Charlie Munger's secret to a long & happy life:

"simple... you don't have a lot of envy, don't have resentment, don't overspend your income, stay cheerful in spite of your troubles..."

Warren Buffett on why chasing yield on cash is a mistake:

A Berkshire shareholder, Ed Schmidt, asks where all the sidelined money is being held, pointing out that every option looks bad:

Banks paying nothing, risky corporate bonds, and government bonds that "seem less and less sound as each day passes."

Buffett agrees the choices are poor, but says it doesn't matter, because Berkshire treats short-term money completely differently from most investors.

"He's certainly right that all the choices are lousy for short-term money now, but we don't play around with short-term money."

He explains that in 2008, before the crisis hit, Berkshire owned no commercial paper and no money market funds.

The big money stayed in treasuries, earning almost nothing, and Buffett is blunt that the temptation to reach for a little more is exactly the trap to avoid:

"The last thing in the world we would do at Berkshire is to try and get five or 10 or 20 or 30 basis points more by going into some other things with our short-term money."

His framing for why is simple:

"It is a parking place. It's an unattractive parking place, but it's a parking place where we know we'll get our car back when we want it."

The reason that matters became clear in September 2008. Berkshire had committed $6.5 billion to the Mars-Wrigley deal months earlier, long before anyone knew what that autumn would bring.

When the date arrived, the form of the money was everything:

"I had to show up with $6.5 billion. I couldn't show up with a money market fund or some commercial paper or anything of the sort. I had to show up with cash."

That's why his conviction lands where it does:

"Virtually the only thing I feel good about in terms of having large amounts of ready cash is treasury bills."

Charlie Munger puts it more sharply, reframing the whole question as a discipline issue rather than a yield issue:

"I think it's really stupid to try and maximize returns on short-term money if you're an opportunistic game the way we are, where we want to suddenly deploy money."

He points to pipelines that came up for sale on a Saturday and had to close by Monday.

There was no room to be stuck in "some dubious instrument" when the cash was suddenly needed.

Buffett adds his own version of the same story, a pipeline whose seller feared bankruptcy the following week and needed the money immediately, with regulatory clearance still pending. Berkshire offered to close early and let the regulators review everything afterward, even unwind the deal if required. The point being that readiness, not return, is what closes deals:

"Our ability to come up with cash when people need it, and when the rest of the world is petrified for some reason, has enabled several deals to get done."

And that is the entire logic behind holding tens of billions in treasuries earning almost nothing:

"When somebody comes to us and they say we need a deal right now, we can do it, and they know we can do it, and it can be big. It just has to be attractive."

Warren Buffett:

“Making $1 million a year looks great until this guy who sits next to you, who can't possibly be as smart as you, is making $1 million, too. Then the whole world turns into a very unfair place.”

Buffett & Charlie Munger on what really drives the world:

Mohnish Pabrai on @myfirstmilpod: "[Charlie Munger] never complained."

"Even when he was facing the prospect of complete blindness, he was so stoic [and] never said, 'Oh, poor me.' His response to me was, 'I'm going to have to learn Braille.'"

Charlie Munger, the Stoic: "Life will have terrible blows in it. Horrible blows. Unfair blows. It doesn't matter. And some people recover and others don't."

"There, I think the attitude of Epictetus is the best. He thought that every mischance in life was an opportunity to behave well. Every mischance in life was an opportunity to learn something. Your duty was not to be submerged in self-pity, but to utilize the terrible blow in a constructive fashion."

Nick Sleep identified 𝐟𝐨𝐮𝐫 𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐨𝐟 𝐢𝐧𝐯𝐞𝐬𝐭𝐨𝐫 𝐦𝐢𝐬𝐣𝐮𝐝𝐠𝐦𝐞𝐧𝐭 that he believed explained most mistakes in markets. Twenty years later, not much has changed.

1️⃣ 𝐒𝐨𝐜𝐢𝐚𝐥 𝐏𝐫𝐨𝐨𝐟 / 𝐆𝐫𝐨𝐮𝐩 𝐏𝐬𝐲𝐜𝐡𝐨𝐥𝐨𝐠𝐲

Markets don’t move on fundamentals alone — they move on crowds. Sleep pointed to Milgram’s famous experiment: the larger the group looking up at nothing, the more passersby stopped to look too. Capital allocation works the same way. Once enough companies start building capacity, fear of missing out pulls the rest in — rational individual decisions producing collectively irrational outcomes. Thai cement in the 1990s. US telecom in 1999. Combine social proof with envy and financial incentives, Sleep wrote, and you have a recipe for a sizeable mistake.

