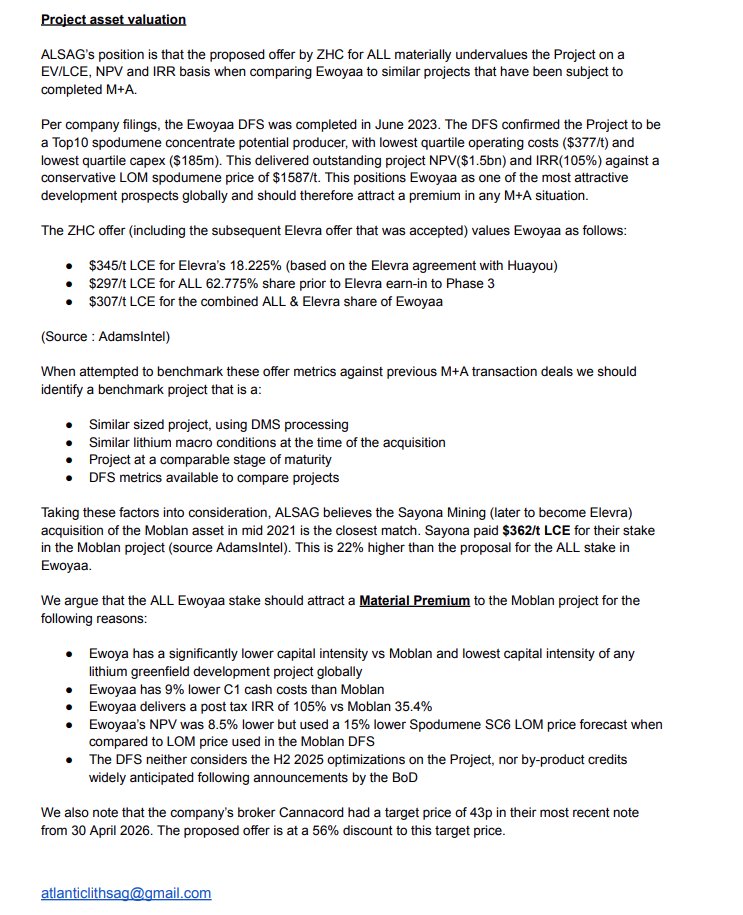

@Atlanticlithium shareholders are being asked to accept a 10.8% premium to hand over control of one of the lowest cost shovel ready #lithium development projects in the western hemisphere.

Some simple numbers cross referencing the valuation on ZHC take'under' proposal:

o ZHC paying $71m for $ELV 22.5% stake in Ewoyaa

o Values 100% of Ewoyaa at $315m

o #ALL $A11 own 58.5% of the project ($ELV 22.5%, MIIF 6%, Govt free carry 13%)

o => #ALL $A11 stake valued at $184m

o #ALL $A11 net cash of $13.9m at end last Q

o Assume $3.5m of cash burn/q til deal close at Y/E (no idea what they are spending this on!!!!)

o =>Y/E end cash ~$3.4m.

o ZHC offer at $210m, less $3.4m cash, less $184m for stake in Ewoyaa - implies ZHC paying $22.6m for change of control and exploration upside in Ghana and Cote d'Ivoire. All when SC6 is trading >$2000/tn and AISC is close to $700!!!

#ALL $A11 @AtlanticLithium are being taken for a ride

$sgml - nothing beats putting your money where your mouth is. @Anacabralgardn1@sigmalithium

'when you know you know!!!'

