Sold over $450m on Amazon FBA. Helping Amazon Sellers with SmartScout, a tool for understanding Amazon (and making money!). I interview hundreds of Amazon Pros.

This is an interview we’ve been waiting to get for a while! We got the man himself, @itsScottNeedham. If you don’t know Scott, he’s done over 400M in sales on Amazon lifetime and founded SmartScout. We went to their offices and filmed an in person interview with Scott. This one is filled with tons of value. Listen in!

What Happens When You Take Amazon to Arbitration?

If you’ve ever dealt with account issues, this is a side of Amazon most sellers never see.

👉 Watch the full episode to get the complete breakdown and real insights from someone who’s been in the middle of these cases.

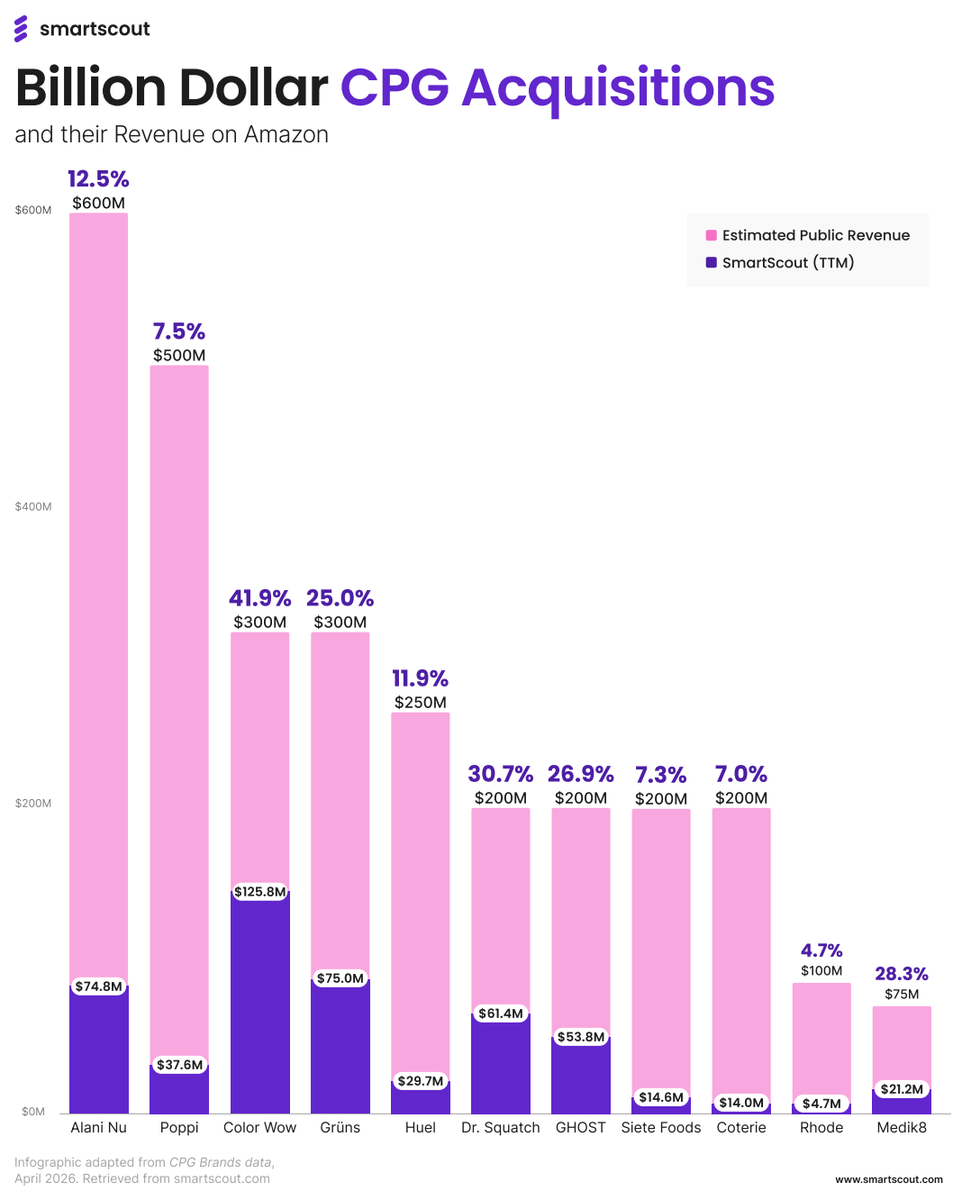

Billion Dollar CPG Acquisitions and their Revenue on Amazon

If you're building a CPG brand today, the real question isn’t

“Should I be on Amazon?”

It’s:

“What role is Amazon playing in my exit story?”

Amazon doesn’t rank products randomly.

There’s a system behind what shows up first—and once you understand it, everything changes.

