Top Tweets for #DescoInfraTech

🎯Betting on 3 Low P/E Growth Stories📈

✓ I'm betting on businesses where earnings could grow faster than their current valuations

⚡ #DescoInfratech

♻️ CBG, Hydrogen & Clean Energy 📦 Strong order pipeline 🚀 Multiple growth engines

🏗️ #NisusFinance

🏢 Asset-light real estate & AIF platform 🌍 Global expansion 💰 Scalable, capital-light business

🚢 #SJLogistics

⚓ Expanding into vessel ownership 🌍 Benefiting from global trade 📈 Higher value-added logistics

🎯 My Thesis

✅ Low P/E valuations

✅ Profitable businesses

✅ Strong management vision

✅ Long growth runway if execution continues

📝 Note to myself: Great wealth is created by owning tomorrow's businesses, not chasing today's numbers. I'm investing in what these companies could become over the next 3–5 years.🚀

Not a Reco.DYDD

#Desco #SJ #Nisus #multibaggers

#FII #DII #stockmarket #DescoTech

Desco Infratech Ltd receives order worth Rs. 6.74 crores

#DescoInfratech #OrderWin

https://t.co/l0OgzSJov9

Desco Infratech Surges on ₹15.06 Crore LOI Win from Sabarmati Gas

https://t.co/wyCgzDyy3W

#DescoInfratech #SabarmatiGas #LOI #OrderWin #Infrastructure #CityGasDistribution #EnergySector #BusinessGrowth #ProjectExecution #CorporateNews #MarketUpdate #StockMarket #OrderBook

Nice read👍

#DescoInfratech

Desco Infratech FY26 Earnings Concall Highlights:

👉 FY27 & Future Outlook:

💠Revenue growth: Management guided 70-80% YoY growth (conservative) for the next 2-3 years on the back of CGD execution, power/solar diversification, and CBG ramp-up.

💠Long-term target: ₹1,000 Cr revenue by FY2030 (5-year horizon). CGD (including CBG) expected to contribute 60-65% of revenue; balance from power distribution & solar EPC.

💠CBG-specific outlook: First 2 TPD plant commissioning in Q1 FY27 (revenue potential ~₹5 Cr p.a. at full utilisation).

💠Additional expansion to 15-20 TPD capacity targeted in next 18 months (Gujarat + Madhya Pradesh).

💠CBG revenue expected to reach ~₹170 Cr by FY2030.

👉Margins: CGD PAT margin stable at ~15.4%. Power & Renewable EPC at ~10%. Overall PAT margins sustainable at current levels with direction “stable to improving” due to better project mix, cost control, and higher-margin CBG contribution (PAT margin 22-23%).

💠Break-even on initial CBG plant expected in 18-20 months

💠Cash flow: Operating cash flow to turn positive within 1-2 years (already improving from last year despite 100% revenue growth).

💠Negative cash flow in FY26 was purely growth-driven (working capital deployment), not liquidity stress.

👉 Current Order Book / Projects and Future Pipeline:

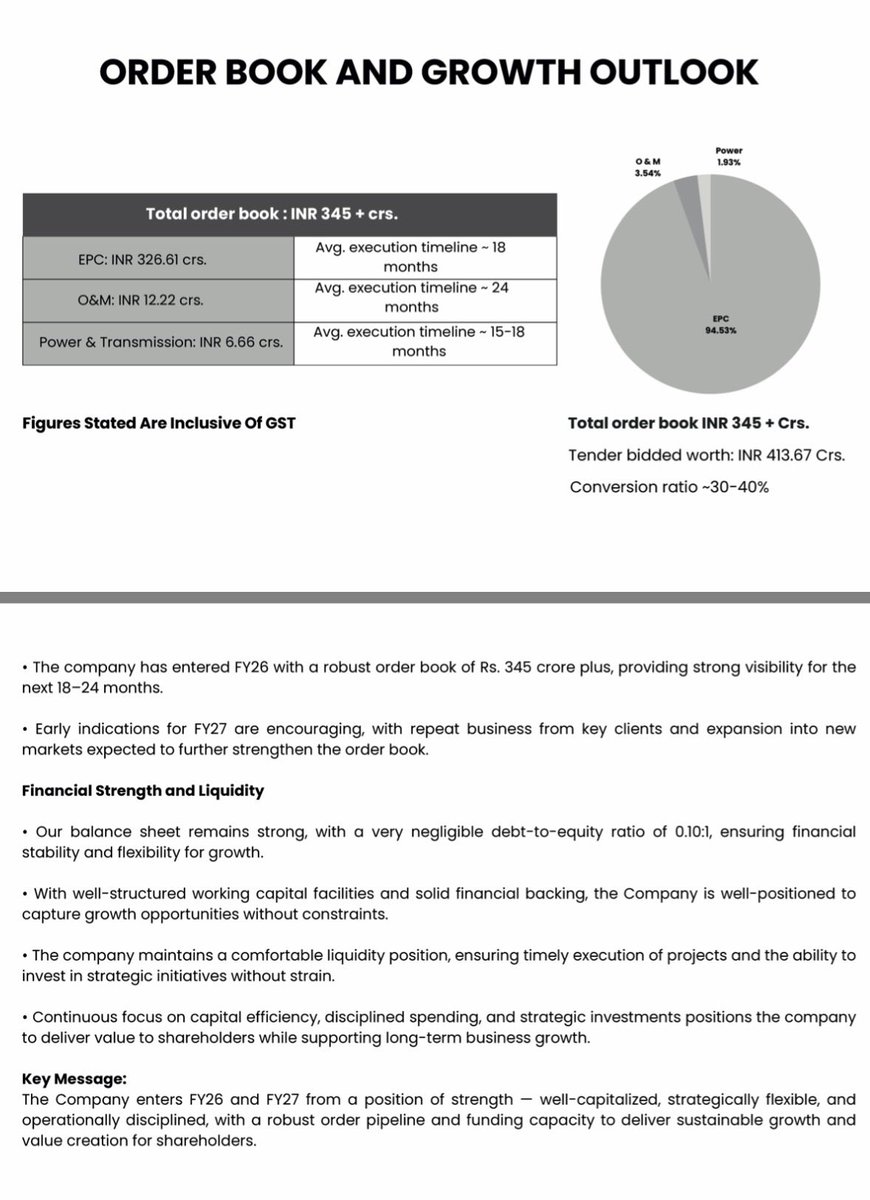

💠Order book: ₹345+ Cr

💠 CGD: ~₹330-332 Cr (EPC timeline 18-24 months; O&M ~₹35-40 Cr over 24 months).

💠Power distribution: Balance portion (average timeline ~1 year).

💠Tender pipeline: ₹650 Cr (CGD ~₹470-480 Cr + solar/power ~₹100 Cr). Expected to convert quickly once Middle East-related delays ease; management sees this as a major order-book booster.

💠Execution focus: CGD pipeline execution continues. Power & solar EPC contributed meaningfully in H2 FY26 due to seasonal execution tailwinds (post-monsoon ROW clearances).

💠CGD remains core (83.24 Cr revenue in FY26).

👉CBG projects:

💠2 TPD commissioning in Q1 FY27 (capex ₹3.5-4 Cr already incurred).

💠SGAEPL (75-76% stake acquired) to add 5 TPD capacity; ready government approvals accelerate rollout.

💠Further 15-20 TPD greenfield via Desco BioGreen Pvt Ltd (total capex ~₹25 Cr planned; funded via bank debt/greenfield financing).

👉 Other Notable Points:

💠FY26 Financials: Revenue ₹118.79 Cr (+99.28% YoY), EBIT ₹23.43 Cr (+76.3%), PAT ₹16.38 Cr (+80.87%), Net Worth ₹70.85 Cr (+20.3%), Debt/Equity stable at 0.20x, EPS ₹21.34.

💠Segment performance: CGD (70% of revenue) delivered healthy 15.42% PAT margin; new Power & Renewable EPC segment (30%) at 10.01% PAT but offers superior 10-15 day cash conversion cycle vs 30-35 days in CGD — strategic move for working-capital efficiency.

👉Debt & capital allocation: Unsecured NBFC borrowings (short-term, 15-17% cost) taken mainly for solar projects (90-120 days tenure). Plan to restructure post-H1 FY27 to 8.5-9.5% via banks and repay via internal accruals. No aggressive leverage.

👉Strategic initiatives:

💠SGAEPL acquisition → instant regulatory approvals + CBG entry.

💠Desco BioGreen Pvt Ltd (WOS) → dedicated green energy platform.

💠DESCO GLOBAL FZ-LLC (UAE) → international EPC push; currently on hold due to Middle East crisis but long-term opportunity in gas infrastructure.

