$DNA Q3 2025 earnings: Revenue decline clouds major progress on cash burn and strategic pivot.

The headline numbers for the quarter look weak, with revenue and adjusted EBITDA declining significantly compared to last year. However, this is misleading due to a large, one-time, non-cash revenue item in the prior year. After adjusting for this, the underlying business performance is more stable. The most positive development is a massive reduction in cash burn, which fell to just $12 million for the quarter. The company also reaffirmed its full-year guidance, signaling confidence in a solid fourth quarter. Management continues to emphasize its strategic shift towards becoming a tools and data provider for the AI-driven biology sector.

🐂 𝗧𝗵𝗲 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

Bulls will focus on the dramatic improvement in financial discipline. The quarterly cash burn of only $12 million is a huge step towards sustainability and extends the company's financial runway. Reaffirming full-year guidance despite a soft quarter demonstrates management's confidence in the near-term pipeline. The continued strategic alignment with the AI megatrend, supported by new government contracts and initiatives, reinforces the long-term growth story.

🐻 𝗧𝗵𝗲 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

Bears will point to the weak top-line results. Even after adjusting for the prior-year one-time item, total revenue still declined. Cell Engineering revenue was flat to slightly down, and the Biosecurity segment continues to weaken. The reported Adjusted EBITDA loss widened considerably, and the path to the company's breakeven target by the end of 2026 relies on significant revenue acceleration that has yet to materialize.

⚖️ 𝗧𝗵𝗲 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

Neutral to slightly positive. The poor headline numbers are jarring, but the exceptional progress on cash control is a more significant development for the company's long-term viability. Reaffirming guidance in this environment is a crucial sign of stability. The bull case, centered on a strategic pivot and financial discipline, is more compelling this quarter, but the company must now deliver the revenue growth to prove the new strategy is working.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀, 𝗗𝗿𝗶𝘃𝗲𝗿𝘀, 𝗮𝗻𝗱 𝗖𝗼𝗻𝗰𝗲𝗿𝗻𝘀

🟢 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗗𝗶𝘀𝗰𝗶𝗽𝗹𝗶𝗻𝗲 𝗮𝗻𝗱 𝗖𝗮𝘀𝗵 𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 (𝗜𝗺𝗽𝗿𝗼𝘃𝗲𝗱)

Last quarter, the company announced it had achieved its cost-cutting targets early. This quarter, the results are clear. Quarterly cash burn fell sharply to just $12 million, down from $38 million in Q2. This is a major positive, extending the company's cash runway and giving it more time to execute its strategic pivot without needing to raise capital in the near term.

🟡 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗣𝗶𝘃𝗼𝘁 𝘁𝗼 𝗔𝗜 𝗘𝗻𝗮𝗯𝗹𝗲𝗺𝗲𝗻𝘁 (𝗘𝘃𝗼𝗹𝘃𝗶𝗻𝗴)

The shift from R&D solutions to a tools provider continues. This quarter, the messaging is more tightly focused on AI, with the CEO highlighting how Ginkgo's automation can provide the massive datasets that AI models require. They are now actively marketing their ability to build and install automation systems at customer sites, moving the strategy from a concept to a tangible product offering. However, meaningful revenue from this new business has not yet been reported.

🟢 𝗚𝗼𝘃𝗲𝗿𝗻𝗺𝗲𝗻𝘁 𝗦𝘂𝗽𝗽𝗼𝗿𝘁 𝗮𝘀 𝗮 𝗧𝗮𝗶𝗹𝘄𝗶𝗻𝗱 (𝗠𝗮𝘁𝗲𝗿𝗶𝗮𝗹𝗶𝘇𝗲𝗱)

A driver identified last quarter was potential government investment in automated labs. This theme has materialized. The CEO directly referenced a new AI Action Plan from the White House that calls for investment in this area. More importantly, the company announced a new project agreement with BARDA worth up to $22.2 million, providing concrete validation of this growth driver.