👏 👏 👏 🚀 📈

https://t.co/WH1G8PNKXp

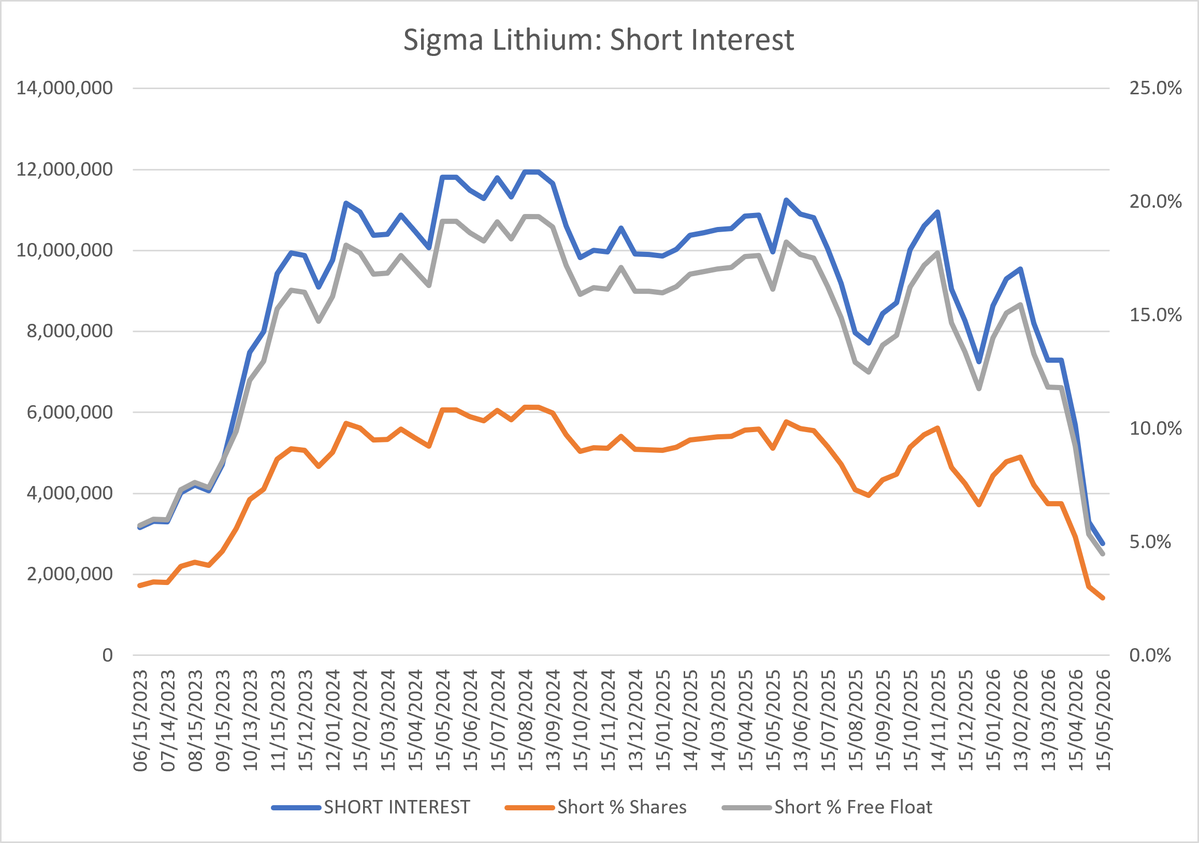

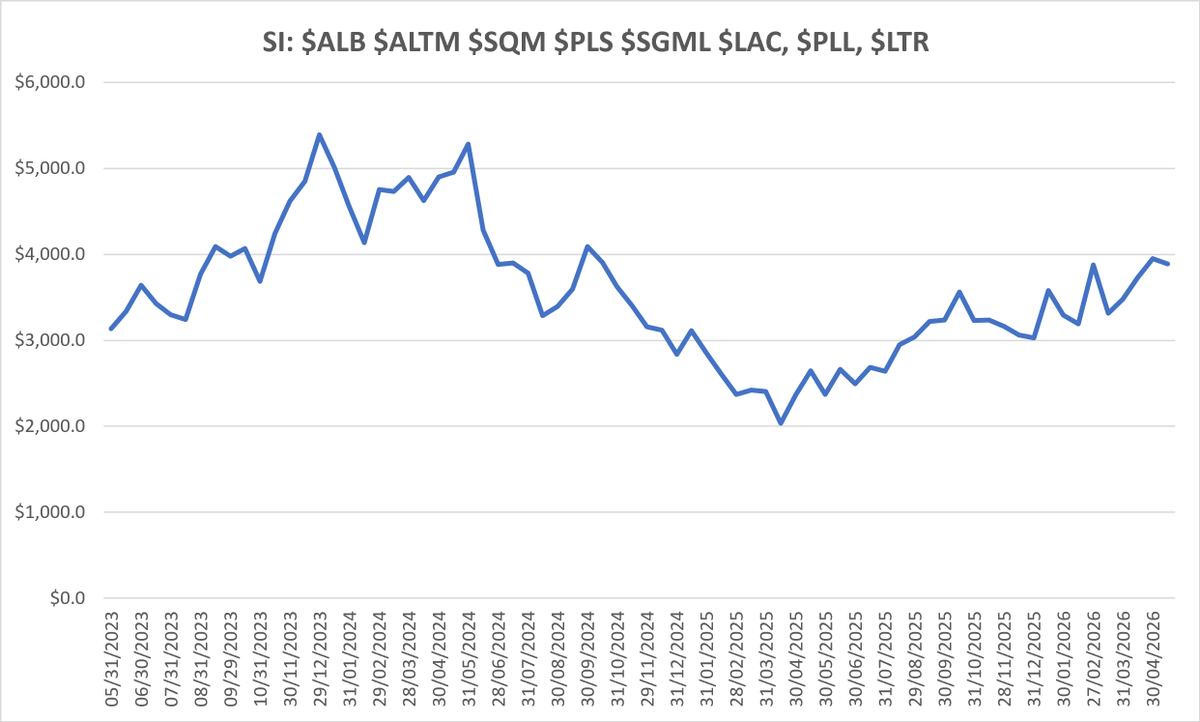

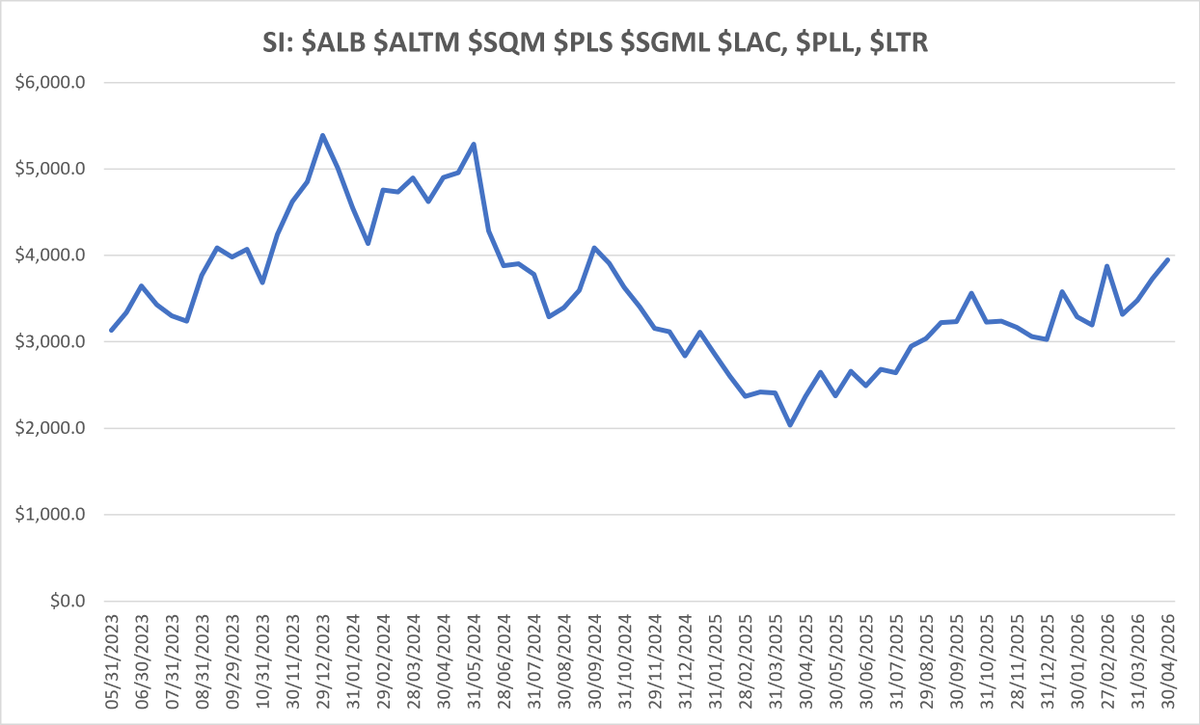

