Top Tweets for #FORCAS

#SME #ForcasStudio #Forcas

Forcas Studios H2 FY26 Concall Highlights

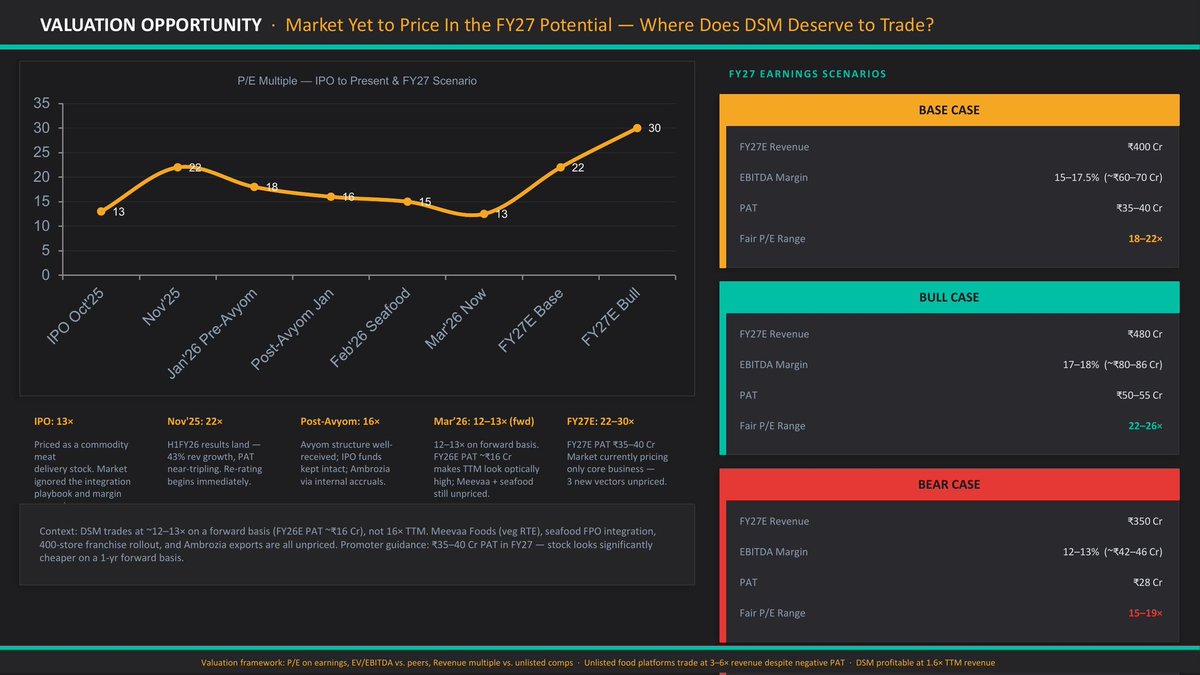

👉 FY27 & Future Outlook

▫️ Management remains optimistic and guided 25-30% revenue growth for FY27

💠Noted a historical practice of conservative guidance (previously communicated 25-35%) to understate and over-deliver

▫️ Multi-brand strategy as the core growth engine:

💠FTX (economy fast fashion, Gen Z focus, price point ₹199-599): Scale driver, targeting ~₹160-170 Cr in FY27; expanded into women’s wear (formal/casual trousers, comfort wear).

💠Tribe (premium bottoms – men & women, ₹599-1,499, avg. ASP ~₹899): Premiumization and margin lever; tested successfully (3.5x growth in FY26 over testing phase); aggressive expansion via distribution, marketplaces, and Quick Commerce.

💠Fitness Exchange (new separate brand – athleisure, activewear, sports-inspired, accessories; semi-premium affordable): Targeting rapidly growing health & fitness segment; 50-50 clothing + accessories mix; expected to scale gradually in FY27 with product-market fit testing.

💠 Quick Commerce positioned as the “next large opportunity” and future of fashion retail in India (wide SKU, option-based buying, Gen Z smartphone preference).

💠Already live on Zepto and Myntra M-Now; Flipkart Minutes paperwork closed and expected live shortly.

💠FY26 Quick Comm revenue ~₹7.5 Cr; targeted mix 10-15% in FY27, scaling to 30-40% over the next couple of years.

▫️ Overall focus:

💠Scaling brands, Quick Commerce expansion, strengthening omnichannel distribution, margin improvement

💠 White labeling to be maintained at ~20% (±5%) of revenue for learning and clean margins without inventory risk.

💠Long-term (3-5 years): Digital/online to 50-60% of non-white-label revenue, distribution 30-40%.

💠Asset-light model, existing sourcing/warehousing/marketplace infrastructure, and omnichannel relationships in focus

👉 Current Order Book / Projects and Future Pipeline

▫️ White labeling (B2B) contributed ~20% of FY26 revenue (~₹39-40 Cr) with a order book of ₹178 Mn at year-end.

💠Strategy is to keep it steady (not exceed 20-25%) while leveraging it for design/forecasting insights and relationships with major retailers.

💠 Quick Commerce pipeline: Expansion from current platforms (Zepto ~120 stores, Myntra M-Now) to Flipkart Minutes and others.

💠Requires higher initial inventory for 10-15 min availability but drives faster rotation and superior margins as the channel matures.

💠 Brand pipeline: Tribe scaling in FY27 with men’s/women’s premium bottoms; Fitness Exchange launch and market testing in FY27 (athleisure + accessories).

