We are a payments company.

At the StoneX Conference, @DanielIshag, Chief Commercial Officer at Bakkt, joined the panel “The Role of Stablecoins in Global Finance”.

Thank you to @StoneX_Official for hosting the conversation and bringing together leaders across payments, digital assets, and financial infrastructure.

For important information: https://t.co/MJO8pIBnOz

@Bakkt $BKKT @mikealfred

Single biggest change in last 6 months is that Bakkt is now 'Founder-Led' with @Akshay_Naheta owing 20%+ of the company. Focused execution will lead to revenue growth and margin expansion. Need to control dilution. Meets my criteria of 100 bagger.

Still day one. 🚀

1️⃣ India 🇮🇳 and Japan 🇯🇵 are just getting started.

2️⃣ Tokenization is just getting started. 🔗

3️⃣ Stablecoins as settlement rails are just getting started. 💵

The biggest value creation lies ahead as we continue to build and scale these businesses. We're running a marathon, not a sprint.

Separately, @Bakkt Markets volume continues to expand, and I'm encouraged by the progress we're seeing relative to the guidance provided on our last earnings call. 📈

Heads down. Executing. ⚙️

$BKKT

The Company Inside Bakkt

Over the past year #Bakkt changed its CEO, its core business, its board and its balance sheet. The stock price still reflects the old company, not the new one – and that's the opportunity.

A few days ago I said I bought 22,000 shares at $10.20. Let me show you the company inside Bakkt.

Start with the old Bakkt. It was built inside the New York Stock Exchange. ICE, the NYSE's parent, launched it in 2018 and took it public in 2021 at a $2.1 billion valuation. Then it lost the plot. The first leg down came post-SPAC, when the original vision never materialized and the stock collapsed roughly 95%. The second leg came on March 17, 2025, when Bakkt disclosed in an 8-K that both Bank of America and Webull were walking from their contracts. Webull alone was 74% of crypto revenue. The stock fell 27% that day and shareholders sued.

Then, four days later, the company did something unusual.

On March 21, 2025 — the same week the existing revenue model died — Bakkt brought in Akshay Naheta (@Akshay_Naheta) as co-CEO and signed a commercial partnership with his stablecoin payments firm, DTR. If that name doesn't mean anything to you: Naheta spent five years at SoftBank investing next to Masa Son, with a hand in the ARM and Nvidia positions. By August, the old CEO was gone and Naheta was running the company alone. The loyalty business was sold off. The dual-class super-voting share structure was scrapped. The balance sheet was cleared out: no debt, $82.6 million in cash. In October, Mike Alfred (@mikealfred) joined the board, then Lyn Alden (@LynAldenContact) a few days later. And in January 2026, Bakkt formally acquired DTR. On paper, Bakkt acquired DTR. In substance, it was a reverse merger — the acquired company is now running the acquirer.

So when you pull up $BKKT today, the chart you're looking at belongs to a company that effectively no longer exists. New CEO, new core business, new board, a clean balance sheet. The only things that carried over are the NYSE listing and the licenses. And the licenses, as you'll see, are the one piece of old Bakkt actually worth keeping.

That gap is the entire opportunity. When the company underneath a ticker gets swapped out but the ticker, the name and the chart all stay, the price can sometimes stay stuck to the ghost.

Even the one number that looks current is misleading. The headline says Q1 revenue "collapsed 77%." But open the filing. Revenue was $243.6 million. Of that, $242.0 million was pass-through crypto cost. The actual margin left over was about $1.6 million. Bakkt's "revenue" was always gross transaction notional, a number that looks enormous and tells you nothing. The real cost of running this company is around $18.5 million a quarter, against $82.6 million in the bank.

Now look at what the new company owns.

The licenses come first. Pan-U.S. money transmitter licenses, a New York BitLicense, a European VASP license. And while that may sound trivial, it's actually what protects the business. Assembling that stack from scratch takes 2-3 years and millions of dollars. Plenty of bigger players have it — Coinbase, Circle, PayPal, Robinhood — but for each of them, licensed crypto payments is one piece of a much wider business. The faster route is M&A, which is why Stripe paid $1.1 billion for Bridge and Mastercard paid $1.8 billion for BVNK — both private. As far as I can tell, Bakkt is the only publicly traded, NYSE-listed company whose entire forward business is the licensed stablecoin payments rail. If you want public-market exposure to this, there is nothing else to buy.

