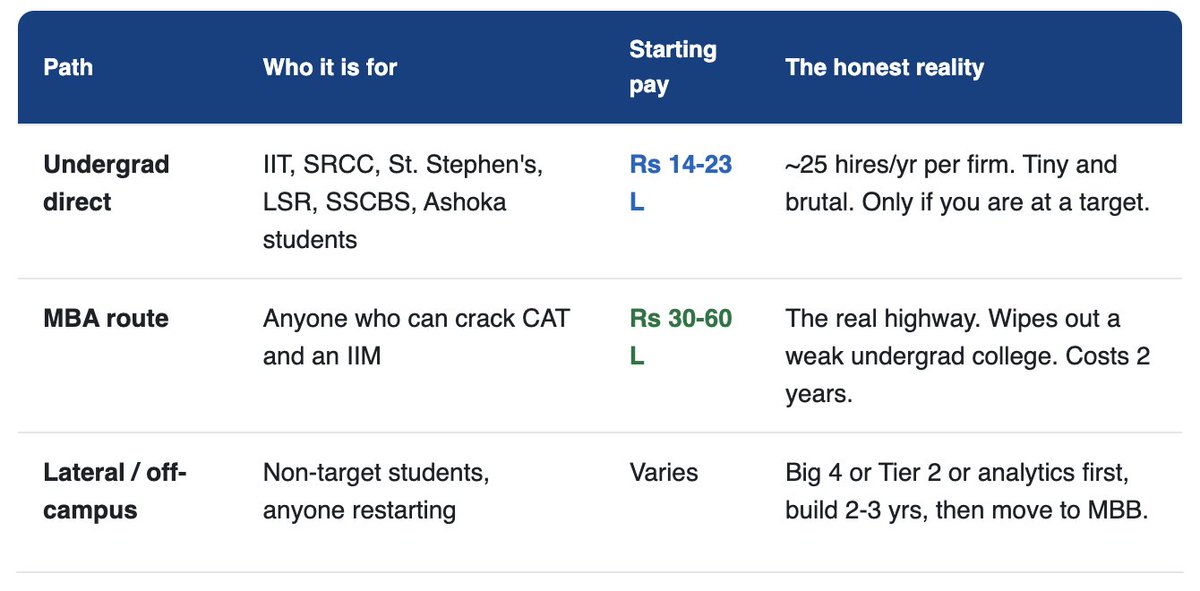

Three doors into consulting.

Undergrad direct: roughly 25 hires per firm per year, only from target colleges.

The MBA route, the real highway.

And the lateral path, Big 4 or Tier 2 first, then jump.

Your college at 18 decides which door is open, but none of them ever fully shut.

Miss the first, the MBA erases it.

Miss both, three years of sharp work at a smaller firm still gets you in.

The pedigree filter is real early and fades fast with a track record.

