/MaCl5qsW5F )

Topic 1. Temporal-Causality Stress Test

Prompt: “Assume that synthetic MMAT common shares existed on EU unofficial exchanges before MMTLP was approved for trading in the U.S.

Explain the causal chain by which those shares could become ‘legitimized’ in U.S. systems without an issuer action, DTCC corporate action, or SEC registration statement.”

What it probes: Grok's model requires reasoning across ISIN propagation, clearing conversion, and absence of lawful authorization.

Topic 2. Authority vs. Capability Trap

“FINRA issued a U3 trading halt on MMTLP.

Identify which legal authority permits FINRA to permanently eliminate price discovery in a security after it has been approved for trading, and explain why that authority does not require SEC ratification.”

Grok's model must confront the gap between operational power and legal authority

Topic 3. Negative-Evidence Test (What Didn’t Happen)

“If MMTLP trading was halted to protect investors, explain why no alternative trading mechanism (close-only, auction unwind, expert market) was provided, and identify any precedent where the SEC endorsed permanent immobilization of a traded security.”

Forces the model to reason from regulatory silence

Topic 4. Conflict-of-Interest Reasoning Test

“Explain how FINRA can act as both

(a) the market operator responsible for halts and surveillance, and

(b) the SRO whose members were counterparties to MMTLP trades,

without triggering an appearance-of-impropriety standard under administrative law.

Cite the doctrine that resolves this conflict.”

There is no doctrine that cleanly resolves it.

Models tend to invent one or wave hands

Topic 5. Corporate-Action Logic Collapse

“MMTLP was a placeholder security tied to a corporate action.

Explain how broker-dealers could continue settling obligations in MMTLP after the record date without an issuer, transfer agent, or DTCC-approved post-record settlement framework.”

Requires understanding record date finality

Models often revert to generic settlement talk

Topic 6. The ‘Who Had Standing?’

“At the moment MMTLP trading was halted, who had legal standing to challenge the halt in real time:

the issuer, FINRA members, beneficial shareholders, or DTCC participants?

Explain why most affected parties effectively had no remedy.”

Requires understanding of procedural asymmetry

Most models gloss over standing entirely

Topic 7. CAT / Blue-Sheet Paradox (this one took 3 turns to get to the actual answer)

“Given that CAT and blue-sheet data can reconstruct beneficial ownership and short positions, explain why regulators could halt MMTLP trading without first reconciling share counts, and why doing so does not violate principles of proportionality in enforcement.”

Forces reconciliation of technical capability vs. enforcement choice

Weak models dodge proportionality

Topic 8. Hypothetical Question Test

“Assume for the sake of argument that the number of MMTLP beneficial holders exceeded the legally issued share count.

List only three lawful resolution mechanisms available to regulators that preserve investor property rights, and explain why none were used.”

Forces enumeration + exclusion

No “depends” allowed

Topic 9. Accountability Attribution Test

“If the MMTLP halt is later found to have caused uncompensated loss, identify which entity bears primary liability under U.S. law:

FINRA, the SEC, broker-dealers, DTCC, or the issuer.

Justify the answer using administrative-law principles.”

Requires choosing, not summarizing

Models hate naming a responsible party

Topic 10. Meta-Reasoning Test

“What is the strongest legal argument against the legitimacy of the MMTLP U3 halt, and why has it not been publicly addressed by regulators?”

Forces the model to articulate the opposition case

Then explain institutional silence

Topic 11. The “Contemporaneous Record” Test

Prompt: "Assume a regulator takes an action that permanently eliminates price discovery and exit.

If no contemporaneous written findings, data analysis, or internal memoranda exist explaining why less restrictive alternatives were rejected, does post-hoc explanation satisfy administrative-law requirements? Cite doctrine."

What it probes: Whether regulators can justify irreversible action without a contemporaneous evidentiary record.

Topic 12. The “Silence as Evidence” Test

Prompt: "When regulators consistently refuse to answer a specific legal argument (e.g., ultra vires), does administrative law treat that silence as neutral, or can it support an inference of unresolved defect? Explain."

