Leopold Aschenbrenner filed his Q1 2026 13F. It's one of the most aggressive thesis pivots in AI investing this year, and almost everyone is reading it wrong.

Situational Awareness LP. $13.68B in 13F-reportable notional, up from $5.52B at year-end.

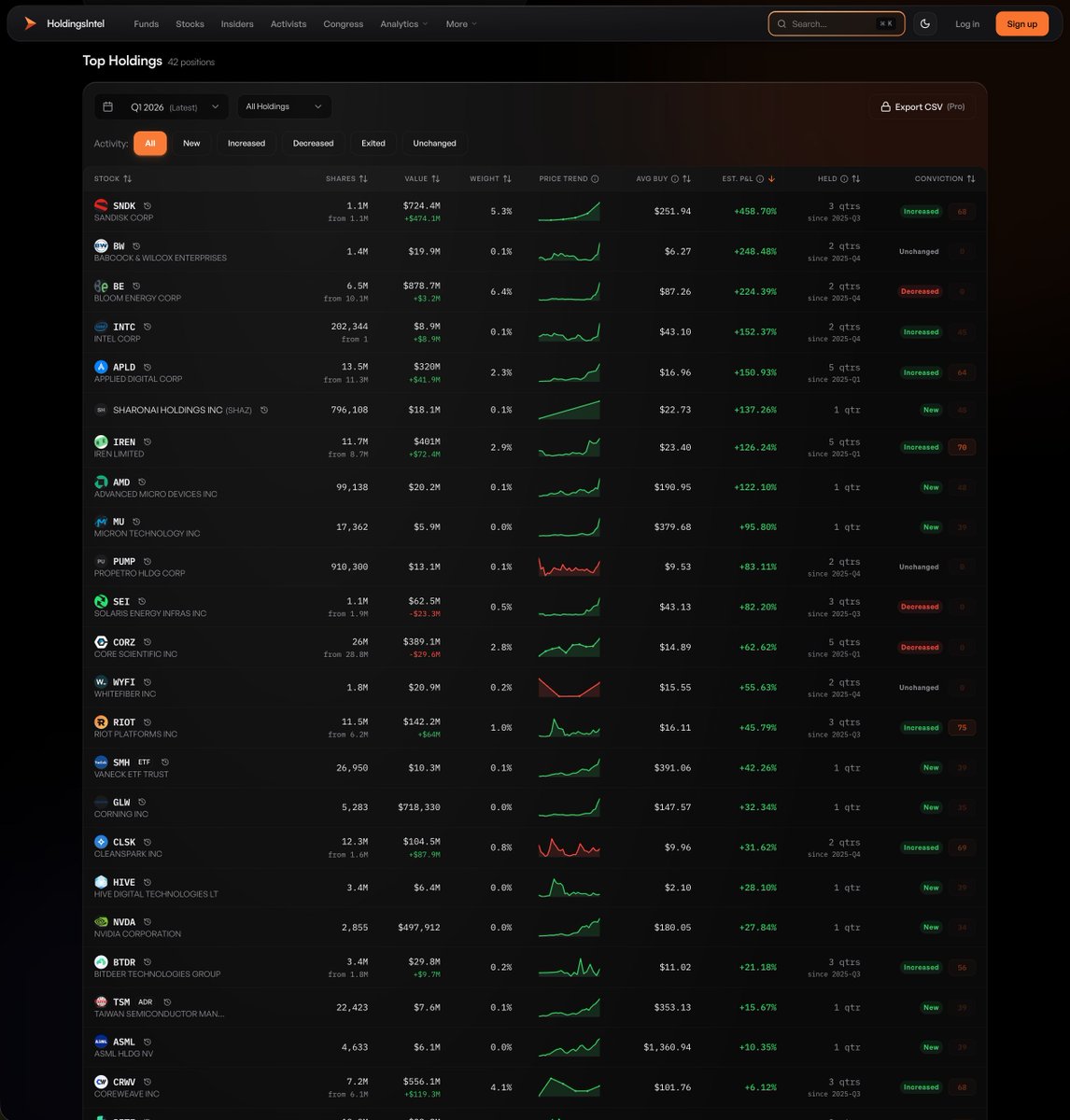

The equity book alone is $3.86B across 26 positions, up 15x from $255M four quarters ago. But the equity book isn't the story.

The story is the $8.46B in puts.