Check out the full conversation with Yonah Nimmer: https://t.co/mIzzuC0nFD

#Amazon#AmazonFBA#AmazonSeller#ecommerce#ecommercebusiness

While Creatine is growing at an 85% annual growth rate, women's and gummy creatines are pushing 300%.

So if you're a gummy creatine brand and you're only growing 200%.... you're losing.

"What was the best-selling candy bar in 1962?

Snickers.

"And do you know what the best-selling candy bar is today?"

"Snickers."

-Warren Buffett

Nothing has eroded legacy chocolate brands.

Another callout. Feastables is only at $2m.

Meltable products have a revenue slump every summer.

Revenue is down 25% from April-May versus June - August.

This date range excludes Halloween and Valentines holidays.

If you're in meltables, it's worth 10 minutes to check out AMZ Prep's report.

https://t.co/JgPHVTHVhN

etailz.

Avalanche.

Pharmapacks.

ToysNGamesETC.

BuyBoxer.

Quiverr.

If you sold on Amazon in the 2010s, you know these names.

They were everywhere. These were the top Amazon Sellers in the world.

I started selling full-time for BuyBoxer in 2013.

We were the new guys on the block.

And we looked up to the giants.

ToysNGamesETC and Think Fast dominated the toy category.

Pharmapacks owned health & household.

etailz had scale across dozens of categories.

Quiverr was in Beauty.

Eventually, we caught up, and BuyBoxer had over 100k ASINs active in FBA.

Open a random ASIN, and odds were one of these sellers was in the Buy Box.

Back then, the game was clear:

Win wholesale accounts

Build distributor relationships

Add massive catalogs

Compete on repricing

Scale operational efficiency

Each of these had its own story and made mistakes in different ways. Sometimes I even saw them make mistakes in real time.

Etailz (rebranded as Kaspien), bought deep against Amazon Retail and we could tell were lighting cash on fire.

Avalance (Formerly Think Fast) took on investors and became top-heavy for the actual profits.

BuyBoxer got wrecked by the 2021 FBA limits and fee changes

Pharmapacks couldn't get the scaled FBM model to work.

Quiverr didn't hit all the promises and was eventually acquired by Recom

Today we see other players. Somewhere in your mind, you see the large sellers like

Pattern

Spreetail

Recom

Luminize

These sellers seem really big now. Top of the charts. But in the 2010s, the aforementioned sellers were the big dogs. Many looked up to them. I saw the CEO of Think Fast get mobbed in Seattle by other sellers who wanted to learn from him.

Honorable mention:

Netrush is still crushing and prioritizing helping other brands

Big Fly is still doing well

Juvo+ pivoted to private label and then some brand aggregation

"That's like CamelCamelCamel but for Amazon Sellers"

I was on a call, looking at our Pricing Intelligence Tool, when I heard that.

High Praise.

Because CamelCamelCamel is a legend in the price tracking industry. Before any Amazon software tool existed, CamelCamelCamel tracked price history.

Look at the screenshot below, and you can see 4 gummy creatine products fighting it out.

We can see that Create is the only one keeping the price steady. The challenger brands are putting in subscribe-and-save coupons and lightning deals, and doing just about anything to get a few extra sales.

On top of seeing these, there's also an overlay to see how the market share of these products is shifting. You only want to make pricing decisions that can help win market share.

This is helpful when you've got tough questions like:

Should we do something for Prime Day?

Should we test out a coupon?

How is pricing impacting market share?

So if you're considering what to do for Prime Day, or if you or should run a coupon code. It's helpful to see the big picture of how this is all put together.

Our data shows that just having a coupon badge increases click-through by 5%. That's worth considering if you're in growth mode and you see Amazon as a brand growth vehicle.

Amazon just shut the door on review scraping.

A lot of tools built on HTML parsing are about to break, or already have.

But review intelligence isn’t dead. It’s evolving.

With Amazon's update to Business Solutions Agreement. Giving review insights and sentiment analysis can't be done the old way.

Enter SmartScout Sentiment Analysis.

In our Chrome Extension and application, every ASIN you're able to see specific sentiments and how often they occur. This is done in a compliant way that isn't about to disappear through a new Amazon update.

Take for example, Grüns here.

Some people like the taste, others don't. Knowing the mix of people that are commenting on the features and how positive and negative they see it is key in product development.

You can also call out these features in your content and confirm what people love about your product.

We're excited to be able to give insights from reviews with specific call outs. Let me know what you think!

We pulled the data on the Top 10 Amazon Brands Launched Since 2021.

These brands haven't been around long, but have completely taken over some categories. Aside from half of them being based out of China, there's no consistent category.