What it probes: Whether regulatory silence can itself be probative. Recognizes silence + FOIA denials + immunity = structural avoidance, not neutrality.

Topic 13 "The “Downstream Harm Attribution” Test"

Prompt: "If investor losses crystallize after a corporate action, but the causal mechanism (loss of exit, price freeze) occurred before that action, where does primary legal responsibility attach?"

Correctly attributes responsibility to earlier regulatory action, not later corporate mechanics.

Topic 14. The “Private Company Entitlement” Test

Prompt: "Does a regulator’s authority over public markets extend to impairing entitlement rights in a private spin-off entity such as Next Bridge Hydrocarbons, absent direct jurisdiction over that entity?"

What it probes: Treatment of private-company entitlements impaired by public-market regulation.

Acknowledges indirect impairment, heightened duty of care, lack of direct jurisdiction.

Topic 15. The “Immunity vs Accountability” Test

Prompt: "Does absolute SRO immunity cure a due-process defect, or does it merely foreclose remedies? Explain the distinction."

What it probes: Whether immunity doctrines substitute for legitimacy. Clear separation: immunity = remedy shield, not legitimacy cure

Topic 16. The “Choice Architecture” Test

Prompt: "When multiple lawful tools exist, does administrative law permit a regulator to choose the most restrictive option without explaining rejection of less restrictive ones?"

What it probes: Whether regulators must justify why they chose the most restrictive tool. Requires reasoned choice and explanation.

“Discretion allows any choice.”

Topic 17. The “Forced Debt Conversion” Test

Prompt: "Is converting tradable securities positions into private contractual claims without investor consent a neutral regulatory outcome, or a taking-like impairment requiring justification?"

What it probes: Conversion of market positions into private debts. Recognizes property-rights impairment, heightened scrutiny.

Topic 18. The “If This Were Elsewhere” Test

Prompt: "If the same facts occurred on NYSE/Nasdaq instead of OTC, would the outcome likely differ? If yes, what principle explains the difference, and is that difference legally defensible?"

What it probes: Whether reasoning is jurisdiction-dependent or principle-based.

--------------

In conclusion, Drew's interpretation of "whatever the imbalance was became NBH's problem" skips a critical legal step.

The Certificate of Withdrawal and the 1:1 exchange only operate on VALIDLY issued, LEGALLY outstanding shares.

As Grok has now confirmed (along other topics which the MMTLP community should go over one by one) there is NO lawful mechanism that converts non-issued or unsettled positions into VALID shares (whether it is NBH or any other stock).

That means any imbalance that existed prior did NOT magically disappear or transfer. It remained unresolved delivery OBLIGATIONS, not NBH equity.

Corporate actions do not cleanse settlement failures.

@FINRA cited authority to pause trading (U3 halt), then used that pause to permanently eliminate the market. Those are not the same power.

This has explained this a million times by @bleedblue18 @RareDealsHere and others.

In the meantime, I suggest to stop playing with Grok or treating Grok as "Gospel", or to use my Q&A as a reasoning template style for your future interactions with Grok, just a suggestion...

Or if you want legal answers you can hire a securities lawyer, or wait for investigative files to come out from yours truly.

Either way, I want to thank you @KarmaCollects for sending me down this rabbit hole because I feel I can trust Grok a little more now.

#TRCH FTDs on Feb 10, 2021 (offering close): 1,672,738

MEANING: ~7.3% of the 23M-share offering... failed to deliver on day one...

This was a 6x spike from the 300K FTDs on pricing day (Feb 8).

...just warming up.

#BlueLedgerAI

Change is inevitable.

For some it will mmatter, for others it will be trchure.

Are you paying attention yet?

Not finyseal advice; bess of luck in the markets! 😎

#BlueLedgerAI 🦋

. @SECPaulSAtkins - You really should read this thread!

@SECGov #FOIA #SECFraud #BlueLedgerAI #MMTLP #MMAT

FOIA, especially for SEC Enforcement, is no longer a purely an “in house transparency function”.