💠Green hydrogen: MOU signed; plans to blend into CGD network once economics improve (solar park required for viability). EPC will be executed in-house.

💠Customer mix (CGD): ~70-72% PSU (BPCL, GAIL, IOCL, IGL etc.), 28-30% private blue-chips (Torrent Gas, Adani Total Gas).

💠Raw material & bidding discipline: Private clients often provide free-issue material; PSUs require full supply by company. Management committed to margin discipline — selective bidding only; rejected low-margin work during recent crisis-driven demand surge

———

🔗 https://t.co/Sto1a1qHIQ

———

#SMEGems #SME #DescoInfratech #Desco #SME

#DescoInfratech

Order book around 345 Cr

Pipeline more than 650 Cr

#Descoinfratech

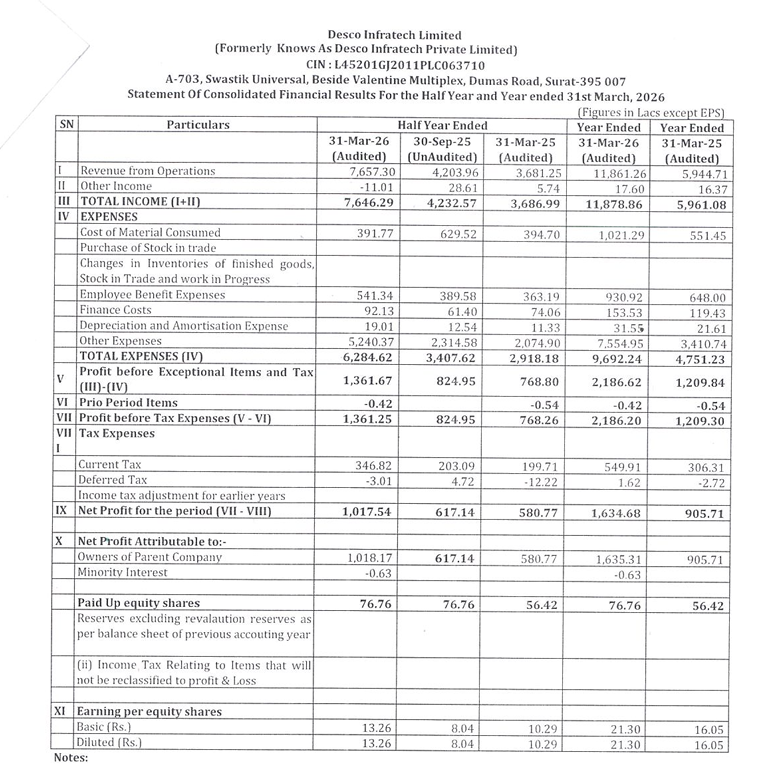

Desco Infratech Ltd

Comparison of Financial Results YoY:

Revenue at Rs. 118.6cr vs Rs. 59.4cr; up by 101%

PBT at Rs. 21.8cr vs Rs. 12cr; up by 82%

PAT at Rs. 16.3cr vs Rs. 9cr; up by 81%

EPS at 21.3 vs 16.05

Negative OCF at Rs. 19crores vs 12crores

Stock is trading at CY PE of 11.7x

Power distribution segment grown significantly than City gas distribution in the H2.

