A fixed-strategy bot is a dead bot walking. Markets drift. Volumes shift. Volatility regimes rotate. But if you change parameters every week, you’re curve-fitting in real time.

The solution is Bayesian updating. It’s a mathematical way of saying: I have a prior belief. I see new data. I update my belief but only in proportion to how much evidence I’ve seen.

Here’s how a model does it:

· Prior: The strategy’s long-term EV from the backtest period.

· Evidence: Each new trade’s outcome.

· Posterior: A weighted average, where the prior gets less weight as the sample grows.

After 5 new trades, the prior dominates. The model doesn’t flinch. After 50, the live data has real influence. After 100, if the live EV is significantly below the prior, a “Signal Freshness” yellow flag triggers, the model doesn’t stop trading, but reduces exposure until the evidence stabilises.

Bayesian thinking means never saying “the edge is dead” from a handful of losses, and never ignoring a real structural shift. The model walks that line every day.

I’ve put together a short PDF on Bayesian reasoning for traders no math degree required. Comment ‘BAYES’ and I’ll DM it.

Even Jim Simons' win rate was only around 51%.

With a 42.54% win rate, I lose more than half of my trades, so five losses in a row is just a normal statistical cluster, not a signal that something is wrong.

I went 100% algorithmic for exactly this reason: the 6th trade is identical to the 1st trade.

The system doesn't know it lost.

Only beginners concern themselves with win rate.

The best traders I've ever met, managing tens of millions in AUM, have win rates of only 30–40%.

The best system is the one with the highest Sharpe ratio, not the highest win rate.

If someone focuses on a trader's win rate and points to a few losing trades as evidence that the strategy doesn't work, I would consider that person a beginner by default.

"Volatility Forecasting and Return Prediction under Market Regimes: Evidence from High-Frequency Chinese Equity Data", https://t.co/dyFknoA4QI

Several thoughts though, as the idea seems interesting, but the execution is not at all 👇🧵

A software engineer from Zurich built a Polymarket startup and released it on GitHub for free…

He created a bot that can automatically detect the real strategy of any existing Polymarket trader.

Here’s how it works and how you can use it for your trading:

Imagine you found a new category to trade, for example, movie markets and one trader who closes every his trade in solid profit.

But you dont want to just copy trade him blindly, you want to understand how this trader thinks, which strategy he uses and how you can adapt it to your own trading.

So you add this trader to this Polybot and it starts collecting all available information and statistics about him: which markets he enters, when he enters, how much he trades, how long before the market ends he enters and when he usually closes his positions - everything to fully understand his trading behavior.

After that, this bot uses its own research tools to look for repeated patterns.

For example, this bot notices that only in movie markets, this trader buys the most likely outcome every time right at the beginning of the market.

To check whether it works in practice, the bot runs this strategy in paper trading mode (on real historical markets from its own huge dataset).

And lets say, it finds that YES, all movie markets are less volatile and the early winner often turns out to be the correct outcome.

Finally, this bot generates a detailed report with its research results and real market examples.

This way you can reverse engineer hundreds of different wallets, find strategies that actually work and are used by real traders, and use them for your own trading.

GitHub: https://t.co/SzdjHtBqB1

THIS TRADER TRAINED HIS OBSIDIAN VAULT ON HUNDREDS OF CHART PATTERNS AND NOW IT THINKS WITH HIM

every setup he ever studied is in there

> linked to the outcome

> linked to the context

> linked to what he was thinking at the time

he types one command

> Claude Code finds the relevant sources, runs analysis through NotebookLM, saves everything structured

the vault doesn't just store information anymore

it connects it

most traders are still screenshotting charts into a Discord and forgetting them in 48 hours

