Homeownership 101

1⃣Your monthly mortgage payment should not exceed 30% of your income.

If you earn Ksh 100,000 per month, your mortgage payment should be Ksh 30,000 or less.

2⃣The total home value should not exceed three times your annual income.

If your annual income is Ksh 1.2 million, aim for a home worth no more than Ksh 3.6 million.

Live in a home you can comfortably afford.

Model Budget Breakdown for a Net Income of Ksh 70,000

Net Income = Ksh 70,000

➡ Bucket 1 = Ksh 14,000 (Savings)

Eg. MMF – 7,000, Stocks – 5,000, Sacco/Retirement Fund – 2,000

Always pay yourself first. Automate this if possible.

➡ Bucket 2 = Ksh 35,000 (Expenses)

Eg. Rent – 15,000, Food – 10,000, Transport – 4,000, Utilities – 3,000, Insurance – 3,000

These are your essentials—costs you must cover to live and work comfortably. Aim to keep them under 50% of your income.

➡ Bucket 3 = Ksh 21,000 (Wants)

Eg. Entertainment – 6,000, Personal shopping – 5,000, Family outings – 5,000, Subscriptions & hobbies – 5,000

These are flexible and can be adjusted depending on your financial goals.

It is wise to track every shilling for at least 3 months. You’ll quickly see where your money leaks and where you can save more.

One more thing, any unspent amount or extra income should go straight into your savings or investments.

Typical stages of financial wellness:

1. Stability

Bills are paid, savings are funded, little/no debt.

2. Soaring

2-3 income sources, money works for you.

3. Security

Frequent travel, eat good food, enjoying your money.

4. Freedom

Money is not an issue, high living standards.

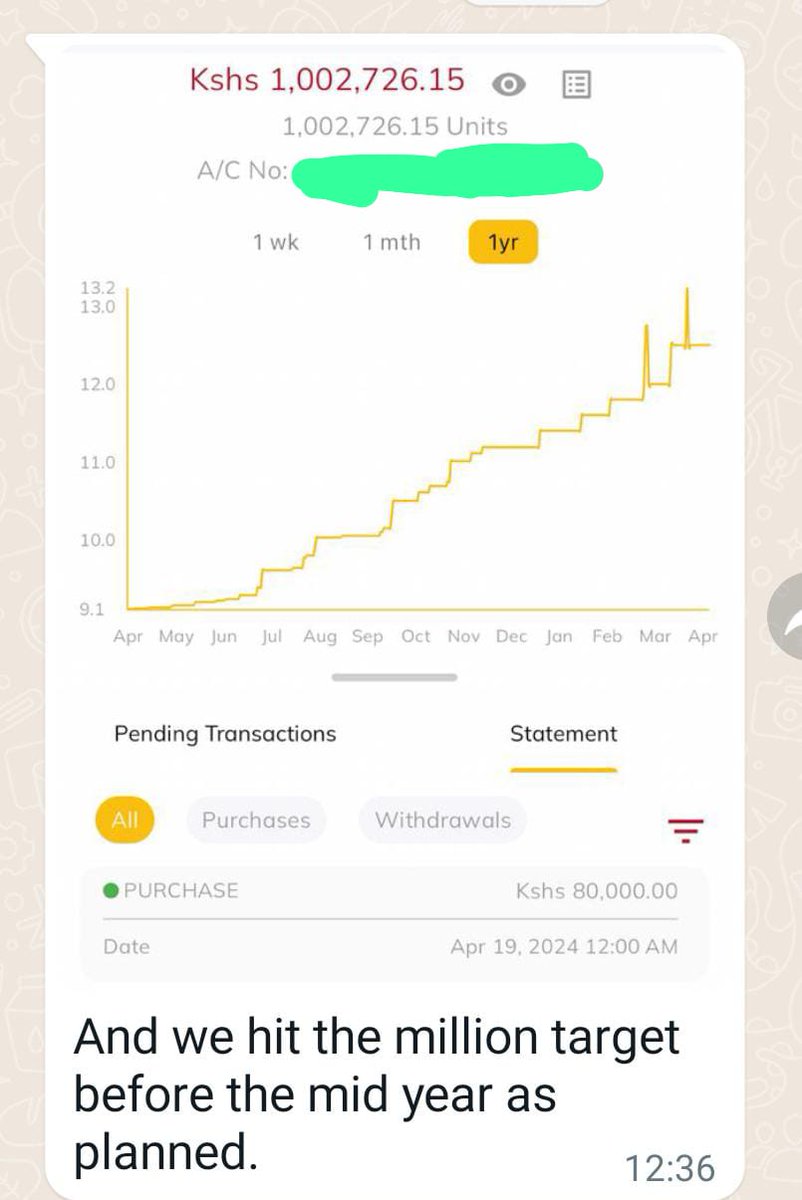

Your first Sh 100K invested in the stock market is the hardest. Hitting Sh 250K comes significantly faster.