💠Continued hero product development and new launches under FTX (double-digit hero SKUs already driving growth).

💠Offline reach expanding from 8 to 10 states; retail network >18,000 retailers; serviceable pincodes >21,000; warehouse expanded to 60,000 sq. ft. in Kolkata

👉 Other Notable Points

▫️ Margins:

💠Gross margins expected to improve via

(1) Quick Commerce logistics savings

(2) Higher ASP/margin mix from Tribe & Fitness Exchange

(3) Maturing FTX product portfolio with better acceptance and selective price hikes.

💠Digital gross margins currently highest (30-35%), distribution ~22-23%, white labeling 19-21%.

💠EBITDA margins already improved in FY26; further uplift targeted in FY27 through premiumization and operating leverage.

💠Ad & promotion spend ~3-4% (mainly marketplaces/Quick Comm visibility).

▫️ Balance sheet & cash flow:

💠Inventory rose sharply (to ~₹50 Cr) due to Quick Commerce stocking requirements, new brand launches (Tribe/Fitness Exchange), and ensuring availability for impatient Gen Z customers.

💠Cash conversion cycle lengthened but expected to normalize as brands strengthen, inventory turns faster, and higher-margin products scale.

💠Management expects gradual improvement in cash flows over the next couple of years with brand maturity.

▫️ Differentiation & resilience:

💠Purely asset-light (no own stores or factories for FTX; third-party MBOs + marketplaces + Quick Comm).

💠Omni-channel at economy price points with fast delivery (15 min to 24 hrs).

💠No direct national brand competition in core FTX range.

💠Repeat rates: ~29-30% online, 65-70% offline retailers reorder within 4-6 months.

💠Hypothetical competition from Zudio/Westside in Quick Comm addressed by their retail/franchise model constraints and massive market size (no single winner possible).

▫️Challenges/Bottlenecks:

💠Talent acquisition (hiring experienced people for scaling) and brand-building process (iterative learning curve).

💠No major manufacturing or distribution bottlenecks cited due to asset-light model and existing infrastructure.

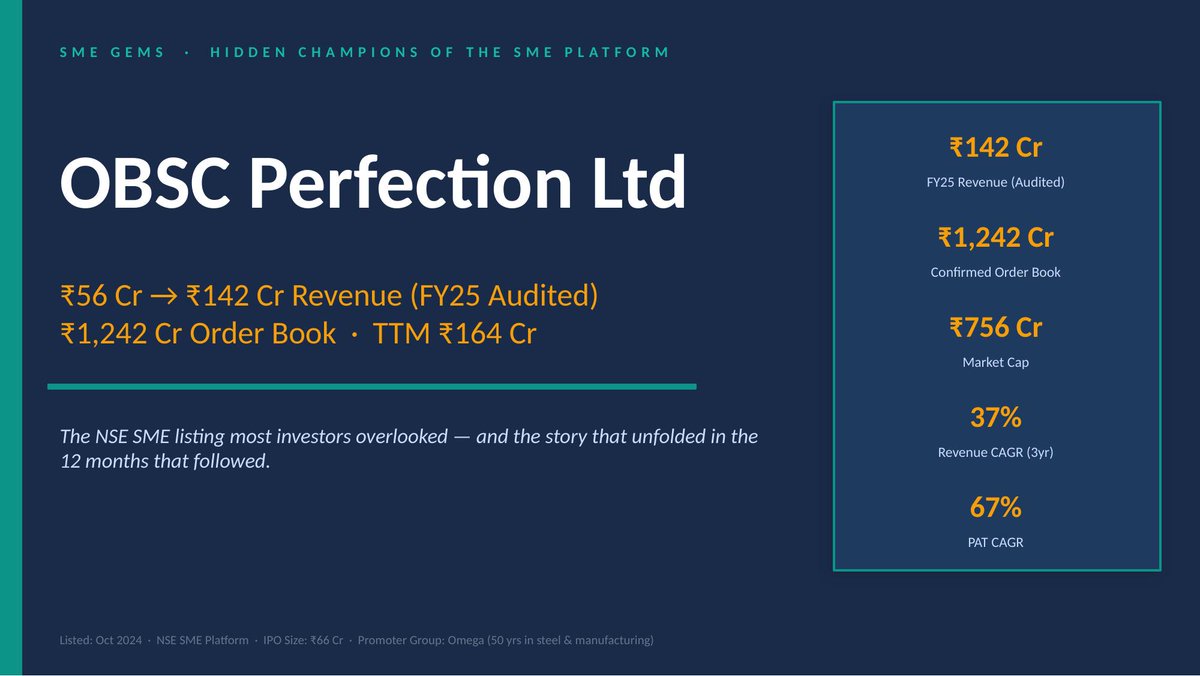

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 https://t.co/Sto1a1qHIQ

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

kongddo be flirting with e/o half of the behind 🤣

🦌 i'll give u a kiss

🐺 u can kiss this

🦌 am i really doing it!?

🐺 u said u'd give me a kiss

🦌 u said no!

🐺 but i'm ok with it

🐺 hold hands?

🦌 give me ur hand

🐺 ur mic is pretty

🦌 ur prettier

mds se fosse cmg eu me matava #forcas

BELIFT Ent. anuncia saída do integrante Heeseung do ENHYPEN, seguindo como artista sob o selo da empresa.

