Good morning. Woke up to $1 now equals 18.100 rupiah. Pertamax has risen from Rp12.300 to Rp16.250, and 5kg rice from Rp75.000 to Rp90.000. If you see nothing wrong with Indonesia's current fucked-up situation, you're either a nepo baby or braindead assholes who voted for 02.

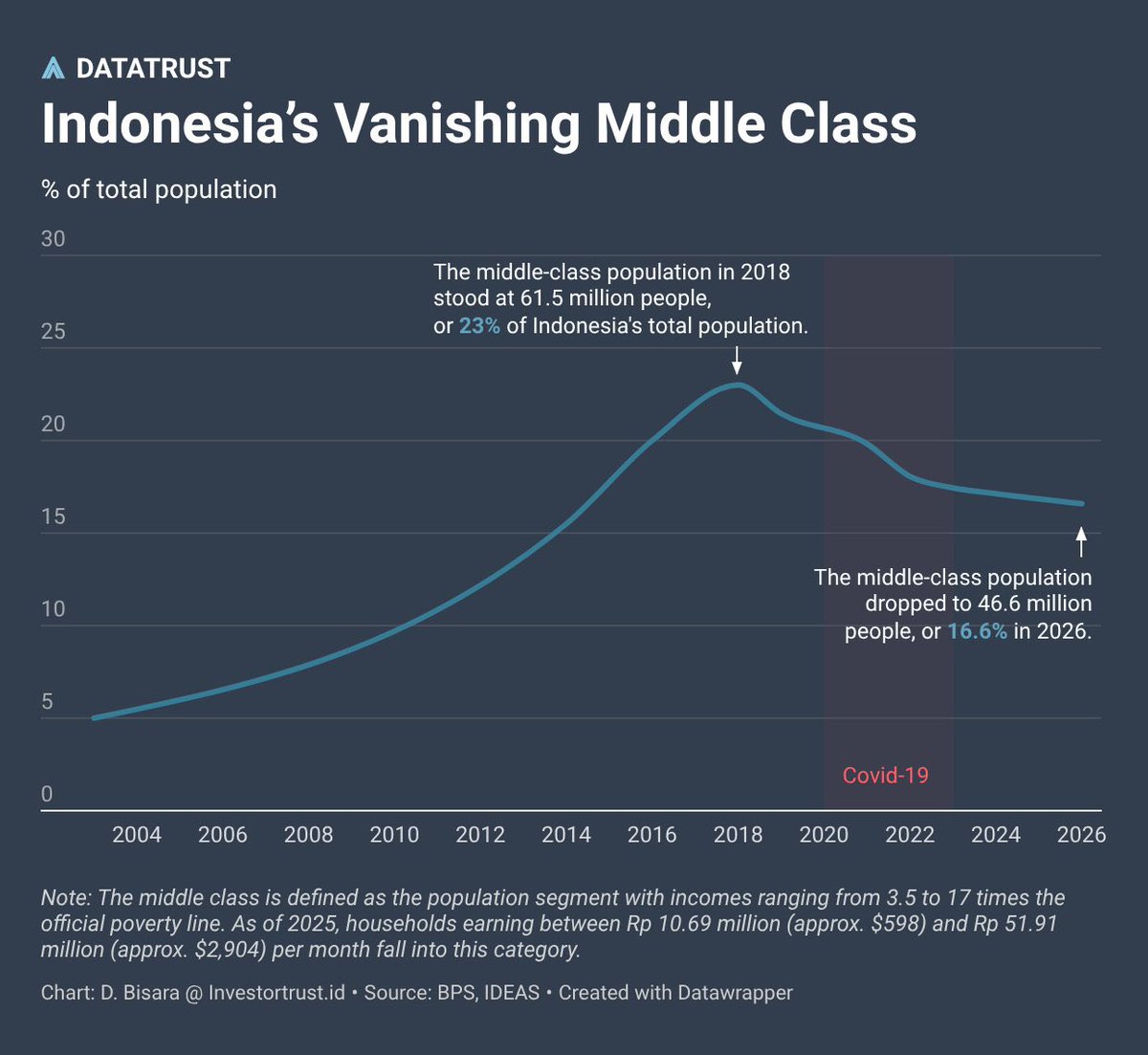

This chart should terrify policymakers. Indonesia’s middle class did not merely slow down. It went into reverse.