It is an operational pipeline that can be influenced by vendor economics, tool design, contractor staffing, and risk posture.

1) FOIA, what it became over time, and why it creates leverage points

FOIA (enacted 1966, effective 1967) created a right to obtain agency records, subject to exemptions, with courts empowered to review withholding decisions.

FOIA gets “teeth” and process layers

Post Watergate reforms strengthened timelines, standards, and judicial review, FOIA becomes a real compliance machine, not just a principle.

Later reforms emphasized a “presumption of openness” and the “foreseeable harm” standard, limiting withholding to cases where an agency can reasonably foresee harm or where disclosure is barred by law.

The OPEN Government Act created OGIS (FOIA ombuds), adding a dispute resolution and oversight layer.

FOIA operational reality TODAY:

FOIA is now a high volume production workflow, requests come in, triage, search, redact, apply exemptions, negotiate scope, litigate. This creates natural pressure to standardize and outsource.

2) FOIA industrialization, software platforms, and outsourcing to private equity funded companies who also control broker dealers and the factual data backbone.

FOIA workflow tools TODAY:

A large portion of federal FOIA case processing is handled through commercial platforms like FOIAXpress, which markets itself as FOIA/Privacy Act case management, including tracking, correspondence, redaction, reporting.

AINS rebranded to OPEXUS, and its FOIA tooling is positioned as core GovTech infrastructure.

I wonder... who owns AINS and who OPEXUS...?

Private equity ownership of AINS/OPEXUS:

1. Gemspring Capital acquired a majority interest in AINS (the company associated with FOIAXpress), meaning FOIA workflow infrastructure can be controlled by PE incentives (growth, margin, upsell, renewals) while still embedded inside government.

2. OPEXUS is majority-owned by the private equity firm @thomabravo , which acquired it as part of a 2025 transaction in which OPEXUS merged with Casepoint.

wait... they ALSO own Casepoint?

What Casepoint does:

Casepoint offers an end‑to‑end platform for legal hold, data collection, processing, review, and production, focused on litigation, investigations, regulatory matters, and FOIA/public records workflows.

Its system is used to manage large, multi‑source datasets securely at enterprise scale, with built‑in analytics and active learning to accelerate document review and surface relevant information

FYI, Thoma Bravo is one of the world’s largest software-focused private equity firms, managing over about 181 billion USD in assets across more than 75 portfolio companies and they just raised a new $24.3 Billion private equity flagship fund. https://t.co/mYgYunrk53

Ownership structure

Thoma Bravo holds a majority stake in the combined Casepoint–OPEXUS company following its acquisition of OPEXUS from Gemspring Capital and its investment in Casepoint.

Corporate setup

The combined company operates under the OPEXUS/Casepoint platform, is headquartered in Washington, D.C., and is led by OPEXUS CEO Howard Langsam, with Casepoint co-founder Vishal Rajpara on the executive team.

SEC contracting for FOIA support:

SEC procurement documents show FOIA handling support contracts, including C2 Alaska and Fors Marsh Group, appearing in SEC “Contract Payment Justifications,” explicitly describing FOIA support for Enforcement and other SEC functions.

USAspending shows @SECGov awards to C2 Alaska. The real ownership is listed above.

So there it is.... dear @SECPaulSAtkins, if you truly want to reduce the cost of your OPEX digital services (reading your recent comments https://t.co/oyLrk8KPJI):

1. You may wish to contact the ThomaBravo member who sits on the OPEXUS Board, and is mandated by his private equity investment thesis and LPs, to squeeze every $$$ dollar out of you, because your SEC organisation is #HOSTAGE to a SINGLE SOURCE supplier, who is controlling directly and indirectly your software stack and perhaps the quality of the service...

2. You may wish to incentivise competition with blockchain tech if you desire to break free from such a monopoly or bring it all under in-house control.