'Após conversas aprofundadas com cada um dos membros sobre o futuro que eles vislumbram e a direção do grupo, ficou claro que HEESEUNG tem sua própria visão musical distinta e decidimos respeitá-la.

Sendo assim, HEESEUNG se separará do ENHYPEN, e o ENHYPEN continuará suas atividades oficiais como um grupo de seis membros.

É difícil transmitir todo o processo em um curto período de tempo, mas essa decisão foi tomada após muita deliberação. Entendemos que essa notícia é difícil de assimilar e pode ser recebida com reações diversas. Mesmo assim, esperamos que compreendam que essa decisão foi tomada pensando no futuro do ENHYPEN e de HEESEUNG.

O ENHYPEN continua comprometido em compartilhar performances energéticas com o ENGENE. HEESEUNG estará preparando um álbum solo como artista pela BELIFT LAB.'

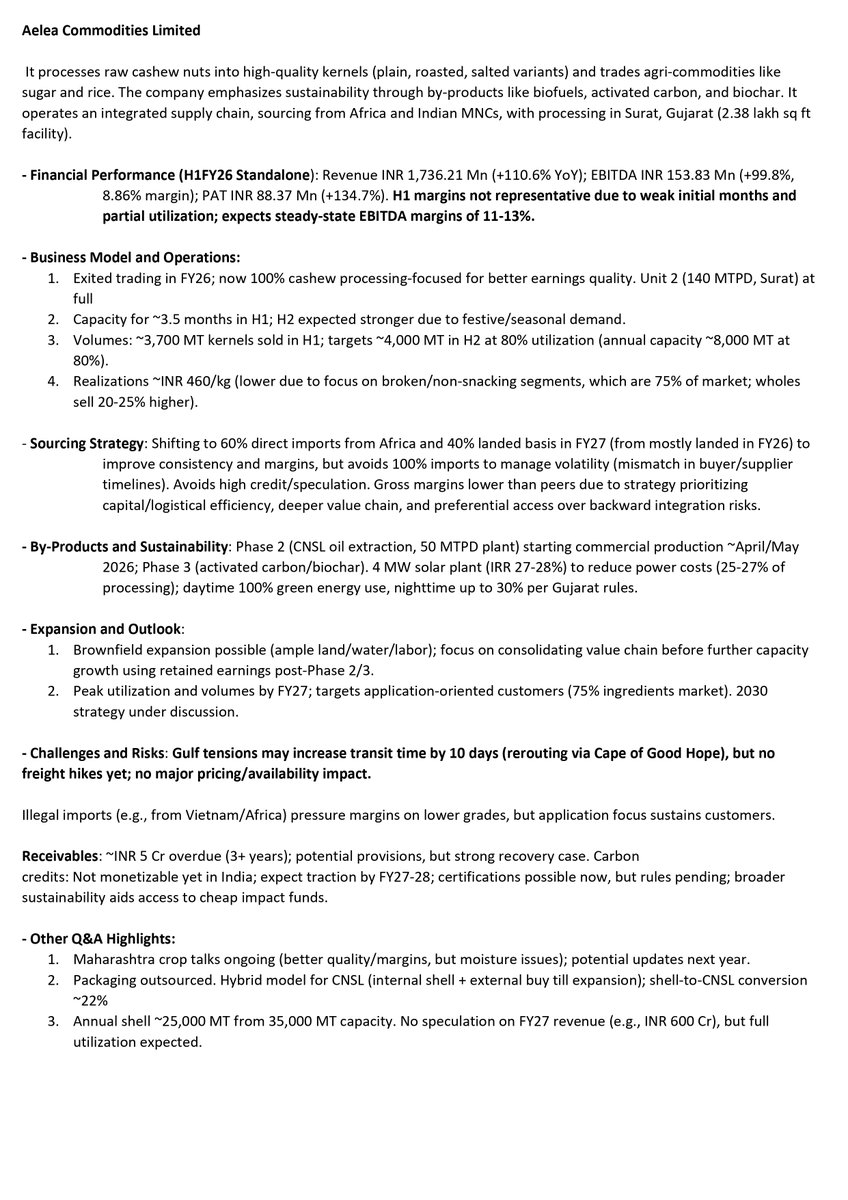

Arihant Bharat Connect Conference March '26:

👉Day 1:

