Pulled the trigger today and switched 100% of Lindy traffic to DeepSeek v4, churning from Anthropic models.

Saves us millions of $ and we're actually seeing an *increase* in performance on many core use cases. Transformative for the business.

Labs rug pulling the subsidy to turn profitable makes it near impossible for companies downstream to demonstrate ROI.

We’ve just seen a wave of redundancies justified by AI efficiencies. Those budgets were built on subsidised token cost which has now been blown out the window.

The true cost is starting to show up and is why companies are burning through their annual token budget in weeks.

🦔GitHub Copilot switched to token-based billing this morning and users are already out of credits. Pro+ subscribers paying $39 a month are reporting 60% of their credits gone in two hours of normal use. One user lost 20% of their allowance from a single file review with no code changes. Another hit their monthly cap before the calendar even flipped to June.

Orgs with shared token pools have no way to see individual usage, so entire teams get cut off when one person runs a heavy prompt. Users are canceling and moving to Claude Code and Codex. GitHub community forums are on fire.

My Take

Flat-rate AI subscriptions were always subsidized. Everyone in the industry knew it. Today the subsidy ran out for a few million developers at once. The problem is a lot of companies already restructured around these tools. They cut headcount and told remaining engineers to lean on Copilot instead of building skills internally. Those companies now depend on a tool whose cost just became unpredictable and whose usefulness completely changes when you have to ration prompts to stay under budget.

The developers moving to Claude Code and Codex will hit the same wall eventually. Every AI provider faces the same unit economics. Anthropic filed its S-1 this morning, and the durability of its revenue depends on whether customers stick around once real pricing kicks in everywhere. If a $39 subscriber cancels after one day because the tool became unusable, multiply that across millions of seats and the churn risk becomes very real.

Today showed what happens when AI pricing meets reality. The companies that built their workflows around cheap tokens just discovered the tokens aren't cheap anymore and the people who knew how to do the work without them are already gone.

Hedgie🤗

Labs rug pulling the subsidy to turn profitable makes it near impossible for companies downstream to demonstrate ROI.

We’ve just seen a wave of redundancies justified by AI efficiencies. Those budgets were built on subsidised token cost which has now been blown out the window.

The true cost is starting to show up and is why companies are burning through their annual token budget in weeks.

Google is reportedly planning to sell up to $80B in new shares to fund growth, with Berkshire Hathaway said to be considering a $10B investment in $GOOGL.

Today I learnt in 1913, John D. Rockefeller’s net worth peaked at 3% of the country’s GDP.

Elon Musk’s paper worth is the same today ($850 bn/$30,500 bn).

His net worth exceeds the GDP of 83% of the world’s nations.

How do you even comprehend the scale of that? Wild.

I think we're going to need the log scale to chart the @grass revenue ramp

"Despite everybody thinking the market is super crowded, we still don't have enough good quality data vendors that actually understand how to deliver product plus services in a way researchers are looking for."

"I have not seen a contract for genuinely good data gets turned down because of budgetary concerns yet."