2️⃣ 𝐀𝐯𝐚𝐢𝐥𝐚𝐛𝐢𝐥𝐢𝐭𝐲

Investors gravitate toward what can be measured and ignore what cannot. Sleep’s point was precise: there is a wealth of information in items accountants expense or ignore entirely — advertising effectiveness, product integrity, management character, market share trajectory. The edge rarely lives in the spreadsheet. It lives in the questions the spreadsheet doesn’t ask.

3️⃣ 𝐏𝐫𝐨𝐛𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐁𝐚𝐬𝐞𝐝 𝐓𝐡𝐢𝐧𝐤𝐢𝐧𝐠

Munger said the right way to think is the way Zeckhauser plays bridge — through decision trees with probabilities attached to each branch, updated as facts change. Most investors don’t think this way. They anchor on a single outcome and defend it. Sleep’s observation: understanding the value of a business means weighing the probable range of outcomes, not betting on one. An inability to think in probabilities is behind most misevaluations.

4️⃣ 𝐏𝐚𝐭𝐢𝐞𝐧𝐜𝐞

When asked what separates him from the average investor, Buffett answered with one word: patience. Sleep found this indicting. The average stock holding period at the time he wrote this was 10 months. Quarterly reporting had become, in his words, borderline obsessive-compulsive. And he identified exactly why — fund managers performing for clients, clients performing for fund managers, a spiral of dysfunctional behavior that nobody individually believes is correct but everyone participates in anyway. His most important line on this: as equity owners we hold the only permanent capital in a company’s capital structure. Everything else — management, assets, employees — can change. The equity remains. Institutional investors have never reconciled their ability to trade daily with the permanence of what they own.

___

The four compound on each other.

𝘚𝘰𝘤𝘪𝘢𝘭 𝘱𝘳𝘰𝘰𝘧 𝘤𝘳𝘦𝘢𝘵𝘦𝘴 𝘵𝘩𝘦 𝘤𝘳𝘰𝘸𝘥. 𝘈𝘷𝘢𝘪𝘭𝘢𝘣𝘪𝘭𝘪𝘵𝘺 𝘵𝘦𝘭𝘭𝘴 𝘵𝘩𝘦 𝘤𝘳𝘰𝘸𝘥 𝘸𝘩𝘢𝘵 𝘵𝘰 𝘧𝘰𝘤𝘶𝘴 𝘰𝘯. 𝘗𝘰𝘰𝘳 𝘱𝘳𝘰𝘣𝘢𝘣𝘪𝘭𝘪𝘴𝘵𝘪𝘤 𝘵𝘩𝘪𝘯𝘬𝘪𝘯𝘨 𝘮𝘦𝘢𝘯𝘴 𝘵𝘩𝘦𝘺 𝘮𝘪𝘴𝘱𝘳𝘪𝘤𝘦 𝘪𝘵. 𝘈𝘯𝘥 𝘪𝘮𝘱𝘢𝘵𝘪𝘦𝘯𝘤𝘦 𝘮𝘦𝘢𝘯𝘴 𝘦𝘷𝘦𝘯 𝘪𝘯𝘷𝘦𝘴𝘵𝘰𝘳𝘴 𝘸𝘩𝘰 𝘬𝘯𝘰𝘸 𝘣𝘦𝘵𝘵𝘦𝘳 𝘢𝘤𝘵 𝘣𝘦𝘧𝘰𝘳𝘦 𝘵𝘩𝘦 𝘵𝘩𝘦𝘴𝘪𝘴 𝘩𝘢𝘴 𝘵𝘪𝘮𝘦 𝘵𝘰 𝘱𝘳𝘰𝘷𝘦 𝘪𝘵𝘴𝘦𝘭𝘧.