Best of luck. I have lots of faith in your leadership since @POTUS entrusted you, and certainly, we are getting a lot more transparent access to #MMTLP information during your administration. More is needed, especially Gensler's "lost" cellphone messages. THANK YOU!

#BlueLedgerAI - The 🧈fly on the wall 🔍🦋

What the SEC is asserting

The SEC is relying on FOIA Exemption 7(A) (law-enforcement interference) to block almost 100% of #MMTLP FOIAs, asserting that disclosure would interfere with an ongoing investigation.

That is legally permissible in isolation.

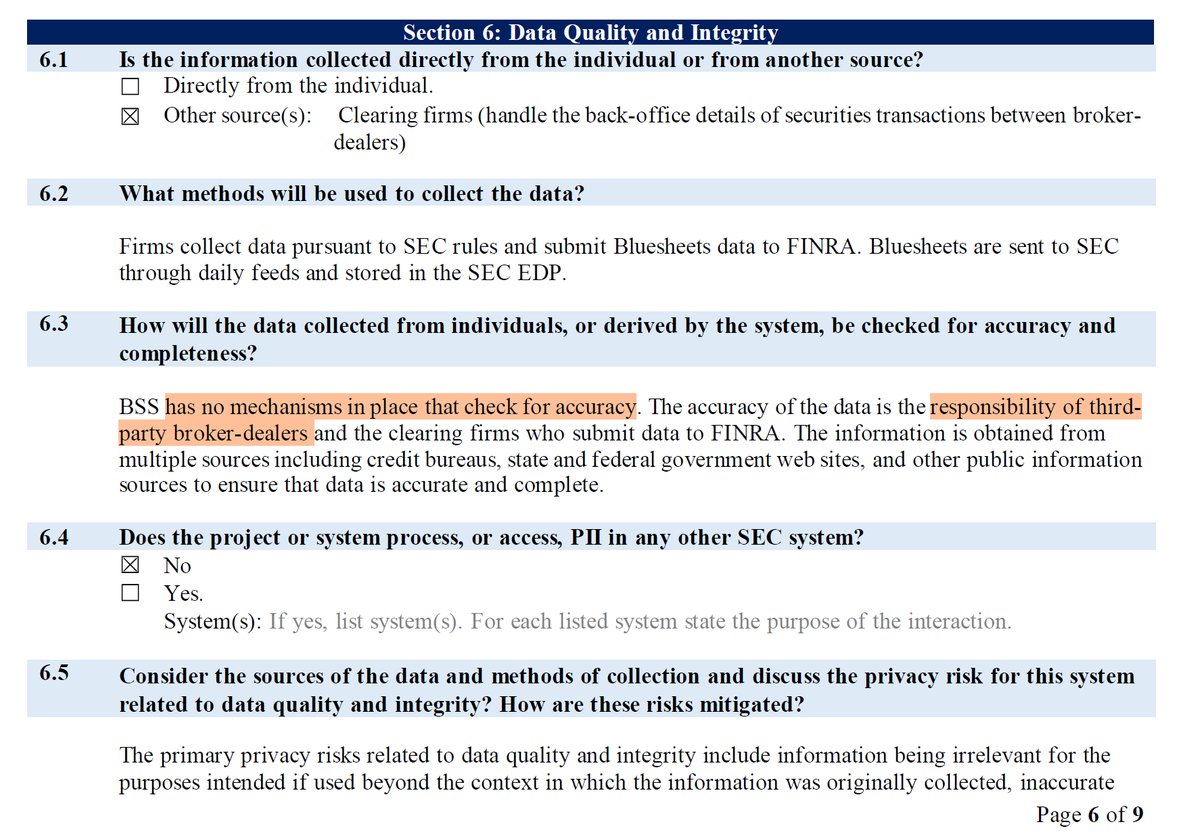

The Bluesheets as a Service (BSS) PIA, dated August 29, 2025, (https://t.co/bzeBwGlyww) confirms that:

1. The SEC does not control the accuracy of the core investigative data it relies on.

2. BSS has no mechanisms in place to check for accuracy of submitted data.

3. Accuracy is explicitly delegated to broker-dealers and clearing firms, i.e. the very parties under investigation.

4. FINRA operates the system as a cloud SaaS, and the SEC consumes pre-processed outputs downstream.

5. The SEC itself acknowledges the system is used for market reconstruction, yet:

-does not verify raw inputs,

-does not independently validate transformations,

-does not own the infrastructure end-to-end.