Then the plan. Three businesses. Bakkt Markets is institutional trading rails, with transacting volume the company expects to grow from $241 million last quarter to around $2.5 billion by year-end. Bakkt Agent is programmable payments for AI agents, launching in Q3. An AI agent can't pull out a credit card. It needs licensed, programmable money rails, and very few companies can legally provide them. Bakkt Global is a capital-light international arm. The Japan position — $11.5M into Bitcoin Japan Corporation (TSE: 8105, formerly Marusho Hotta) — is marked at $31.7M as of March 31, a 2.8x return that includes $14.9M of cash already received from Rizap share sales. The India position is a $9.5M warrant subscription in Transchem (BSE: 500422), an Indian brokerage that will offer regulated access to offshore and tokenised investment products. The warrants are subscribed but not yet exercised — conversion is pending regulatory and shareholder approval — with an illustrative quarter-end mark of $44.3M (4.7x). Combined Bakkt Global asset value: $76M. Strip that out of the $445M market cap along with $82.6M of cash and you are left with an enterprise value of roughly $286M for the entire operating business — the licenses, the rails, Bakkt Markets, and a yet-to-launch Agent product.

Then there's the board. Lyn Alden (author of Broken Money) is on it - one of the most respected voices on how money actually works. She describes the financial system that's run since the 1970s as "antiquated monetary technology." She has now agreed to help govern a company building the replacement for it. Sitting next to her: Mike Alfred, who also sits on the $IREN board and recently bought 585,000 shares of Bakkt in the open market, and Richard Galvin, who runs an institutional digital-asset firm.

So what could it be worth?

Sum-of-the-parts, today. On 44.6M shares: cash is $1.85/share, Bakkt Global is $1.70/share at current levels (Japan $0.71 + India $0.99). That is $3.55/share of net assets before you value the operating business. Put the licensed, NYSE-listed payments rail at a 50% discount to what Stripe paid for Bridge and Mastercard for BVNK — call it $500-900M — and the operating business is worth $11 to $20 per share. SOTP fair value today: $15 to $25. The stock is trading at $10 following the rally this week.

From there, two paths to the bull case, and you don't need both. Path one: an acquirer decides buying the only public-market licensed rail beats building one, and pays a strategic premium. Path two — the one I think is underappreciated — the Clarity Act passes, the sector re-rates, and Bakkt trades like the public pure-play it is. If Markets and Agent together drive $200–300M of real (non-pass-through) revenue by year three, and the sector trades at 15–20x revenue — still a discount to where Circle trades today — that's a $3–6B company, or $60 to $115 per share. If multiples expand the way they did in 2021 and Bakkt commands a scarcity premium as the only public option, you can defend higher. Circle, the only public stablecoin pure-play, is worth $28 billion today.

One more piece I’m following with interest. Bakkt has changed its investment policy to allow it to hold Bitcoin on the balance sheet. Bakkt would be a Bitcoin treasury sitting on top of a real, licensed, operating business. The market currently prices that option at nothing.

The Pharaoh's view: the market is paying $10 for the ghost. The company inside is worth far more, and eventually the market will figure it out.

🔔 A few key updates @Bakkt: Momentum is accelerating 🚀

1. Bakkt Markets: projecting >$2.5B YE’26 volume, driven by the massive stablecoin on/off-ramp opportunity. Pipeline conversion is in full swing now that the tech + talent are fully in-house.

2. Leadership boost: thrilled to welcome Daniel Ishag as Chief Commercial Officer. Our go-to-market engine just got materially stronger; execution against the sales pipeline is everything.

3. Unified platform unlocked: DTR’s stack is now fully inside Bakkt. One platform = better economics, stronger compliance/control, and meaningful operating leverage at scale.

4. Bakkt Agent: Significant partnerships pipeline. We hope to make announcements when ready. As distribution is secured, we’ll provide clearer visibility into MAUs and monetization.

5. Bakkt Global: India regulatory approval expected, with meaningful near-term earnings impact. @bitcoincojp’s June AGM will be a key milestone as the company unveils its roadmap.

6. Cost discipline: Legacy systems and outdated overhead are being dismantled rapidly, driving a cleaner, more efficient operating model.

We’re building next-generation financial infrastructure at the intersection of stablecoins, AI agents, and programmable money.

Nothing @Bakkt is incremental.