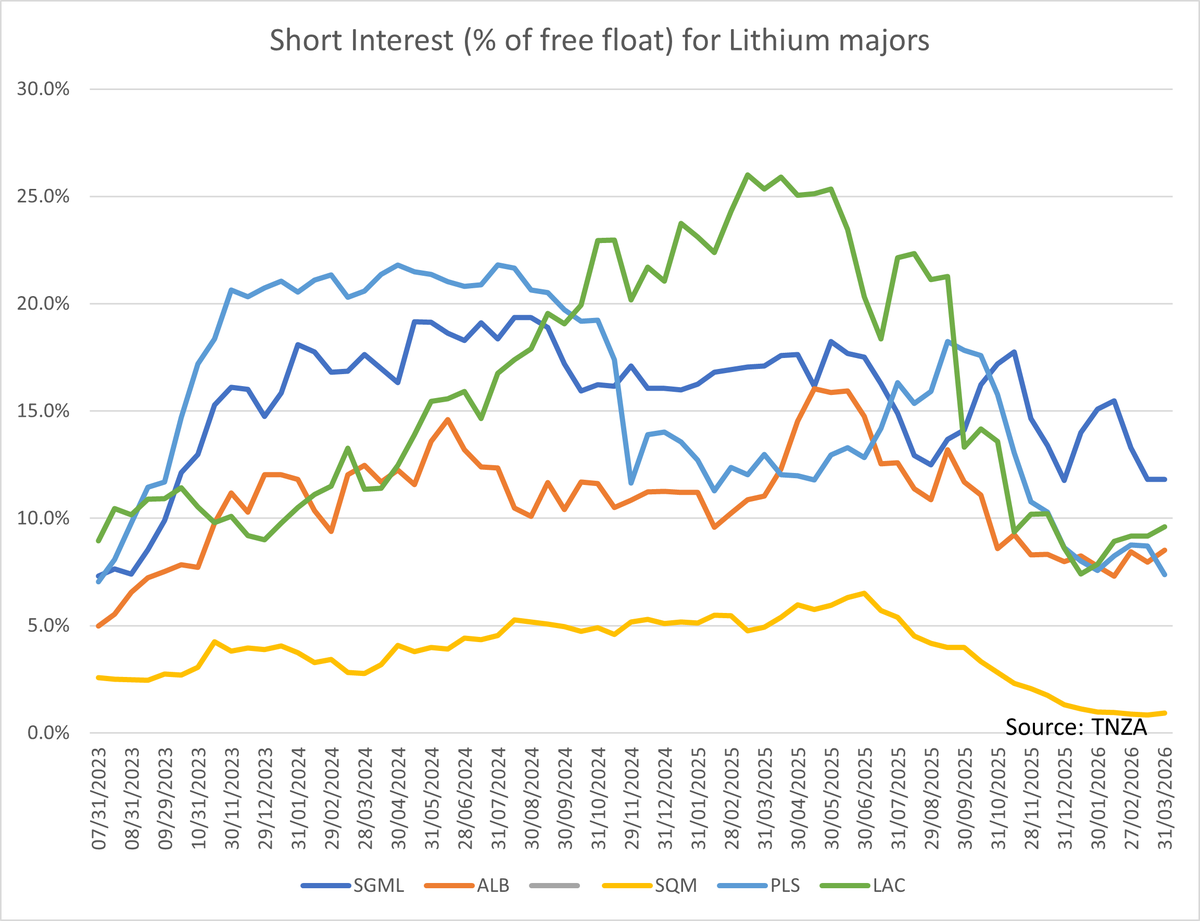

#lithium stock short interest data is out for mid May (more timely from me as feet back under the desk).

