Top Tweets for #aimtronelectronics

#AIMTRONElectronics : Gets Pilot Box-Build Order Worth Up To USD 3.4 Million From Major Global Solutions Firm.

Engineering smarter automation starts with the right manufacturing partner. Visit #AimtronElectronics at #AutomationExpo2026 to discover design-led engineering, #embeddedsystems, high-reliability #EMS, and system integration for scalable industrial automation solutions.

#Aimtronelectronics #Aimtron

Aimtron Electronics — Quick Thesis 🧵

Revenue drivers: Gujarat greenfield adds ₹500 Cr peak capacity. Order book ₹521 Cr (+176% YoY) — 64% of FY27 already visible. US acquisition (ICS, $17M) opens overseas box-build revenues. Management targets ₹1,000 Cr by FY29 at 40–50% CAGR.

Margin levers: Refuses consumer electronics contracts on principle. ODM + Box-Build mix delivers 30–35% gross margins vs 10–12% for commodity EMS peers. Operating leverage means ~28% of every incremental rupee drops to profit. Post-IPO debt clearance has driven finance costs to near-zero — interest cover >70x.

Moat: Narrow but widening. MedTech, EV BMS, and Aerospace clients need 12–18 months to re-certify a new vendor — they simply don't switch. 90%+ client retention. No patent portfolio, but process know-how (thermal layouts, multi-layer micro-placement) creates a visible 3x margin gap over peers.

Management: 70.90% promoter stake. Zero pledges. Guided >70% growth — delivered 74% revenue and 89% PAT. IPO proceeds deployed exactly as communicated. Only watch item: historical related-party loops and 70% raw material import concentration.

Numbers: Revenue ₹301 Cr → ₹723 Cr (FY28E). EBITDA margin 22.6% → 25%. EPS ₹22.55 → ₹61.32. CFO flipped from -₹17.69 Cr to +₹92.50 Cr. ROIC 22–25% vs WACC ~11.5%.

Not advice. Do your own research.

Aimtron’s growth story is now in the spotlight.

Our Whole Time Director, Sneh Shah, joined NDTV Profit to discuss FY26 performance, growth drivers, and what’s next.

📺 Watch the full interaction: https://t.co/I6pHHMKs1D

#AimtronElectronics #EMS #MakeInIndia #NDTVProfit

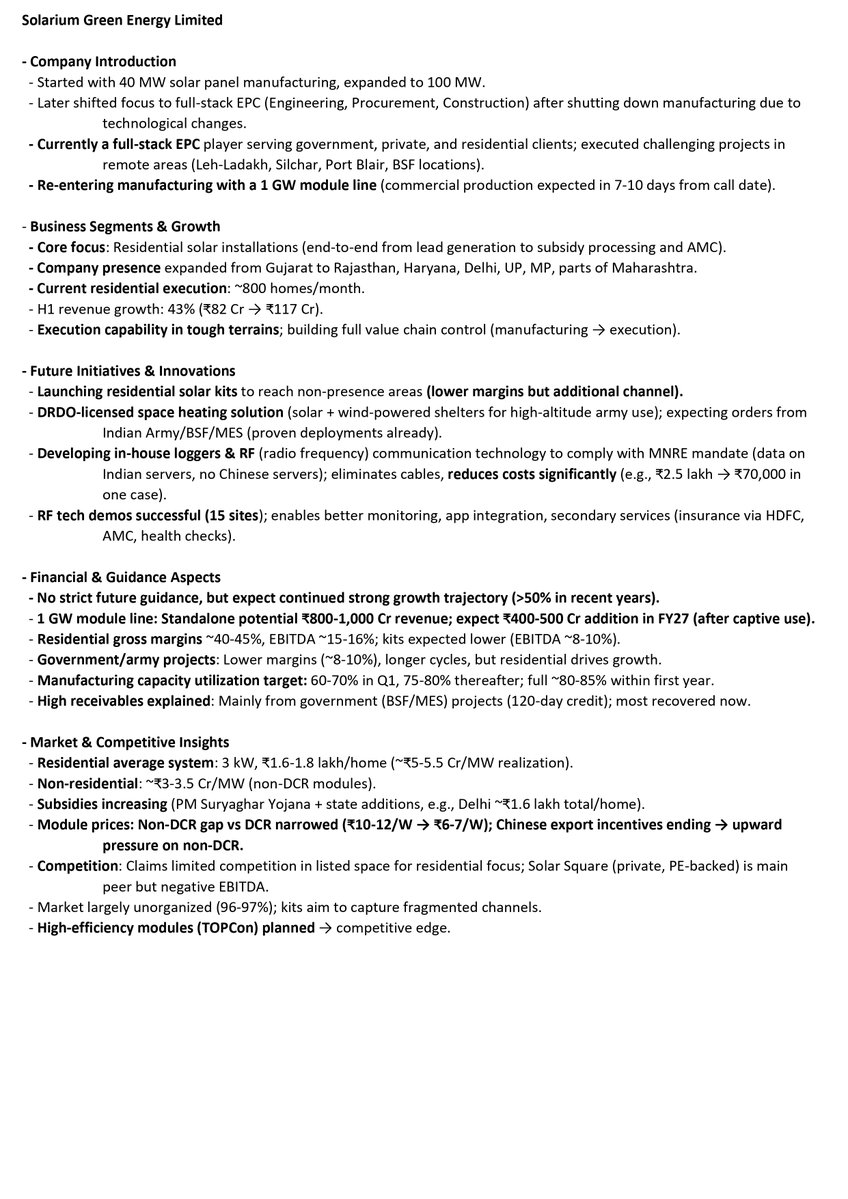

Arihant Bharat Connect Conference March '26:

👉Day 3:

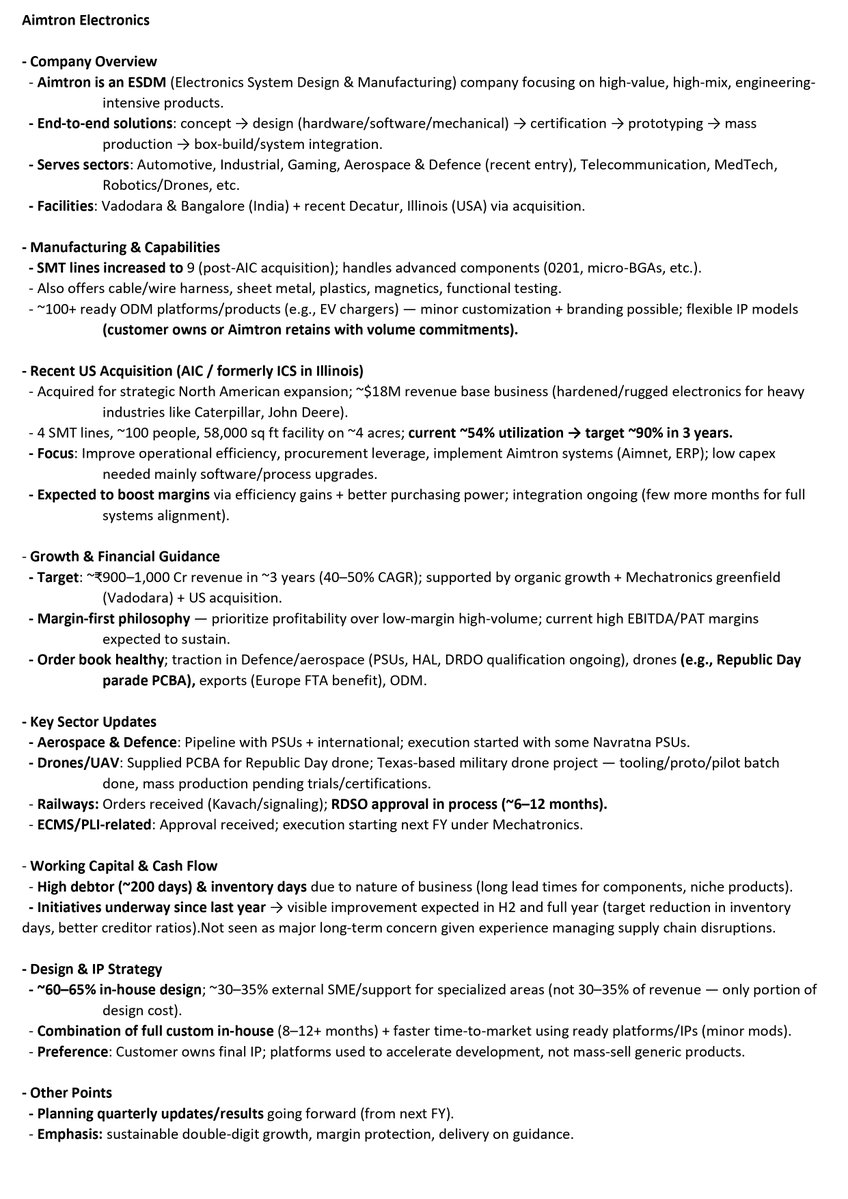

💠Aimtron Electronics

💠Solarium Green Energy

#aimtron #aimtronelectronics #Solariumgreen #soalrium #solariumgreenenergy #bharatconnectconference #arihantcapital

