QUICK MARKET UPDATE

• Stocks bounced back today after last week’s tech-led weakness, with the Nasdaq leading as mega-cap tech and AI names recovered.

• S&P 500 ( $SPY): +1.2% to 7,440.43

• Nasdaq ( $QQQ): +2.1% to 25,820.14

• Dow( $DJIA): +0.6% to 52,182.74. The Dow closed above 52,000 for the first time, marking another record close.

• Big Tech helped carry the rebound, while the S&P 500 snapped a five-day losing streak.

• Comcast rallied after announcing plans to separate its media assets, including NBCUniversal and Sky.

• Charter jumped on media-deal speculation, while Rocket Lab and Iridium moved sharply higher after an $8B acquisition announcement.

• Treasury yields were mostly steady, with the 10Y around 4.38%, keeping rate pressure contained for growth stocks.

• Oil rose as markets watched renewed U.S.-Iran talks and Strait of Hormuz risk.

• Today was a relief bounce led by tech and deal activity, but investors still need confirmation from yields, oil, and labor data.

• Watch Fed Chair Warsh’s comments and the June jobs report next. Those will shape the next move in rate expectations.

QUICK MARKET UPDATE

1/ U.S. futures are mixed this morning as AI-chip weakness returns after Monday’s rebound.

Fact: $SPY, $QQQ, and $DIA ETFs are trading higher premarket, but Reuters reports Nasdaq futures are under pressure as semis fade again.

Interpretation: tech leadership is still fragile.

2/ The macro setup is not clean.

10Y Treasury yield is around 4.50%. Oil is bouncing after vessel attacks near the Strait of Hormuz, with Reuters reporting Brent around $72.60 and WTI around $69.04.

Fact: higher yields + higher oil can pressure growth stocks and inflation-sensitive trades.

3/ Main catalyst this week: Fed minutes.

Investors are watching Wednesday’s FOMC minutes for clues on how the Fed is reading softer jobs, sticky inflation risk, and tighter financial conditions.

Key risk: if yields keep moving higher, the Nasdaq ($QQQ) bounce could struggle.

4/ Stock movers:

$RIVN is lower after announcing a 75M share offering.

$FI is higher after Reuters reported talks around a possible debit-card network sale.

Semis remain the key tape read: $NVDA, $AMD, $MU, $AVGO, $SMH.

5/ Key takeaway:

The market is not fully risk-off, but it is less clean than Monday. Dow strength shows rotation is alive, while Nasdaq weakness shows AI names still need confirmation.

This week is about whether earnings and Fed commentary can support valuations while oil and yields move higher.

QUICK MARKET UPDATE

• Stocks started the week strong as AI and semiconductor names bounced back after recent pressure.

• S&P 500( $SPY): +0.72% to 7,537.43

• Nasdaq( $QQQ): +1.12% to 26,121.16

• Dow( $DJIA): +0.29% to 53,055.91

• The Dow closed above 53,000 for the first time, while the Nasdaq led as tech regained momentum.

• Broadcom( $AVGO) rose after extending its Apple chip-supply agreement through 2031, helping lift semiconductor sentiment.

• The S&P 500 Information Technology sector gained 1.3%, while the Philadelphia Semiconductor Index rose 2.2%.

• Microsoft ( $MSFT)slipped after announcing more layoffs, showing cost discipline remains a theme even inside mega-cap tech.

• ISM Services came in at 54.0 for June, still signaling expansion but slightly slower than May.

• Treasury yields eased slightly, with the 10Y around 4.48%–4.49%, helping support growth stocks.

• Clean read: today’s rally was led by tech and AI, but breadth was not perfect. More S&P 500 stocks fell than rose.

• Next focus: Q2 earnings, SK Hynix’s Nasdaq debut, and the July 28–29 Fed meeting.

• The market is rewarding AI exposure again, but investors still need confirmation from earnings before calling this a full leadership reset.

📊 ISM Services PMI Remains in Expansion, but Growth Slows

Fact: The ISM Services PMI eased to 54.0 in June from 54.5 in May, remaining above the 50 level that signals expansion. The Prices Paid Index also cooled to 67.7 from 71.3, while the Employment Index returned to expansion at 51.2 after three months of contraction.

