Goldman Sachs on High-End CCL:

High-end CCL has become one of the fastest-growing segments in the AI hardware stack, with demand significantly outpacing supply additions.

NVIDIA VR200: Expected to require 3.5x more CCL dollar content than GB300, driven by higher-grade M8+ materials and additional midplane boards.

Trend extends to AI ASICs and high-speed switches, steadily increasing CCL content per system.

Strong structural tailwinds for CCL in AI infrastructure.

Morgan Stanley: Optical vs Copper in AI

Scale-Out: Small adoption (10–15%) in 2027; CPO low single-digit in 2028, scaling meaningfully in 2029 (Feynman era).

TAM Drivers: Capex 2x higher than expected last year + exploding cluster sizes (8 → 72 → hundreds → thousands) as multipliers.

Supplier Exposure:

Lumentum: Most positive (Google transceiver exposure, less CPO risk).

Coherent: Balances transceiver business with CPO opportunity.

Corning: Less direct impact from CPO; GlassBridge still early-stage.

Copper Position: Strong runway through 2026–2027 (retimers, better SerDes). Hybrid environment expected before full optics shift. Ethernet (Broadcom) and UALink (Marvell, Astera Labs) key debates.

Keysight: Agnostic winner — benefits from multiple architectures, higher speeds, and frequent changes requiring advanced testing.

Copper dominant short-term; optical scale-out ramps later. CPO more relevant in scale-up.

$ALAB $NVDA $AVGO $MRVL $CRDO $SMTC $APH $KEYS $COHR $LITE $GLW $GOOGL

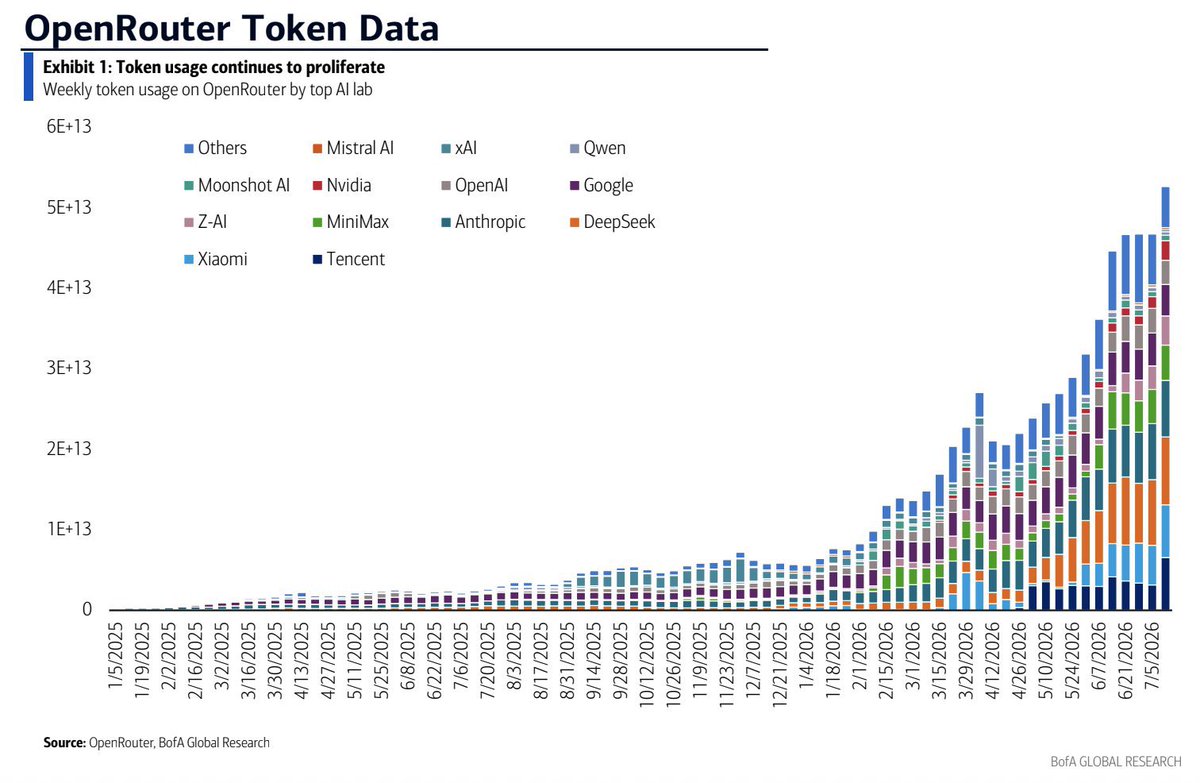

BofA: Kimi K3 Release & AI Compute Race

Kimi K3: Moonshot’s new 2.8-trillion-parameter MoE model with 1M token context window. Positions China closer to U.S. frontier labs.

Pressure on U.S. Labs: Google Gemini 3.5 Pro reportedly delayed; OpenAI, Anthropic, Google need larger training runs, more RL, synthetic data, and faster cadences.