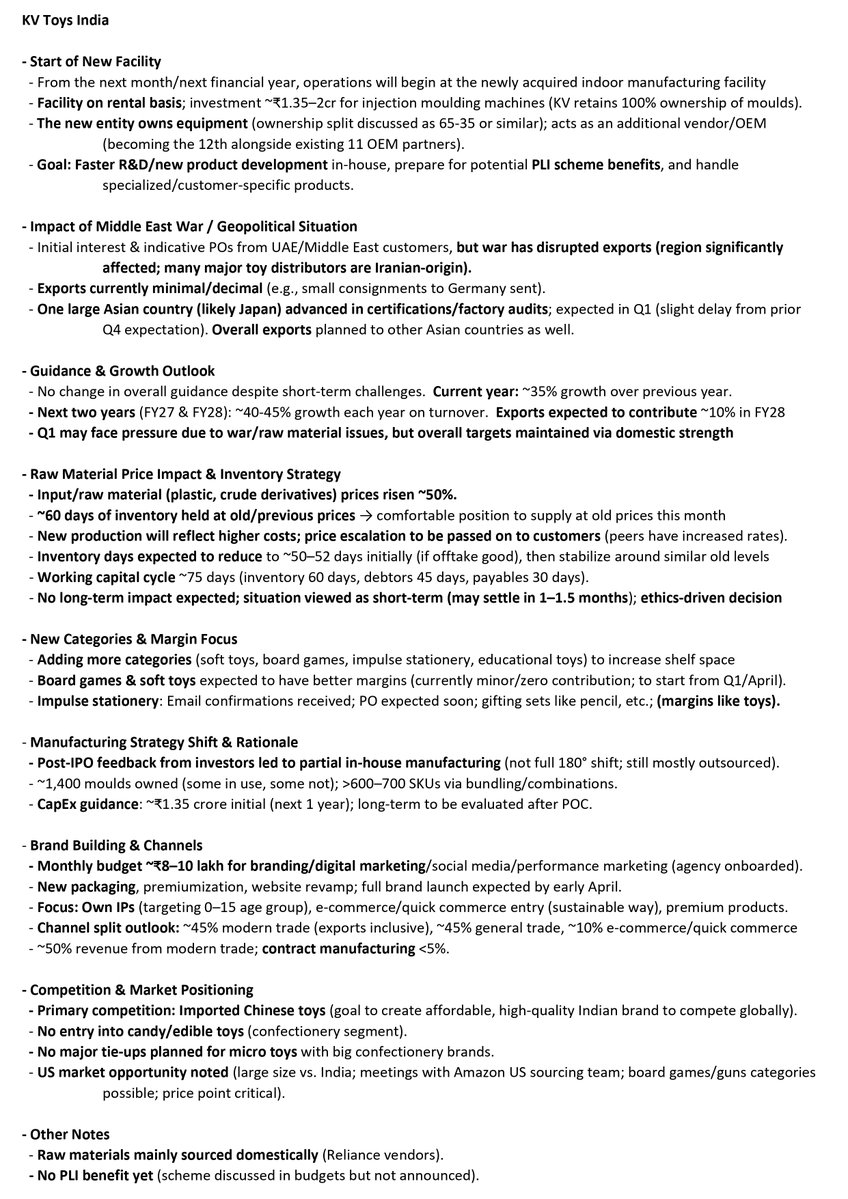

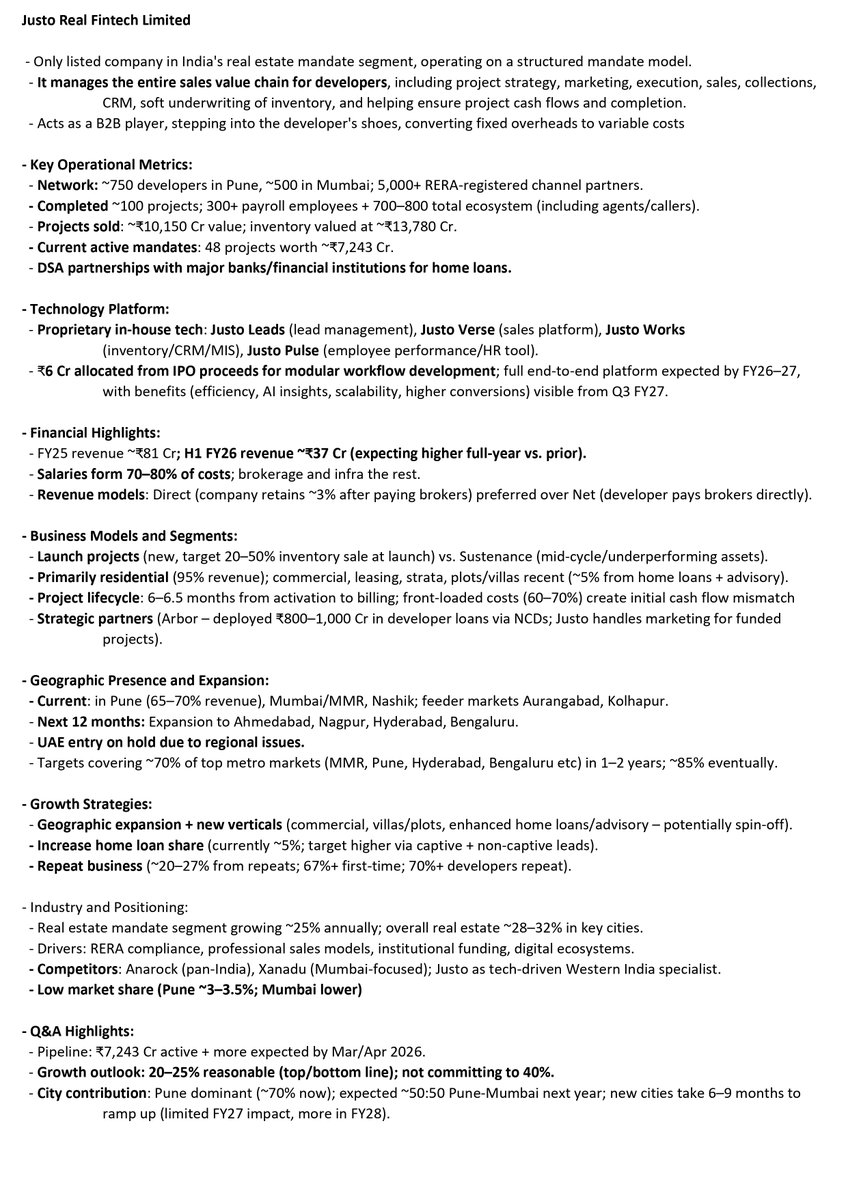

Arihant Bharat Connect Conference March '26:

👉Day 2:

💠KV Toys

💠Justo Realfintech

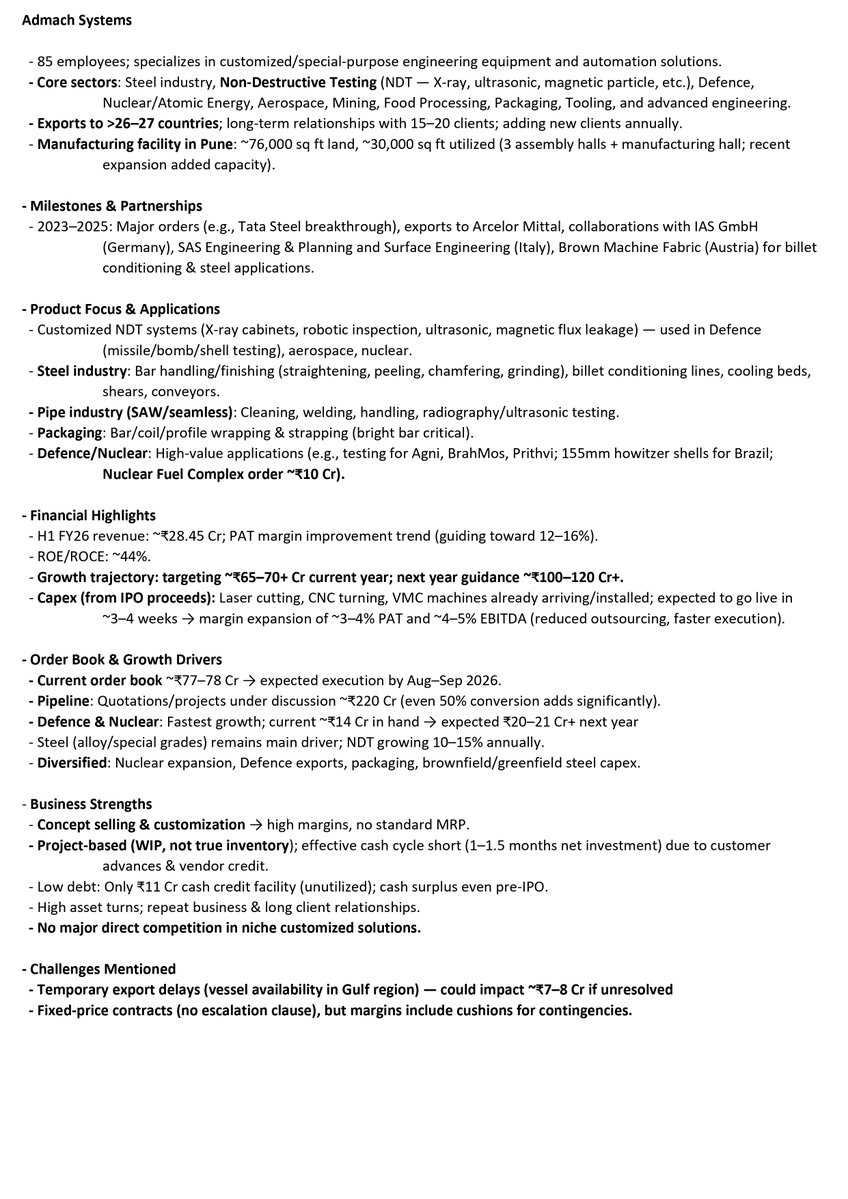

💠Admach Systems

💠AJC Jewel Manufacturers

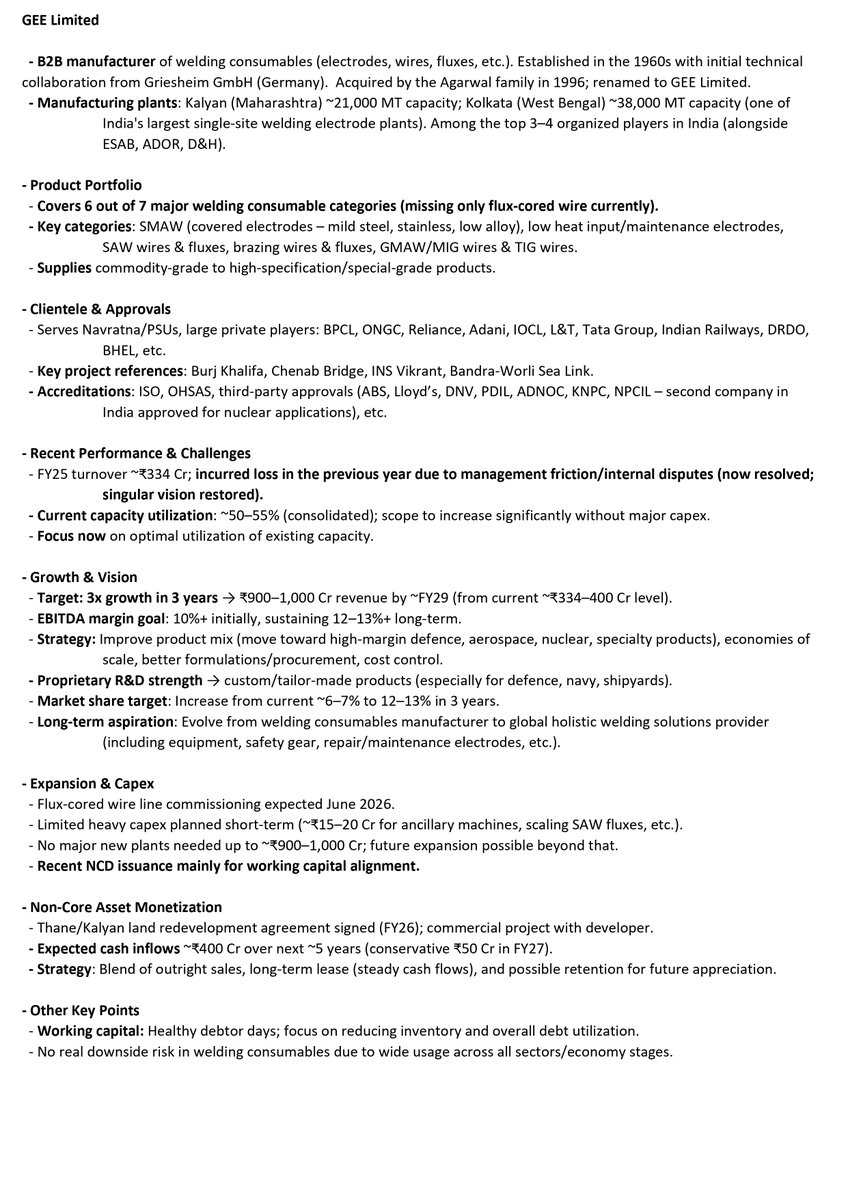

💠Gee Limited

#kvtoys #kvtoysindia #admach #admachsystems #justo #ajcjewel #gee #geelimited #bharatconnectconference #arihantcapital

#AimtronElectronics: Why an SME Company Looks Like a Mainboard Company (But Isn't)

Deep dive into the story of @aimtronindia Aimtron Electronics Ltd. as our equity research team member @LawofInvesting explores a rising star in India's Electronic System Design and Manufacturing (ESDM) sector. Listed on the NSE Emerge, Company is transitioning from a traditional PCB assembly player to a high-value, end-to-end "Box-Build" solutions provider

Link for Youtube video: https://t.co/h7oTyQ5Gxx

Key Highlights of the Analysis:

🟢The "Trinity Crossover": How Aimtron is positioned at the intersection of a massive electronics boom (22.8% CAGR), the "China+1" supply chain shift, and aggressive government policies like the ₹40,000 Cr ECMS booster.

🟢High-Margin Strategy: Discover how Aimtron maintains consistent 20-25% EBITDA margins by focusing on complex "heart" components for regulated sectors like Aerospace, Defence, and MedTech.

🟢Strategic US Expansion: An inside look at the 2026 acquisition of International Control Services (ICS) in Illinois, providing Aimtron immediate access to major US industrial OEMs like Caterpillar and John Deere.

🟢Financial Performance: From a turnover of ₹20 Cr in 2018 to a target of ₹270–280+ Cr for FY26, we break down the growth trajectory and operational leverage.

🟢Sector Diversification: Exploration of their multi-sector capabilities across EV chargers, medical ventilators, drones, and industrial IoT.

Why Watch?

Understand the structural moats—such as vertical integration and long-term customer stickiness—that make Aimtron a unique outlier in the competitive EMS landscape.

Disclaimer: This video is prepared for informational purposes only. Minerva Capital Research Solutions is a SEBI Registered Research Analyst (INH000018896). Please consult a financial advisor before making any investment decisions