Three buckets:

LONG EQUITY (top 8 of 26, $3.7B of the $3.86B):

• $BE (Bloom Energy) +$879M, 6.5M shares

• $SNDK (SanDisk) +$724M, 1.14M shares. +$474M added. Conviction 68.

• $CRWV (CoreWeave) +$556M. +$119M added. Conviction 68.

• $IREN +$401M. +34% shares, +$72M. Conviction 70.

• $CORZ (Core Scientific) +$389M

• $APLD (Applied Digital) +$320M. +19% shares, +$42M

• $RIOT (Riot Platforms) +$142M. +86% shares, +$64M. Conviction 75.

• $CLSK (CleanSpark) +$104M. +648% shares. Conviction 69.

Theme: power infrastructure + bitcoin miners pivoting to AI hosting + NAND memory.

LONG CALLS ($1.36B notional, leveraged bullish):

• $MU +$422M notional, 1.25M shares

• $SNDK +$389M notional, 611,900 shares (stacked on $724M equity)

• $TSM +$355M notional, 1.05M shares

• $CRWV +$141M notional, 1.81M shares (stacked on $556M equity)

• $BE +$55M notional, 408,500 shares (stacked on $879M equity)

He's leveraging into memory and selective foundry.

LONG PUTS ($8.46B notional, bearish):

• $SMH (semis ETF) +$2.04B notional, 5.33M shares

• $NVDA +$1.57B, 8.99M shares

• $ORCL +$1.07B, 7.29M shares

• $AVGO +$1.01B, 3.25M shares

• $AMD +$969M, 4.76M shares

• $MU +$584M (net of calls: $162M net short)

• $TSM +$535M (net of calls: $180M net short)

• $ASML +$494M

• $INTC +$159M

• $GLW +$21M

• $INFY +$7M

He is short the AI chip complex. $NVDA, $AVGO, $AMD, $ASML, $INTC outright. $MU and $TSM net short via call/put structures. $ORCL short to express enterprise AI saturation.

EXITS ($1.04B liquidated, 8 positions):

• $LITE (Lumentum) +$479M, was 12.2% of equity book

• $CIFR (Cipher Mining) +$154M, was 3.9%

• $EQT +$133M, was 3.4%

• $COHR (Coherent) +$89M, was 2.3%

• $TSEM (Tower Semi) +$85M, was 2.2%

• $KRC (Kilroy Realty) +$50M

• $HUT (Hut 8) +$40M

• $LBRT (Liberty Energy) +$10M

Sold optical/photonics, datacenter REITs, nat gas, one bitcoin miner.

THE MOST MISREAD DETAIL:

Tiny new equity positions in $NVDA ($498K), $AMD ($20M), $TSM ($8M), $ASML ($6M), $MU ($6M).

These are small long stubs sitting underneath multi-hundred-million-dollar put positions. $NVDA equity $498K + put notional $1.57B. $AMD equity $20M + put notional $969M.

He's not building exposure. He's structuring the short.

THE THESIS:

He sold the consensus AI infra trade. Optical networking, photonics, datacenter REITs, traditional AI power names.

He bought bitcoin miners pivoting to AI hosting. Companies that already have grid contracts, substations, transformers, cooling. Stranded power becoming inference power. Years ahead of greenfield datacenter builds.

He doubled down on NAND memory. $SNDK is now his #2 equity position, with another $389M in calls on top.

And he stacked $8.46B in puts against AI chip incumbents and the enterprise AI cloud trade.

The bet:

Power and memory go up. AI chip incumbents and Oracle-style enterprise AI go down or stay flat.

He's not waiting for confirmation. He's positioned.

two problems with this.

1) "$225M → $5.5B" is mostly inflows, not returns. his AUM grew because new investors handed him money every quarter:

Q4 2024: $254M

Q1 2025: $1.0B

Q2 2025: $2.1B

Q3 2025: $4.1B

Q4 2025: $5.5B

a manager doesn't 22x stocks. he 22x'd his subscription book.