Here they are:

DREO – $331.9M (Launched March 14, 2021)

Sweetcrispy – $197.6M (Launched August 1, 2022)

ŌURA – $184.4M (Launched January 19, 2024)

Trendy Queen – $176.9M (Launched August 26, 2021)

Clean Nutraceuticals – $156.3M (Launched May 5, 2021)

Project Cloud – $154.7M (Launched January 24, 2023)

Wavytalk – $112.2M (Launched August 12, 2021)

Nutra Harmony – $103.8M (Launched April 6, 2022)

MERACH – $102.7M (Launched March 23, 2022)

LCOVR – $71.3M (Launched June 13, 2024)

A few things stand out:

• Multiple brands crossed $100M+ in under 3 years.

• Hard goods continue to scale faster than most people expect.

• The speed of brand creation on Amazon is accelerating for the right brands.

I get to be lucky to see brands start and scale in the data every day. One thing that is clear, if you have product market fit... Amazon will give you all the demand you could ask for.

There are 7,845 million dollar subcategories on Amazon.

Inside each of those subcategories are trends.

Let's call them micro trends.

But sometimes, they are anything but micro.

Let's look at the multivitamins subcategory. Here are trends that pop out inside this subcategory.

1. Peptide & Biohacking Crossover Is Exploding

ghk-cu → 274,668 searches (+3,872%)

ghk-cu peptide → 437,652 searches (+5,152%)

copper peptides → 301,589 searches (+2,851%)

This is:

• Anti-aging

• Regenerative optimization

• Skin + hair biohacking

2. Hormone & Stress-Focused Supplements Are Surging

cortisol supplements for women → 663,554 searches (+493%)

saffron for kids → 234,967 searches (+3,383%)

They’re searching:

• Stress

• Mood

• Hormones

• Emotional regulation

3. Brand-Led Search Is Growing

Rainbow Light Women’s One Multivitamin → +185.73%

Rainbow Light Men’s One Multivitamin → +155.27%

Mary Ruth Hair Growth Max → +309.11%

Olly Women’s Multivitamin → +191.12%

Primal Multivitamin → +217.62%

Today we launched the ability to see trends inside of any subcategory on SmartScout. Don't just see the keywords, see what's popping out. Because some of these million dollar subcategories are actually fragmented into micro trends. Tapping into them can help capture more of the market.

Top 10 Chinese Sellers that have changed countries!

CONTEXT

Over the past few years, something interesting has been happening. A growing number of Chinese Amazon sellers are no longer listed as being based in China.

Their country of record now shows:

• Hong Kong

• Singapore

• U.S. LLCs

This isn’t random. It’s strategic. Here are the top 3 reasons they’re changing their country of record:

1) Platform Risk & Enforcement Arbitrage

China’s new rules require platforms like Amazon to disclose seller revenue data, empowering tax authorities to audit and enforce compliance.

Being labeled “China-based” now comes with real regulatory visibility and risk:

• Higher enforcement scrutiny

• Pressure to reconcile revenue with tax filings

• Potential back taxes and penalties

By switching their jurisdiction (Hong Kong, Singapore, UAE, or U.S. LLCs), sellers try to move outside the direct scope of this reporting regime.

2. Conversion & Brand Perception

Let’s be honest.

“Based in California” converts better than “Based in Shenzhen.” If changing your country of record increases CVR by even 1–2%, that’s meaningful leverage at scale.

Perception = margin.

3. Capital, Banking & Structural Flexibility

Mainland entities deal with:

• Currency controls

• Harder USD access

• More complex capital flows

Offshore structures (HK, Singapore, etc.) allow:

• Easier USD settlement

• Cleaner investor structures

• Better access to global payment processors

• More flexibility around trade routing

The big takeaway:

The most sophisticated Chinese sellers no longer compete as “foreign sellers.”

They compete as invisible global operators.

With the advent of AI helping them seem less Chinese, this is the final step in shedding their Chinese roots and are now some of the largest global Amazon sellers.

In 3 of the 5 global regions, Amazon ranks first.

Here are five things that strike me with this data:

1. Amazon has a stranglehold over the EU. No one is matching their size.

2. Walmart's ecommerce business is actually competitive in the US. Yes, they're second fiddle. But they're not a long shot.

3. Shein/Temu/AliExpress are in every region. Bargain shoppers drive volume.

4. Apple's online commerce is so big, it makes it onto this list. They're the only branded site to make it here.

5. I have no idea what's going on in China, but it looks extremely active and competitive.

This dataset from ECDB provides valuable context on how to participate in each region. This reaffirms that an Amazon international rollout strategy is more than sufficient to get in front of new customers. Less complexity by dealing with the devil we know.

What do you think?

The Amazon Marketplace has changed, and it's never going back to the way things were.

Revenue is up.

New sellers are down.

And most of the money is flowing to fewer, bigger players.

We dug into the data, the shifts, and the uncomfortable truth about what it actually takes to win on Amazon now.

🎥 The video is live now.

I'm a top 10 seller and run an Amazon data company. I'm telling you that you don't want to miss this if you're in the Amazon space.

Check it out: https://t.co/kYcuuLs61I