💠Aelea Commodities

💠Utssav CZ Gold Jewels

💠Forcas Studios

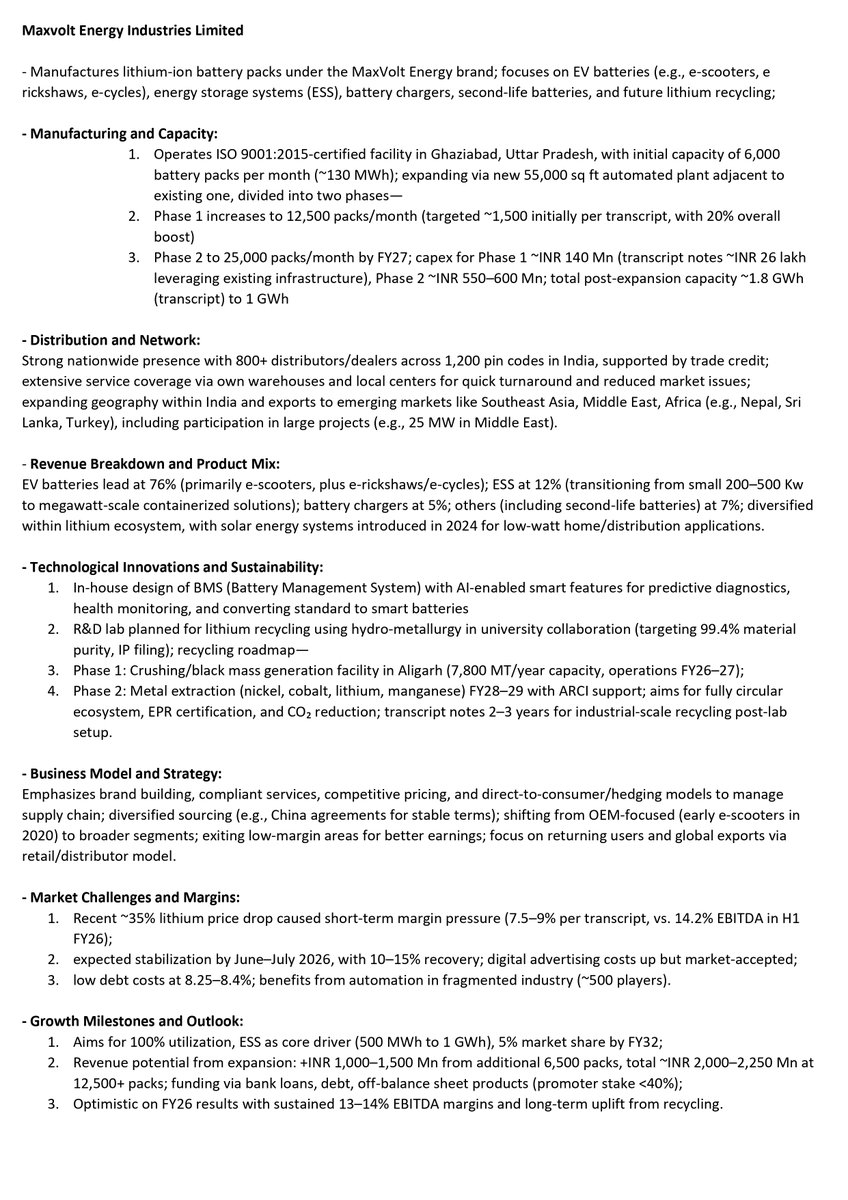

💠Maxvolt Energy Industries

💠AVP Infracon

#aelea #acld #utssav #forcas #avpinfra #avpinfracon #maxvolt #maxvoltenergy #utssavcz #bharatconnectconference #arihantcapital

