OpenAI and Anthropic are effectively telling the market they can't solve every problem with a generic AI coworker.

You don't pour billions into massive forward-deployed joint ventures if you think the next model release is going to take care of it.

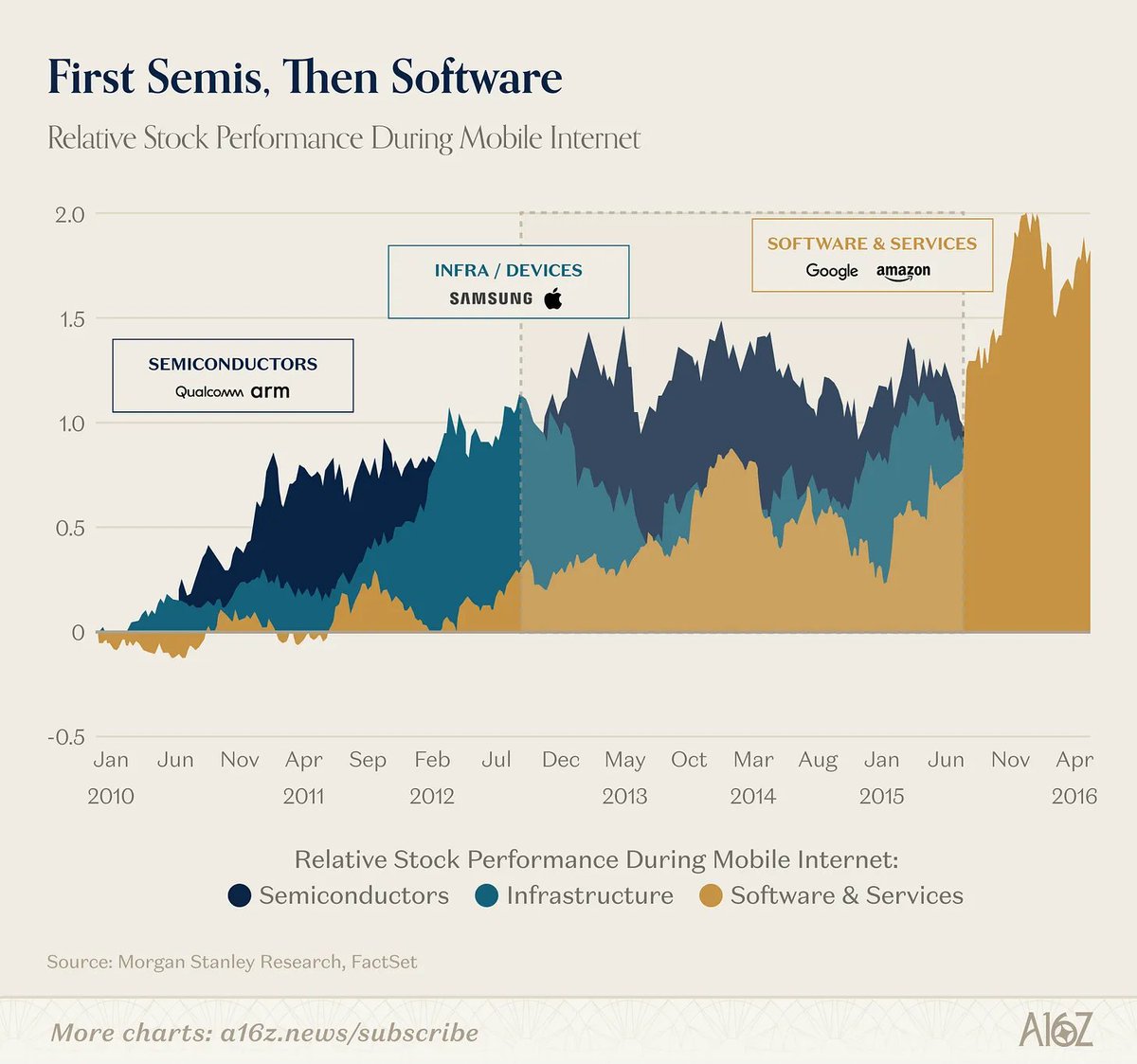

In the cloud supercycle, semis led and software followed (and you didn't need Qualcomm or ARM to tell you the value was migrating up the stack).