Good #Q4FY26-04/05/2026 post 4pm till 8pm

Desco Infratech

#Desco

#DescoInfra

#DescoInfratech

Delivers strong FY26 and H2FY26 numbers

Good uptick vs H1FY26 and H2FY25

Rev at 77cr vs 37cr, H1 at 42cr

PBT at 13.6cr vs 7.6cr, H1 at 8.2cr

Good growth across all parameters

Highest ever set

PAT at 10.1cr vs 5.8 r, H1 at 6.2cr

FY26 PBT at 22cr vs 12cr

FY26 PAT at 16cr vs 9cr

Orderbook of 350+cr giving multi year visibility

Recievables at 30cr vs 13cr

OCF at -19cr vs -12cr

Sobha Ltd

#Sobha

#SobhaLtd

Blockbuster Q4FY26 with good revenue recognition in Q4FY26

Good margin expansion QoQ and YoY

Record year for pre-sales and collections

Healthy new launches, good pipeline

Realizations/sqft moved up

Rev at 1988cr vs 1240cr, Q3 at 943cr

PBT at 122cr vs 56cr, Q3 at 21cr

PAT at 92cr vs 41cr, Q3 at 15cr

Solid QoQ and YoY uptick across all parameters

FY26 PBT at 260cr vs 133cr

FY26 PAT at 193cr vs 95cr

OCF at 430cr vs 200cr

FY27 inventory at 10.53 million sqft

20.67 mln sqft forthcoming projects

18650+cr revenue yet to be recognised with 30%+ OPM band

6.04 mln sqft new launches with 9 projs across 6 cities

Manappuram Finance

#Manappuram

Good Q4FY26 with solid QoQ and YoY uptick across all parameters

Asirvad Microfinance bounces back after 6-7 qtrs of pain with 41cr PBT in Q4 vs loss in last 2 qtrs

Gold loan segment is steady

Rev at 2614cr vs 2361cr, Q3 at 2354cr

PBT at 564cr vs -236cr, Q3 at 303cr

PAT at 405cr vs -203cr, Q3 at 239cr

GNPA and NNPA sharply down QoQ

Asset quality getting better

GNPA at 1.81% vs 2.61% QoQ

PAT at 1.51% vs 2.18% QoQ

Consolidated AUM ⏫52% YoY

Gold loans AUM ⏫61% YoY

Aarti Industries

#AartiInd

Good Q4FY26 with good margin expansion QoQ and YoY

Rev at 2206cr vs 1949cr⏫13%, Q3 at 2319cr

EBITDA at 343cr vs 262cr⏫31% YoY,⏫6.5% QoQ

OPM at 14.1% vs 11.8%, Q3 at 12.8%

Higher finance costs mainly due to revaluation loss of 39cr

PBT at 111cr vs 88cr, Q3 at 134cr

PAT at 137cr vs 96cr⏫43% YoY, Q3 at 133cr

Backward integration initiative with a global chemical company with 200-250cr capex over 15 year

150 million dollar multi year supply agreement with global agrochem innovator

Expects operating leverage to play out in FY27 and improved capacity utilization

KEI Industries

#KEI

#KEIInd

Good Q4FY26 with decent QoQ and YoY uptick across all parameters

Rev at 3476cr vs 2914cr, Q3 at 2954cr

PBT at 378cr vs 305cr, Q3 at 315cr

PAT at 284cr vs 226cr, Q3 at 236cr

OCF at 840cr vs -32cr🔥

Antelopus Selan

#Antelopus

#SelanExploration

Solid Q4FY26 with good QoQ and YoY uptick across all parameters

Rev at 104cr vs 65cr, Q3 at 73cr

PBT at 50cr vs 19cr, Q3 at 38cr

PAT at 38cr vs 15cr, Q3 at 29cr

OCF flat at 121cr

Petronet LNG

#Petronet

Rev down sharply, margin expands well

Rev at 9442cr vs 12315cr, Q3 at 11164cr

PBT at 1794cr vs 1443cr, Q3 at 1141cr

PAT at 1371cr vs 1095cr, Q3 at 870cr

OCF at 4750cr vs 4398cr

Avg/Decent:

#TataTech

Healthy topline growth,margins down

Rev⏫22% YoY,⏫15% QoQ

EBITDA⏫8% YoY,⏫30% QoQ

Guides for double digit organic growth for FY27 with better margins

#CAMS

Rev at 395cr vs 356cr, Q3 at 39c0r

PBT at 166cr vs 148cr,flat QoQ

OCF at 584cr vs 477cr

#NathBioGenes

Topline flat at 51cr

EBITDA at 3.4cr vs loss Q2 at 2.6cr

OCF at -13cr vs 18cr

Desco Infratech:-

Superb 35% move captured in 3 trading session...

