#S32 Hermosa (4% Zn, 4% Pb, 80g/t Ag) has an NSR around US$370/t of ore here ($100 Zn, $70 Pb, $200 Ag). Costs ~US$100/t ore.. margin US$270/t ore on 4.3mtpa is ~US$1.2bn pa.

What does a US based "critical minerals" project that has been gold plated and has decades of life trade at under Trumps America? 8x EBITDA? So it's a US$10bn project? Even after its big run #S32 is trading <US$12bn EV and this is one fraction of the company..

What a deal by MP Materials:

- 10-year offtake agreement with a massive $110/kg NdPr price floor

- $400M equity injection from the DoD, making it the largest shareholder

- $1B+ in committed financing from JPMorgan & Goldman Sachs for a new “10X” magnet plant targeting 10,000 mtpa of NdFeB magnets

This is a game-changer for Mountain Pass and MP Materials $MP

Zinc today is $1.40/lb, copper $4.35/lb. Divide one by the other (Cu/Zn) and you get 3.1x

But from a miners POV.. a smelter typically pays ~83% of contained Zn in conc and charges ~$0.25/lb TC ($250/t on 50% Zn conc)… so Zinc today for the miner is in fact ~$0.9/lb

Copper gets paid at ~96% and ~$0.17/lb TCRC ($60/t on 25% conc TC and 6c/lb RC).. so for the miner ~$4.0/lb..

So 3.1x becomes 4.4x

then factor in typically lower recoveries and you soon realise why insitu CuEq is proper bs. I don’t expect 95% to understand this but for the others 🫡

Congratulations to my good friend @eadatt after years of holding $YRL on their discovery made today.

As it’s actually a legitimate discovery, and not a redrill/nearology ‘discovery’.

Imagine having a drill hole ‘rained out’ though…that’s shit luck.

And yes, I bought it.

@winston12358@AvidCommentator Isn't the issue though that currently, PAYG earners can deduct interest from their salary income. In your example it's a company with deductible expenses. If they can't deduct interest as an expense then it's unfair vs any other company claiming interest expenses?

@AvidCommentator Interested in your thoughts on how this would work in practice. If negative gearing was revoked, isn't this just another case of populist policy tweaks? Impact will be middle Australians taking a massive tax hit yet ...

AMP’s Oliver weighs into Qatar/Qantas fracas

‘Blocking Qatar’s request for 28 extra flights to Australia is hard to fathom in the context of the need to lower prices and boost productivity.’

https://t.co/weLeC8xupO

The panic slowly setting in for the Aussie energy operator with their 6mth update.. worth reading just the exec summary #faderhetransition