In AI, the infra layer itself is telling us the application layer is a separate, massive opportunity they can't fully capture.

a16z's @joeschmidtiv on why the app layer isn't dead: https://t.co/84QN5Mj9T3

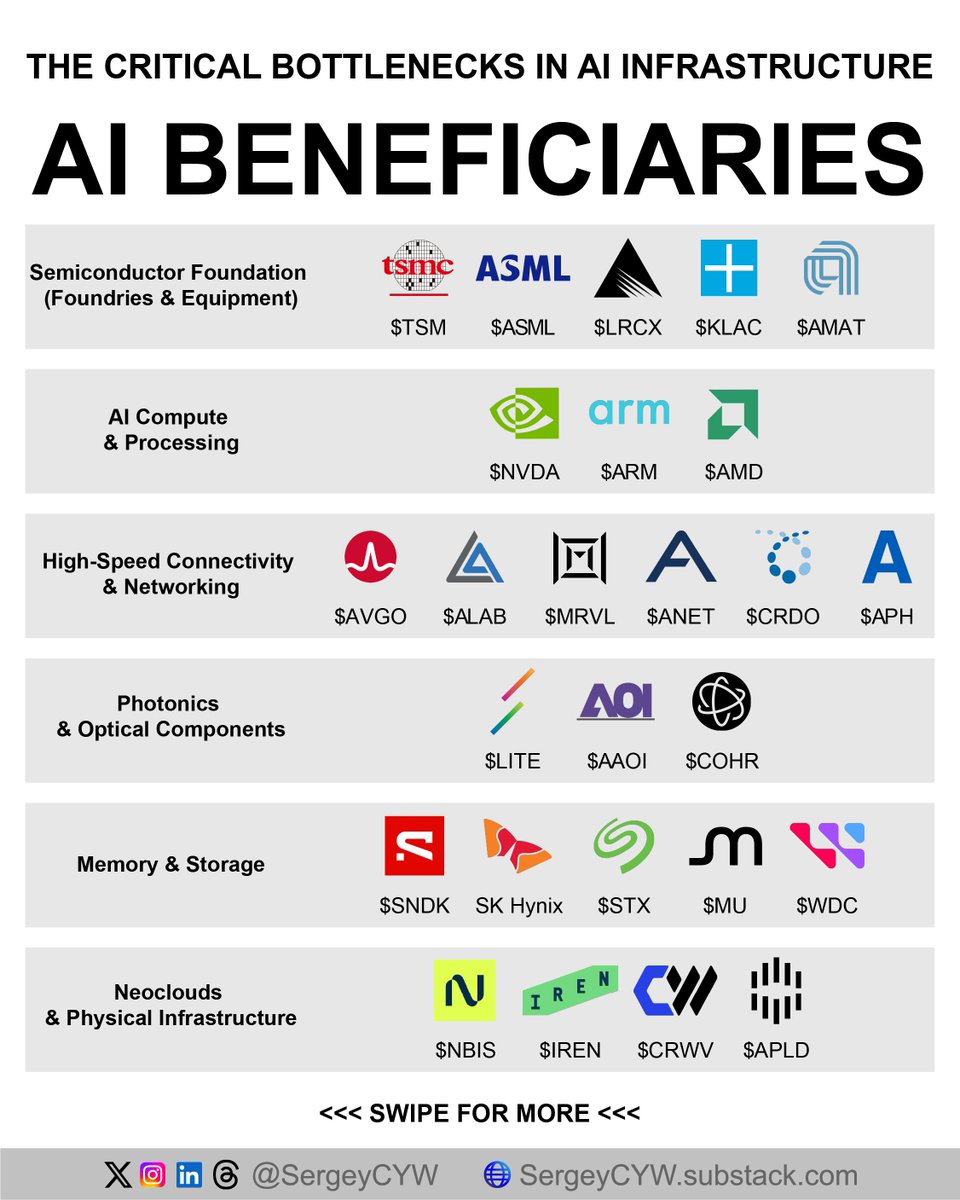

The network layer is starting to find its footing in the AI infrastructure stack as inference scales, helping explain the continued strength in names like $ANET, $ALAB, and $CRDO.

As hyperscalers push distributed training and inference workloads tied to the $100B deal between $AMZN and Anthropic, high-speed interconnect and custom silicon from $MRVL and $AVGO are becoming critical parts of the scaling equation.

That shift is turning networking into a structural tailwind rather than a supporting layer as AI clusters expand beyond single-node compute into full-fabric infrastructure.