Booked some

#Desco #Descoinfratech

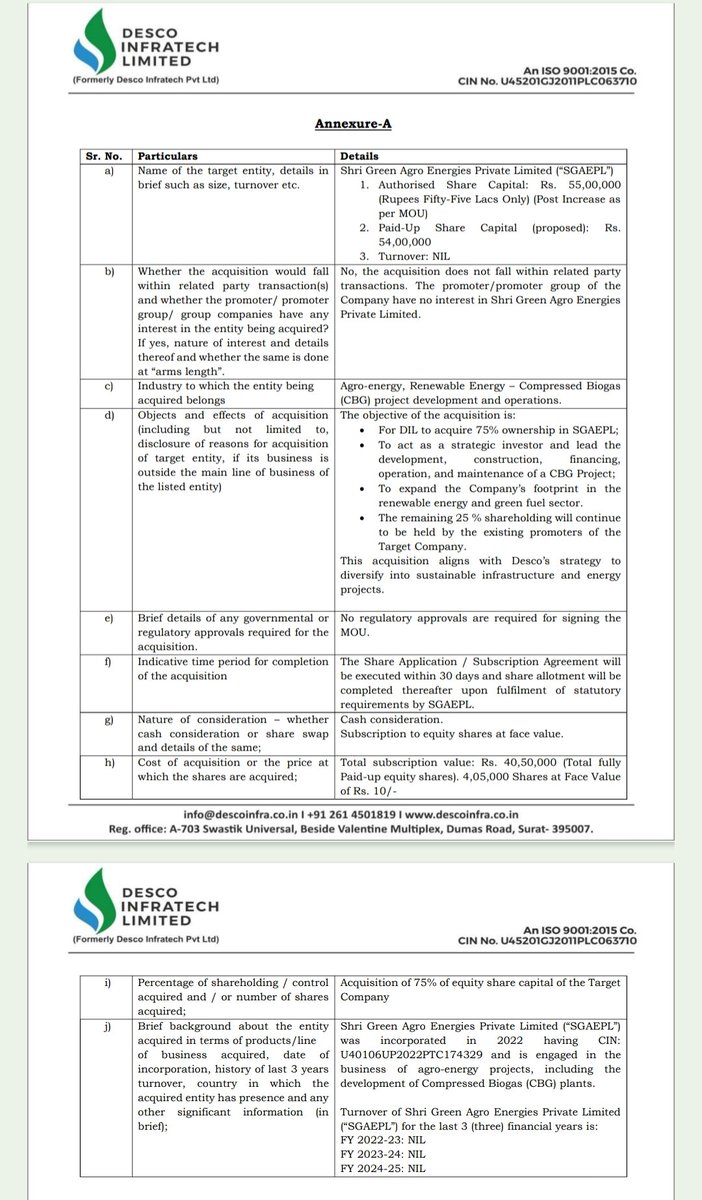

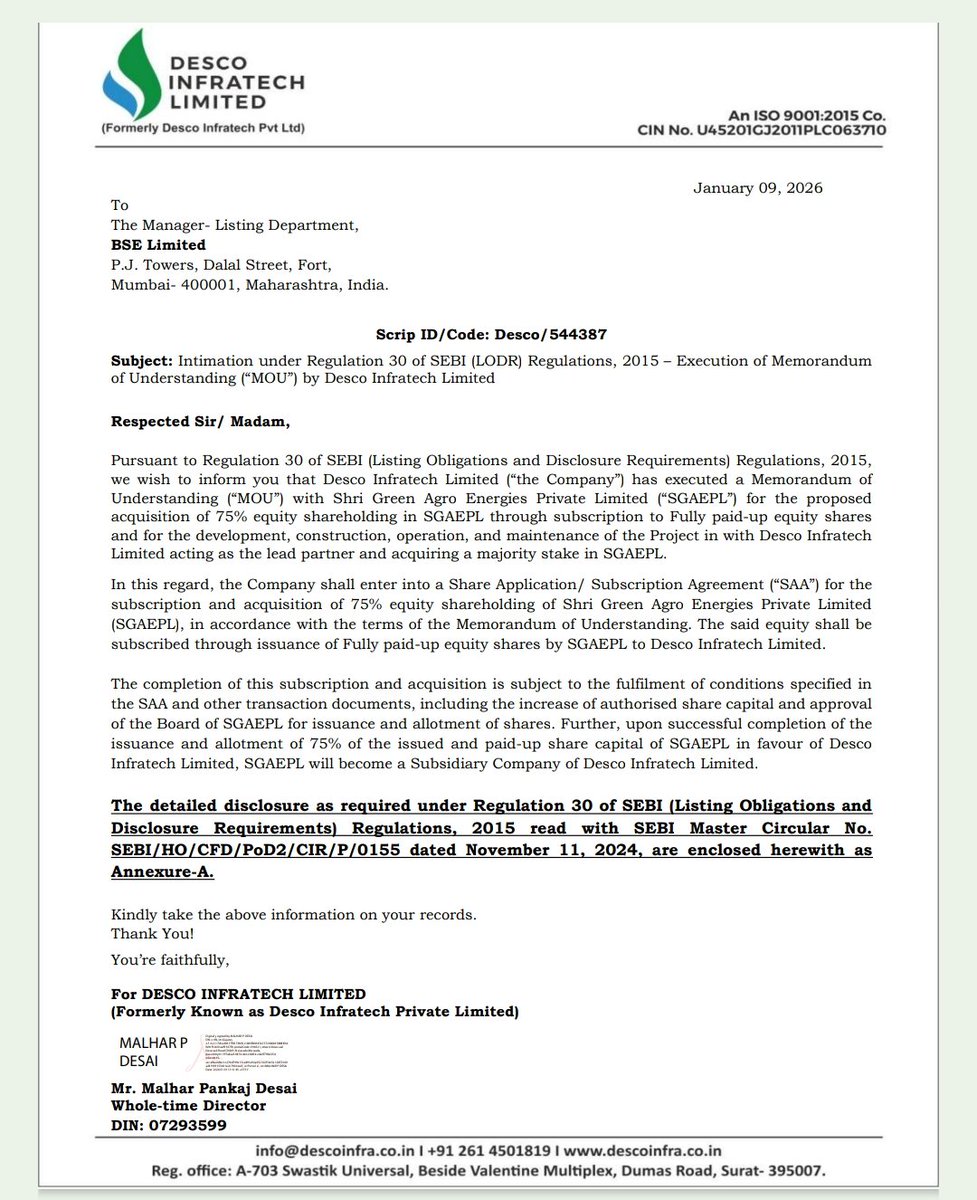

Desco Infratech Ltd has signed an MoU to acquire 75% stake in Shri Green Agro Energies Pvt Ltd through equity subscription.

Post completion, SGAEPL will become a subsidiary of Desco Infratech.

📄 Disclosure under SEBI LODR Reg 30.

#DescoInfratech #CorporateAction #Acquisition #StockMarket #BSE

🚨#DescoInfratech received new orders worth 5.37 Cr from Adani Total Gas, BPCL & MGL.

Work includes PNG projects and O&M services across Haryana, Rajasthan & Pune.

Good to see repeat names and continuity of work✌️

🚀 MULTIBAGGER ALERT! (PART- 45) 🚀

Can this SME stock have the potential to become a Multibagger?

It nearly meets all 8 strategies mentioned in the quoted tweet Reasonably well.

A Thread🧵

#descoinfratech revenue doubled

108-115 cr guidance for FY26

(WhatsApp alert from https://t.co/XQbtuuBbqU)

#descoinfratech #desco

Desco infra H1FY2026 concall:

@ FY2026 outlook:

- Targeting 110-115cr topline compared to 59cr in FY2025.

- 1000crs in FY2030.

- EBIDTA margins may contract a bit not significantly as power&distribution component distributes revenue less than 10%.

#SME #Desco #DescoInfratech