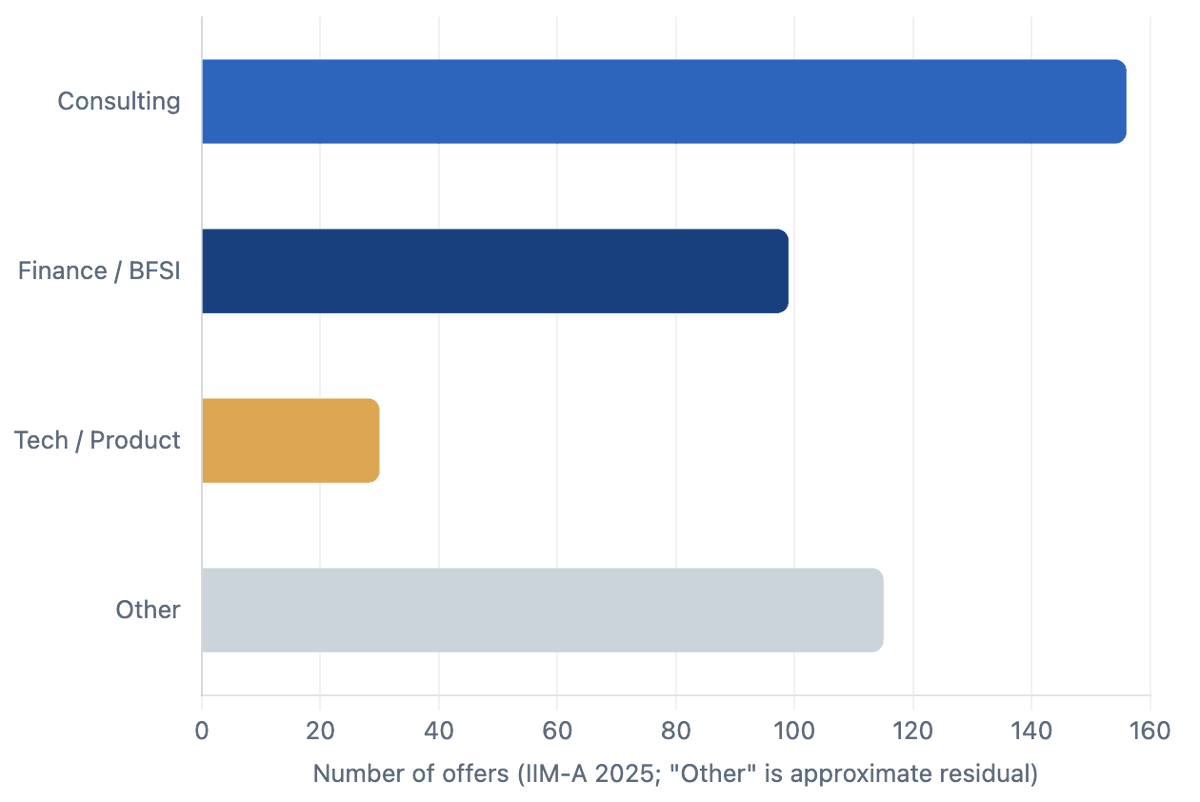

At IIM Ahmedabad in 2025, consulting pulled 156 offers, more than finance or tech, and BCG was the single largest recruiter on campus.

Median package hit Rs 34.59 lakh.

On a top IIM campus, consulting hunts you, not the other way around.