Takeaway: The U.S. services sector is still growing, but momentum is moderating. Encouragingly, hiring improved and inflation pressures eased from May's elevated levels.

Why investors should care: Services account for roughly 70% of the U.S. economy. A resilient services sector supports corporate earnings and economic growth, while softer price pressures could help ease inflation concerns heading into the next Fed meeting.

Risk / Context: Fact: The sector remains in expansion, but new orders slowed from the previous month. Interpretation: If demand continues to cool over the coming months, economic growth could moderate further. Conversely, persistent strength could reinforce expectations that the Federal Reserve keeps policy restrictive for longer.

@HariOm82979806@barstoolsports Shouldn't be a red card

He got the ball first according to the rule shouldn't be a foul. what else he can do in that situation fold his leg after the tackle? 🤣

BREAKING

Meta Platforms ( $META ) is reportedly negotiating a massive $6.5 BILLION chip-manufacturing deal with Samsung Foundry to produce its third-generation custom AI chip, the Meta Training and Inference Accelerator (MTIA), South Korean financial publication Sedaily reported.

QUICK MARKET UPDATE

-U.S. markets are closed today for Independence Day observance, so the real setup is for Monday.

The Dow ($DJIA) just closed at a record 52,900.07, while the S&P 500 ($SPY) finished flat at 7,483.24 and Nasdaq ($QQQ) fell 0.8% as semis dragged.

-The macro read: softer labor, but not a layoff shock.

June NFP: +57K

Unemployment: 4.2%

Labor force participation: 61.5%

Initial claims: 215K

Fact: hiring slowed. Interpretation: markets are pricing less near-term Fed pressure, but the participation drop makes the unemployment decline less clean.

-Sector setup is rotation-heavy.

Dow strength = defensives / blue chips catching flows.

Nasdaq weakness = AI and semiconductor profit-taking.

Reuters reported the SOX chip index fell 5.4% Thursday after a 6.3% drop Wednesday. Watch $NVDA, $MU, $AVGO, $AMD, $LRCX, and $SMH for confirmation Monday.

-Oil remains a key inflation input.

Brent is near $71.76 and WTI near $68.49 as U.S.–Iran peace efforts continue to hold. Lower crude helps the inflation narrative, but the geopolitical risk premium is not fully gone.

-This is not a full risk-on signal yet. The clean setup is: softer jobs + lower oil supports multiples, but tech leadership is wobbling.

Next major catalyst: Fed minutes on July 8, early Q2 earnings, and whether semis stabilize after the

QUICK MARKET UPDATE

• Stocks closed mixed as investors digested a softer June jobs report and renewed weakness in tech.

• S&P 500 ( $SPY): -0.13%

• Nasdaq ( $QQQ): -1.73%

• Dow ( $DJIA): +0.45%

• The Dow outperformed and posted its fourth straight weekly gain, while Nasdaq weakness came from tech and semiconductor selling.

• June payrolls came in at +57,000, below expectations, while unemployment held at 4.2%.

• Treasury yields fell after the labor data, with the 10Y around 4.46% and the 2Y around 4.11%.

• Tesla dropped despite stronger-than-expected Q2 deliveries, showing the good news was already partly priced in.

• Semiconductors stayed under pressure as investors continued questioning AI capex, valuations, and near-term earnings durability.

• Oil moved lower as U.S.-Iran diplomatic progress helped ease supply-risk concerns.

• Softer jobs reduced near-term Fed hike pressure, but tech leadership still looks fragile.

• Monday’s reopen after the holiday weekend, followed by Fed commentary, yields, and whether chips can stabilize.

QUICK MARKET UPDATE

NFP is out, and the market is getting a softer labor print without a major layoff signal.

The U.S. added 57K jobs in June, below the 110K expected. May was revised down to 129K, and April/May were revised lower by a combined 74K.

Unemployment fell to 4.2%, but the labor force participation rate dropped to 61.5%, so the lower unemployment rate is not a clean “strong labor market” signal.

Wages rose 0.3% MoM and 3.5% YoY, while weekly jobless claims came in at 215K, showing layoffs are still controlled.

Markets initially liked the report because it reduced near-term Fed hike pressure. Reuters reported futures higher after the print: Dow futures +0.40%, S&P 500 futures +0.37%, Nasdaq 100 futures +0.58%.