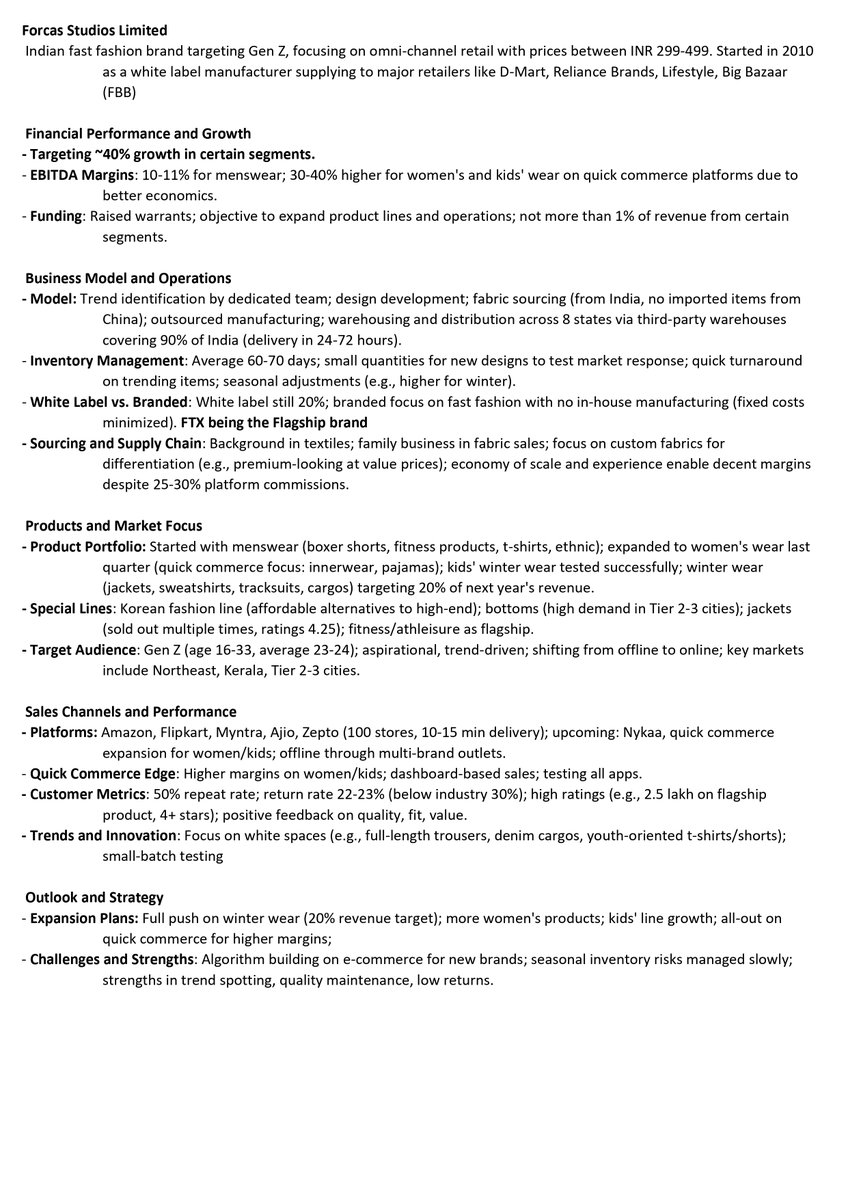

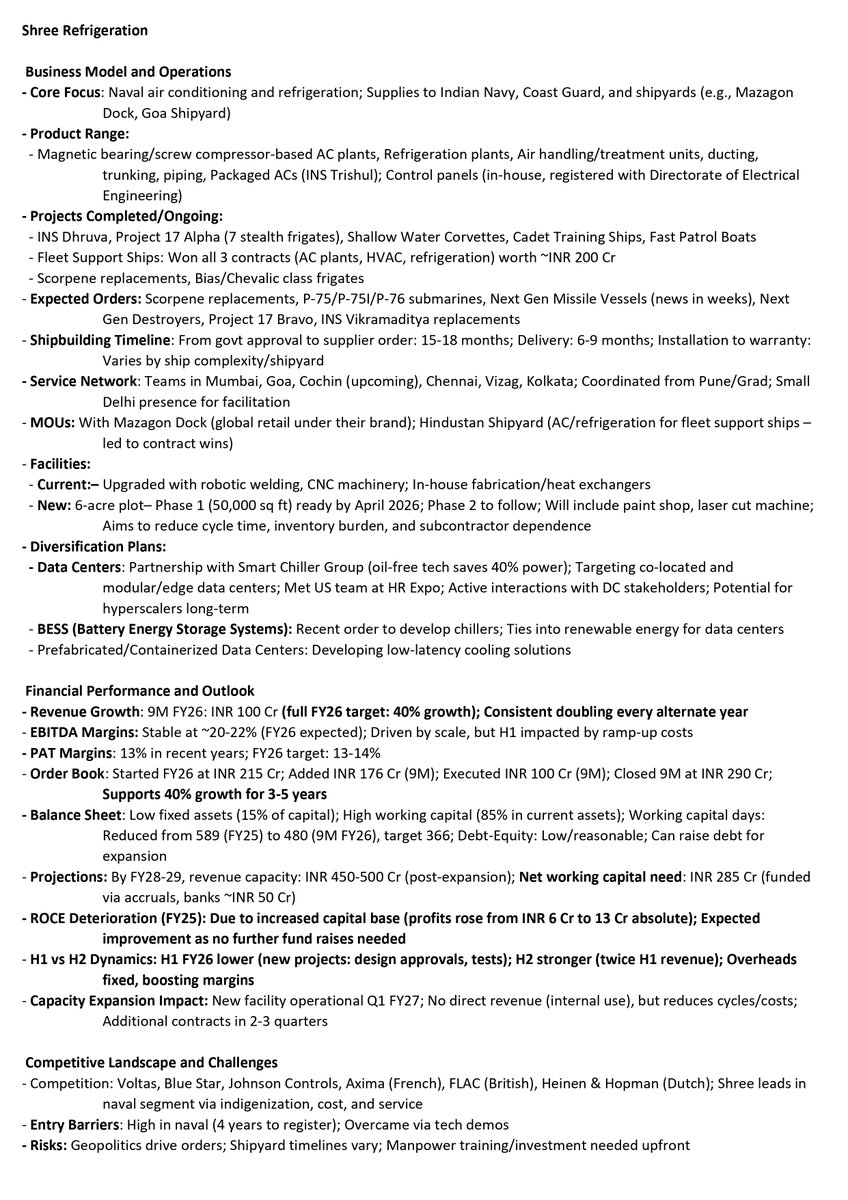