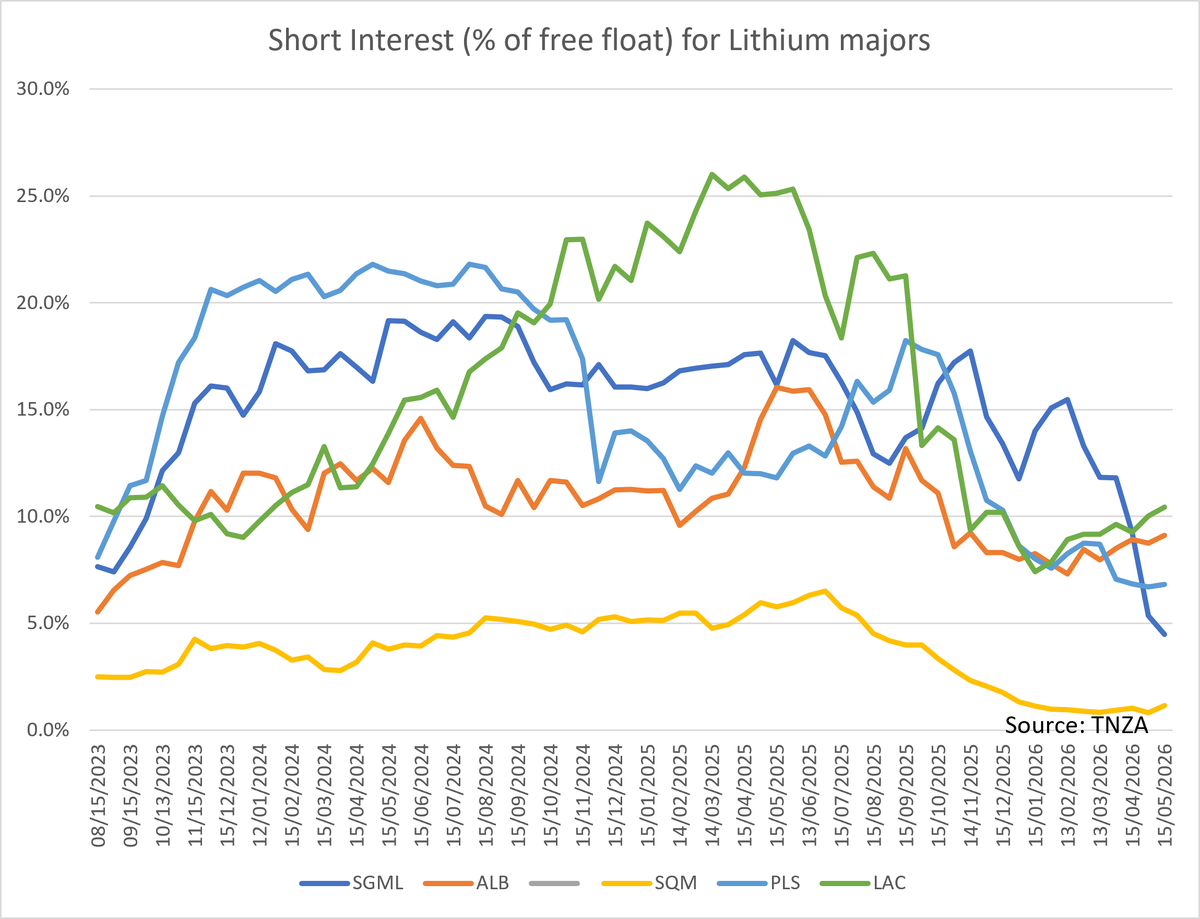

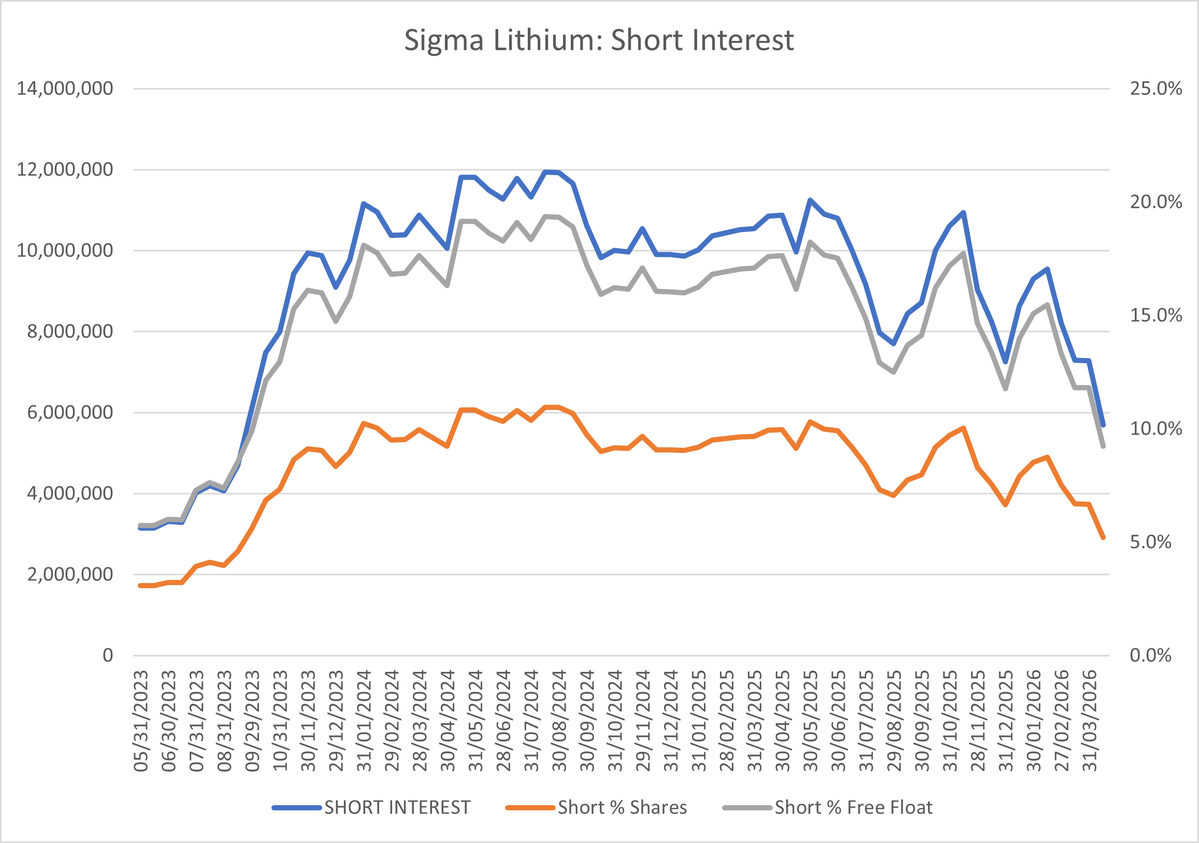

Slight increase in SI across most names with the noticeable exception of $SGML where SI continued to collapse ahead of Q1 results - (interesting to see what the SI has done post the figs & continued FUD).

Strikes me as a tricky market for shorts - couple of small cap bids ($A11 #ALL and $ZINN) vs equity calls to fund capex ($ELV & $SLM).

Spending some time on solar high SI names $ENPH $SEDG $RUN etc....