Oil is also helping sentiment. Brent fell near $70 and WTI near $67 after U.S.–Iran talks in Doha made progress around the Strait of Hormuz, but there is still no final peace deal yet.

Tech remains the swing factor. Semis were hit hard yesterday, with the SOX chip index down about 6.3%, so today’s bounce needs confirmation from $QQQ, $NVDA, $MU, $ARM, and $SNDK.

Stock movers to watch:

$RIVN raised its 2026 delivery outlook after stronger Q2 deliveries.

$BSP is pulling back after a strong Nasdaq debut.

$META is still in focus after yesterday’s AI cloud-related rally.

$TSLA delivery numbers remain a major EV catalyst today.

Softer NFP helps rate-sensitive stocks, lower oil helps inflation pressure, and low jobless claims reduce recession fear. But this is not a full all-clear. The next big test is CPI on July 14, plus whether tech can stabilize after the chip selloff.

QUICK MARKET UPDATE

• S&P 500 ( $SPY): -0.19% to 7,485.02

• Nasdaq ( $QQQ): -0.65% to 26,044.16

• Dow ( $DJIA) : -0.01% to 52,315.58

• Stocks slipped to start the second half as weakness in tech and semiconductors outweighed broader support.

• Semiconductors stayed under pressure, weighing on the S&P 500 and Nasdaq after a strong Q2 run.

• Meta jumped on reports it may sell unused AI computing capacity, helping cushion the broader tech decline.

• General Mills rose after earnings, while Alcoa dropped after agreeing to buy South32 aluminum assets.

• Treasury yields moved higher, with the 10Y around 4.49%, keeping pressure on long-duration growth stocks.

• Fed Chair Kevin Warsh said inflation risks have eased recently but reaffirmed the Fed’s 2% inflation target.

• Manufacturing data came in softer, but investors are waiting for the bigger labor-market test.

• This was rotation and profit-taking after a strong quarter, not a broad risk-off breakdown.

• Watch Thursday’s June jobs report. That will drive the next move in yields, Fed expectations, and tech sentiment.

QUICK MARKET UPDATE

U.S. markets are trying to hold a small risk-on bounce after the latest labor data came in softer than expected.

ADP reported 98K private jobs added in June, below the 118K expected and down from **122K in May**. That points to slower hiring, but not a labor-market breakdown yet.

$SPY, $QQQ, and $DJIA are all green premarket, with tech leading again. $QQQ is up the most, showing investors are still willing to buy growth when labor data supports lower rate pressure.

The 10Y Treasury yield is near 4.50% so the bond market is not giving stocks a full green light yet. If yields keep pushing higher, the tech bounce could lose momentum.

U.S.–Iran technical talks are also underway in Doha today, focused on the Strait of Hormuz, shipping flows, and frozen Iranian assets. That matters because oil is still one of the biggest inflation risks for this market.

$BTC is slightly lower, oil is softer, and the market is now looking ahead to ISM Manufacturing at 10:00 a.m. ET and tomorrow’s June jobs report.

Softer ADP helps rate-cut hopes, but yields and Iran headlines still control the tape today.

QUICK MARKET UPDATE

• Stocks finished the quarter strong as tech and AI-related names bounced back.

• S&P 500 ( $SPY) : +0.8% to 7,499.36

• Nasdaq ( $QQQ) : +1.5% to 26,213.72

• Dow ( $DJIA) : +0.3% to 52,319.20

• Russell 2000: +0.5% to 3,024.37

• The Dow closed at another record high, while the S&P 500 and Nasdaq posted their strongest quarter since 2020.

• Tech led the move, with chip names rebounding after recent valuation pressure.

• AeroVironment surged after stronger-than-expected earnings, while $AMD , $SNDK.NE , Applied Materials, and Lam Research were among the stronger tech/chip movers.

• Treasury yields moved higher, with the 10Y around 4.42%, keeping rate risk in the background.

• JOLTS showed job openings at 7.6M in May, signaling the labor market remains resilient even as hiring stays cautious.

• Oil moved lower, helping ease some inflation pressure into the quarter-end close.

• Clean read: the market ended Q2 with strong momentum, but the next test is whether tech strength can hold with yields rising and jobs data still ahead.