𝙏𝙝𝙚 “𝙖𝙣𝙩𝙞𝙙𝙤𝙩𝙚” 𝙩𝙤 𝙖𝙡𝙡 𝙛𝙤𝙪𝙧 𝙞𝙨: 𝙞𝙣𝙙𝙚𝙥𝙚𝙣𝙙𝙚𝙣𝙩 𝙩𝙝𝙞𝙣𝙠𝙞𝙣𝙜, 𝙖𝙥𝙥𝙡𝙞𝙚𝙙 𝙥𝙖𝙩𝙞𝙚𝙣𝙩𝙡𝙮, 𝙩𝙝𝙤𝙪𝙜𝙝𝙩𝙛𝙪𝙡𝙡𝙮 𝙢𝙚𝙖𝙨𝙪𝙧𝙞𝙣𝙜 𝙬𝙝𝙖𝙩 𝙤𝙩𝙝𝙚𝙧𝙨 𝙤𝙫𝙚𝙧𝙡𝙤𝙤𝙠, 𝙪𝙥𝙙𝙖𝙩𝙞𝙣𝙜 𝙮𝙤𝙪𝙧 𝙥𝙧𝙤𝙗𝙖𝙗𝙞𝙡𝙞𝙩𝙞𝙚𝙨 𝙖𝙨 𝙛𝙖𝙘𝙩𝙨 𝙘𝙝𝙖��𝙜𝙚 — 𝙤𝙫𝙚𝙧 𝙖 𝙝𝙤𝙧𝙞𝙯𝙤𝙣 𝙡𝙤𝙣𝙜 𝙚𝙣𝙤𝙪𝙜𝙝 𝙩𝙝𝙖𝙩 𝙩𝙝𝙚 𝙙𝙚𝙨𝙩𝙞𝙣𝙖𝙩𝙞𝙤𝙣 𝙢𝙖𝙩𝙩𝙚𝙧𝙨 𝙢𝙤𝙧𝙚 𝙩𝙝𝙖𝙣 𝙩𝙝𝙚 𝙟𝙤𝙪𝙧𝙣𝙚𝙮.

___

📝 Nomad Investment Partnership Letters (Dec 2005)

In 2005, Nick Sleep wrote one of the most brilliant pieces of investment analysis ever published on $COST Costco.

Sleep measured something most analysts weren’t even looking for.

He called it the 𝐑𝐨𝐛𝐮𝐬𝐭𝐧𝐞𝐬𝐬 𝐑𝐚𝐭𝐢𝐨.

𝘛𝘩𝘦 𝘤𝘰𝘯𝘤𝘦𝘱𝘵 𝘸𝘢𝘴 𝘴𝘪𝘮𝘱𝘭𝘦: 𝘵𝘢𝘬𝘦 𝘵𝘩𝘦 𝘤𝘰𝘮𝘣𝘪𝘯𝘦𝘥 𝘣𝘦𝘯𝘦𝘧𝘪𝘵𝘴 𝘥𝘪𝘴𝘵𝘳𝘪𝘣𝘶𝘵𝘦𝘥 𝘵𝘰 𝘤𝘶𝘴𝘵𝘰𝘮𝘦𝘳𝘴 𝘢𝘯𝘥 𝘦𝘮𝘱𝘭𝘰𝘺𝘦𝘦𝘴, 𝘥𝘪𝘷𝘪𝘥𝘦 𝘪𝘵 𝘣𝘺 𝘸𝘩𝘢𝘵 𝘴𝘩𝘢𝘳𝘦𝘩𝘰𝘭𝘥𝘦𝘳𝘴 𝘳𝘦𝘤𝘦𝘪𝘷𝘦. 𝘛𝘩𝘦 𝘩𝘪𝘨𝘩𝘦𝘳 𝘵𝘩𝘦 𝘳𝘢𝘵𝘪𝘰, 𝘵𝘩𝘦 𝘸𝘪𝘥𝘦𝘳 𝘢𝘯𝘥 𝘮𝘰𝘳𝘦 𝘶𝘯𝘢𝘴𝘴𝘢𝘪𝘭𝘢𝘣𝘭𝘦 𝘵𝘩𝘦 𝘮𝘰𝘢𝘵 — 𝘣𝘦𝘤𝘢𝘶𝘴𝘦 𝘵𝘩𝘦 𝘣𝘶𝘴𝘪𝘯𝘦𝘴𝘴 𝘪𝘴 𝘥𝘦𝘭𝘪𝘣𝘦𝘳𝘢𝘵𝘦𝘭𝘺 𝘶𝘯𝘥𝘦𝘳-𝘦𝘢𝘳𝘯𝘪𝘯𝘨 𝘵𝘰𝘥𝘢𝘺 𝘵𝘰 𝘮𝘢𝘬𝘦 𝘪𝘵𝘴𝘦𝘭𝘧 𝘪𝘮𝘱𝘰𝘴��𝘪𝘣𝘭𝘦 𝘵𝘰 𝘤𝘰𝘮𝘱𝘦𝘵𝘦 𝘸𝘪𝘵𝘩 𝘵𝘰𝘮𝘰𝘳𝘳𝘰𝘸.