MoE Impact: Boosts demand for memory movement, routing, latency, and interconnects.

NVIDIA Advantage: GB300 NVL72 offers up to 25x performance-per-watt improvement on leading open MoE models.

Bullish for Semis: Open models drive infrastructure spend on GPUs, HBM, networking, and efficient inference. EDA (Cadence, Synopsys) remains critical despite open-source mentions.

Token Usage: Chinese labs leading weekly token volume; U.S. enterprise AI adoption at 55% (Anthropic 42.4%, OpenAI 39.5%).

Kimi K3 accelerates the compute race and remains structurally positive for AI semiconductors.

$CDNS $NVDA $GOOGL $SNPS

Citi: EML Output Trends

Industry Shift: Rapid transition from 100G EML to 200G EML and CW (Continuous Wave) by 2028 across listed companies.

AXT, Inc.: 200G EML output surges from 13.54M chips (2025) to 157.82M chips (2028).

Chinese Players: Strong expansion in CW output. Source Photonics (Dongshan Precision) from 14.66M (2025) to 161.77M (2028).

Sumitomo Electric: Maintains high production, especially 200G EML from 28.93M (2025) to 128.58M (2028).

Accelerated upgrade to higher-speed lasers driven by AI optical module demand.

Goldman Sachs: Innolight & Optical Modules

Speed Migration: 1.6T moving to volume production; 3.2T ramp in 2027. 1.6T expected to be mainstream by 2027 (45.72M units).

SiPh Adoption: Penetration 60% (800G), 80% (1.6T), 100% (3.2T) by 2026. SiPh revenue share from 28% (2025) to 62% (2028E).

Innolight: Leading 1.6T pluggable supplier, projected 50–60% (or up to 70%) market share in 2026. Capex +155% YoY in 2026 for capacity.

ASP Trends: 1.6T ASP from $840 (2025) to $435 (2028E); 3.2T starts at $1,023 (2027E) → $768 (2028E).

TAM: Global optical module market from $34.2B (2025) to peak $72.6B (2027E). High-speed (1.6T+3.2T) revenue from $3.9B (2025) to $44.9B (2028E).

Rapid shift to higher-speed SiPh-based modules driven by AI demand.

Morgan Stanley: CXL Market Update

Raised long-term CXL market forecasts due to faster industry adoption and elevated memory shortages.

2030E Estimates:

CXL MXC chips: US$2.1B (up from previous $990M)

CXL switch chips: US$1.9B (up from previous $664M)

Significant upward revision reflecting stronger demand for CXL solutions to address memory bandwidth and capacity challenges in AI systems. ($PENG $MRVL $ALAB)

Morgan Stanley: ZAM Memory

Cloud Memory Spending: Projected to reach $418B by 2030 (8% CAGR from 2026). Share of total cloud capex rises to 40% in 2027 (from 12% in 2023 pre-AI).

Bandwidth Lag: Memory bandwidth improvements (+14% from DDR5-5600 to DDR5-6400) lag far behind token growth (320x on major clouds from Apr 2024–Jun 2026).

Spending Peak: Absolute cloud memory spend peaks in 2028E at ~$520B, then declines as % of total capex to 25% by 2030E (non-memory capex hits $1.28T).

DRAM S/D: Deep structural shortage persists through 2028E (deficit -10% to -16% in 2026E).

NAND S/D: Moves from surplus to tight (deficit -9% in 1Q26E, moderating to -3% to -4% later). Transitioning to enterprise storage/LLM KV caches.

AI driving sustained memory tightness and high cloud spend share through late 2020s. ($DRAM $MU $SNDK $WDC $EWY)

BofA: 3Q Memory Contract Price Check

Server DRAM: +20–30% QoQ (stronger than consensus ~20% or less), led by high-speed LPDDR5.

Spot Demand: Healthy, driven by commodity DDR5 and legacy DDR4; July prices rising MoM.

HBM4 Transition: Shifting orders toward higher-priced HBM4 from HBM3e.

LTAs: Represent <50% of DRAM sales (non-LTA 60–70%), allowing solid QoQ increases (5–10%), often settled even under existing contracts.

Rush Orders: OEMs rushing to buy ahead of peak 4Q season, confirming >20% QoQ increase for commodity DRAM and NAND.

ASP Outlook: BofA forecasts +21% QoQ for 3Q DRAM ASP (more optimistic than TrendForce).

Spot Market: DRAM spot prices up for 8 consecutive weeks; NAND rebounding (1Tb wafers +4% WoW).

Strong pricing momentum continuing into 3Q, defying earlier skepticism. ($DRAM $MU $SNDK $WDC $EWY)

UBS: Materials Sector (H2 2026 Price Hike Visibility)

Ranking (Highest to Lowest):

MLCC Materials > MLCCs > WF6 > Semiconductor Wet Chemicals > Helium

MLCCs:

High-capacitance MLCC supply remains tight due to AI server demand crowding out capacity.

Yageo raised prices from July 1 across automotive, industrial, AI server, and consumer segments.