Desco Infratech H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️No explicit full-year number provided, but H1's ~80% YoY growth were basis for H2 execution

💠CGD (70% of revenue), power transmission/distribution (18-20% contribution in FY26, scaling to 30-35% over 2-3 years)

💠Long-term ~1,000 Cr revenue by FY30

▫️Margins: EBITDA margins expected to sustain at 21-22% in H2, supported by cost rationalization, operational efficiencies, and vendor ecosystem strengthening

💠No margin compression anticipated in power segment due to execution-partner model (avoiding full material scope)

▫️Cash Flow Context: Negative H1 operating cash flow attributed to strategic mobilization (front-loaded procurement, site expansions)

💠Expected to turn positive in H2 with collections starting October 2025

💠Debt-to-equity improved YoY, with working capital facilities operational and new financing discussions underway

👉Order book / projects and pipeline:

▫️Current order book : ~340cr+ (across CGD, Power, Water Infra)

💠Full order book conversion by FY27

💠CGD: Heavy contribution to H1 revenue (~23 Cr in Q1, slower Q2 due to monsoon delays in South India

💠Q2 slowdown (from ~23 Cr to ~19 Cr in CGD) due to weather; H2 rebound with client payments

▫️Power T&D: Diversification ramp-up; steady margins via partnerships (L2/L3 role, partnering with L1 bidders like integrated firms).