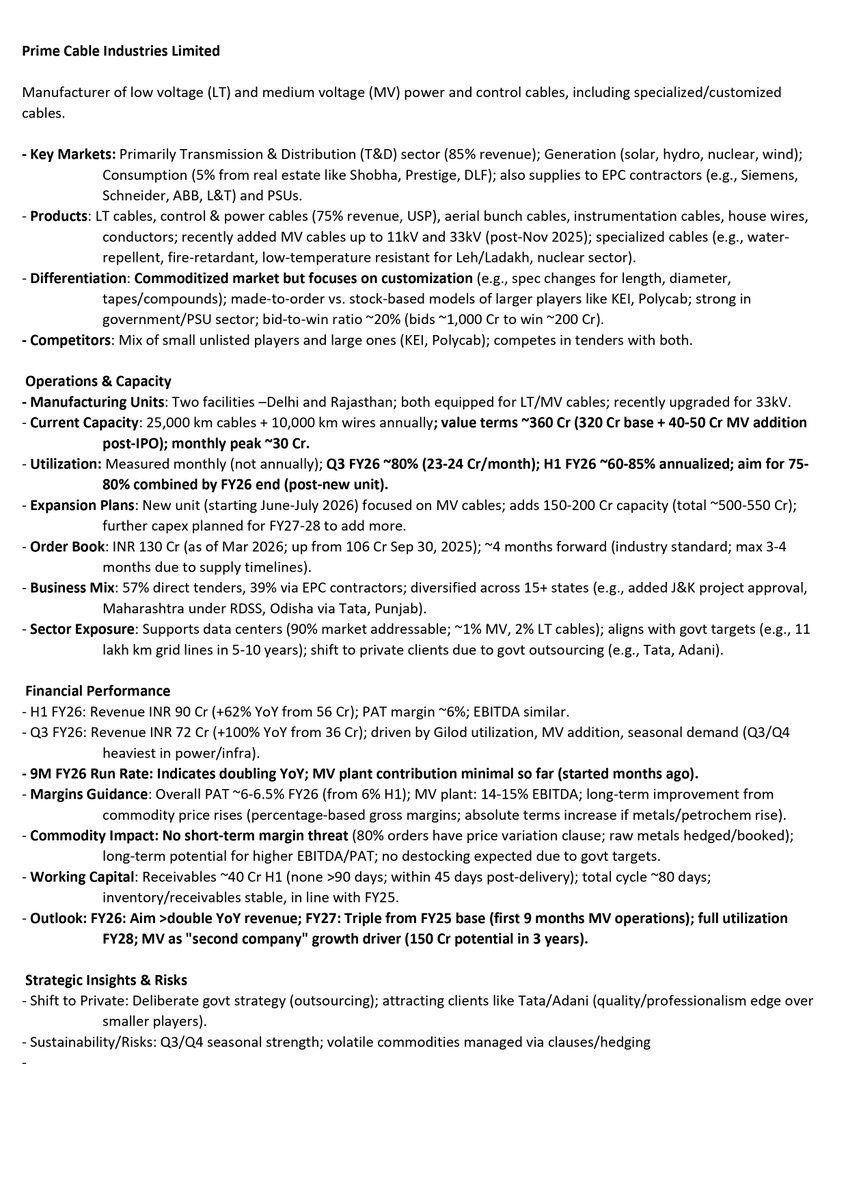

Arihant Bharat Connect Conference March '26:

👉Day 1:

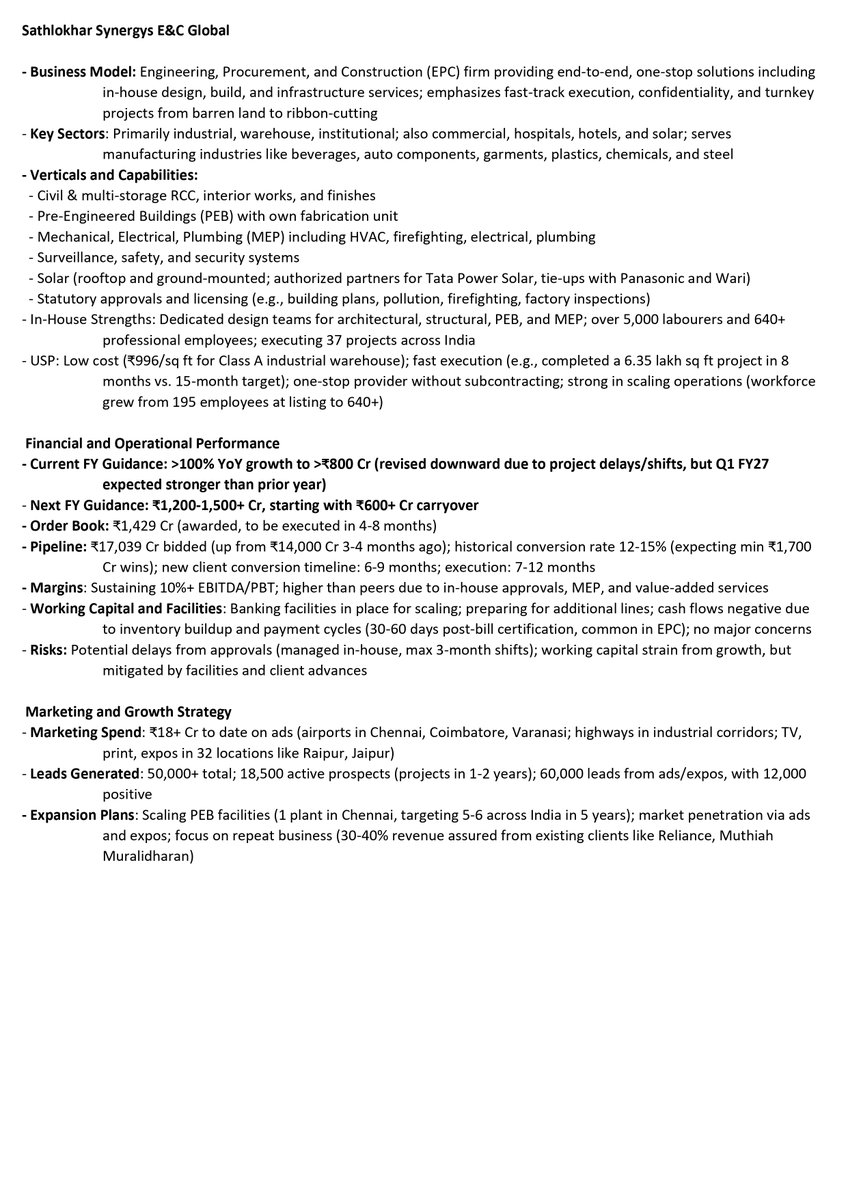

💠Sathlokar Synergys E&C Global

💠Prime Cable Industries

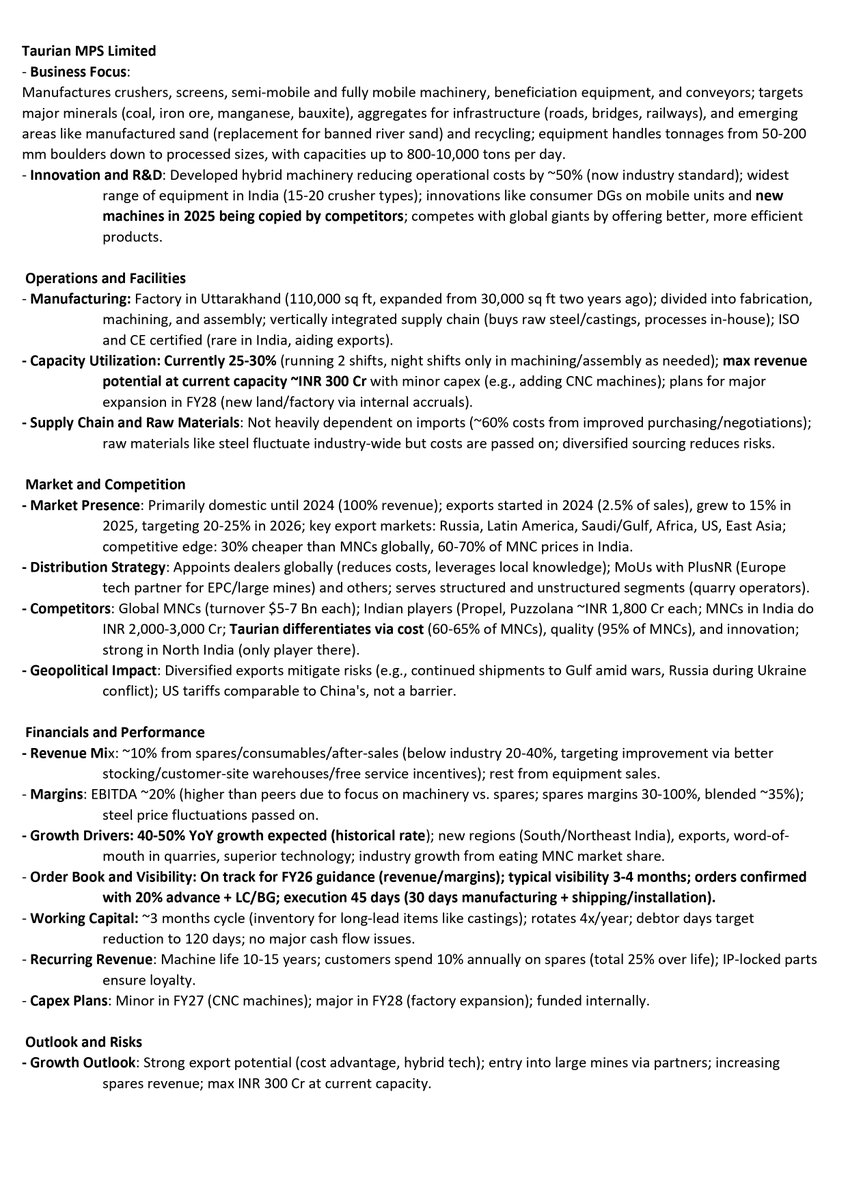

💠Taurian MPS

💠Shree Refrigerations

💠Silkflex Polymers

💠Classic Electrodes

💠TBI Corn

💠Dar Credit & Capital

#sathlokar #ssegl #primecab #primecableindustries #taurian #taurianmps #shreeref #shreerefrigerations #silkflex #classiceil #tbi #tbicorn #dccl #darcreditandcapital #bharatconnectconference #arihantcapital

dm aberta no surubyler https://t.co/fxVLZPktPW

stupid rarepair I pulled out my ass… I call them #vickcas AAAA I want to doodle them but idk how to draw I’m cooked