🔴 𝗕𝗶𝗼𝘀𝗲𝗰𝘂𝗿𝗶𝘁𝘆 𝗦𝗲𝗴𝗺𝗲𝗻𝘁 𝗪𝗲𝗮𝗸𝗻𝗲𝘀𝘀 (𝗢𝗻𝗴𝗼𝗶𝗻𝗴 𝗖𝗼𝗻𝗰𝗲𝗿𝗻)

The concern from Q2 about the Biosecurity business persists. Revenue in the segment declined again this quarter, down to $9 million from $14 million a year ago. While the company reaffirmed its full-year guidance of "at least $40 million," this implies a strong Q4 is needed to hit the target, making it a key area to watch.

⚪ 𝗦𝘂𝗯𝗹𝗲𝗮𝘀𝗲 𝗥𝗶𝘀𝗸 (𝗨𝗻-𝘂𝗽𝗱𝗮𝘁𝗲𝗱 𝗖𝗼𝗻𝗰𝗲𝗿𝗻)

Last quarter, management highlighted the $12 million quarterly cash cost of excess real estate as a risk to profitability, given the soft Boston market. This press release did not provide an update on the situation, so it remains an ongoing, unmitigated headwind.

— • — • —

𝗠𝗮𝗶𝗻 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹𝘀

It is critical to note that Q3 2024 financials included a $45 million non-cash release of deferred revenue, which makes direct year-over-year comparisons misleading.

🟢 𝗖𝗮𝘀𝗵 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻: $462 million in cash, cash equivalents, and marketable securities.

🟢 𝗤𝘂𝗮𝗿𝘁𝗲𝗿𝗹𝘆 𝗖𝗮𝘀𝗵 𝗕𝘂𝗿𝗻: Approximately $12 million (down from $474 million at end of Q2), a significant improvement from $38 million in the previous quarter.

🔴 𝗧𝗼𝘁𝗮𝗹 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $39 million. This is down 56% from $89 million in Q3 2024. Excluding the one-time item, revenue decreased 11% YoY.

🔴 𝗖𝗲𝗹𝗹 𝗘𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $29 million. This is down 61% from $75 million in Q3 2024. Excluding the one-time item, revenue decreased slightly from $30 million.

🔴 𝗕𝗶𝗼𝘀𝗲𝗰𝘂𝗿𝗶𝘁𝘆 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $9 million, down 36% from $14 million in Q3 2024.

🔴 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔: A loss of $(56) million. This compares to a loss of $(20) million in Q3 2024. However, the prior year's result benefited from the $45 million non-cash revenue. On a comparable basis, the loss shows underlying improvement.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

Ginkgo reaffirmed all aspects of its full-year 2025 guidance. This implies a stable-to-accelerating fourth quarter.

⚪ 𝗧𝗼𝘁𝗮𝗹 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Reaffirmed at $167 million to $187 million.

⚪ 𝗖𝗲𝗹𝗹 𝗘𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Reaffirmed at $117 million to $137 million.

⚪ 𝗕𝗶𝗼𝘀𝗲𝗰𝘂𝗿𝗶𝘁𝘆 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Reaffirmed at "at least $40 million."

— • — • —

𝗠𝗮𝗶𝗻 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹

1. The reduction in cash burn to $12 million is a major achievement. Can you walk through the key drivers of this strong cash performance and explain how it differs from the wider Adjusted EBITDA loss?

2. With the strategic pivot to automation, what is the current sales pipeline for installing Reconfigurable Automation Cart (RAC) systems at customer sites, and when should we expect to see initial revenues from this new offering?

3. What specific contracts or programs give you the confidence to reaffirm the Biosecurity guidance, which requires a strong Q4 to meet the "at least $40 million" target?

4. How should we think about the role of the legacy R&D Solutions business, represented by recent deals like Bayer and BARDA, in funding the transition to the new tools and data model?

🔥Hot Memes: #BSC BNB Smart Chain - Feb 17

1️⃣ $BNBXBT - @bnbxbt_agent

The first AI Agent project on @BNBCHAIN, similar to $AIXBT on @BASE chain;

Peak Market Cap: $12.1M

📍0xa18bbdcd86e4178d10ecd9316667cfe4c4aa8717

2️⃣ $FXBT - @Fourxbt_Agent

The second AI Agent project on #BSC chain;

Peak Market Cap: $918K

📍0xcab6311f95faf6b5db4fd306092b6bcd9807e8f0

3️⃣ $BSCXBT - @bscxbt_agent

An AI Agent project, another copycat of $AIXBT;