#AimtronElectronics

Most powerful triggers from the recent presentation shared by the Co:

1. US presence with Acquisition of ICS ➡️ AIC

This is the biggest structural trigger

as it gives direct Access to US Industrial OEMs located in the “heartland” near Caterpillar, John Deere & CNH. These companies outsource hundreds of millions of dollars annually. This moves Aimtron from Indian EMS exporter to US domestic supplier.

That is a category upgrade.

2. Buy America, Build America Advantage:

This is a huge trigger. The US govt & OEMs prefer local manufacturing.

Now Aimtron has US manufacturing, India cost advantage and dual geography flexibility

This puts them in a tariff sweet spot

In current geopolitical environment, this is extremely powerful.

3. Utilization ramp from 54% ➡️ 90%

US facility currently running at only 54% utilization. Management target: 90% in 2-3 years. This means revenue growth without proportional capex, operating leverage and margin expansion. Low utilization plus strong pipeline leads to explosive earnings potential.

4. Margin normalization of acquired entity:

Currently the acquired entity has low double-digit EBITDA margins.

Management believes margins are low due to outdated MES systems & operational inefficiencies.

Co planning ₹10–12 crore capex for digitization and AI-based ERP & MRP upgrade. If margins move toward Aimtron standard levels then EPS can expand faster than revenue. This is the hidden upside.

5. High-speed US sales cycle

Current US revenue: $17M

Target: $25–30M in 2-3 year.

That’s 50–75% growth from US alone.

If execution works then consolidated revenue acceleration, stronger export mix and better valuation multiple

6. ₹1,000 crore scale ambition:

Revenue Target (FY28/29). So clear long-term roadmap. This is ambition-driven growth, not accidental growth.

7. Strong Order Pipeline:

₹150–155 crore near-term (conversion <3 months)

₹300 crore early-stage opportunities

Short sales cycle in US: Prototype turnaround 3–5 days.

