@InTheAssembly the biggest vix call firday is 60000 contracts of 35 on 2026-7-22 ,this is not huge, young man. if you trade based on this kind of information, you can barely succeed in trading.

MIT, Yale, Oxford, Columbia uploaded their entire quant trading courses for free.

The same lectures their students pay $200K for.

40 hours of pure math and systematic strategies.

Block 2-3 hours this weekend and actually start.

so let me get this right:

Oracle says Openai committed $300B for cloud compute → oracle stock jumps 36% (best day since 1992)

Oracle runs on Nvidia GPUs → has to buy billions in chips from Nvidia

Nvidia just announced they're investing $100B into openai

Openai uses that money to... pay oracle... who pays Nvidia... who invests in Openai

Traders in the US bond market are drastically underestimating what is about to take place in macro volatility

This next move in interest rates will set the stage for macro flows over the next 2 years and no one in the media is even talking about it

Let's dig in 🧵👇

Elon sells → Vision, not Technology.

Apple sells → Trends, not phones.

Ferrari sells → Status, not cars.

Nike sells → Motivation, not shoes.

Disney sells → Memories, not movies.

Amazon sells → Convenience, not products.

McDonald’s sells → Happiness, not burgers.

Sell the emotion and not the service.

7 Grok prompts to Sell like a PRO���

3/I am going to argue that the US is now in late-stage exorbitant privilege.

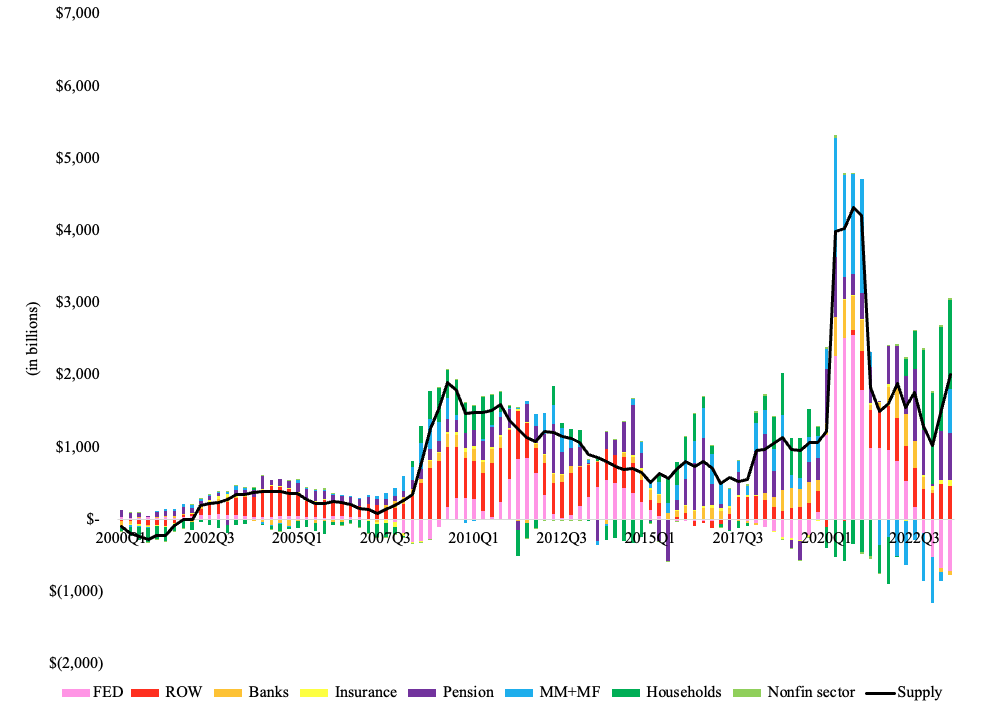

The first signs of cracks in the armor were seen when COVID arrived in US. When the COVID-19 pandemic arrived in the US, the yield on the 10-year increased by 68 bps over the course of eight trading days between March 9 and March 18. Treasury yields increased as stocks were declining in value and as the VIX peaked. There was no textbook flight to safety by foreign investors.

Foreign investors were net sellers of Treasurys in the first quarter of 2020. The rest of the world sold more than $ 284 billion in Treasurys in the first quarter of 2020. Most of the foreign selling was concentrated at longer maturities. In March of 2020, foreign investors sold more than $400 billion of U.S. Treasury Notes and Bonds, followed by sales of $200 billion in April. The Fed purchased more than $1.01 trillion in the first quarter of 2020, absorbing more than twice the Treasury’s total issuance of $ 385 billion. Put differently, the private sector sold $616 billion in Treasurys in the first quarter of 2020. (below plots of 4-quarter moving average of net purchases of Treasurys at annual rates.)

That’s some evidence from quantities about the reduced appetite for Treasurys abroad.

Quickest explanation of a basis trade and how it blows up.

What is the Basis Trade?

It's an arbitrage trade aiming to profit from the price difference between a bond and its futures contract.

"Basis" means "a spread".

For instance, if a futures is trading at a higher price ($99) than a cash bond ($98.50), the trade is:

• Short the Treasury futures at $99

• Buy a Treasury bond at $98.50

Hedge funds need leverage to make meaningful profit, so they borrow money to buy the bond for the trade.

To borrow money in the repo market they pledge the same Treasury bond as collateral for the loan and have to pay a repo rate.

The basis trade locks in a profit once prices converge as the futures approaches expiry.

Why does it blow up?

If Treasury bond prices fall

⬇️

Loan collateral value shrinks

⬇️

Margin call

⬇️

Need to post more collateral or close the trade

Unwinding the trade means the hedge fund needs to sell cash bonds/buy futures back, driving bond prices lower.

This kickstarts a feedback loop.

As bond prices fall further, more funds may be forced to close the trade, if they struggle to post more collateral.

To keep the trade alive, it's important to have access to repo funding, which usually dries up during market stress.

Where can you see this?

For example, you can track the spread between SOFR rate and Fed Funds rate.

• SORF rate represents a secured (collateralized) borrowing (i.e. repo).

• Fed Funds is the unsecured borrowing.

Usually, SOFR < FF rate since collateralized borrowing should be safer and more secure.

However, when the repo market financing tightens, the SORF rate can be higher than Fed Funds.

I.e. it's more expensive to borrow on a collateralized basis than not!

This is what we're seeing now, as shown in the chart below 👇

(This is "SR1J2025-ZQJ2025" on TradingView)