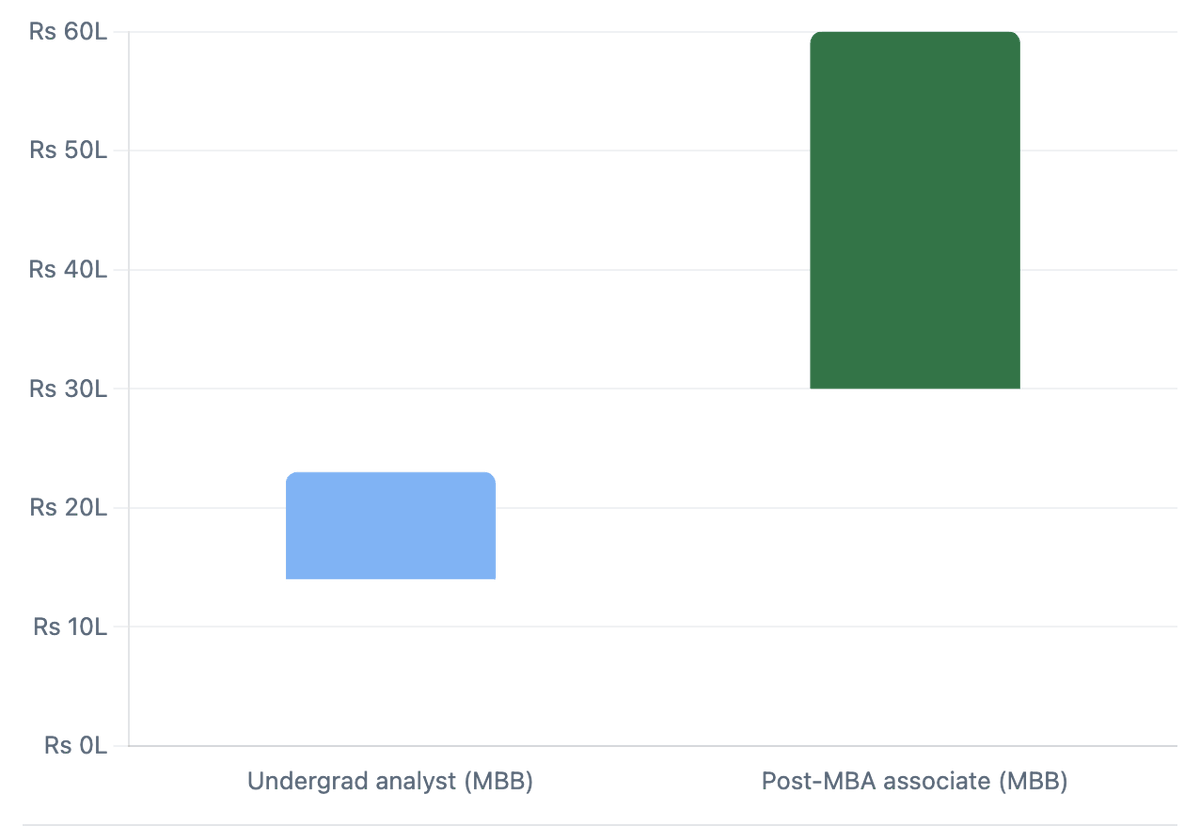

That is the entire reason the MBA route is the highway and not the scenic road.

Get onto the campus and the door opens itself.

The hard part is the CAT percentile, not the job hunt that follows.

An undergrad analyst at McKinsey or BCG in India starts at Rs 14-23 lakh.

Do a top MBA first, and the same firm pays you Rs 30 to 60 lakh, roughly double, for the same badge of MBB

The MBA is not about the degree; it is a Rs 20 lakh-a-year salary reset and a clean way to erase the stigma of a non-target undergrad college.

If you missed the elite college door at 18, CAT at 22 reopens it fully.

The gap between the two bars is what two years of your life is worth.

Consulting is a pyramid.

Three firms- McKinsey, BCG, and Bain- sit at the top and hire the fewest.

Below them are the Big 4, then Tier 2 firms like Kearney and LEK, then boutiques like Praxis and Redseer with far more seats.

Most students obsess over the top three and ignore the rest.

But a Tier 2 or Big 4 seat teaches the same skills, then becomes your lateral ticket into MBB three years later.

The bottom of the pyramid is a side door, not a consolation prize.

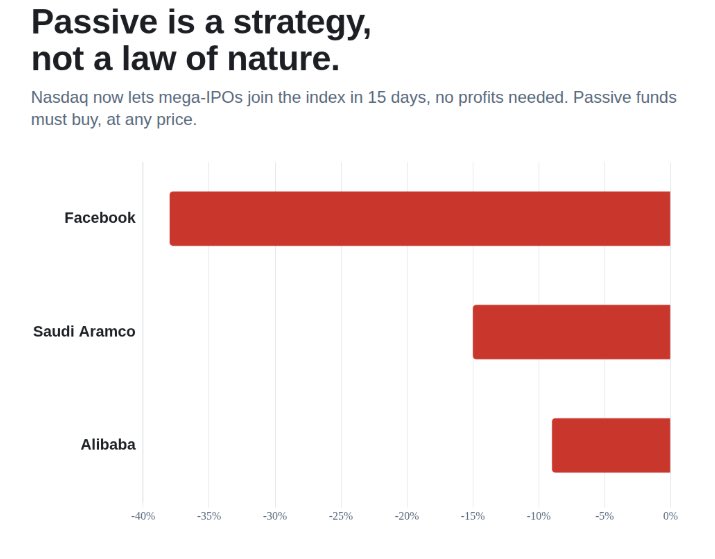

Passive investing was sold to you as the safe choice.

Buy the index, skip the noise, let it ride.

That's quietly changing, and most people haven't noticed.

Nasdaq now lets mega-IPOs join the index in just 15 days.

No profits required.

So passive funds must buy a loss-making giant at whatever price it lists at.

History isn't kind. Facebook fell 38% after listing. Aramco 15%. Alibaba 9%.

The index is no longer the same as quality.

India's power index peaked in 2008, then went nowhere for 14 years.

Here's the strange part.

It was never a demand problem.

Peak demand rose 68% in that stretch, from 148 GW to 250 GW.