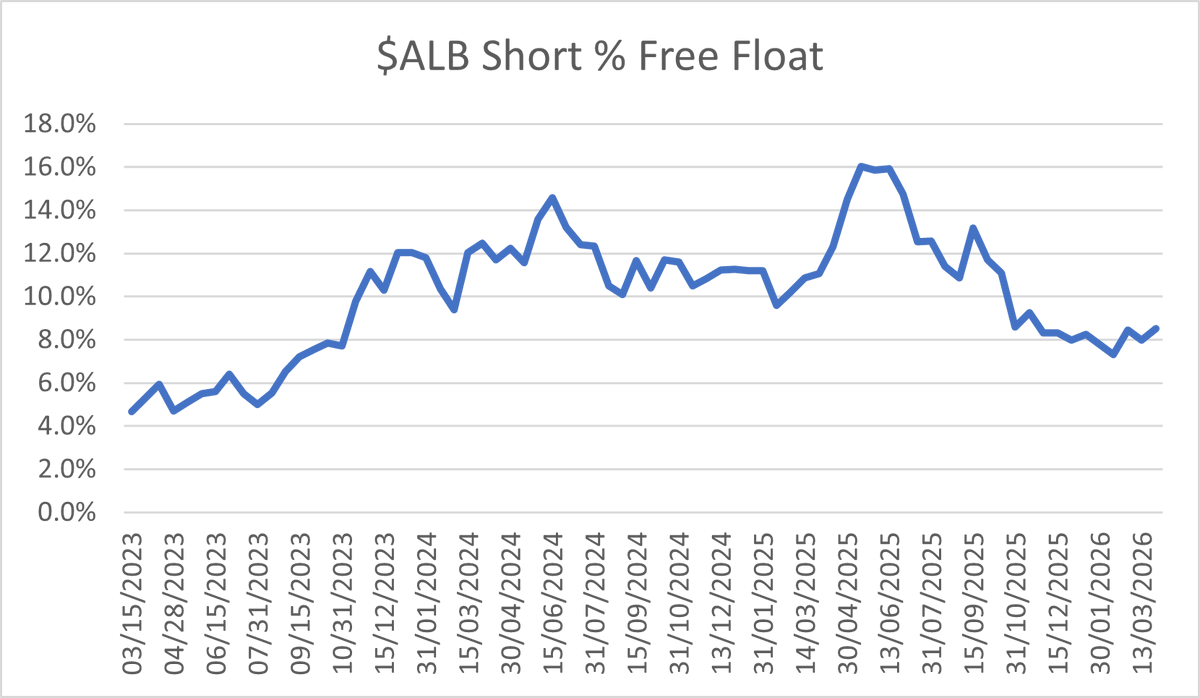

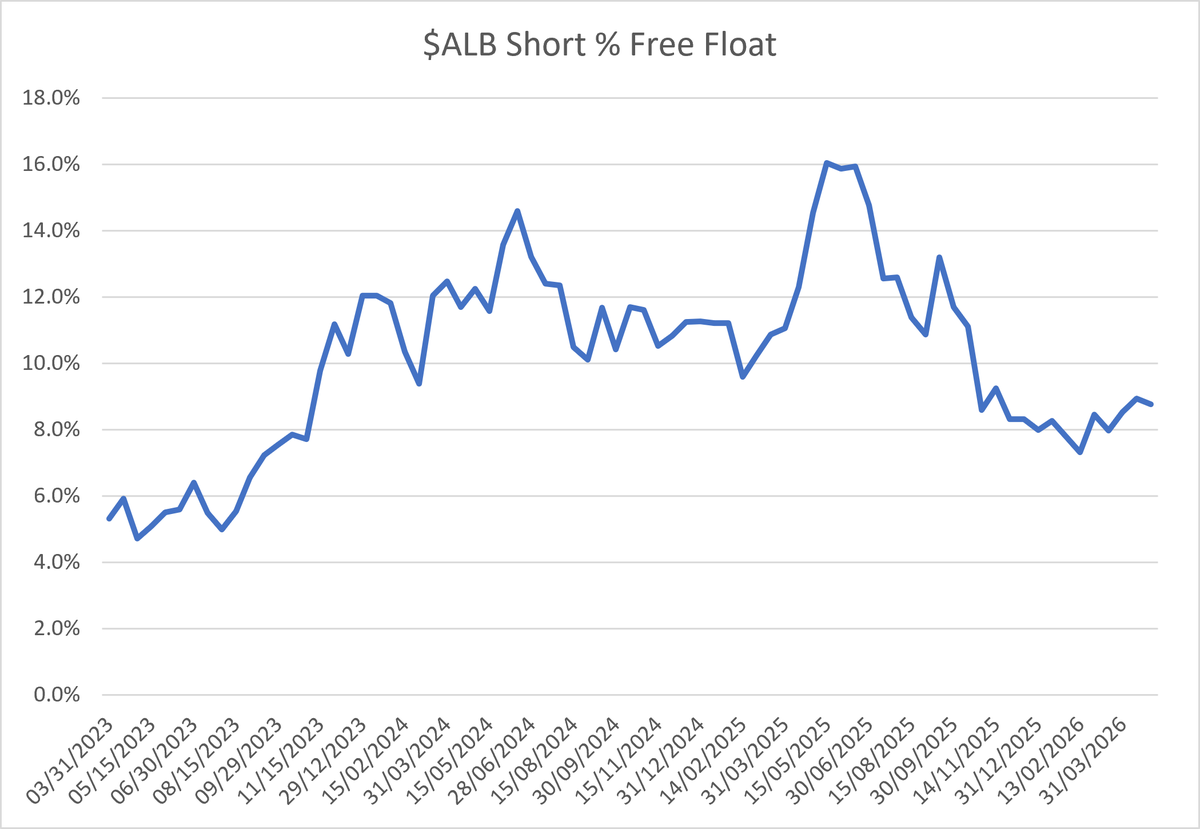

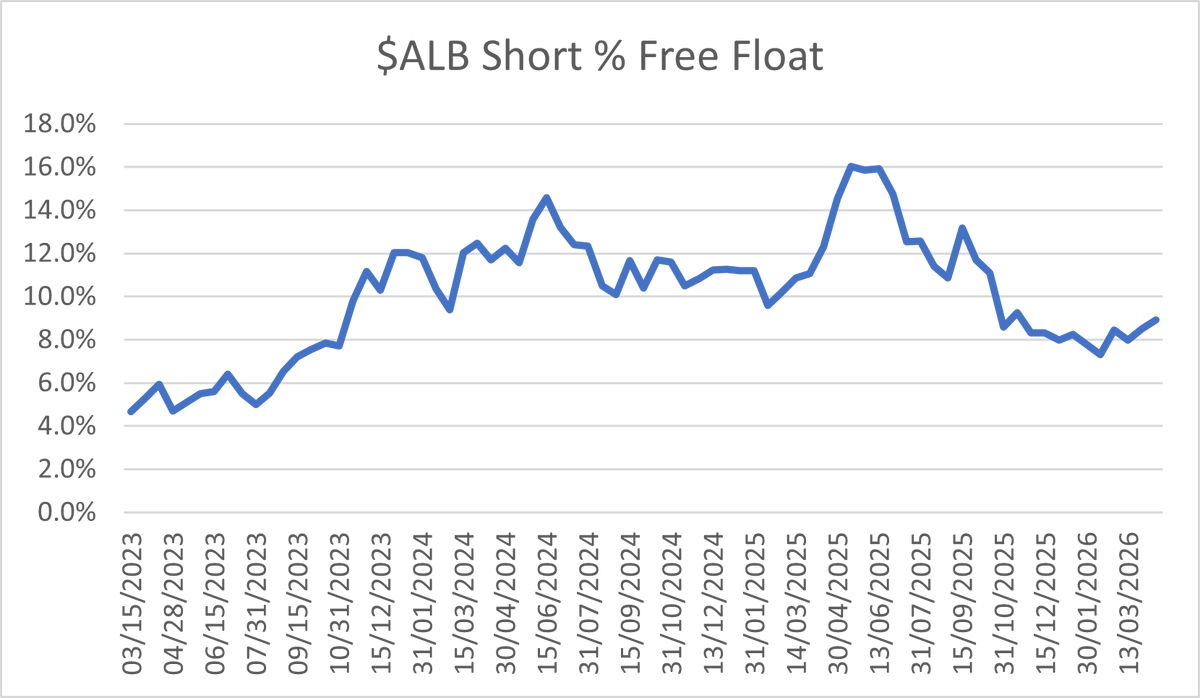

o $ALB 9.1% vs 8.8% (mid may vs end Aprl)