Credit to @SergeyCYW for the image

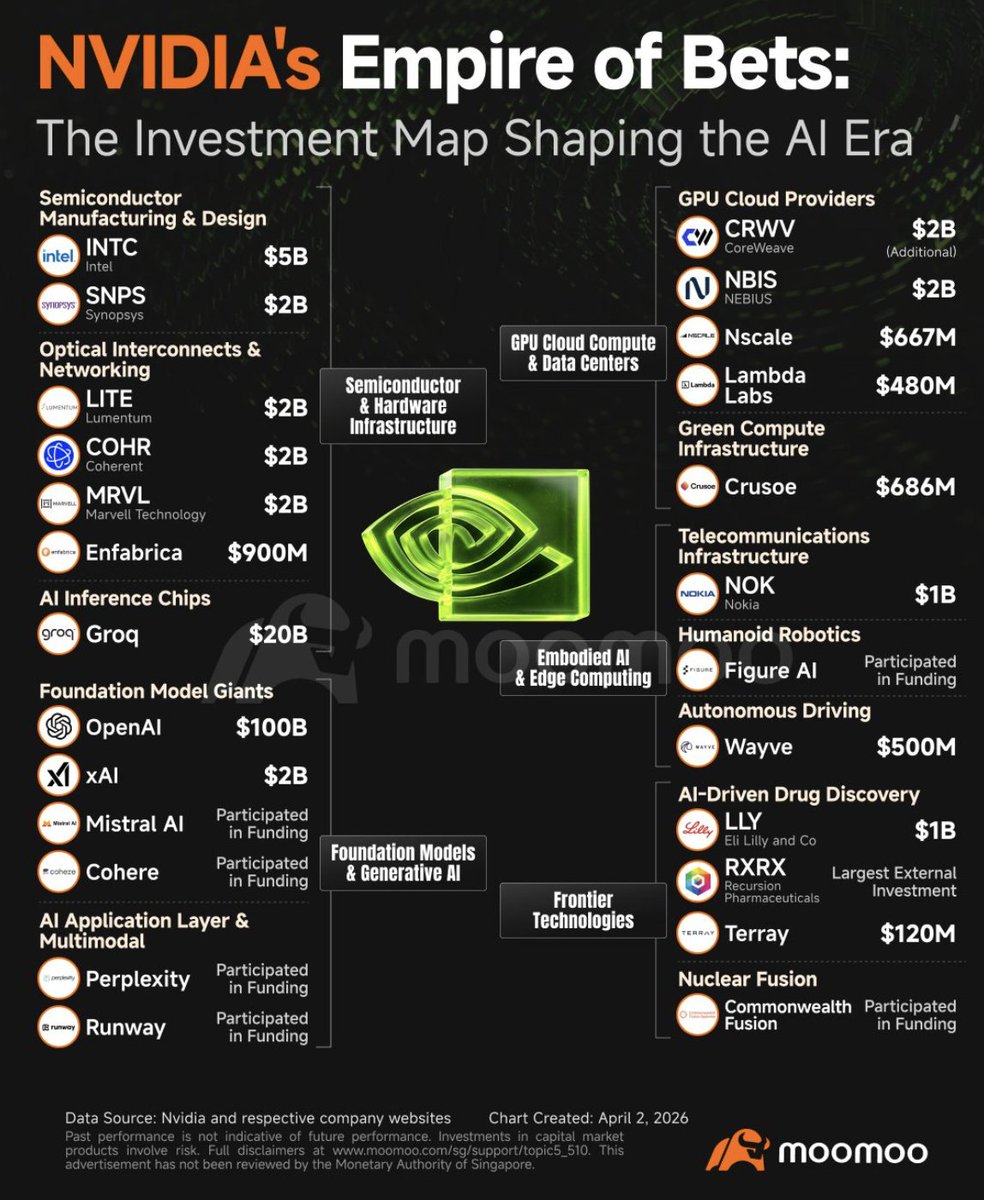

$NVDA is building an AI empire across the stack, and the investments tell the story.

You’ve got names like $INTC and $SNPS on the semiconductor side, $LITE, $COHR, and $MRVL in optical and networking, $CRWV in GPU cloud, $NOK in telecom infrastructure, and even $LLY and $RXRX in AI-driven drug discovery.

That’s what makes this bigger than one product cycle.

Nvidia isn’t just selling picks and shovels. It’s buying exposure to the roads, rails, and power grid around the AI gold rush.

That’s how real leaders extend.

They stop acting like a company with one product and start acting like a platform with stakes in the whole ecosystem.

Robotics is quietly becoming one of the most important technology shifts of the next decade.

The companies on this chart span the entire ecosystem:

Automation leaders like $ROK, $ZBRA, and $CGNX

AI and chip infrastructure like $NVDA and $QCOM

Logistics automation from $AMZN and $SYM

Surgical robotics from $ISRG and $SYK

Defense robotics from $AVAV, $KTOS, and $LMT.

It's not one industry, it's an entire stack.

Best case scenario:

Robotics drives a productivity boom. Factories become more efficient, warehouses run faster, surgeries become more precise, and dangerous jobs move from humans to machines. Companies that build the hardware, software, and infrastructure behind it could see massive demand for years.

Worst case scenario:

The transition gets messy. Rapid automation displaces large parts of the workforce, geopolitical tensions push robotics toward military applications, and supply chains become even more dependent on a small group of technology providers.

Either way, robotics is moving from science fiction to economic reality. The only real question now is how fast the world adopts it.

$TSLA $MSFT $META report tomorrow.

Everyone's watching AI numbers. Almost no one's watching the 15 year DXY 💸 trendline that just broke.

Weaker $USD means foreign revenue is worth more when converted back & these companies get 40-50% of revenue overseas.

Double tailwinds most aren't pricing in. Full breakdown below

https://t.co/wKNiXOuKaz

About 30% of people are naturally "night owls," a preference known as a chronotype, which is largely genetic and is not due to a lack of discipline.

Forcing a night owl to adhere to an early schedule can lead to chronic sleep deprivation and associated health problems.