After two decades of expansion, the middle-class population peaked at 61.5 million people in 2018, representing 23% of the population. By 2026, that figure had fallen to just 46.6 million people, or 16.6%. That is not a cyclical slowdown. That is structural deterioration.

For years, policymakers celebrated GDP growth, infrastructure projects, commodity booms, and headline investment numbers. But the ultimate scorecard of an economy is whether ordinary people become wealthier over time. This chart suggests millions of Indonesians are moving in the opposite direction.

The middle class is the economic engine of every successful country. They buy homes, cars, insurance, consumer goods, education, travel, financial products, and healthcare. They generate tax revenue. They create small businesses. They drive domestic demand. When the middle class shrinks, the economy loses its most important customer.

The uncomfortable question is simple: where did the gains go? If GDP is growing, if conglomerates continue expanding, if commodity exports remain large, then why are fewer Indonesians qualifying as middle class than eight years ago?

More importantly, if you are born poor in Indonesia today, what ladder exactly are you supposed to climb?

If you are exceptionally good looking, perhaps you can monetize attention through social media. If you are academically gifted, perhaps you can break into an ultra-competitive institution like MBB, survive years of brutal expectations, and eventually use that platform to do something bigger. If you are entrepreneurial, maybe you build a business against overwhelming odds. If you are lucky, perhaps you benefit from family connections, inheritance, or access to opportunities unavailable to most people.

But an economy cannot rely on exceptionalism. A healthy economy creates millions of pathways upward, not a handful of lottery tickets.

The situation becomes even more concerning when you consider that well-paying white-collar jobs are becoming increasingly scarce. Many multinational companies that once established regional operations, technology centers, shared-service hubs, and professional offices in Indonesia have either downsized, relocated, or shifted future expansion elsewhere.

Those jobs were not valuable merely because of the salaries they paid. They were valuable because they transferred knowledge, management expertise, technical skills, global best practices, and professional networks into the local workforce. Over time, they helped develop intellectual capital that could later be recycled into entrepreneurship, leadership positions, startups, and domestic businesses.

When those opportunities disappear, the loss is not limited to employment. The country also loses a training ground for future managers, engineers, consultants, analysts, and business leaders. Human capital compounds just like financial capital. Once that pipeline weakens, rebuilding it can take years or even decades.

The bigger risk is that social mobility slows. When people stop believing hard work leads to a better life, trust in institutions weakens. Aspirations decline. Consumption slows. Talent leaves. The country’s most productive people increasingly look elsewhere for opportunity.

This is why Indonesia’s biggest economic challenge is no longer growth. It is upward mobility. A country cannot thrive without a growing middle class, a steady pipeline of high-quality jobs, and a clear path for ordinary people to join it. And right now, all three appear to be moving in the wrong direction.

@daryono_eq_talk Betul tweetnya memang edukatif dan saya banyak belajar juga dari situ. Tapi hari ini mulai banyak perempuan yg speak up (cek reply tweet ini). Sbg sesama perempuan, lebih baik tidak saya ikuti akunnya :)

Sebelumnya aku juga ngefollow si Georitmus itu karena akunnya informatif soal pembacaan cuaca sama bencana alam. Tapi sejak banyak perempuan ngeluhin interaksi yg ga nyaman, aku unfollow aja. Masih ada @daryono_eq_talk yg worth to follow untuk topik yg sama

gue s1 di malay temen-temen di sana kaget krn kita yg dr indo pd umur 17-18…mereka soalnya s1 br di umur 20-21an, bahkan ada yg 24 ngulang lg krn pindah jurusan.

Asal fafifu, fearmongering, ngomong waswiswus negatif di situasi saat ini emang aman 😀.

Saya ngomong spesifik soal fakta soal berita yg dikutip yg bermula di Bloomberg ini. Fact checking.

Tentang jargon "Sell Indonesia" yg "digoreng."

Bukan soal saham Indonesia. Tapi soal narasi "Indonesia."

Tentang 1 orang yg dikutip & mengatakan "‘Sell Indonesia’ Sweeps Trading Desks." Yg mohon maaf sama aja dengan random akun di medsos ngomong soal "info A1", "menurut teman saya", dari kata "orang di lembaga x."