The real bottleneck was a broken customer.

State discoms were bankrupt, buying power high and selling below cost.

So power firms couldn't collect.

The whole chain froze.

Sometimes the constraint isn't your product.

It's whether your customer can actually pay.

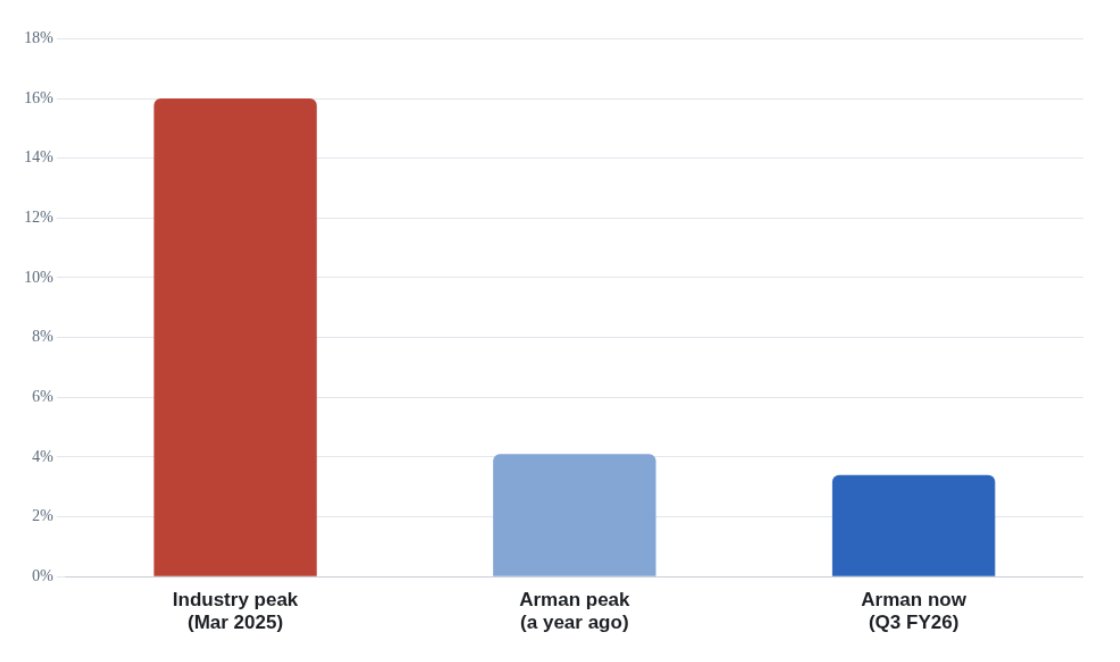

India's microfinance sector has been brought to its knees again, industry bad loans hit about 16% in the 2024-25 crisis.

It's happened before. Andhra 2010. Demonetisation. Covid.

Now, a 2024 heatwave is wrecking rural incomes.

Each time, the obituaries get written.

Each time, the sector comes back.

Through it all, one lender, Arman Financial, peaked at 4.1% and is already down to 3.4%.

The next up-leg belongs to whoever survived the down-leg.

A simple valuation gauge for India just fell from 75 to 52.

On a scale where 0 is cheap and 100 is expensive, 75 was frothy.

52 is fair.

Sensex P/E is around 20 now, and the dividend yield is about 1.2%.

So notice what happened. The market didn't crash. It cooled.

And history rhymes here.

Readings in the low 50s have been followed by roughly 17% a year over the next three years.

The crowd remembers the high.

The gauge only remembers the average.

The whole world is suddenly hunting for a pharma supplier that isn't China.

That's the real story behind India's CDMO boom.

The sector is set to grow from $3.5bn to $24bn by 2035.

Roughly 15% a year, for a decade.

The US BioSecure Act is the push nudging global drugmakers away from Chinese suppliers.

And a shift like this shows up in order books long before it shows up in headlines.

The slow, structural story is the durable one.

India's defence exports went from Rs 700 crore in FY14 to Rs 23,400 crore in FY25.

34 times bigger in eleven years.

The world's largest arms importer is turning into a seller.