o $ELV 5.4% vs 5.3%

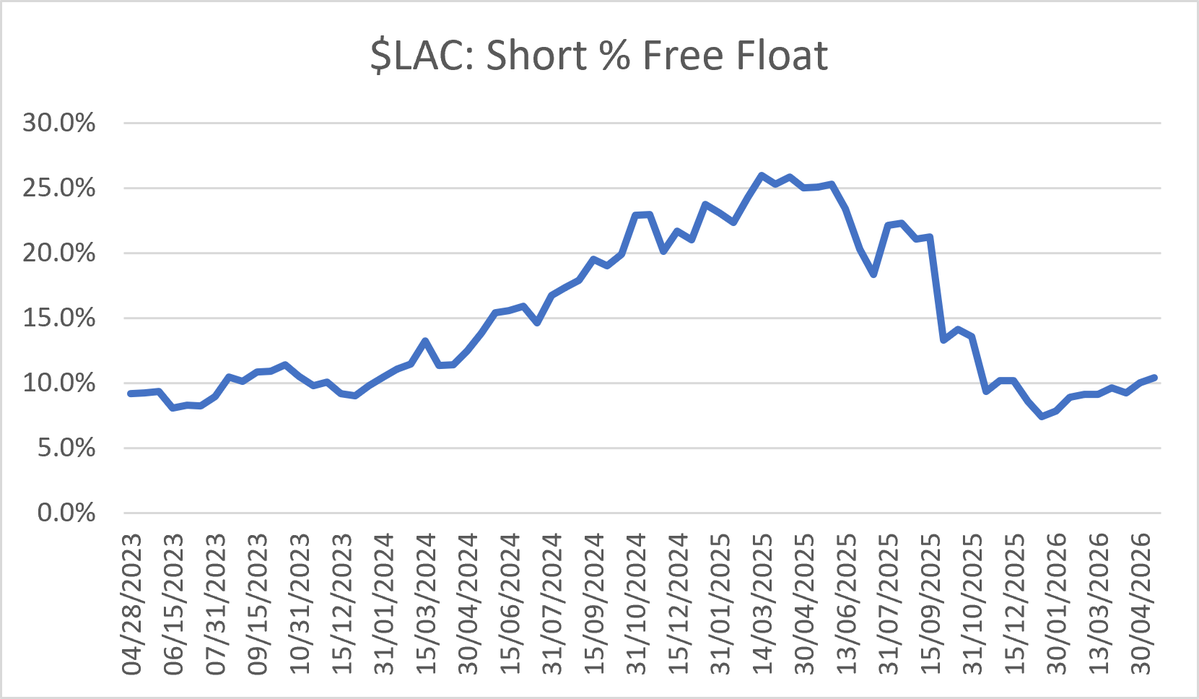

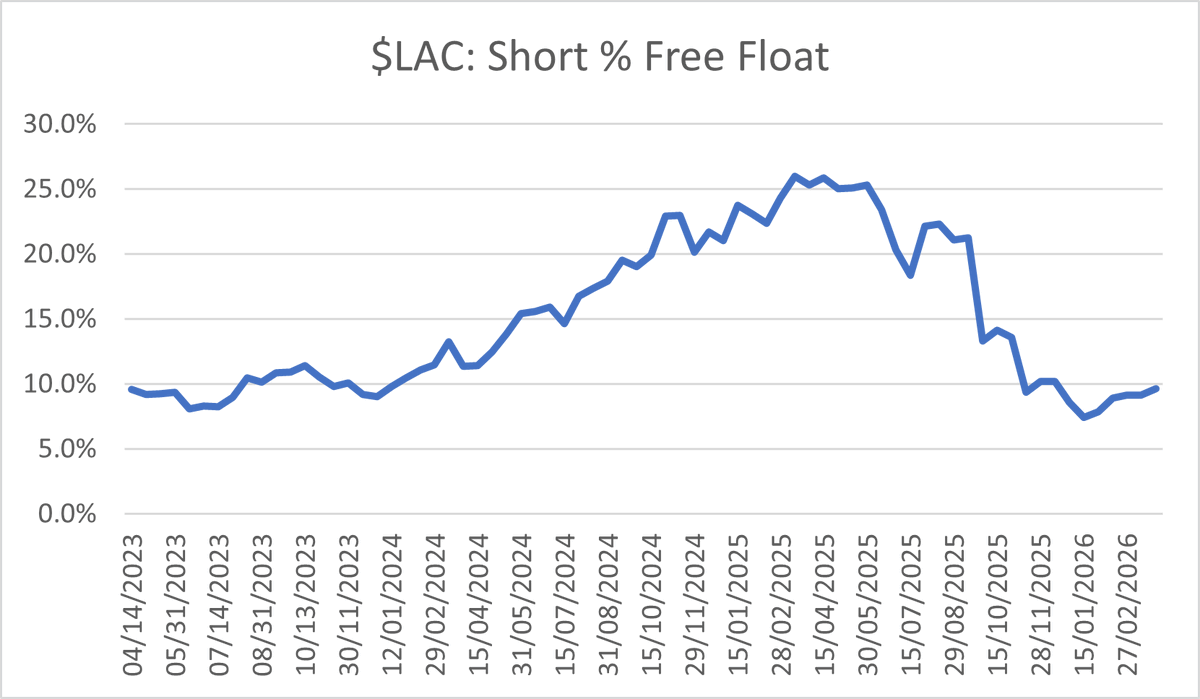

o $LAC 10.4% vs 10.0%

o $LAR 4.3% vs 3.5%

o $LTR 2.3% vs 2.2%

o $MIN 5.8% vs 5.7%

o $PLS 6.8% vs 6.7%

o $SGML 4.5% vs 5.3%

o $SQM 1.1% vs 0.8%

#lithium stock short interest data for end of April is now available.

Will try and update the data for mid May in a more timely fashion over the next few days as likely some changes to note.