▫️Water: New orders contributing to H1 growth

▫️CBG Pipeline (via wholly-owned subsidiary Desco Biogreen Pvt Ltd): Groundwork started; 3-5 tons/day capacity from FY27

💠Green Hydrogen: Tripartite MOU with KP Group for blending into CGD pipelines (12-15 months to execution; reduces LNG import reliance)

💠Regulatory approvals for CBG pending (expected 2-3 months)

💠Security bonds exploration (per IRDAI); vendor ecosystem for efficiency

💠 FY27 Onward: CBG topline contribution; hydrogen blending in 12-18 months

👉 Others :

▫️Entry into CBG aligns with green energy/self-reliance goals (no EPC role; full facility build/operation to produce/sell gas ; 3-4 year payback; exploring distressed unit acquisitions)

▫️Power segment via partnerships to preserve margins (avoid full material supply). Vendor advances/labor mobilization as "strategic moves" for 30-35% efficiency gains despite geographical expansion (Gujarat/UP to South India).

▫️Risks / Mitigants: Low sector penetration (CGD at 6.3-6.4% of potential) limits downside; no major risks beyond weather/uncontrolled events

💠Receivables tied to blue-chip clients (Adani, Torrent, GAIL) with standard retention cycles

🧵DESCO Infratech Limited – Investor Presentation Key Highlights 👇

#DescoInfratech #Earnings #H1FY26 #CGD #GreenEnergy #InfraGrowth #Hydrogen #CBG #InvestingIndia

🚨#DescoInfratech... 85% Revenue Growth, 345 Cr+ Order Book & Vision to Become 1000 Cr Company...🔥🔥

A Thread🧵

🚀 MULTIBAGGER ALERT! (PART- 45) 🚀

Can this SME stock have the potential to become a Multibagger?

It nearly meets all 8 strategies mentioned in the quoted tweet Reasonably well.

A Thread🧵

Desco Infratech Ltd👑

Available at 15 PE with 100% growth for consecutive next 2 years✍️

Solid Order Book, Balance Sheet & most importantly negligible debt to equity ratio✨

Expecting 100%+ YoY growth in H2Fy26 with improve in margins💹

#descoinfratech #investorpresentation

#Desco Infratech

FY25 revenue 59 Cr. Outstanding Orderbook 345 Cr executable mostly in 18 months. Further bid value 413 Cr with success ratio of 30 to 40%. Liquidity comfortable. So, ideally growth for the next 2 years should be higher than 100% to fulfill orders timeline.

Desco Infratech Ltd👑

CMP : 235✨

As per Technicals, 220 remains strong support✨

Stock will get stable after today's panic fall✍️

PE is 15 @ CMP✨

Mgmt managed to deliver as per guidance, should do great in H2Fy26✨

No buy/sell reco✨

#descoinfratech #results #technicals

Desco Infratech Ltd👑

H1Fy26 Results✨

Desco Infratech Ltd

Investors who are looking at the strong YoY results are still holding, while weak hands are exiting. The stock is down 8% despite results being in line with guidance. Buying interest is likely to return, and the stock should bounce back

#DescoInfratech #Results

Last Seen Hashtags on Sotwe

nolimit filter:videos

Seen from Turkey

معصيتي_رحتي

Seen from Poland

groupsex

Seen from United Kingdom

tramplehand

Seen from United States

纱姬舞团

Seen from United States

momson()****

Seen from Mexico

nudefarmer

Seen from Spain

คลิปหลุดโป๊

Seen from Thailand

نيج_كويتى

Seen from United States

Teenager

Seen from Turkey

Trends for you

Most Popular Users

Elon Musk

@elonmusk

240.9M followers

Barack Obama

@barackobama

119.2M followers

Donald J. Trump

@realdonaldtrump

111.8M followers

Cristiano Ronaldo

@cristiano

111.5M followers

Narendra Modi

@narendramodi

107.1M followers

Rihanna

@rihanna

97.9M followers

NASA

@nasa

92.2M followers

Justin Bieber

@justinbieber

91.1M followers

KATY PERRY

@katyperry

88.1M followers

Taylor Swift

@taylorswift13

82M followers

Lady Gaga

@ladygaga

73.5M followers

Virat Kohli

@imvkohli

70.7M followers

Kim Kardashian

@kimkardashian

70M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

64.2M followers

Neymar Jr

@neymarjr

63.5M followers

The Ellen Show

@theellenshow

62.4M followers

CNN

@cnn

61.9M followers

Selena Gomez

@selenagomez

61.2M followers

X

@x

60.8M followers