• Watch Thursday’s June jobs report. That will shape the next move in Fed expectations, yields, and risk appetite.

QUICK MARKET UPDATE

U.S. stocks opened mixed, but tech is trying to lead again into the final trading day of Q2.

$SPY +0.30%

$QQQ +0.85%

$DIA slightly red

The market is still holding up after a strong quarter, but the move is not broad. Tech is doing most of the work while the Dow is lagging.

Fresh macro data is mixed. JOLTS job openings came in around 7.59M, above expectations, showing labor demand is still firm. Consumer confidence rose slightly to 91.2, but consumers are still showing concern about jobs and high prices.

Treasury yields are still the main pressure point, with the 10Y near 4.38%–4.39%. If yields keep climbing, tech could lose momentum fast.

Oil is still a major relief factor. Brent is around $73 and WTI around $71, with crude heading for its steepest quarterly drop since 2020 as markets watch U.S.–Iran talks.

Stock movers:

$AVAV is ripping after strong earnings and revenue growth.

$CNXC is getting hit hard after cutting guidance.

$MU is holding up as semis try to stabilize.

Tech is trying to carry the tape, but yields, labor data, oil, and Thursday’s jobs report will decide if this rally keeps going or starts fading.

QUICK MARKET UPDATE

• U.S. futures are starting the week risk-on after another Middle East de-escalation headline. Fact: Dow futures were up 0.51%, S&P ( $SPY) 500 futures +0.91%, and Nasdaq 100 futures ( $QQQ) +1.28% early Monday.

• The hook: tech is leading the bounce, but this is not a clean “all-clear.” Investors are buying relief from lower geopolitical risk, while still questioning AI spending, chip margins, and elevated tech valuations.

• Macro setup: the 10Y Treasury yield is near 4.38%. May PCE inflation hit 4.1% y/y, still well above the Fed’s 2% target. The next major macro checkpoint is Thursday’s June jobs report.

• Stock/sector movers: $CMCSA jumped premarket after announcing a spin-off plan. $SPCX rose after Nasdaq said it will join the Nasdaq 100 on July 7. $VRDN surged after FDA approval for its thyroid eye disease drug.

• Lower geopolitical stress can support risk assets, but inflation and labor data still control the Fed narrative. Clean read: short-term sentiment improved, but tech needs earnings follow-through to keep leadership.

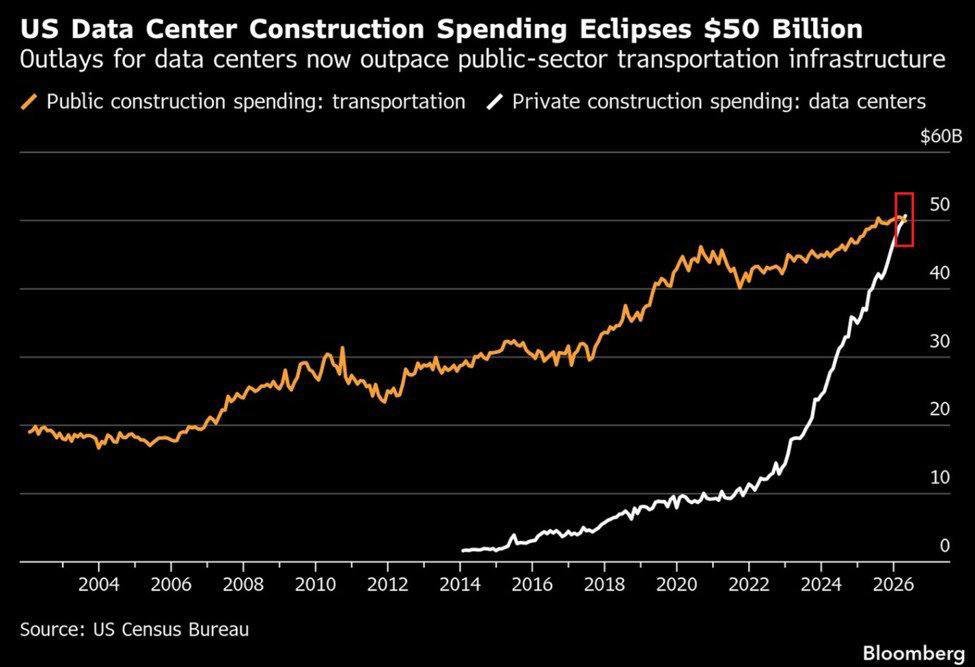

U.S. data center spending now surpasses most infrastructure projects.