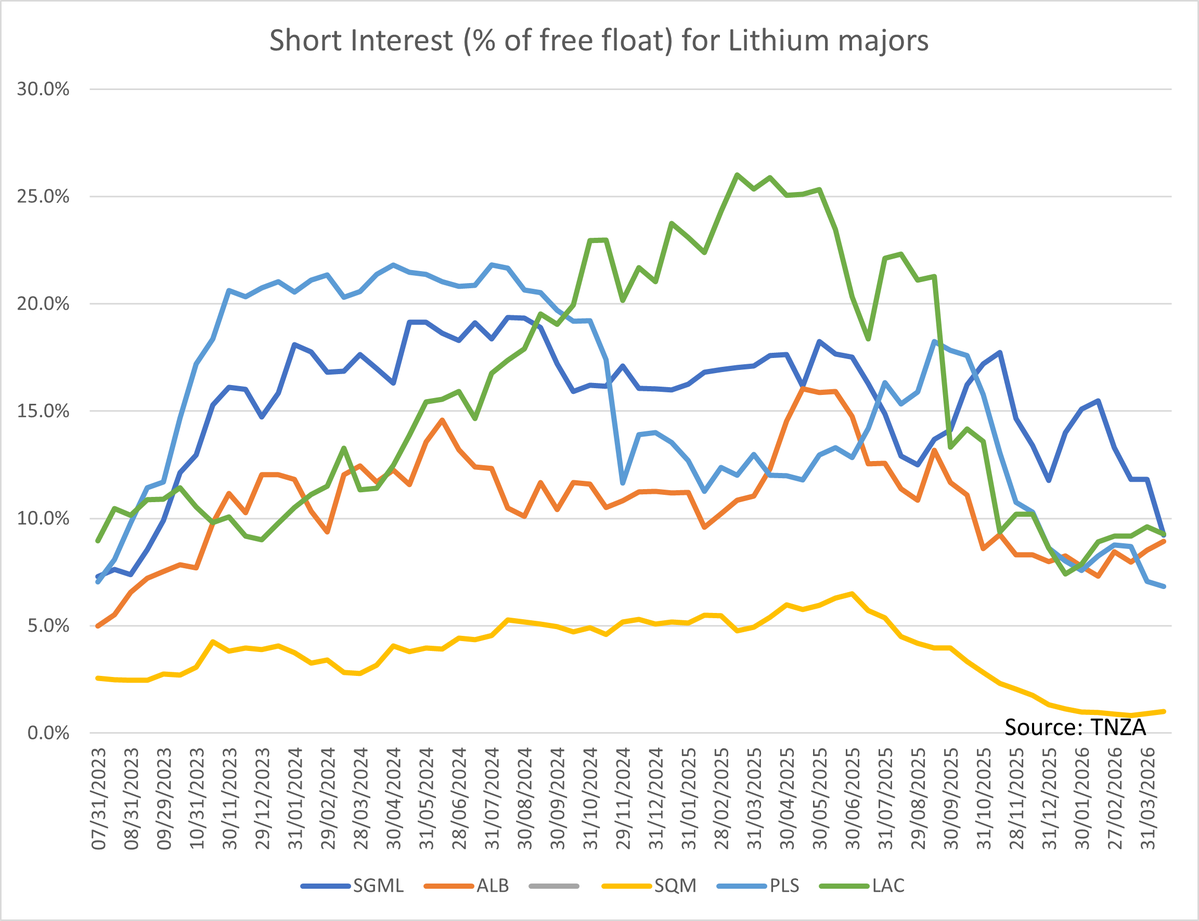

Noticeable decline at $SGML to 5.3% ahead of Q1 results & a chart break out and SI now at lowest level since April 2023

$LAC continues to creep higher & $ALB looking stubbornly high

o $ALB 8.8% vs 8.9% (end April vs mid March)

o $ELV 5.3% vs 5.6%

o $LAC 10.0% vs 9.3%

o $LAR 3.5% vs 3.9%

o $LTR 2.2% vs 2.9%

o $MIN 5.7% vs 6.1%

o $PLS 6.7% vs 6.8%

o $SGML 5.3% vs 9.2%

o $SQM 0.8% vs 1.0%

Admire your confidence 😃. A typical merger arb discount to an all cash offer would be ~5%. IMO #all discount is wider due to: 1. Multi jurisdiction al antitrust & foreign investment approvals, 2. Ghana regulatory waivers, 3. Corporate restructuring of the Ewoyaa operating subsidiary, 4. 75% shareholder vote threshold. Each one of those hurdles has added approx 2%pts to the discount. Which is at odds to @ALLTheChairman statement of "the most attractive, certain, and accelerated realisation of value". Market saying its not certain.

18.8p per share vs 16.2p today implies 16% discount to the bid price. Assume close at year end then equals a 27% annualised return between now and close. Market clearly thinks it doesn't close. But if it doesn't the $elv announcement today implies that #all have a partner that can and will fund their share of the capex. Plus highly unlikely outside chance of a counter bidder IMO. FWIW I 2x my position at 16p last week to capture some of the annualised return. Might be missing something 🤷 NFA.

@ALLTheChairman kindly explain why 18.8p is better than buying out $elv from the jv, signing an off take for half the capex, fresh equity for the other half, for a 'simple DMS process' with 'exceptional transport links' at the low end of the cost curve with exploration optionality creates value for long suffering shareholders when we have just entered a higher for longer #lithium price environment!!! Your minority shareholders deserve better.

@Trisseswe@AtlanticLithium SP reaction seems to be suggesting that this one gets blocked - lots of regulatory approvals required - and we know how fast Ghana works.

Hope I'm wrong and it flushes out a proper bid, but...

So $A11 #ALL@AtlanticLithium I've seen some sh1t deals in my time, but this one even surpasses the Arcadium/RIO sell out at the low point in the cycle.

Even assuming shareholders had to fund 100% of the capex with fresh equity, it is IMO impossible to justify a sell out at the proposed Huayou valuation.

#lithium short interest data now available for mid April.

Noticeable decreases at $LAR and $SGML, $PLS also lower vs $ALB slight increase.

The short squeeze in $CAR might have forced some de-risking in other high SI names and feels like some short term positioning moves.

IMO SI across the sector still well above a normalised level in a higher for longer #lithium price environment.

o $ALB 8.9% vs 8.5% (mid april vs end march)

o $ELV 5.6% vs 5.9%

o $LAC 9.3% vs 9.5%

o $LAR 3.9% vs 6.1%

o $LTR 2.9% vs 2.6%

o $MIN 6.1% vs 6.2%

o $PLS 6.8% vs 7.1%

o $SGML 9.2% vs 11.8%

o $SQM 1.0% vs 0.9%

@Milinkoeterno Hard to get reliable data for .v stocks - but looks like the short interest is only 134.6k shares or 0.1% of the float. Will keep an eye on it.