GEICO’s ratio was 1:1. A fair division.

Costco’s was 5:1.

Five dollars going to customers and employees for every one dollar going to shareholders. Wall Street looked at that and saw a business leaving money on the table. Sleep looked at it and saw a fortress.

Sleep didn’t just study Costco in isolation — he stress-tested the moat against its closest competitor. His conclusion: for Sam’s Club to simply match Costco’s customer savings and employee pay scales would cost them over $2B annually. Not to beat Costco. Just to tie. That gap, he noted, was not insignificant even to Walmart — which at the time earned $9B in net profits. The competitive gap wasn’t narrow. It was structural and widening.

And here’s what I find most admirable. Sleep watched Wall Street pressure Costco’s management to shift the division of benefits toward shareholders. To satisfy what he called the “𝐪𝐮𝐚𝐫𝐭𝐞𝐫𝐥𝐲 𝐄𝐏𝐒 𝐣𝐮𝐧𝐤𝐢𝐞𝐬.” And he said clearly that long-term shareholders should view any such slippage as worrying and unnecessary.

Because the entire thesis depended on Costco maintaining the discipline to under-earn. 𝙏𝙝𝙚 𝙢𝙤𝙢𝙚𝙣𝙩 𝙢𝙖𝙣𝙖𝙜𝙚𝙢𝙚𝙣𝙩 𝙨𝙩𝙖𝙧𝙩𝙚𝙙 𝙤𝙥𝙩𝙞𝙢𝙞𝙯𝙞𝙣𝙜 𝙛𝙤𝙧 𝙧𝙚𝙥𝙤𝙧𝙩𝙚𝙙 𝙚𝙖𝙧𝙣𝙞𝙣𝙜𝙨, 𝙩𝙝𝙚 𝙢𝙤𝙖𝙩 𝙬𝙤𝙪𝙡𝙙 𝙗𝙚𝙜𝙞𝙣 𝙩𝙤 𝙣𝙖𝙧𝙧𝙤𝙬 — not visibly, not immediately, but inevitably. The robustness ratio drifting toward shareholders isn’t a gift to investors. It’s a withdrawal from the competitive fortress that made the investment worth owning in the first place.

And then the final line — perhaps the most important insight:

“𝘞𝘩𝘦𝘳𝘦 𝘳𝘰𝘣𝘶𝘴𝘵𝘯𝘦𝘴𝘴 𝘤𝘰𝘮𝘦𝘴 𝘪𝘯𝘵𝘰 𝘪𝘵𝘴 𝘰𝘸𝘯 𝘪𝘴 𝘪𝘯 𝘪𝘥𝘦𝘯𝘵𝘪𝘧𝘺𝘪𝘯𝘨 𝘤𝘰𝘮𝘱����𝘯𝘪𝘦𝘴 𝘸𝘩𝘪𝘤𝘩 𝘮𝘢𝘺 𝘣𝘦 𝘶𝘯𝘥𝘦𝘳-𝘦𝘢𝘳𝘯𝘪𝘯𝘨 𝘸𝘩𝘦𝘯 𝘤𝘰𝘮𝘱𝘢𝘳𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦𝘪𝘳 𝘱𝘰𝘵𝘦𝘯𝘵𝘪𝘢𝘭. 𝘛𝘩𝘪𝘴 𝘨𝘦𝘯𝘦𝘳𝘢𝘵𝘦𝘴 𝘴𝘶𝘱𝘦𝘳 𝘭𝘰𝘯𝘨-𝘵𝘦𝘳𝘮 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵 𝘰𝘱𝘱𝘰𝘳𝘵𝘶𝘯𝘪𝘵𝘪𝘦𝘴 𝘧𝘰𝘳 𝘵𝘩𝘰𝘴𝘦 𝘸𝘪𝘭𝘭𝘪𝘯𝘨 𝘵𝘰 𝘭𝘰𝘰�� 𝘣𝘦𝘺𝘰𝘯𝘥 𝘳𝘦𝘱𝘰𝘳𝘵𝘦𝘥 𝘦𝘢𝘳𝘯𝘪𝘯𝘨𝘴.”