#jackpotcrashcourse #vickjcc #eloquentcountenance #forcas

#SME #Forcas #ForcasStudio

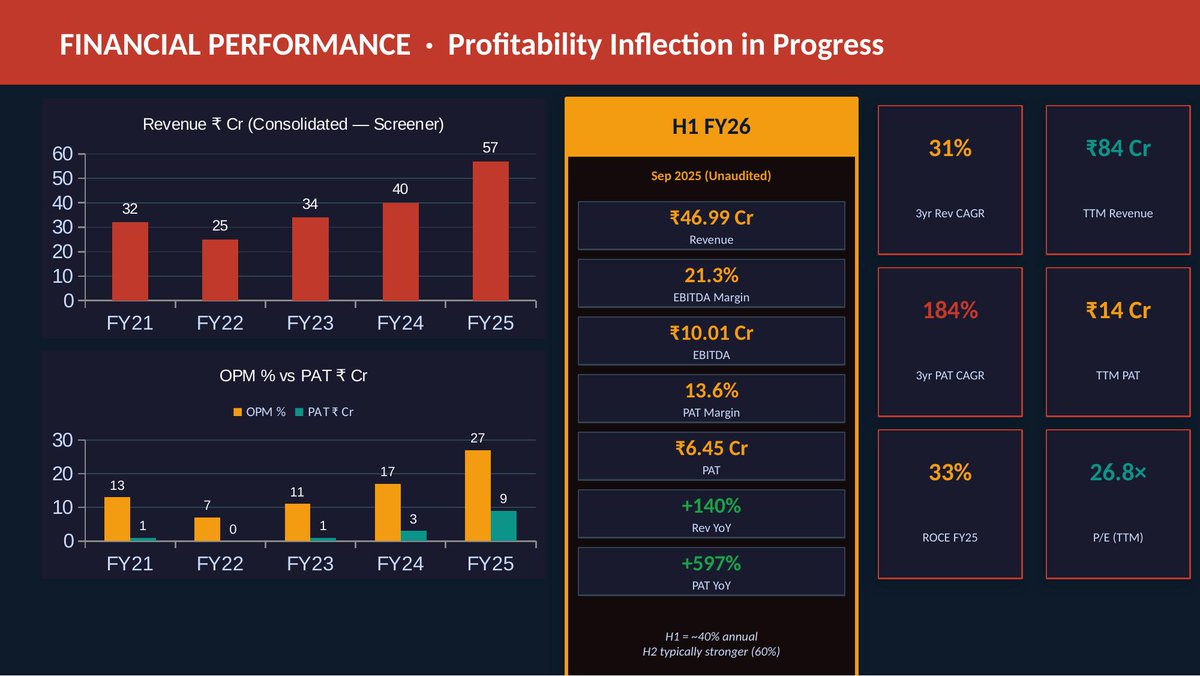

Forcas Studio H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️Emphasized a core target of ~35% YoY revenue growth, but as actuals exceeded this, expectations are now revised to 30-40% YoY for FY26

💠Own-brand revenue: ~₹72 Cr, with FTX at ~49% and TRIBE at ~35% growth

▫️EBITDA margins are expected to sustain and improve

💠Supported by higher-margin categories like women's wear (20-30% better than men's) and kids' wear (10-15% better than men's)

💠Rising ASPs (from ₹350-370 to ₹450) due to increased bottom wear sales

💠Net profit margins are projected to expand further, with H1 nearly doubling YoY profits, aided by channel diversification and low return rates (<12% vs. industry 18-19%)

👉Projects and pipeline:

▫️Quick commerce expansion: Stocked on Zepto across 17-18 cities (dark stores), delivering to 50-60 towns; added 7 new categories (e.g., kurtas, jackets, sweatshirts, trousers) since July, with rapid traction (e.g., kurtas driving sales in Hyderabad, Lucknow, South India; winter wear via 10-min delivery)

▫️E-commerce: Live on Myntra FWD with ~2,000 options; generated initial orders for shirts and denims from quick commerce platforms

▫️New categories: Women's and kids' wear under FTX launched offline first (₹5.5 Cr revenue to date); Varanasi warehouse added for UP/North India coverage

▫️Inventory pipeline: 2M units holding capacity (up from 600K); 90% is "set" inventory for proven SKUs, with intentional build-up for Q3 winter (e.g., sweatshirts, kurtas)

▫️Pipeline:

💠 Q3 launches: Online rollout of women's/kids' wear; new women's sportswear line (₹299-599 price band)

💠Expansion: Add 1-2 more quick commerce/e-commerce sites; deepen women/kids' lines; summer product pipeline with new options/channels

💠Growth Strategy: Data-driven stocking (pincode-level insights from 15+ years experience); omni-channel push (9 states for e-commerce, 15-16 cities for quick commerce); target 5-10% revenue mix from quick commerce by FY27 (rapid scaling expected post-3-month testing)

👉 Others :

▫️Customer acquisition: Added ~1mn customers in H1 via B2C platforms; strong repeat ratios and 4+/5 ratings on marketplaces

💠Asset-light (outsourcing manufacturing, no in-house production); lean omni-channel

💠No D2C for FTX due to high ad costs at low ASP ~₹400; prefer marketplace commissions of 30-33% only on sales)

💠Data / Algo optimization (views → clicks → conversions → low returns → availability) ensures visibility

▫️Working capital: Receivables down; inventory up 30-40 days due to 50%+ H1 growth/seasonality (Durga Puja shutdown, Punjab raw material crisis—strategic bulk buying in Aug-Sep)

💠Payables shortened (13 days) for supplier loyalty (earlier 124 days: FY24 / 47 days: FY25)

▫️Stake ownership: Promoter group subscribed 70-80% to warrants, increasing stake; no further dilution/debt planned

▫️Risk management: Low returns (tops <7%, bottoms 14-15%, avg. <12%) via quality focus and data (e.g., starting women's with low-return bottoms/athleisure); inventory write-offs <2% (test 100 new options/month at small depths, fail fast via discounts)

Last Seen Hashtags on Sotwe

Trends for you

Most Popular Users

Elon Musk

@elonmusk

240.2M followers

Barack Obama

@barackobama

119.3M followers

Donald J. Trump

@realdonaldtrump

111.6M followers

Cristiano Ronaldo

@cristiano

109.2M followers

Narendra Modi

@narendramodi

106.9M followers

Rihanna

@rihanna

97.3M followers

NASA

@nasa

92.1M followers

Justin Bieber

@justinbieber

90.6M followers

KATY PERRY

@katyperry

87M followers

Taylor Swift

@taylorswift13

80.8M followers

Lady Gaga

@ladygaga

72.3M followers

Kim Kardashian

@kimkardashian

69.5M followers

Virat Kohli

@imvkohli

68.8M followers

YouTube

@youtube

68.6M followers

Bill Gates

@billgates

63.5M followers

The Ellen Show

@theellenshow

62.5M followers

CNN

@cnn

61.9M followers

Neymar Jr

@neymarjr

61.4M followers

X

@x

60.9M followers

Selena Gomez

@selenagomez

60.1M followers