According to Bloomberg, U.S. spending on data center construction has reached $50 billion, surpassing the combined spending on airports, ports, and mass transit.

The AI infrastructure boom continues to accelerate, with US data center construction spending up 357% since 2022 and now accounting for 2.3% of all U.S. construction spending.

QUICK MARKET UPDATE

- $SPY (S&P 500): Softened by -0.08% to close at 7,351.82. The broader benchmark navigated heavy multi-directional institutional crosscurrents, carving out an introspective intraday range between 7,294.83 and 7,368.81 before consolidating steadily into the final weekend bell.

- $QQQ (Nasdaq Composite): Edged lower by -0.24% to settle the active week at 25,297.62. Stretched technology multiples faced brief mechanical adjustments, with structural tracking funds actively balancing large cap risk parameters as the massive post-earnings technology distribution began to taper off.

- $DJIA (Dow Jones Industrial Average): Outperformed major capitalization peers on a relative basis, sliding -0.08% to wrap up the session at 51,876.11. The blue-chip index successfully defended its near-term trading floor after testing an early session high of 52,130.07, anchored by defensive industrial and healthcare capital inflows.

Macro Catalyst: Portfolios are calculating systematic adaptations following a wave of hawkish macro developments. June's sticky headline metrics have forced systematic models to adjust for a "higher-for-longer" rate horizon. The 10-year Treasury yield consolidated around 4.38%, with institutional traders actively managing collateral ahead of upcoming quarter-end rebalancing mandates.

-Digital Assets & Core Crypto Levels:

Bitcoin ( $BTC): Mounted a vital technical defense, sliding marginally into the weekend tape at $59,975. Despite enduring nearly $3 billion in aggregate month-to-date spot ETF outflows, real-money volume stepped in to preserve structure, preventing a prolonged drop below the crucial $58,115 multi-month support floor.

Ethereum ( $ETH): Experienced severe technical friction, tumbling -5.04% to settle near $1,563. Algorithmic liquidations triggered roughly $600 million in wider derivatives flushouts, forcing macro desks to closely guard the vital $1,500 psychological demand boundary.

QUICK MARKET UPDATE

• U.S. futures are pointing to a softer open as the tech trade cools again. $SPY futures are down roughly 0.4%–0.5%, Nasdaq futures are leading lower, and $DJIA futures are holding up better.

• The hook: this market is no longer “everything AI goes up.” Micron’s strong forecast helped semis yesterday, but the follow-through is fading as investors question AI valuations and hyperscaler spending.

• Macro setup: PCE inflation remains above the Fed’s 2% target. May PCE rose 4.1% y/y, with prices up 0.4% m/m. Treasury yields are easing, which helps, but inflation is still not fully solved.

• Stock/sector movers: semis are under pressure again, $MU is giving back part of its post-earnings move, and $ON agreed to buy $SYNA in a $7B all-stock deal. Banks remain in focus after the Fed said large banks are well positioned after stress tests.

• Lower yields and lower oil can support risk assets, but the market still needs proof that AI earnings can justify premium valuations. Clean read: macro is improving at the margin, but tech leadership is being tested.

📊 QUICK MARKET UPDATE:

Wall Street navigates a massive structural tug-of-war as inflation numbers drop and tech faces a historic realignment.

$DJIA hits a new all-time intraday high before closing up +0.14% to 51,960.62.

$SPY finishes virtually flat, dipping just -0.01% to 7,357.49.

$QQQ drops -0.50% to 25,358.60 as a deep mega-cap split dictates the tape.

-The AI vs. Consumer Split: Micron ( $MU) rockets +15.7% on blockbuster AI guidance, but Apple ( $AAPL ) craters -6.1% after raising Mac prices by 15-20% to fight rising input costs. Meanwhile, Core PCE inflation hits exactly as expected (+3.4% y/y), cooling 10-year yields to 4.38%.

-Crypto Flush: A violent $397M long liquidation cascade and persistent ETF outflows drag Bitcoin ( $BTC) down to $59,772 and Ethereum ( $ETH) to $1,692