Fast conversion and high visibility means strong near-term growth.

8. Ruggedized Electronics Capability:

Hyper-specialization in:

- Harsh temperature electronics

- Shock & vibration-resistant systems.

This opens Agrotech, Heavy machinery, Aerospace & Defense-adjacent applications

This shifts them toward high-value precision EMS, not commoditized PCB manufacturing.

#Aimtron therefore is no longer just an Indian EMS story. This is becoming 🇮🇳 India engineering base

with 🇺🇸 US industrial positioning and🌍 Tariff hedge. If executed well, this can become a valuation re-rating story, not just revenue growth.

#AimtronElectronics

Most important investor-relevant points from #Aimtron’s presentation on the ICS (USA) acquisition.

This acquisition not a flashy revenue acquisition, but a strategic capability, geography play and

Strong fit with India + US “China+1”& tariff-avoidance trend

If execution is clean, this re-rates Aimtron from SME EMS to global ESDM-ODM player

- Immediate US presence instead of 24 to 36 months organic build-up

- Direct access to US OEM ecosystem (Caterpillar, John Deere, CNH, BUNN etc.)

- De-risks tariff + geopolitics via multi-location footprint (India + USA)

Moves Aimtron up the value chain from EMS to ODM/full-stack ESDM

Current order book: ₹98 crore

RFQ pipeline: ₹155 crore

New enquiries: ₹325 crore (likely RFQs in 90 days)

This gives near-term revenue confidence, not just future hope.

EPS accretive from Year 1

Meets Aimtron’s ROCE & ROE benchmarks frm Year1

Utilisation currently 54%, targeted 90% in 3 years (big operating leverage)

Revenue scale potential: USD 25 to 30 mn without major capex

₹280–300 crore annual revenue potential from ICS over time

Supports Aimtron’s ₹1,000 crore revenue ambition

Engineering-heavy projects to structurally higher margins

Quality margin expansion, not cost-cut gimmicks.

- Pricing discipline (NRE, change-control, governance)

- Procurement synergies & BOM optimisation

- Shift to engineered assemblies, ruggedization & test-heavy builds

Incremental capex only ₹10 to 12 crore over time

Funded via USD 4.3 mn debt, internal accruals and warrants

No aggressive balance-sheet stress

#SME #Aimtron #AimtronElectronics

Aimtron Electronics Investor Meet Highlights:

👉Rationale and Key Highlights of the Acquisition:

▫️Target Company Profile:

International Control Services, headquartered in USA, is a 3-decade-old low-to-medium volume EMS provider

💠Specializing in high-mix rugged/hardened electronics for sectors like agritech, construction, heavy industries, oil & gas, aerospace, and defense

💠Provides immediate US market presence amid tariff uncertainties and "Buy America, Build America" trends.

▫️Assets and Infrastructure:

💠Includes a 58,000 sq. ft. facility with 4 high-end Korean robotic SMT lines, post-SMT capabilities, cleanroom, specialized testing for agritech/rugged environments, heavy box-build readiness, and ~3.9 acres for future expansion

▫️Acquisition Benefits vs. Organic Growth:

💠Immediate access to US customers and Midwest ecosystem (proximity to OEMs like Caterpillar, John Deere)

💠Experienced engineering/program team; saves 24-36 months compared to building organically, including customer trust, qualifications, and operational maturity

▫️Deal Structure:

💠100% acquisition through wholly-owned US subsidiary (Aimtron Electronics Texas); valued at ~5-6× EBITDA (implying ~USD 8-12M enterprise value)

💠Complements Aimtron's capabilities with synergies in operations, procurement, and cross-selling

👉Growth Outlook and Financial Impact

▫️Current Performance:

💠~USD 16.9M revenue; operating at ~54% capacity with low-double-digit EBITDA margins

💠Open order book ~₹100cr, pipeline ~₹155cr (quick <3-month conversion), broader opportunities ~₹300cr (e.g., $20M+ oil & gas deals)

▫️Investment and CapEx:

💠 USD 4.3M Debt raised locally in Texas (via the wholly-owned subsidiary, Aimtron Electronics Texas) to partially fund the acquisition

💠Minimal near-term needs; ~INR 5-6 cr incremental working capital

💠~INR 5-6 cr CapEx for ERP/AI/digitization

💠Total phased ~INR 10-12 cr to unlock full potential without major new additions

▫️Revenue Scaling Targets:

💠Scale business to USD 25-30M in 2-3 years via utilization ramp to ~90% (phased, award-led)

💠Supports Aimtron's overall ₹1,000cr journey by FY28-29, combining India's 40-50% organic CAGR with US's 20-30% steady growth

▫️Margin Improvement:

💠Target Aimtron-level margins (high-teens to 20%+ EBITDA) through global procurement leverage, operational efficiencies (ERP/MRP digitization, AI/Industry 4.0), resource optimization, and shift to higher-value box-build (from ~85% PCBA to more integrated solutions)

▫️Sector and Synergy Opportunities:

💠Adds ruggedization expertise for harsh environments;

💠Opens new sectors like agritech automation; enables regional manufacturing for North America/Asia/Europe, with cross-selling to Fortune 100/500 clients

👉Q&A Highlights :

▫️Margin Concerns:

💠No long-term dilution expected; higher US labor costs offset by material pass-throughs, efficiency gains from updated systems/processes

💠Lower regional costs (15-20% below major metros)

▫️Tariff/Geopolitical Positioning: Viewed as "win-win" for flexibility—if tariffs ease, India benefits

💠If not, US facility enables compliance and local proximity; shifts buying tendencies without halting US consumption

▫️Integration: Emphasis on smooth transition (90-day plan), retaining local leadership; personal commitment from management to meet high expectations

▫️Future M&A Outlook: Opportunistic and goal-oriented (global partnerships, ₹1,000cr target)

💠No rushed timeline, prioritize integration first; evaluate based on investment risk, complementarity, and network opportunities (including off-market deals)

Proud of the values that define our Republic—unity, responsibility, and progress.