This is the edge Sleep was describing. A framework for finding businesses that look mediocre on the income statement precisely because they are busy building something that a competitor cannot afford to match. Most investors look at reported earnings and see the business. Sleep looked at reported earnings and asked what the business was choosing not to report — and why.

That one-level-deeper question was the difference between seeing Costco as a low-margin retailer or seeing it as one of the greatest compounding machines with strong long-term potential.

Occidental Petroleum CEO Vicki Hollub: "We made the decision that, geopolitically, we needed to be more of a U.S. company."

"When I took over in 2015, 50% of our production was in the Middle East and international operations. Now, 83% of our production is in the United States."

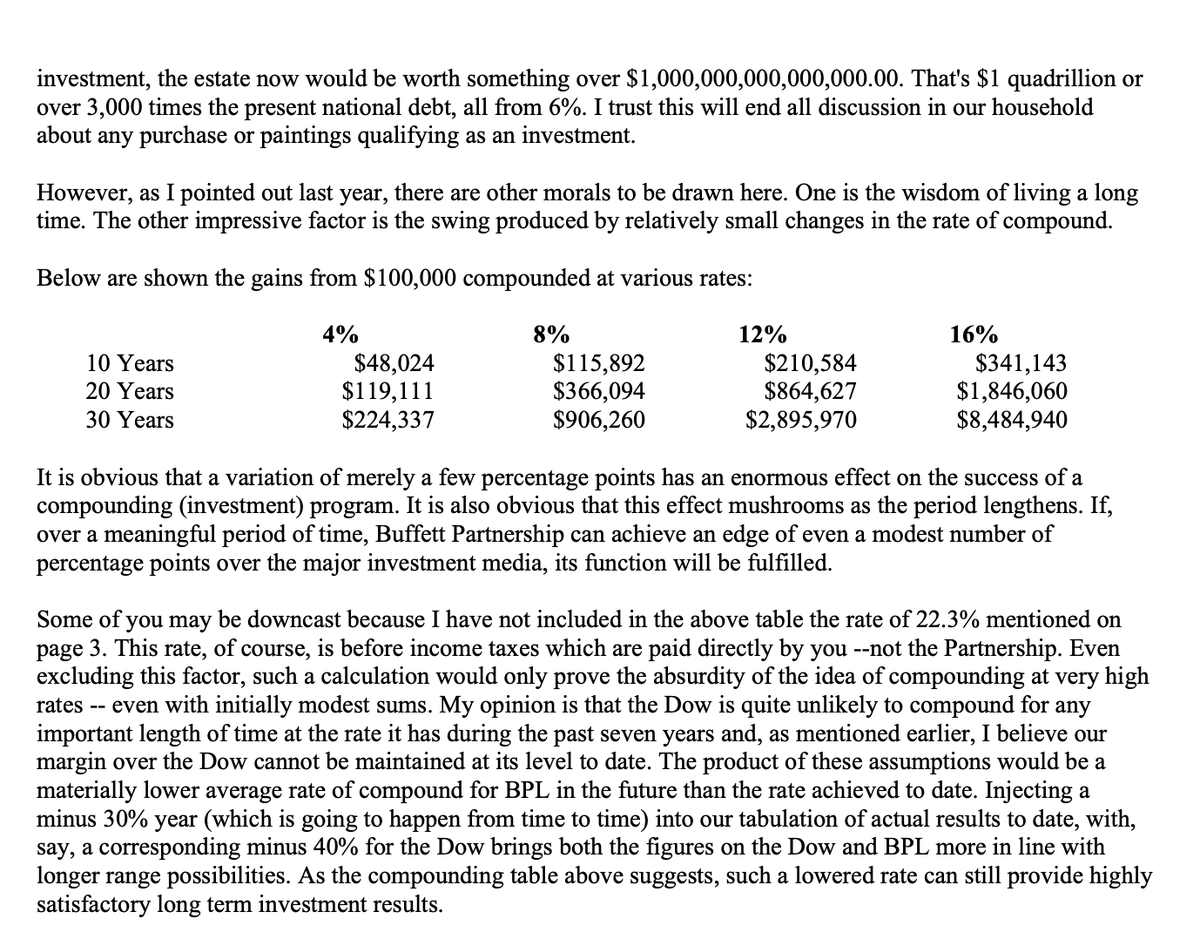

Love this excerpt from Buffett's 1864 partnership letter 👇🏻

In 1540, King Francis I bought the Mona Lisa for roughly $20,000.