Kemudian berikutnya, narasi kredibilitas narsum agar berita atau ucapan di atas dibeli/kredibel. Dengan "oversee 4.3 bio." Saya cek ke info di terminal Bloomberg mengenai narsum dan lembaga dia.

"Gak tau aja", di pasar keuangan itu simetris.

There's a buy for every sale.

Emang jual terus dananya menguap begitu saja? Kan ada yg beli?

Bapak ini kan sepertinya mungkin lebih ahli dan paham soal hal di atas. Dan ngomong juga di bawah soal "Tetep Sell Indonesia."

Please dong berikan pencerahan buat kami-kami ini 🙏

Valuation-wise, Indonesia is arguably one of the cheapest equity markets in Asia today. Many well-known blue-chip companies are trading at what can only be described as crisis-like multiples despite maintaining healthy balance sheets, dominant market positions, and attractive dividend yields.

BBCA trades at roughly 11x forward earnings and 2.6x book value. Bank Mandiri trades at around 6x forward earnings and 1.2x book value. BRI trades at approximately 7x forward earnings and 1.3x book value. Astra sits at 6x forward earnings. Kalbe trades at 9x forward earnings. Amman trades at roughly 10x forward earnings. The list goes on.

Many of these companies also offer high single-digit dividend yields, with some names approaching double-digit yields. On paper, this should attract significant investor interest. Yet share prices continue to drift lower.

The obvious question is: where are the buyers? Where are all the investors who have spent years believing Indonesia’s long-term potential? Indonesia’s weight in MSCI Emerging Markets remains only around 0.5-0.6%, remarkably small relative to the size of its economy, population, and long-term growth aspirations.

More importantly, where is Danantara? It was presented as a potential new source of domestic capital and a stabilizing force for Indonesian financial markets. If the local market is trading at distressed valuations, this should be the type of environment where a large domestic institutional investor helps establish confidence.

The problem, however, is that cheap valuation alone is rarely enough. Markets ultimately pay for growth.

Indonesia’s core challenge today is not valuation. It is earnings growth. Aggregate earnings growth for the market has slowed materially, with many sectors struggling to generate meaningful expansion. Compare that with South Korea and Taiwan, where investors are being offered direct exposure to AI, semiconductors, advanced manufacturing, memory, and high-performance computing. Foreign investors are naturally willing to pay higher multiples for companies whose earnings are compounding rapidly.

Currency concerns add another layer of complexity. Investors are not simply underwriting Indonesian corporate earnings. They are also underwriting the rupiah. If currency depreciation continues to offset equity returns, valuation discounts can persist far longer than expected.

There is also a credibility issue that should not be ignored. For years, many foreign investors have complained that parts of the Indonesian market function primarily as distribution channels rather than genuine capital formation venues. Domestic equity sales teams routinely promote names that later become exit liquidity for local institutions seeking to reduce exposure. Over time, repeated experiences like this erode trust.

The persistent allegations of wash trading, questions around effective free float, concentrated ownership structures, and concerns over genuine liquidity have further damaged confidence. Investors do not simply buy low valuations. They buy governance, transparency, liquidity, and confidence in future earnings.

This is why cheap markets can remain cheap for years. A stock trading at 6x earnings can still fall to 5x. Valuation itself is not a catalyst.

The harsh reality is that Indonesia does not have a valuation problem. It has a growth and confidence problem.

Until investors see stronger earnings growth, more credible policy execution, better market governance, improved liquidity, and a clearer path for capital to generate attractive real returns, low multiples alone will not be enough to attract meaningful foreign capital back into the market.

Cheap without growth is a value trap. Cheap with deteriorating confidence is even worse.

@kun6manuk Haha, setuju. Kemarin juga ikut nanggepin tweet lain tentang ini yg framingnya negatif padahal yg kyk gitu sih lebih gampang nyari irisannya😅

@gwsyababi@trickyinvestor Gimana kalo ga butuh orang lain itu maksud sebenernya ga butuh orang yg ga kompeten. Ga mau memahami orang yg dasarannya ga make sense.

Kadang orang yg berusaha menghargai diri sendiri itu dipandang self-centered oleh orang lain sih (pengalaman)

if you're a performance marketer, here's how I use a custom Claude Cowork plugin to manage Google Ads at @AnthropicAI. it connects to the Google Ads API via MCP, encodes my common paid search workflows into skills, and works on desktop and Dispatch.