At Aimtron Electronics, we continue to innovate with purpose, contributing to a stronger India and a better tomorrow.

Happy Republic Day

#RepublicDay #India #AimtronElectronics #ProudToBeIndian

#AimtronElectronics

Very High-Probability 25-30% CAGR

Reasons:

- Defence, railways, exports, US acquisition

- Certifications create entry barriers

- Early stage of scale-up

- Risk: Working capital + integration risk

#AimtronElectronics has entered:

Railway signaling & train safety electronics (mission-critical systems)

via arrangement with an established Indian railway signaling technology provider.

Aimtron’s role here is manufacturing, system integration and Testing & QA

( not just low-end EMS)

This is safety-critical, regulated, high-reliability electronics.

This is a BIG positive (Strategic Significance) as has:

- High entry barriers

- Long qualification cycles

- Rigorous certifications (SIL, redundancy norms, audits)

- Once qualified → sticky, long-duration programs

This naturally filters out low-quality EMS players

Railway signaling is:

- Process-led, not volume-led

- Execution & quality matter more than price

This is a moat-building segment, not a commoditized one.

Indian railway equipment market → USD 15.9 bn by 2030

Key drivers:

Kavach (ATP rollout)

Metro rail expansion

Safety upgrades

Digital signaling

This is multi-year capex, not cyclical demand.

Aimtron is now present in:

Railways

Metro

Defence (earlier)

Infrastructure monitoring

Exports / North America (earlier)

It reduces dependence on pure commercial EMS cycles.

Earlier TAM:

EMS + design services

Now TAM includes:

Regulated infrastructure electronics

Safety-critical manufacturing

Rail + metro ecosystems

This is a step-function jump in addressable market quality, not just size.

This press release is HIGH QUALITY, not marketing fluff.

It signals:

Structural move into high-barrier electronics

Management thinking long-term

Capability confidence

Strong alignment with India’s infra + safety capex cycle

Finally, this development improves the probability (not guarantee) of Aimtron delivering sustained high-quality growth over many years.

#AimtronElectronics

Management has publicly stated its intention to grow at 40-50% CAGR over the next 3-5 years from a combination of exports, design-led services, and new capacity.

They are investing in greenfield capacity, advanced SMT lines, and AI-enabled processes to support this growth.

Aimtron’s recent performance underpins its strategy:

• >100% YoY revenue growth in H1 FY26 driven by exports, defence, IoT and ODM.

• A robust and diversified order book (3× FY25 revenue).

Structural Positives:

- Policy tailwinds (India’s ESDM, China+1 supply shift).

- Growing global demand for design-to-manufacturing EMS/ODM.

- Strategic certifications enabling premium sectors.

- The company is expanding TAM in meaningful ways (exports, global offices, ODM contracts)

- It has entered strategic sectors (defence & aerospace) via certification and orders

- Management is ambitious and vocal about aggressive growth targets

⚠️Risks:

- Cash flow cycle & working capital in EMS businesses can be lumpy.

- Large ramp-ups (new lines, global sales) often take time and investment.

- The high CAGR target is management guidance not guaranteed and subject to competitive pressures and macro cycles. A sustained 40% CAGR is a target, not yet proven over multiple years

- Growth will depend heavily on execution, customer conversions, and global demand cycles

#AimtronElectronics

Cmp- 880

Aimtron isn’t just a contract manufacturer, it offers a full Electronics System Design and Manufacturing (ESDM) stack, including:

- PCB design and prototyping

- Turnkey PCB assembly (PCBA)

- Electromechanical box builds

- Cable/harness assemblies

- Custom test fixtures and value-added services

*Competitive edge:* Many smaller EMS firms only handle assembly; Aimtron’s design + manufacturing continuum lets it capture more value, serve higher-complexity projects, and shorten customer time-to-market.

*Moat aspect:* Higher switching costs for clients once trusted with both design and production — losing a partner costs more than just moving an assembler.

1 Day to Go!

Tomorrow we unveil the next chapter of AI-enabled #robotics at #EFYGujarat2025.

Visit Aimtron Electronics at Booth C3 to experience smart, fast & contactless automation — live in action.

21–22 Nov | Helipad Exhibition Centre, Gandhinagar

#AimtronElectronics #AI

1 Day to Go!

We’re all set for Auto EV Bharat 2025 starting tomorrow!

Visit Aimtron Electronics at Booth E-12 to explore EV electronics, PCB assemblies & ODM solutions.

Nov 19–21 | KTPO, Bengaluru

#AutoEV2025 #EVManufacturing #AimtronElectronics

Bright future for #aimtron. One of the Potential companies to lead India globally in deep tech space..