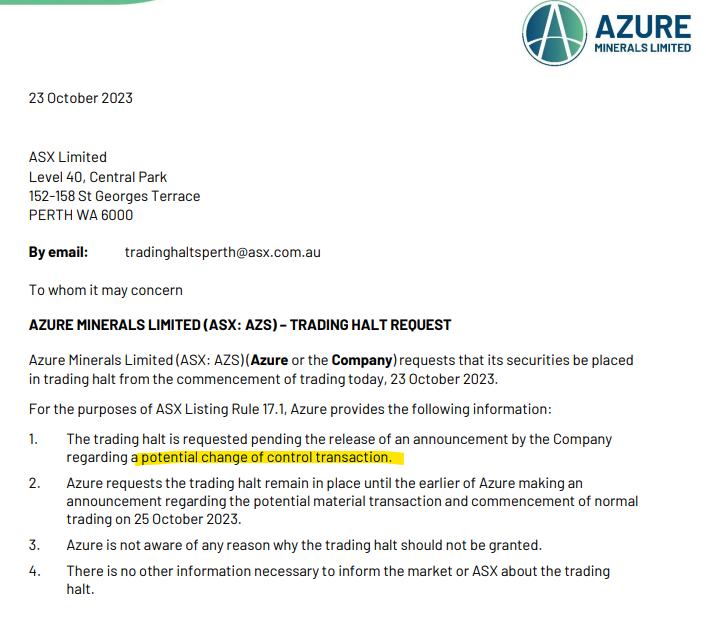

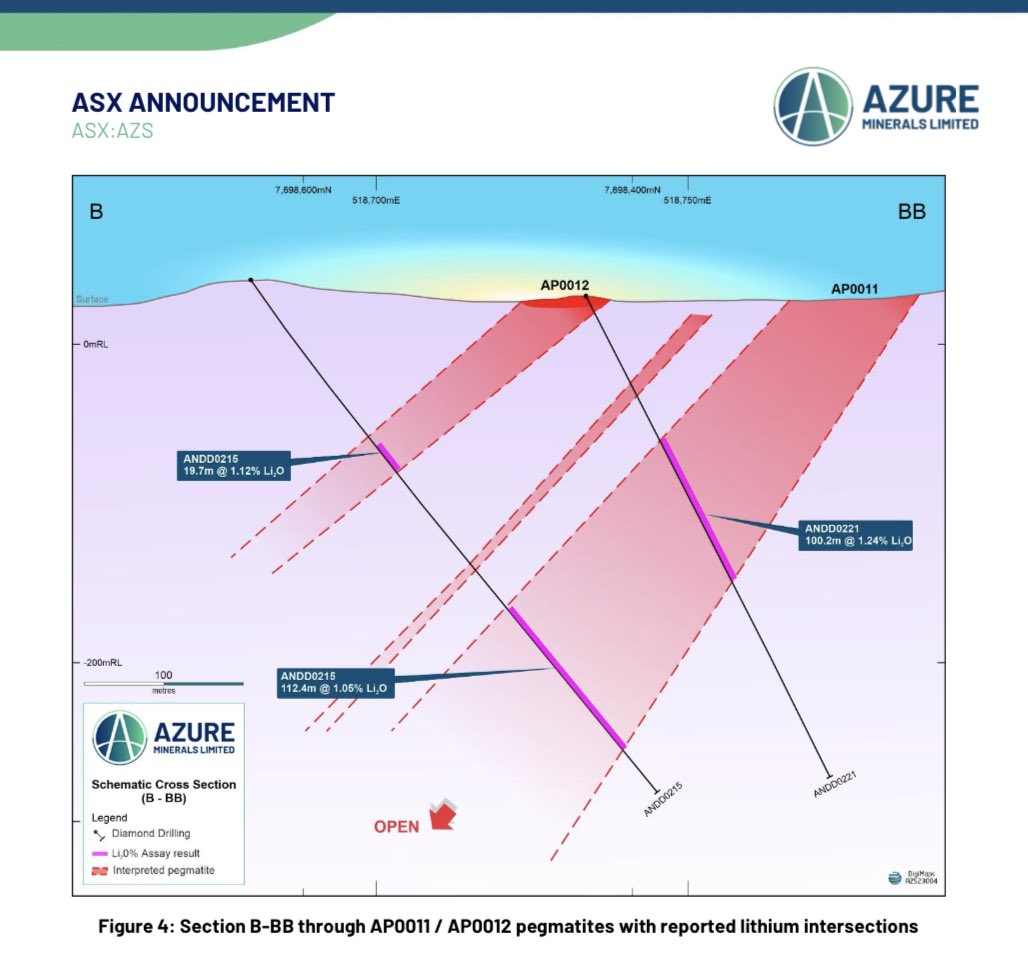

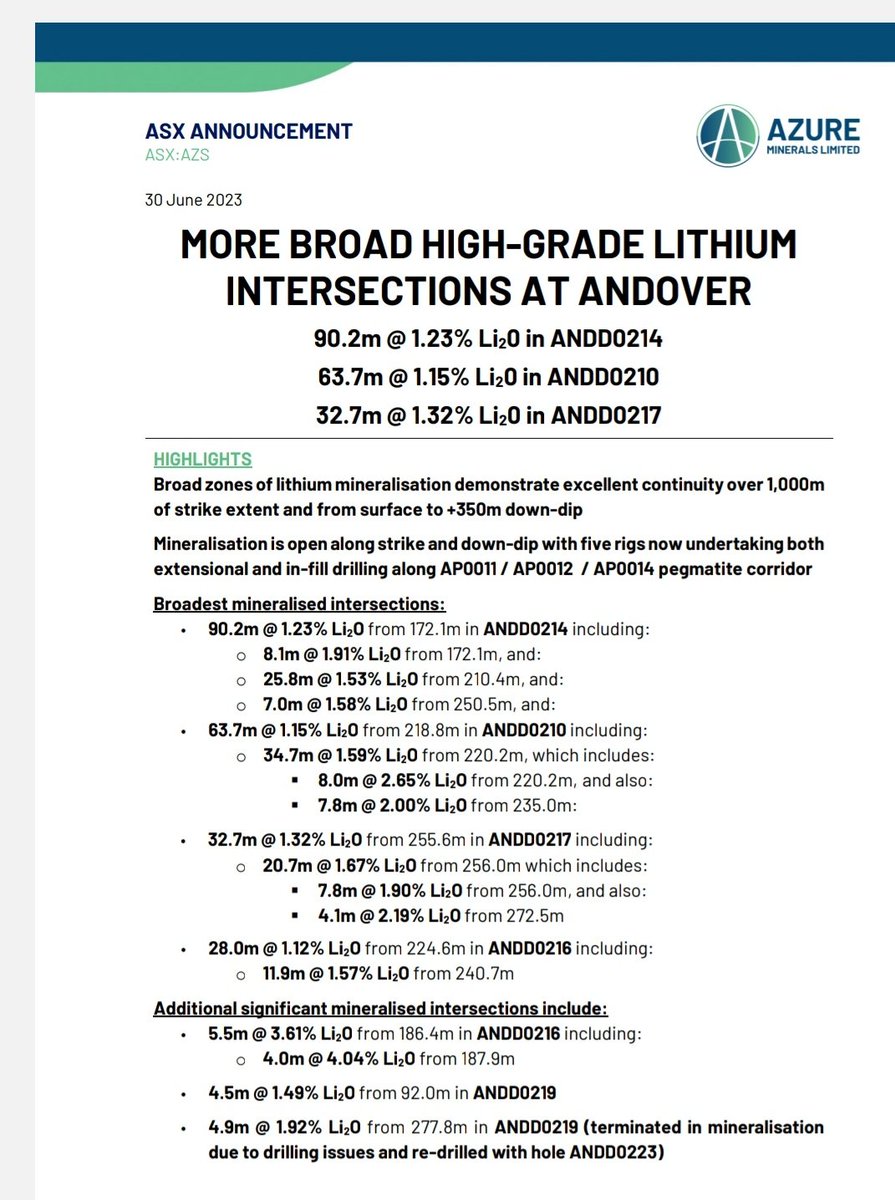

$AZS News

90.2m @ 1.23% Li201✅

63.7m @ 1.15% Li20✅

32.7m @ 1.32% Li20✅

True thicknesses of the pegmatites are estimated to be > than 90% of the intersected widths✅

If thicknesses average 50m with down dip 350m extent, I think we are looking at massive resource

#Lithium

More Mammoth Intersections for $PMT who’ve now returned -

127.7 m at 1.78% Li2O

95.3 m at 1.62% Li2O

This is looking like it exceed grade of Pilgangoora & maybe even tonnage..

A Monano Comparison is more like if they keep getting hits like this