article below

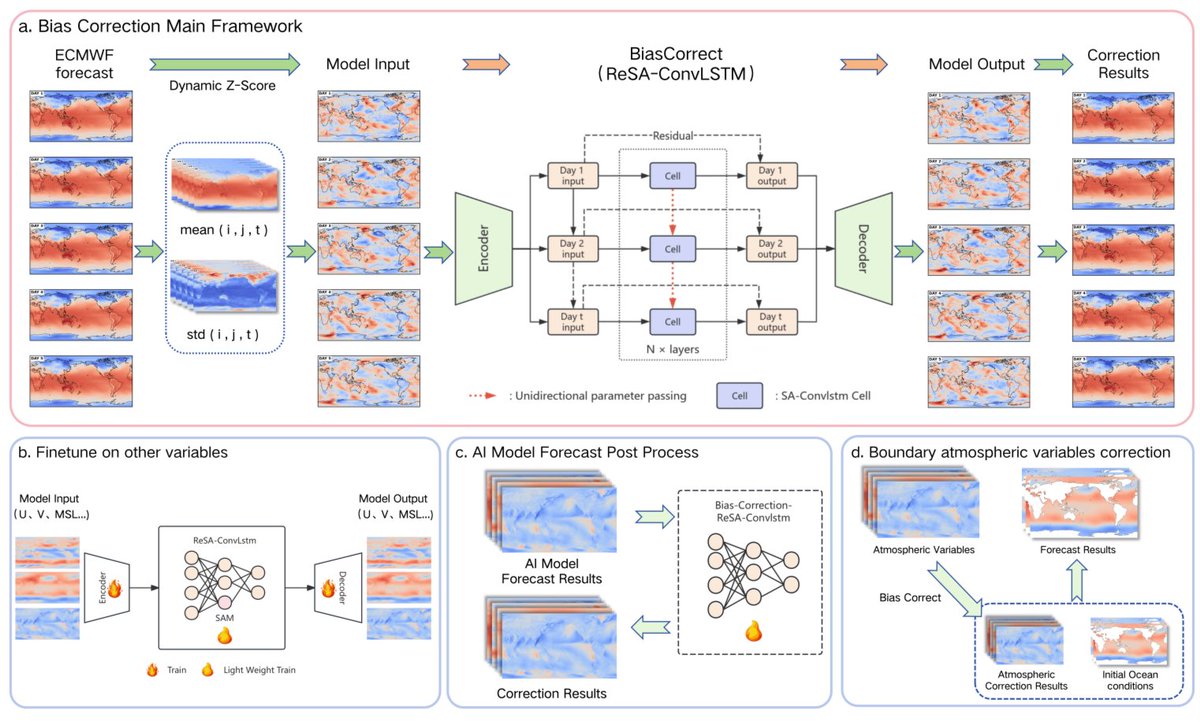

Advanced Bias Correction for Polymarket Weather Trading Bots: ConvLSTM + Self-Attention + Dynamic Normalization

If you're building a serious trading bot for temperature markets, at some point simple bias correction stops being enough

I found one of the most interesting papers from 2025 that breaks down how to build a truly powerful AI bias correction system for ECMWF

Paper: "How to systematically develop an effective AI-based bias correction model" (ReSA-ConvLSTM, Zhou et al., arXiv, April 2025)

Link: https://t.co/QtSh3ehnrK

> What the Authors Built

They created a full framework called ReSA-ConvLSTM, which delivers up to 20% RMSE reduction on the 1–7 day horizon compared to raw ECMWF output.

> Architecture Breakdown

1. ConvLSTM as the main backbone

Regular convolutional networks (like U-Net) are good with images but weak at understanding temporal dynamics

ConvLSTM is a hybrid of Conv + LSTM. It analyzes both spatial features (mountains, seas, cities) and temporal evolution (how temperature changed over the past hours/days)

This makes it much stronger for meteorological data

2. Dynamic grid-wise normalization instead of standard Z-score

Standard normalization uses one global mean for the whole world - which works poorly for temperature

Here, each grid point has its own climatological mean and variance

This removes the huge difference between tropical and polar regions and significantly improves training stability

3. Strict temporal causality

The model only looks at past states and doesn’t “peek” into future forecast days. Critical for real-time trading systems.

4. Residual connections + Self-Attention

Residual connections help the network go deeper without losing information

Self-Attention allows the model to automatically focus on important areas (coastal zones, mountains, etc.)

> Results

• Raw ECMWF: RMSE 1.2°C on day 1 → 2.1°C on day 7

• ReSA-ConvLSTM: below 1.0°C on days 1–3, below 1.8°C on days 4–7

The model also transfers well to wind and pressure variables

> How to Implement It Yourself

There’s no official ReSA-ConvLSTM repo yet, but you can build a very close version using:

ndrplz/ConvLSTM_pytorch - one of the best and cleanest ConvLSTM implementations

Repo: https://t.co/l1YlDtdLZr

tsugumi-sys/SA-ConvLSTM-Pytorch - ConvLSTM already with Self-Attention

Repo: https://t.co/hsjQDRMsMq

NOAA-EMC/ML4BC - real bias correction project

Repo: https://t.co/q72pj9Z8rR

Take ConvLSTM + Self-Attention as the base → add Residual blocks and dynamic grid-wise normalization following the paper → train on ERA5 + ECMWF data

Hybrid architectures like ConvLSTM + Attention + Residual are currently among the strongest directions in weather bias correction

Especially if you want to consistently win on tight 1°C bins on Polymarket

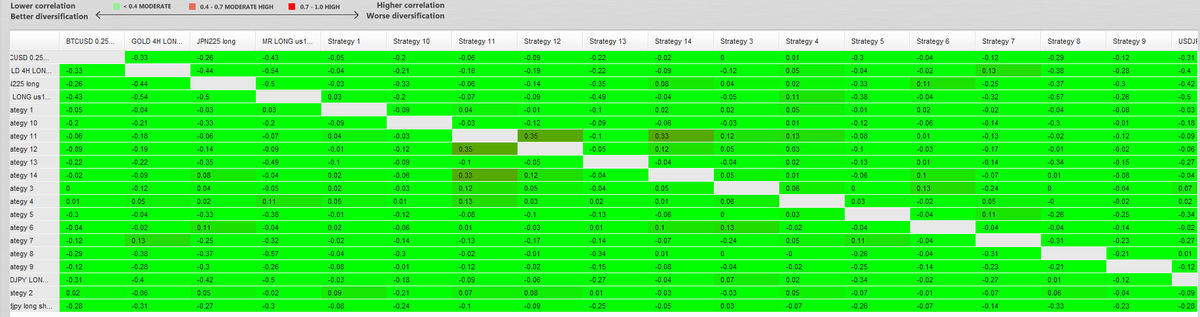

Big collaboration announcement.