Upstream materials (e.g., release films) at high utilization → further upside.

Electronic Specialty Gases:

WF6 (5N-grade): Prices doubled YTD to RMB1,800/kg due to tungsten powder export decline (shortage for Japan/Korea).

Helium: Peaked in April, corrected to RMB250/m³; expected to stabilize at RMB200–300/m³ in H2.

Electronic Wet Chemicals & Targets:

EG-HF: Rising raw material costs (sulfur, anhydrous HF) + strong exports → continued price hikes.

Sulfuric Acid, H2O2: Upward trend since March.

Targets (Molybdenum, ITO): Indium (+70% YTD), Molybdenum (+30% YTD) raw material costs support price increases.

Focus shifting to materials with strong pricing power post-correction, led by MLCC-related segment.

Moonshot AI is about to release Kimi K3, a massive large language model with 2–3 trillion parameters — China’s largest AI model to date.

Expected to surpass Anthropic’s Opus 4.8 on mainstream benchmarks and will be released as an open-weight model available for free download.

The launch could challenge the industry consensus that Chinese AI models lag U.S. frontier labs by 8–12 months.

Moonshot is raising a new funding round at a valuation of ~$31.5 billion.

K3 is scheduled for release in the coming days.

SEMI: Global Semiconductor Equipment Sales Forecast

2026: Record $165.9B (+23.2% YoY).

Long-Term: Momentum through 2028 to $229.5B.

AI infrastructure demand — leading-edge logic, HBM, advanced packaging, and complex architectures.

Segment Breakdown:

Wafer Fab Equipment (WFE): +23.1% to $143.9B in 2026; +21.8% (2027), +14.1% (2028) → surpasses $200B.

Test Equipment: +31.0% to $15.3B in 2026 (after +55.3% in 2025) → $20.8B by 2028.

Assembly & Packaging: +9.6% to $6.7B in 2026 → $8.6B by 2028 (driven by heterogeneous packaging).

Geographic Trends:

China, Taiwan, and Korea remain top 3 through 2028.

China #1 but growth moderating after heavy investment.

Taiwan & Korea focused on leading-edge foundry and HBM.

Other regions accelerating in 2027–2028 due to regionalization and incentives.

Historic AI-driven equipment boom continuing through 2028.

BofA: Optical FAUs (CPO Market Outlook)

Nvidia CPO Switch Shipments:

2026E: 14k units

2027E: 52k units

2028E: 190k units (meaningful volume takeoff)

TAM: FAUs in Nvidia CPO switches projected to reach US$8B by 2030E (based on 1.4M CPO switch units). FAU contributes 5–10% of CPO switch BoM, ASP $80–$200.

Technical Barriers:

Micron-level alignment (< ±0.5μm for NPO, < ±0.3μm for CPO) critical to avoid signal loss.

Automation essential as channel counts rise to 60–100.

GlassBridge (Corning): Early stage, unlikely for current/next-gen CPO due to edge coupling limitations, alignment issues, and wafer-scale testing challenges.

CPO/FAU ramp accelerating with Nvidia, but tight technical requirements create high barriers. ($GLW $MRVL $AVGO $HIMX $LITE $COHR $FN $NVDA $TSMC)

Morgan Stanley: AI Infrastructure Meets Humanoids

Humanoids Semiconductor Opportunity: Could reach $305B in semi sales by 2045 (~24% of BoM from semis, up from 5% today). Potential 1B units/year by 2045. Humanoids could represent 15% of semi spend by 2040.

Top European Picks:

Infineon & STMicroelectronics: Supply microcontrollers.

STMicro: AI vision, Time-of-Flight sensors, Mobileye experience.

Infineon: Inverters, onboard chargers, battery management. BoM per robot ~$500–$700+.

AI Infrastructure (Power):

Shift to 800VDC, GaN/SiC ~35% of server rack BoM.

Infineon highlighted for power efficiency, roadmap, and scale (300mm thin wafer). Strong in 400V/480V (Oberon for NVIDIA), TPUs, Trainium, ASICs. Power semi sales expected to grow from ~$1.5B to $3–4B by FY28.

Long-term bullish on semiconductors in humanoids and power delivery for AI infrastructure. ($STM $IFNNY)

Samsung Electronics is considering outsourcing the back-end design of Google’s 2nm TPU I/O Die due to surging advanced process orders straining internal resources.

Google’s 10th-generation TPU (codename Icefish) is co-designed with MediaTek, with mass production planned for 2028. The compute processor will be made by TSMC on 1.4nm, while Samsung handles the 2nm I/O Die (responsible for HBM data transfer).

Potential partners: ADTechnology, Gaonchips (less enthusiastic, prefer full ASIC projects), and Alphachips (more eager).

Context: Samsung recently secured 2nm customers including Anthropic and DeepX, in addition to Google and Tesla. Back-end design contracts are lower value (tens of billions KRW) compared to full ASIC projects (hundreds of billions to trillions KRW).