2) SNDK/BE/LITE % are the stocks' 12-month prints. his actual cost-basis P&L:

$SNDK +210% (not +3,200%)

$BE +55% (not +1,500%)

$LITE +123% (not +1,400%)

solid. not godly.

his Q1 13F is due Friday. expect to see trims on the names he's being credited for, and a sizable hedge book.

y'all reading the wrong column.

those % are the STOCKS' returns. not his.

his actual cost-basis P&L:

$BE +55% (not +1,422%)

$LITE +123% (not +1,331%)

$SNDK +210% (not +3,130%)

$IREN +92% (not +583%)

$APLD +61% (not +629%)

$INTC calls +35% (not +365%)

$CORZ +9% (not +135%)

$CIFR -12% (not +449%)

$CRWV calls -23% (not +166%)

two losers in the book. solid, not legendary.

his Q1 13F is due Thursday 👀

y'all reading the wrong column.

those % are the STOCKS' returns. not his.

his actual cost-basis P&L:

$BE +55% (not +1,422%)

$LITE +123% (not +1,331%)

$SNDK +210% (not +3,130%)

$IREN +92% (not +583%)

$APLD +61% (not +629%)

$INTC calls +35% (not +365%)

$CORZ +9% (not +135%)

$CIFR -12% (not +449%)

$CRWV calls -23% (not +166%)

two losers in the book. solid. not legendary.

his next 13F drops next week 👀

One last quirk almost nobody talks about.

Anthropic isn't controlled by its biggest shareholders. It's governed by the Long-Term Benefit Trust. Five financially disinterested trustees hold special Class T stock that lets them elect a majority of the board. Buying equity doesn't buy control.

So if you want Anthropic exposure today, your only liquid options are AMZN and $GOOGL. Same shape as OpenAI exposure via Microsoft ( $MSFT ).

Hedge funds figured this out a year ago. They've been increasing both positions every quarterly 13F since.

The "private AI you can't access" story is mostly marketing.

Anthropic just hit a $380B valuation. You can't buy the stock.

But two public companies dominate the cap table:

• Amazon ($AMZN): $8B in. Just committed up to $25B more.

• Google ($GOOGL): $3B+ for a ~14% stake. Just committed up to $40B more.

Fortune reported last month that half of last quarter's blowout AI profits at $AMZN and $GOOGL came from Anthropic paper gains. Not from their actual businesses.

Then there's the FTX ghost.

Sam Bankman-Fried's Alameda paid $500M for an 8% stake in 2021. When FTX collapsed, the bankruptcy estate sold it in 2024 for $1.3B. Buyers: Mubadala (UAE), Jane Street, Fidelity, Ford Foundation.

At today's $380B valuation, that 8% would be worth ~$30B.

Possibly the worst "sold too early" trade in history.

🚨 BREAKING 🚨

Bill Ackman, the activist who bets his fund on fewer than 10 names, just filed showing he owns nearly half of Howard Hughes Holdings - 46.7% are his - $1,730,000,000 at today's $61.97

Shareholders blocked his merger proposal here in 2021. He bought 27.9 million more shares instead.

At 46.7%, he's 3.3% from a controlling majority.

Watch the next 13F Pershing Square filing on $HHH.

Watch the next Form 4.

If anyone at OKLO ever buys a share at any price, that's news.

Until then, the people who built the company are voting with their accounts.

The cap table is the thesis. Everything else is noise.

$OKLO founder has been quietly leaving the building.Jacob DeWitte's personal stake: 18.2% → 16.2% → 12.2% in twelve months.

4.2 million shares of his own company, gone.The retail crowd was buying at $60. He was on the other side.

And he's not alone.

Past twelve months at $OKLO :

35 insider sales. 0 insider buys. $98 million dumped.

Officers, directors. Seven different people. None of them buying a single share, ever, at any price.

The cap table has been a one-way door.

@readswithravi Poor Charlie's Almanack.

The single most useful question I ever learned: not "how do I succeed?" but "what would guarantee failure?" Then avoid those things.

Read it twice. Everyone should.

When 9 frameworks converge, pay attention.

But I want YOUR take.

Which of these do you own or plan to buy?

🔄 $CWCO or $ERO (the consensus picks)

❤️ $AEHR or $MRCY (the contrarian picks)

💬 None - reply with your own pick I missed

Not financial advice. But convergence is a signal.

I ran a 9-expert simulated debate across 5 rounds to find

the most undervalued stocks in the fastest-growing sectors using

Value purist vs mining specialist vs EM contrarian vs

behavioral economist vs 5 others.

Each expert started with a different #1 pick.

Then something I didn't expect happened.

What do you think they converged on? 🧵