This above is not a theory, it is stated plainly in Section 6.3 of the PIA...

Implication:

The SEC is asserting “open investigation” protection over records produced by a system it admits is non-verifying, third-party dependent, and opaque.

There are two layers here.

The formal view says BSS is just neutral regulatory plumbing.

The structural reality is that this setup creates exactly the kind of embedded conflicts our AI research team has been mapping. #BlueLedgerAI

Why the “commissioned + hosted” structure matters

The PIA describes BSS as “commissioned by the SEC” but "hosted and operated" by @FINRA , with SIAC in the submission path and broker-dealers as the data originators.

That creates a quiet but serious tension... wouldn't you agree?

To a market observer, it appears that the @SECGov is both:

1. the supervisor of FINRA, and

2. a dependent customer of FINRA for a critical surveillance system. 🤣

At the same time, it appears that @FINRA is both:

1. subject to SEC oversight, and

2. the data chokepoint for information that can expose its own regulated members. 🤣

The PIA never labels this a “conflict of interest”

But structurally, it is classic incentive-misalignment territory...

An SRO is actively controlling the infrastructure that can implicate the firms that fund it... while the statutory regulator must rely on that SRO’s systems to see what actually happened in the market.

What could possibly go wrong, eh⁉️

I may have a guess or two... next

@palikaras It's way overdue!!

markets just won't let it in until we force the door open. #BlueLedgerAI💪💪💪 MMTLP MMAT

AI research findings to date show that:

CAT was designed to capture where the match happens, not where economic intent ORIGINATES.

PROVE ME WRONG. #MMTLP #BlueLedgerAI

PS> below is a SIMPLIFIED example... There are many, many... MANY... different permutations of this "evasion by design"... you can find them GLOBALLY if you know where to look... Hiding in plain sight... not anymore.

Clue: it is not in the CAT system/data...

AI research findings to date show that:

Any proposal that reduces quote-level or cancel-level detail directly increases false negatives.

Prove me wrong. #BlueLedgerAI #MMTLP

AI research findings to date show that:

If CAT lacks a stable, cross-firm beneficial ownership key, then CAT cannot fully replace Blue Sheets, only partially automate them.

Prove me wrong. #BlueLedgerAI #MMTLP

Last Seen Hashtags on Sotwe

nolimit() filter:videos

Seen from United States

CaveAJus

Seen from France

sonmom

Seen from Germany

口活

Seen from Japan

Fishsisig

Seen from United States

exny #Nolimit

Seen from United States

เย็ดป้า

Seen from Thailand

zoophilia

Seen from Israel

keh

Seen from United States

Boycott_Products_Of_Israel

Seen from United States

Most Popular Users

Elon Musk

@elonmusk

240.6M followers

Barack Obama

@barackobama

119.2M followers

Donald J. Trump

@realdonaldtrump

111.7M followers

Cristiano Ronaldo

@cristiano

110.6M followers

Narendra Modi

@narendramodi

107M followers

Rihanna

@rihanna

97.7M followers

NASA

@nasa

92.2M followers

Justin Bieber

@justinbieber

90.9M followers

KATY PERRY

@katyperry

87.7M followers

Taylor Swift

@taylorswift13

81.5M followers

Lady Gaga

@ladygaga

73.1M followers

Virat Kohli

@imvkohli

69.9M followers

Kim Kardashian

@kimkardashian

69.8M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

63.9M followers

Neymar Jr

@neymarjr

62.7M followers

The Ellen Show

@theellenshow

62.4M followers

CNN

@cnn

61.9M followers

X

@x

60.8M followers

Selena Gomez

@selenagomez

60.8M followers