Updated #lithium short interest data for end of Mar - while there are still any shorts left 🤣🤣🤣. If your #lithium short thesis is prices are lower for longer - you are going to get your face ripped off when the cycle turns. Just saying. $ALB +13%, $SGML +15%, $SQM +8% today at pixel time.

Whilst I'm at it - congrats to $PLS on making a new ATH in 🇦🇺 overnight - goes to show what investing counter cyclically can do - grow vols into rising prices whilst others need years to catch up. Lesson for any budding #lithium CEOs out there -protecting your balance sheet through a down cycle and maintaining capex and opex discipline should imply you explode to the upside when the cycle turns up. Also, if Paul Graves is listening - you sold it at the low point in the cycle!!!

A small increase in SI across the sector over the last 2 weeks of March - likely risk off war related.

o $ALB 8.5% vs 8.0% (end mar vs mid mar)

o $ELV 0.6% vs 2.0% (change of data source and might be inaccurate)

o $LAC 9.6% vs 9.2%

o $LAR 6.1% vs 4.5%

o $LTR 2.6% VS 4.5% (change of data source as per $ELV)

o $MIN 6.2% VS 6.3%

o $PLS 7.4% vs 8.7%

o $SGML 11.8% vs 11.8% (guess while waiting for Q4s)

o $SQM 0.9% vs 0.8%

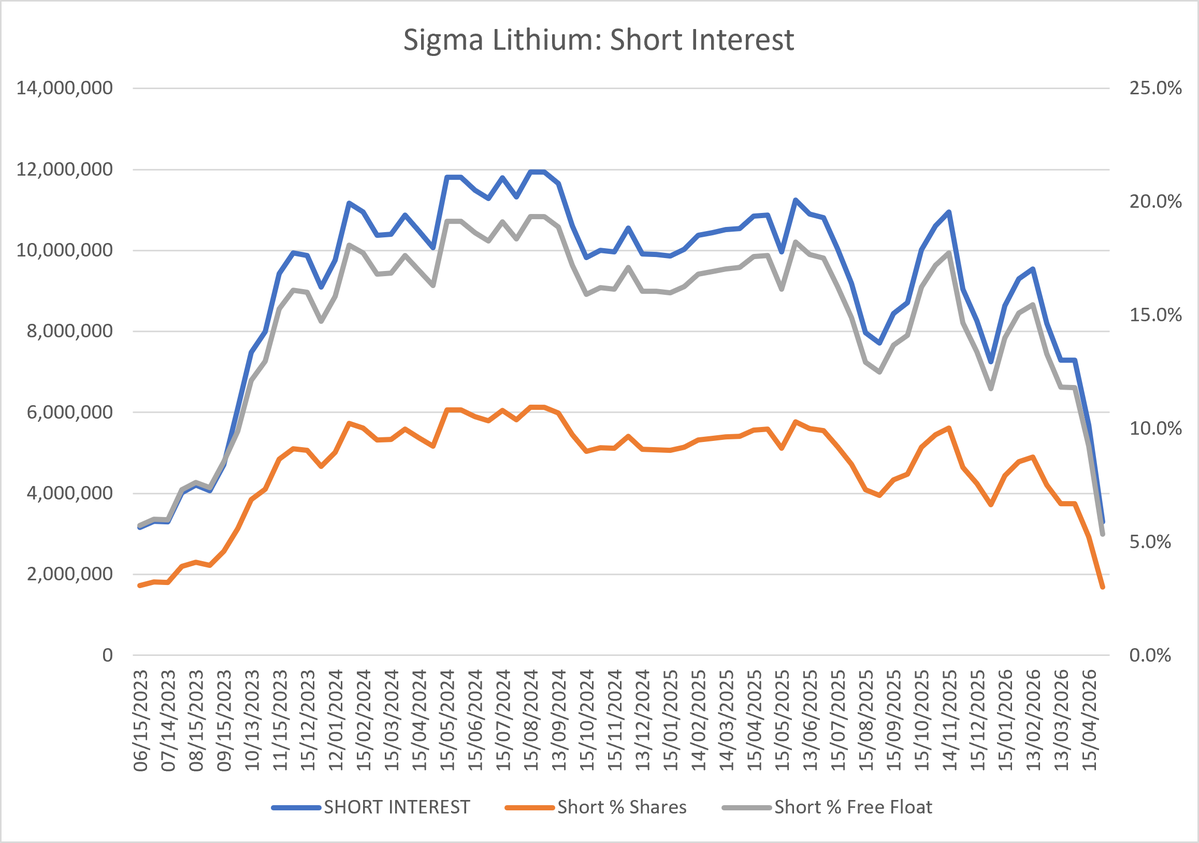

$SGML short interest still stubbornly high at end of Mar - likely before the double barrel they gave that week on the balance sheet.

Share price low of ~$4.50 at end Jun 25 to $21 today and SI has only gone from 1.7% of the free float to 11.8%.

Updated #lithium short interest data for end of Mar - while there are still any shorts left 🤣🤣🤣. If your #lithium short thesis is prices are lower for longer - you are going to get your face ripped off when the cycle turns. Just saying. $ALB +13%, $SGML +15%, $SQM +8% today at pixel time.

Whilst I'm at it - congrats to $PLS on making a new ATH in 🇦🇺 overnight - goes to show what investing counter cyclically can do - grow vols into rising prices whilst others need years to catch up. Lesson for any budding #lithium CEOs out there -protecting your balance sheet through a down cycle and maintaining capex and opex discipline should imply you explode to the upside when the cycle turns up. Also, if Paul Graves is listening - you sold it at the low point in the cycle!!!

A small increase in SI across the sector over the last 2 weeks of March - likely risk off war related.

o $ALB 8.5% vs 8.0% (end mar vs mid mar)

o $ELV 0.6% vs 2.0% (change of data source and might be inaccurate)

o $LAC 9.6% vs 9.2%

o $LAR 6.1% vs 4.5%

o $LTR 2.6% VS 4.5% (change of data source as per $ELV)

o $MIN 6.2% VS 6.3%

o $PLS 7.4% vs 8.7%

o $SGML 11.8% vs 11.8% (guess while waiting for Q4s)

o $SQM 0.9% vs 0.8%