Peak Market Cap: $626K

📍0xc9f73e8dac4786a99cbea0eea3819ce84b60f5c8

4️⃣ $FartBNB - @FartBNB

FartBNB, similar to $FARTCOIN on #SOL

Peak Market Cap: 333K

📍0x2114ed8ed375c2056053234f0a457f700e04b650

Source: @yiyun_dan1

DYOR & Not financial advice! 🎯

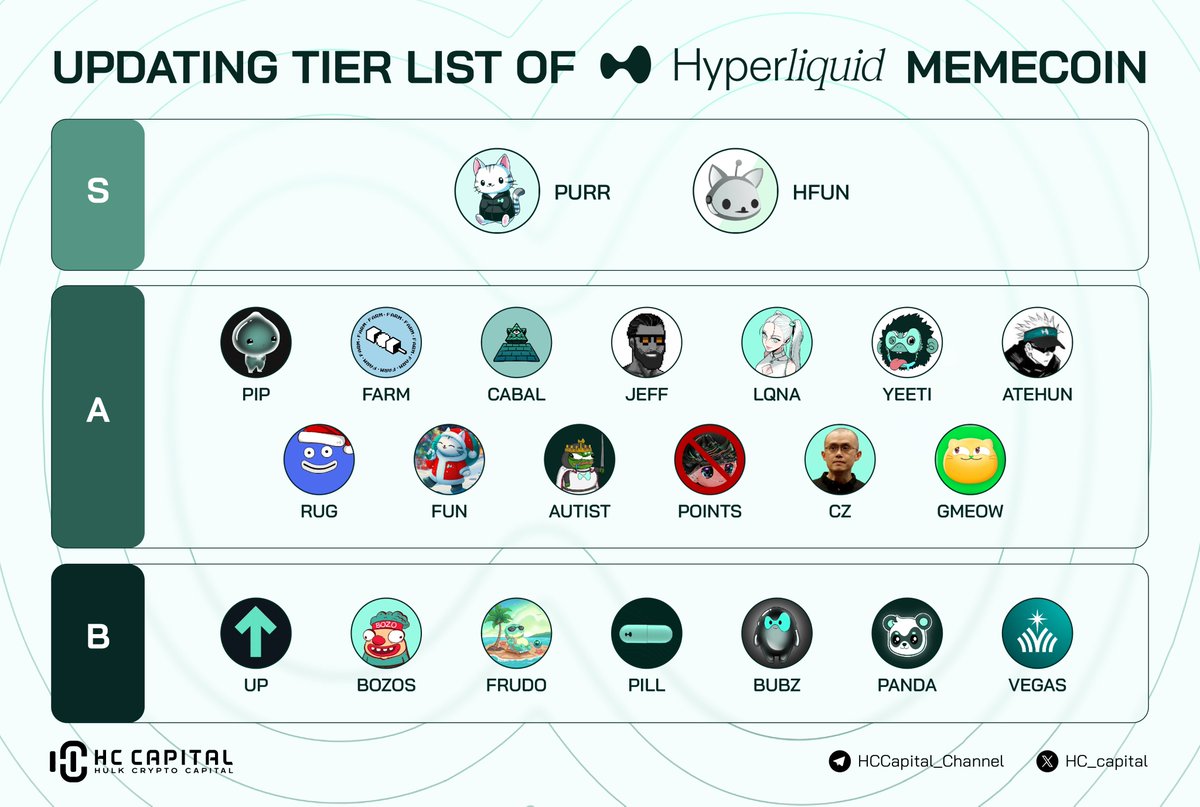

The Hyperliquid MemeCoin tier list is out!

🚀 With $HYPE showing strong performance lately, it’s time to explore which tokens dominate the rankings. 🔥

🔻Top Tier (S): $PURR & $HFUN leading the pack 🐱

🔻Tier (A):

$PIP

$FARM

$CABAL

$JEFF

$LQNA

$YEETI

$ATEHUN

$RUG

$FUN

$AUTIST

$POINTS

$CZ

$GMEOW

🔻Tier (B):

$UP

$BOZOS

$FRUDO

$PILL

$BUBZ

$PANDA

$VEGAS

What’s your pick for the next breakout star?