Then Sh 500K, then Sh 1M in a portfolio comprising stocks, SACCO deposits, MMF, and bonds.

Smashing that Sh 10M mark someday is a reality.

No matter where you are in your financial journey, keep at it.

It's a rollercoaster of dividends and interests at each milestone.

If you are planning to build a house in your rural village,

Do the following:

• Open a bank account. Call it "Project Development Account 2026."

• Write a plan. Use the Triple Constraint Theory in Project Management: BUDGET, TIME and SCOPE.

• Save 50% equivalent of your rent in the account, monthly for 15 months, eg, if your rent is 10,000, then, save 5,000 in that account every month.

• If you can't raise 50% equivalent of your rent to save, then you are living beyond your means. Look for a cheaper house.

• Get an architect and a draughtsman to design a house.

• Do research, consult, read about building and construction online. Travel beyond your comfort.

• Get a Quantity Surveyor to do feasibility and the cost of the project.

• At month 15, draw a budget and begin buying material for construction, eg Sand, Ballast, Stones and timber. Stick to the budget.

• At month 18, start building.

• Get a professional mason licensed by the National Construction Authority. Be present. Supervision by phone calls is disastrous.

• Be hands-on. Learn to do the masonry work alongside the mason. Mix the ballast. Lay the bricks. Be part of the team.

• Create a rapport and good relationship with a hardware. Let this hardware be the only place you will buy construction material.

• Don't live in government houses. Don't buy the so called "affordable houses."

Build your house, to your preference and taste.

Therefore, if you are intending to build, and you start planning today, then you should be building your house in 2026 March.

It is not far.

Start today.

Be patient.

Start.

#BetterTogether

PROCESS OF GETTING MOTOR INSURANCE IN KENYA

Save this for later.

1) Scout for a reputable Insurance Company:

Work with referrals from Friends.

They will guide you well.

Do not get Insurance through a relative or Family Member.

The Best insurance companies have been around for more than 20 years eg. GA, ICEA, CIC

2) Use brokers to get lower rates:

Brokers and Big Agents get low rates from Insurance companies as they have big business portfolios & can easily negotiate with Insurance companies

3) Provide the following by filling a proposal form:

* Logbook in your Name * National ID card *KRA pin *Mobile number * Physical address * Email address *Occupation * Source of Funds

If logbook is not in your name yet provide copy of sales agreement.

You should be issued with one month certificate which will be extended on the whole annual premium payable in instalments after you get logbook in your name.

4) Go for Valuation:

The market price is used by insurance companies to adjust claims so it is important to go for valuation within two days of policy issuance.

The buying price of a car is not its market price.

Once valuation is out have the insurance company rework the annual premium for you using the market value provided in the report and pay the balance from what you paid as first instalment.

Get all the important buy backs into your cover e.g Excess protector own damage & political violence & terrorism.

If you own thief magnets like Axio and Fielder kindly get excess protector on damage and theft.

Make sure the insurance company revises the value of your windshield and entertainment system to match the figures shown in the valuation report.

Pay for extra premium if the windshield and entertainment system values are above the policy free limits.

5) Demand the following after getting insurance certificate :

* Policy document with wording

* Payment Receipt

*KRA E-tims receipt.

6) Drive safely and avoid situations that may land you in accidents:

You have a duty of care not to drive carelessly just because you have insurance.

h/t @alasirimotors

Wealth can only be achieved if you invest in yourself and in financial assets to the extent that passive income exceeds what a job you qualify for can offer.

It means having the ability to do what you want, when you want, and how you want; without asking for permission.

• Sunk Cost Fallacy

You keep doing something because you've already spent time or money on it.

Like eating more dessert even when you're full because you paid for it.

— Sh479 million to support the accelerated electrical connection of more homes, businesses, and institutions

— Sh452 million to improve civil society engagement

—Sh5.28 billion from the US for democracy, human rights and governance programming

— Sh2.4 billion to build the Kenyan criminal justice system’s ability to address terrorism

— Sh2 billion for activities designed to reduce poverty and malnutrition