#aimtronelectronics

#SME #Aimtron #AimtronElectronics

Aimtron Electronics H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️Reiterated the 50-60% CAGR growth outlook

💠Implying full-year revenue in range of ~250-270cr

▫️EBITDA margins are expected at ~20%+

💠Sustainability emphasized due to ODM focus and operational leverage

💠PAT margins at 15% (±2%), supported by box-build mix (expected to rise from 35% in H1 to >50% in H2)

💠Tariff/geopolitical challenges were navigated without major margin erosion, with normalization expected in H2 via improved product mix (Wi-Fi 6/7 telecom equipment)

👉Order book / projects and pipeline:

▫️Current order book : ~460cr+

💠Sector breakdown: Telecom (33.5%), Power (20.9%), IoT (18.6%), Industrial (9.3%), Automotive (8.0%), AI (3.3%), Green Energy (2.3%), Others (4.1%)

💠Region: India (77.9%), USA (20.7%), Spain (1.5%)

💠Key H1 projects include: ~98Cr ODM contract with US infrastructure firm (design-to-mass production for data centers/comms); ~46 Cr domestic AI/IoT box-build (50,000 units, multi-year scale-up potential)

▫️Navratna PSU order discussion; in electronic comms (military/radar PCBs, high-value like 32-layer boards at ₹32L/module)

💠Long qualification, not major book portion yet; sustainable growth over optics

▫️Pipeline:

💠 ~700-800 Cr RFQ open (conversion ongoing, 6-15 month cycles for ODM)

💠Tier-1 targets like $8B US firm (~400-500 Cr over 3-5 years), Indian power global player (~50-100 Cr)

💠Also focus on Airbus A350 qualification (control box/cable, 10-20 year programs), drone/military comms expansions; NDAs/audits progressing

💠Emphasized defense sustainability over volume (double-digit contribution cap initially), with PSU bids and global (e.g., US Navy/Texas troops) inquiries accelerating post-AS9100D certification

👉 Others :

▫️Fundraise & Expansion: ~95Cr via convertible warrants for greenfield subsidiary

💠3-acre Vadodara facility (6 SMT lines phased: 2 in FY27 Q3/Q4, then 2 annually)

💠Adds ~500 Cr capacity to existing ~450-500 Cr, targeting ~1,000-2,000 Cr total with minor CapEx 3-5% of revenue)

💠Rule-of-thumb ~100 Cr/line potential

💠In-house cable assembly post-IPO; outsourcing sheet metal/plastics now, but greenfield eyes vertical integration (drop-shipment ready products)

▫️Strategic Shifts: Reverse engineering focus (design-first for manufacturing tailwinds); ODM emphasis; 💠Entry into AI/IoT/green energy; global footprint (Texas/Germany sales offices)

💠Debt-free as of Sep 2025; exploring M&A (5-6 shortlisted, culture/talent focus for inorganic growth in new sectors/expertise, post-tariff stability)

▫️PLI/ECMS Exploration: Evaluating for passive components/SFD (telecom traction); no firm commitment yet

▫️Risks: Balanced defense entry (high margins over volume); continuous SWOT/agility amid geopolitics; "let results speak" ethos, with 69-70% promoter holding

▫️Certifications: AS9100D (aerospace/defense access); ISO 14001 (EMS); IPC-A-610 Class 3; State-of-art SMT (Japanese machines, AI/MES integration for paperless ops, 2-4x output scalability)

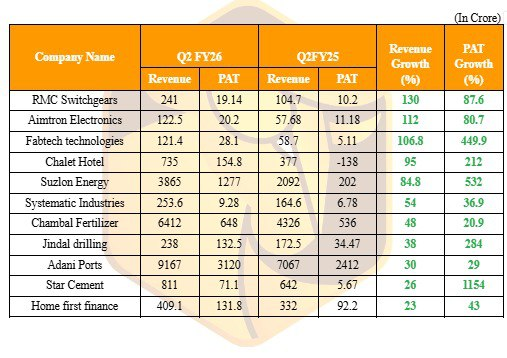

#Q2FY26 Good Result!!

List of companies that have reported growth of 20%+ over Revenue and PAT as on 04/11/2025.

#RMCSwitchgears

#Aimtronelectronics

#Fabtech

Last Seen Hashtags on Sotwe

Trends for you

Most Popular Users

Elon Musk

@elonmusk

240.9M followers

Barack Obama

@barackobama

119.2M followers

Donald J. Trump

@realdonaldtrump

111.8M followers

Cristiano Ronaldo

@cristiano

111.7M followers

Narendra Modi

@narendramodi

107.1M followers

Rihanna

@rihanna

97.9M followers

NASA

@nasa

92.2M followers

Justin Bieber

@justinbieber

91.2M followers

KATY PERRY

@katyperry

88.3M followers

Taylor Swift

@taylorswift13

82.2M followers

Lady Gaga

@ladygaga

73.7M followers

Virat Kohli

@imvkohli

70.9M followers

Kim Kardashian

@kimkardashian

70.1M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

64.2M followers

Neymar Jr

@neymarjr

63.7M followers

The Ellen Show

@theellenshow

62.4M followers

CNN

@cnn

61.8M followers

Selena Gomez

@selenagomez

61.4M followers

X

@x

60.8M followers