It's as clean a sector story as you'll find.

And that's exactly the trap.

These firms sit on order books worth several times their revenue and still disappoint.

Timelines slip.

You can be dead right about the sector and still pick the wrong stock at the wrong price.

Everyone wants the next small-cap multibagger.

Here's what the brochure skips.

Of 1,437 small caps tracked from 2016 to 2025, only a third climbed to large-cap status.

A third got demoted. One in six was delisted.

82.5% left the index.

Now the part nobody mentions.

When you backtest, the dead ones quietly drop out of the data.

That alone inflates small-cap returns by about 5% a year.

The screen shows you the winners.

It hides the graveyard.

Top 5 Certifications for Traders:

1. NISM Series-VIII (EQ Derivatives) - Mandatory in India for F&O dealers/traders on NSE/BSE.

2. CMT (Chartered Market Technician) - Global standard for technical analysis; ideal for traders & PMs.

3. CQF (Certificate in Quantitative Finance) - Best for quant traders, algo/HFT, & desk quants.

4. FRM - Valued for risk-aware desks, model validation, & market/credit risk.

5. NISM Series-I (Currency Derivatives) - For FX & treasury dealers in India.

This one traps smart investors every cycle.

Tata Steel, FY22: ROCE hit 33%, up from 3%.

Margins jumped 6% to 22%.

Run a screen that year, and it looked like a great transformation.

Now look at the next year.

ROCE back to 15%, and Margins to 12%.

It was never a better business.

It was a steel upcycle.

So here's the test.

If the number falls back after the boom, it was a cycle, not a turnaround.

Ask what caused it before you pay for it.

PSU banks trade at 8 times earnings.

Private banks at 17.6.

The market still treats PSU banks as risky.

But look at the bad loans.

FY18: PSU banks 14.6%, private 4.7%.

Today: PSU banks 2.1%, private 1.6%.

The risk gap closed.

The valuation gap didn't.

The market is pricing a bank that no longer exists.

And a price can lag a fact for years.

The Mac Mini M4 just rose by Rs 35,000 in India. Same chip, same specs, same box.

The Galaxy M36 rose by Rs 3,500 with zero upgrade. Indians are paying more for identical hardware.

Dixon, India's largest handset maker, may see shipments fall up to 31% this year.

The box-builder cannot escape the cost of the chip inside the box, and pure pass-through protects margin only by sacrificing volume.

India assembles the world's iPhones and laptops but fabricates zero memory chips.

When global memory triples, there is no buffer, and at under 4% of global demand in the cheapest chips, India is exactly what suppliers are dropping.

Rupee depreciation and 18% GST then stack on top of imported costs, so Apple's India hikes hit 70%, the steepest anywhere.

The factory of the world pays the world's highest price for the part it cannot make.

DRAM contract prices rose 93% in a single quarter, then NAND rose 72% the next quarter.

TrendForce, 20 years in this market, kept revising its forecast up because reality outran it.

Their analyst: "The craziest time ever."

So what: When the input cost of every device nearly doubles in two quarters, no assembler can absorb it.

It flows straight to the shelf price, then to your invoice.

70% of the world's memory now goes to AI data centres, up from under a third in 2022.

AI did not just raise demand. It walked off with the supply.

This is a permanent reallocation, not a passing shortage.

Every phone and laptop maker now bids against AI for the same wafers and loses, so device prices stay structurally higher long after the headlines fade.

Apple TV +67%, MacBook Pro +$300, & iPad Air +$150.

On 25 June 2026, Apple raised prices across its line with no spec changes, marking the first mid-cycle price hike of its kind.

The one product it left untouched: the iPhone.

Apple is signalling which products hold pricing power and which break under it.

If the iPhone 18 finally moves this autumn, the price floor for global electronics has reset permanently, not seasonally.

There is a number in the Indian buyer's head: Rs 1,000.

Above it, most people hesitate to buy a board game. Now look at what games actually cost.

Funskool's made-in-India Catan sits at Rs 3,499. A typical import runs higher.

A small homegrown studio needs to price above the ceiling just to survive a short print run.

So the ceiling quietly hands the mass market to whoever has the volume to price under it.

Scale wins again.