Buffett’s 1964 math: If the King had invested that $20k at 6% instead, his estate would be worth $1 QUADRILLION today. That is 3,000x the national debt (at the time).

The ultimate lesson in the "absurdity" of compounding.

Meet Warren Buffett, the Arbitrageur.

“Because my mother isn’t here tonight, I’ll even confess to you that I’ve been an arbitrageur.”

- Warren Buffett

> In the 1954, a young Warren Buffett spotted an unusual opportunity hidden inside a commodity price shock.

> Cocoa prices in the US had suddenly surged from just 5 cents to 60 cents per pound due to a temporary shortage. One company, Rockwood & Co., happened to be sitting on a massive stockpile of cocoa. On paper, this inventory had turned incredibly valuable overnight.

> Selling it for profit seemed obvious but there was a problem. Because the company used LIFO accounting, unloading that inventory would trigger a hefty tax bill of nearly 50%.

> Instead of taking that hit, Rockwood structured a clever workaround. They offered shareholders the option to tender their shares in exchange for cocoa 80 pounds per share. Under the tax laws at the time, this avoided the heavy taxation tied to selling inventory directly.

> 25 year old Buffett who was working with Graham Newman Corp. quickly realized the arbitrage. Shares were trading around $34, while the cocoa received in exchange was worth about $36.

> The young investor's job at the hedge fund was to scour the market for undervalued opportunities - the type of stocks that met Graham's deep value criteria.

> Buffett bought 222 shares for his own account. He held on till the stock hit $100 a share, producing a profit of $14,000 on the investment.

> He repeatedly executed the trade buying shares, redeeming them for cocoa, and selling the cocoa, cycling capital rapidly. As he later recalled, the margins were attractive, and the only real cost was his subway fare.

Young Buffett made money in totally different manner 🔥

Thread on Berkshire’s acquisition record…

I’ve always been fascinated by $BRK acquisitions of entire companies, mostly because it’s a lot harder to judge performance than it is for stock market investments. It’s a lot easier to do a case study on Berkshire’s purchases of Coke, Gillette, Washington Post, AmEx, etc. because most everything you need to determine returns valuations are public.

Some years ago I started trying to analyze Berkshire’s wholly owned acquisitions for lessons learned by doing rough estimates on deal prices, revenue, PTI at acquisition (a lot of this information is actually public), estimating financials today (which by reconciling segment information in the annual report, I think is possible to come out with pretty reasonable estimate) and coming up with some rough number for how much of net income over the years was distributed back up to Berkshire – you can actually come up with some very realistic and fairly precise estimates for modified IRR, essentially the same annualized return they’d get had these been public company investments.

Thought I’d share a few of the things I’ve noticed and collected. This is probably a strange thread, but I really don’t promote anything, don’t have a Substack and thought at least some people would find this fascinating. I’ll just emphasize for the record something that’s obvious – I think these numbers are directionally pretty correct, but they are just my estimates and don’t want to make the mistake of implying any false precision.

Here’s the paradox I’m thinking of.

When commodity traders or analysts fire off countless warnings, most ppl bash them for exaggerating everything just to get some attention for once.

But that’s not it. They’re just doing their jobs. In fact by doing what they do, they actually help keep us from slamming into a brick wall.

When everyone knows a disaster is waiting at the end and it becomes the consensus, stakeholders and ppl with good intentions will put in the effort to stop it before we get there.

The louder the warnings ring out and the more ppl get on board, the more hands will reach out to try and slow things down—or even stop them entirely.

If we actually end up avoiding the disaster, all you’ll hear is, "See? Those oil traders were just full of crap," but hey what can you do? lol

I can't speak for everyone, but even most oil bulls—excluding the traders who are all in on the prompt—don't actually want to see prices spike too aggressively.

Since many of them own energy stocks, they’d prefer to sit in the sweet spot for a long time, and they know prices nobody ever imagined will only trigger a massive backlash.

But as the "nothing’s gonna happen" chant gets louder and prices stall making ppl think "this is manageable," the incentive to actually solve the root of the conflict just fades away.

Don't dismiss or mock the warning voices so lightly. The more those voices are muffled the more dangerous it gets. Once we actually hit the wall, it’ll be too late to regret it.

That’s the paradox.

#oott #iran