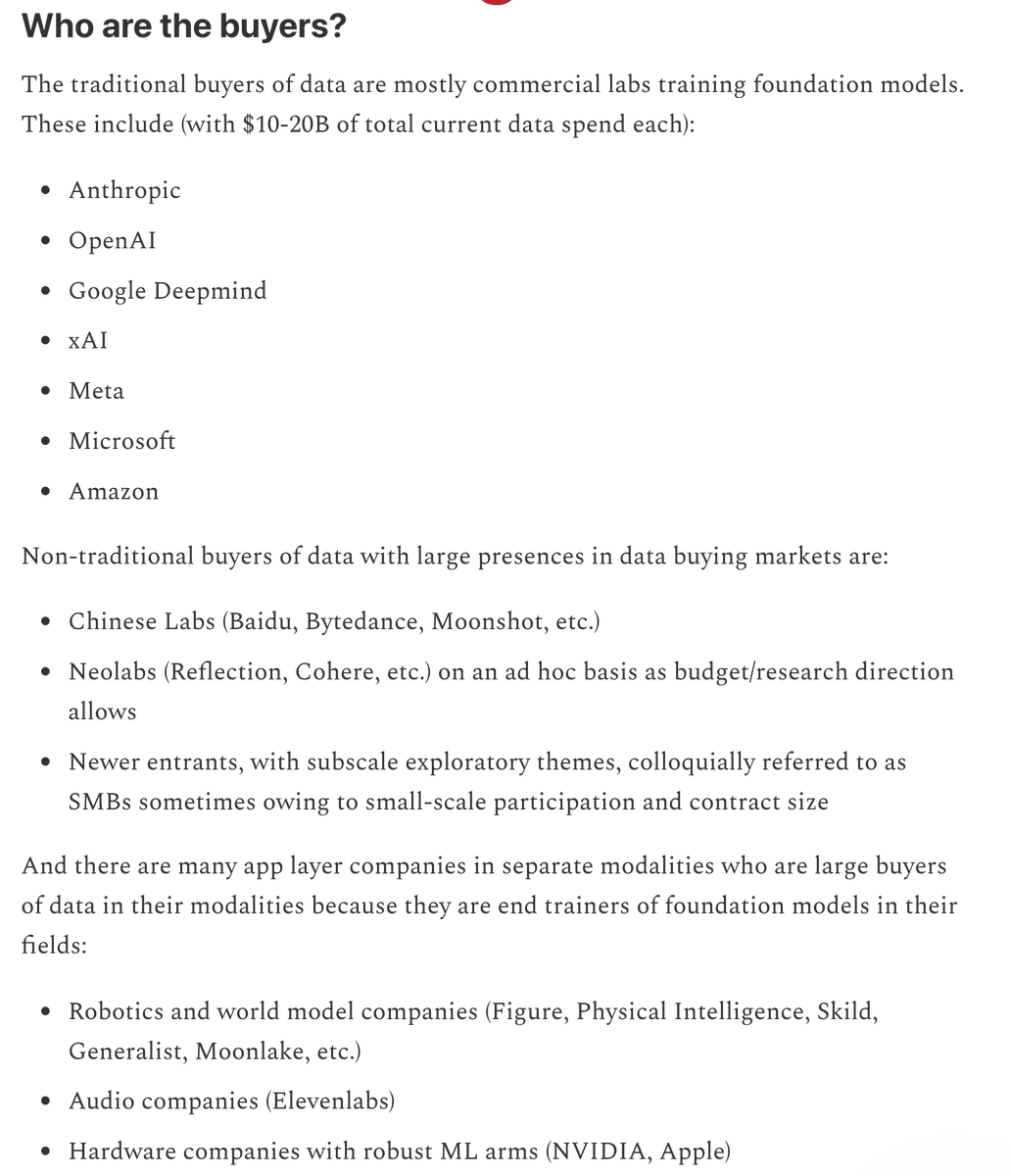

SITUATION EXPLAINED: How much are frontier labs actually spending on training data?

.@SeanZCai: "Frontier labs are spending about $10 to $15 billion per lab on data."

"Really good long horizon tasks go up to $20,000 each. A complete browser-use version of SAP was rumored at $500,000."

"Despite everybody thinking the market is super crowded, we still don't have enough good quality data vendors that actually understand how to deliver product plus services in a way researchers are looking for."

"I have not seen a contract for genuinely good data gets turned down because of budgetary concerns yet."

Hmm... solana:Grass7B4RdKfBCjTKgSqnXkqjwiGvQyFbuSCUJr3XXjs

"Data sold is, therefore, very much resembling selling outcomes rather than an actual reusable product, which is why one must obsess about indexing on the scalable means of producing internal systems that can help end model trainers produce outcomes rather than fixating on data itself when evaluating RL environment companies.

In this way, the TAM of data markets is actually extremely greenfield and growing, because few teams have the sophistication for research services and scale for on demand consistently QA’ed data"

On data markets:

A while ago, Anthropic said that they would be spending a billion dollars this year on RL data. This year, that amount will be far exceeded, with good data rarely being turned down for budget concerns. We can expect OpenAI to be of similar mindset, although the window for banal data projects serviced by the likes of Mercor is rumored to be closing entirely this year. Deepmind, Meta, Microsoft, Amazon, and xAI are known to be N-1 labs who may buy datasets already saturated by the likes of Anthropic, or buy RL environments in light of not having a system like Tundra in Anthropic.

The TAM is still 10s of billions if not more and the raw aggregate spent on data will only continue to increase.

But one must remember what is bought when data is sold, because few today can really differentiate Mercor/Handhshake from a Mechanize/Surge. Data is valuable, to frontier labs, based on how much it can be easily used to improve frontier models. To show this capability, it matters whether teams selling data can show how most directly it can be used to hillclimb models, how much frontier SOTA models struggle on its benchmarks, and how much trouble they can save the frontier lab in its continual acquisition. Data sold is, therefore, very much resembling selling outcomes rather than an actual reusable product, which is why one must obsess about indexing on the scalable means of producing internal systems that can help end model trainers produce outcomes rather than fixating on data itself when evaluating RL environment companies.

In this way, the TAM of data markets is actually extremely greenfield and growing, because few teams have the sophistication for research services and scale for on demand consistently QA’ed data. It is the semblance of this product with which Mercor was able to overtake Scale, the semblance of this product which many newer upstarts are painting as an argument to chip away at Mercor/Handshake/Surge’s lunches.

From my April's edition of State of Data on substack:

the two companies i can see coming through mostly unscathed are apple & amazon

both have extremely strong differentiated asset heavy moats that are hard to displace and stand to benefit hugely from the ai & robotics wave

The next GRASS Token Holder and Network Participant Call will take place on July 7. The call will provide an overview of Grass network progress, the development roadmap, business milestones, growth highlights, and more.

To promote equal access to information, the call will be open to the public. Questions may be submitted in advance for consideration during the session.

Further details, including the exact time and registration information, will be shared soon.

There’s enough demand for tokens right now that the likes of uber & microsoft capping their ai budgets won’t be felt by the model companies for a while.

Eventually this will all reconcile & we’ll see token demand start to plateau & more emphasis placed on value per token type metrics.

Explains why the labs have acquired consulting arms to work with clients on implementation & likely show some real & many made up value creation metrics.

Anyway, the buildout & eventual subsequent gains are not going anywhere on a medium term time horizon so when the market decides this fud is sufficient, buy the dip.

There’s enough demand for tokens right now that the likes of uber & microsoft capping their ai budgets won’t be felt by the model companies for a while.

Eventually this will all reconcile & we’ll see token demand start to plateau & more emphasis placed on value per token type metrics.

Explains why the labs have acquired consulting arms to work with clients on implementation & likely show some real & many made up value creation metrics.

Uber’s COO has said that it’s getting “harder to justify” its AI costs because there was no way to show a link between AI spend and any meaningful increase in useful features. This is the first time I’ve seen a company say this directly.

https://t.co/xUhZvtpwah