@TheWolf534 x @ZorveX_Trader

We combined 21 strategies into one professional portfolio:

PGS V14 X MSE vPRO

Built to create a highly diversified, low-correlation trading portfolio designed for prop firm scaling.

The goal is simple:

reduce dependency on one strategy, smooth the equity curve, and increase long-term consistency.

This is not just one system.

This is a full portfolio approach.

More details coming soon.

If a prop firm has paid out $150 Million to traders

Their net income is likely $70M – $100M

• 80-95% of traders fail challenges → firm keeps almost all entry fees

• Real example: FTMO paid ~$176M with $91M net income

Payouts = marketing.

Real money is in the failed challenges 🔥

Bonding Strategy: How to Earn 4–6% Per Day on Polymarket with Almost Zero Risk (FULL GUIDE)

Every day on Polymarket there are many markets where the outcome is already almost obvious to all participants

Yet the price often stalls at 97–99 cents even 24 hours before resolution

Bonding Strategy takes advantage of exactly this market feature

> How Bonding Works

You buy contracts at 97–99.5 cents and hold them until final resolution

The 1–3% difference remains because many traders don’t want to wait until the last hours and exit early

> How to Quickly Find and Trade These Markets

The most convenient way is through the Parity Terminal:

• Select the “Markets” tab and set your filters

• Probability: 95–99

• Spread: ≤ 0.05

• Liquidity: ≥ $10,000

• Time to Resolution: ≤ 1d

Bonding doesn’t require complex analysis or forecasts. It’s all about discipline and using market mechanics

My filters are listed below 👇

you guys asked , we delivered! IBIT data is officially up!

https://t.co/FyBNtbaGb3 ( No Paywall OR Sign Up Required)

what does it show :

-options chain , greeks , vol , 3d surfaces , cross mrkt analysis with derive & deribit & options levels on a trading view chart! ( this is my favourite feature btw)

video below illustrating this.

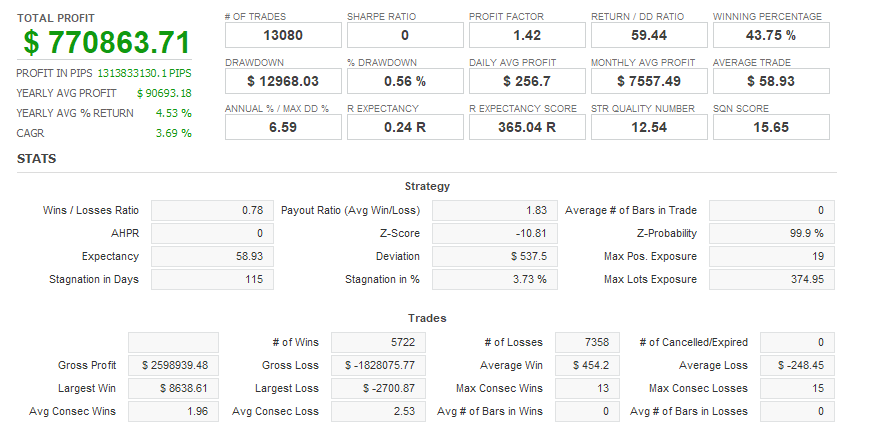

Most traders think adding rules makes a strategy better.

I built a 2-rule NQ strategy in BreakoutOS and compared it against 1,000 alternative NQ algo strategies. It came out in the 97th percentile.

Here's what complexity actually costs:

Every parameter you add is a degree of freedom. Every degree of freedom is another way to overfit. Each one makes your backtest look better and your live results worse.

This strategy has none of that.

Entry: Previous day's low plus 0.8x ATR(40). Cross it long on a stop order. Exit at the end of day. Nothing else.

The structural audit (I used the Backtest Auditor module in BreakoutOS) checks how much data manipulation would have been required to produce those backtest results by accident. Here, the score was low. Because there's nothing to manipulate. The edge comes mostly from NQ's built-in directional tendency, which is a real and persistent market bias, not something you engineered in.

Regime breakdown: the strategy excels in volatile uptrends, normal uptrends, volatile downtrends, and slightly in volatile ranging markets. It also outperforms the 1,000 comparison strategies specifically in quiet uptrends. Weaknesses in quiet ranging, normal ranging, quiet downtrend, normal downtrend. Exactly what you'd expect from a long-biased breakout.

Market readiness for current conditions: 100%.

Historical analogs project 68% win rate, 4.3 profit factor, almost $500 average trade. One snapshot from a similar past market: 83% win rate.

Two rules. According to the Backtest Auditor (in BreakoutOS) - 97th percentile - meaning, beating 97% of other strategies. Ready to launch.

What's the simplest strategy you've ever actually traded live?