As I said yesterday: “We believe we are positioning $BAKKT to lead one of the most important financial infrastructure shifts of our generation.”

THE ETHEREUM FRACTAL IS UNFOLDING.

$ETH is mirroring $BTC's 2018–2021 playbook.

Same pain. Same recovery. Same setup.

Next phase? A vertical +1110% move.

Miss it, and you’ll relive the regret of sitting out the last cycle.

.@GundersonLaw represented Electric Capital as a lead investor in the $425 million private investment in public equity (PIPE) transaction supporting 180 Life Sciences' pioneering Ethereum reserve. Congratulations!

https://t.co/aShmTxkt1R

#EthereumReserve#Blockchain

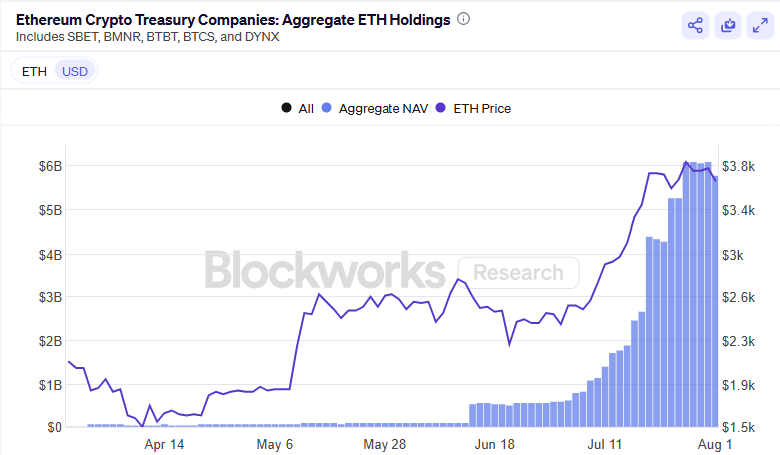

Everyone is looking at the first-order effects of spot buys for these DATS but absolutely NO ONE is ready for when these companies start to put this money to work on chain.

$6B+ injected directly into ETH Defi? LFG.

h/t @blockworksres

I have never felt so energized and optimistic about the future of Ethereum. We are about to land the most profound paradigm shift in recorded history: the societal transition to decentralized trust. Ethereum is no longer an experiment; it is the new foundation for digital trust. We are just getting started.

NEW: SharpLink has acquired 10,000 $ETH directly from the Ethereum Foundation

The purchase closed at ~$25.7M, with $ETH acquired at an average price of ~$2,572

Ethereum is entering a new era of institutional relevance, and we’re proud to support its long-term strength and mission

The asset is $ETH, the ticker is $SBET

This is a very strong piece of work in so many ways. Well articulated thesis. Good level of detail on Ethereum. And clear implications drawn re ETH as a global reserve currency and fuel that powers the future increasingly decentralized economy.

There is much to appreciate in this analysis and narrative and I think the level of detail regarding how Ethereum works was just right. Probably everyone who reads this work will learn something and be stoked by the thesis.

The thesis that "while BTC should be valued as Gold 2.0, ETH should be valued on the scale of the emergent decentralized global economy," was an early metaphor in the space, and it remains a very powerful one. Likening ETH to digital oil or energy that powers the future economy is a good proxy for this metaphor.

But this top tier thought piece has one major structural flaw -- a pretty deep structural flaw: it is not bullish enough.

It is not bullish enough on the profound societal paradigm shift Ethereum will drive and embody. But this is understandable, as none of us at this point can fathom how fast, creative and expansive the hybrid human-machine intelligence society will grow. Many of us are convinced that it will grow largely on decentralized rails. So it is not a great leap to suggest that the value resident on and flowing through Ethereum, which will constitute a large portion of Web3 -- the re-decentralized -- will be orders of magnitude larger that today's global GDP. Just look at how the energy, chips and data center spend is growing exponentially and how AI is accelerating everything.

There are various components that could contribute to the valuation of ETH. I think the two most important components are (a) the world computer / digital oil / energy model elucidated in the report and (b) what I like to call the trust commodity model. If trust is considered a new kind of virtual commodity, then ETH would be the highest grade or gold standard of trust on the planet, largely due to how decentralized Ethereum is. Both of these models will lead to a giant monetary premium for ETH. I have sketched the trust commodity idea here:

https://t.co/yTsdmxdIaK