The Court of Appeal has dismissed NSSF’s application to suspend the ELRC judgment that declared the NSSF Act, 2013 unconstitutional. In simple terms, the Court has refused to revive an invalid law through interim orders and has insisted that constitutional violations cannot be cured by fear‑mongering about alleged chaos in the pensions sector.

The judges reaffirmed the well‑known Rule 5(2)(b) test which states that an applicant must show both an arguable appeal and that, without stay, the appeal would be rendered nugatory. They accepted that the intended appeal raises at least one arguable point including whether the High Court mis‑characterised the NSSF Act, 2013 as social assistance under Article 43(3) rather than a contribution‑based pension scheme and whether the Bill needed Senate input under Articles 110 and 205. However, they were emphatic that arguability alone is not enough. The Fund had to demonstrate concrete, evidenced risk that a successful appeal would be worthless if stay was denied and it failed to do so.

Crucially, the Court called out NSSF’s alarmist claims of destabilisation, governance quagmire and catastrophic financial loss. The Board alleged paralysis of the Haba na Haba scheme, exposure of over 580,000 informal‑sector members and billions in contributions and even the freezing of emigration and burial grants but placed no audited accounts, actuarial reports or empirical evidence before the Court. Bare assertions could not satisfy the stringent nugatory test, especially where respondents showed that contributions have flowed under Cap 258 for nine years without crisis, refunds, or threats of non‑remittance.

This are some of the commercial interests talking. APTAK and AEA need to come clean what their interest is or what's their grievance. None is about workers but pure commercial interests.

It is absolutely NOT OPEN to FKE to advise employers to use NSSF rates prescribed under a law declared as UNCONSTITUTIONAL. It is not a matter of unilateral employer choice or discretion. Employers must revert to the old rates unless they secure their employees' consent, or they set aside the prevailing court order.

It bears repeating: unless & until set aside, court orders must be obeyed, else we end up in a situation of anarchy & legal confusion.

For clarity, any employer who makes unlawful deductions on an employee's payslip is LIABLE to the employee under both law & contract for the deducted sum. Only permitted coercive deductions are statutory deductions or those arising from a court order. Other deductions must be voluntary i.e. founded on employee's written consent or on a collective bargaining agreement (CBA).

NSSF’s USD-denominated deposits, introduced in 2024, surged by 285% to KSh 2.31 billion in 2025.

This marks a significant shift towards foreign-currency holdings as part of a broader diversification strategy.

The deposits were moved from Equity Bank to Stanbic, Absa, and Cooperative Bank, with Cooperative Bank becoming the dominant custodian.

Mike Macharia: NSSF is made up of the chairman of the board, who is appointed by the President. We have two independent directors who are appointed by CS Labour and Social Security. We have two government representatives, one representing the Labour PS and the other representing the PS National Treasury. Then we have two from the social partners; COTU will give two, and FKE will give two. Finally, we have the managing trustee who is appointed by the board to run the fund on a day-to-day basis #CitizenSundayLive

Auditor General says NSSF’s Sh4 billion idle CBD properties are at risk because some land titles are unclear or worthless, costing the fund potential returns.

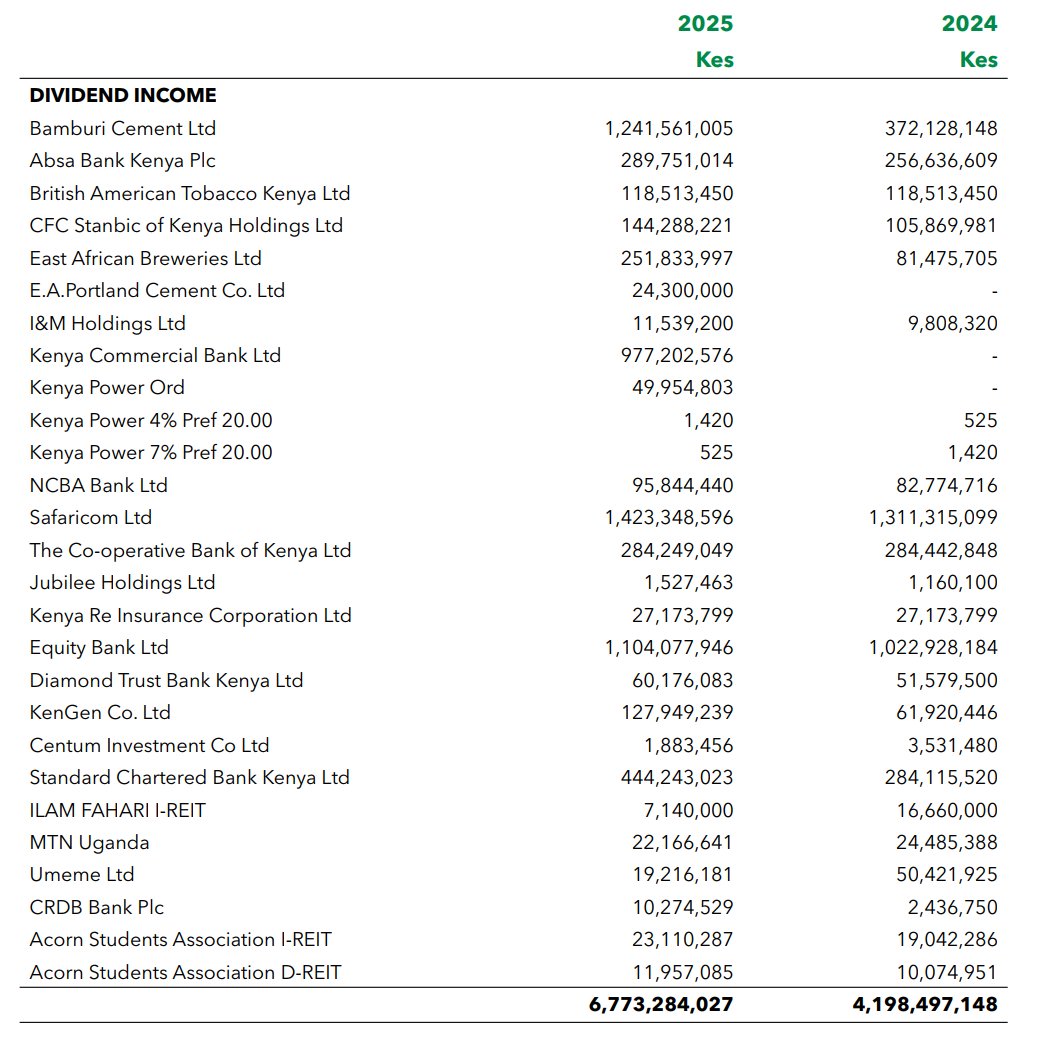

NSSF’s dividend income rose sharply in 2025 to KES 6.77B from KES 4.20B in 2024.

This was driven by strong payouts from such companies as Safaricom (KES 1.42B), Bamburi Cement (KES 1.24B), Equity Bank (KES 1.10B) and KCB (KES 977M).

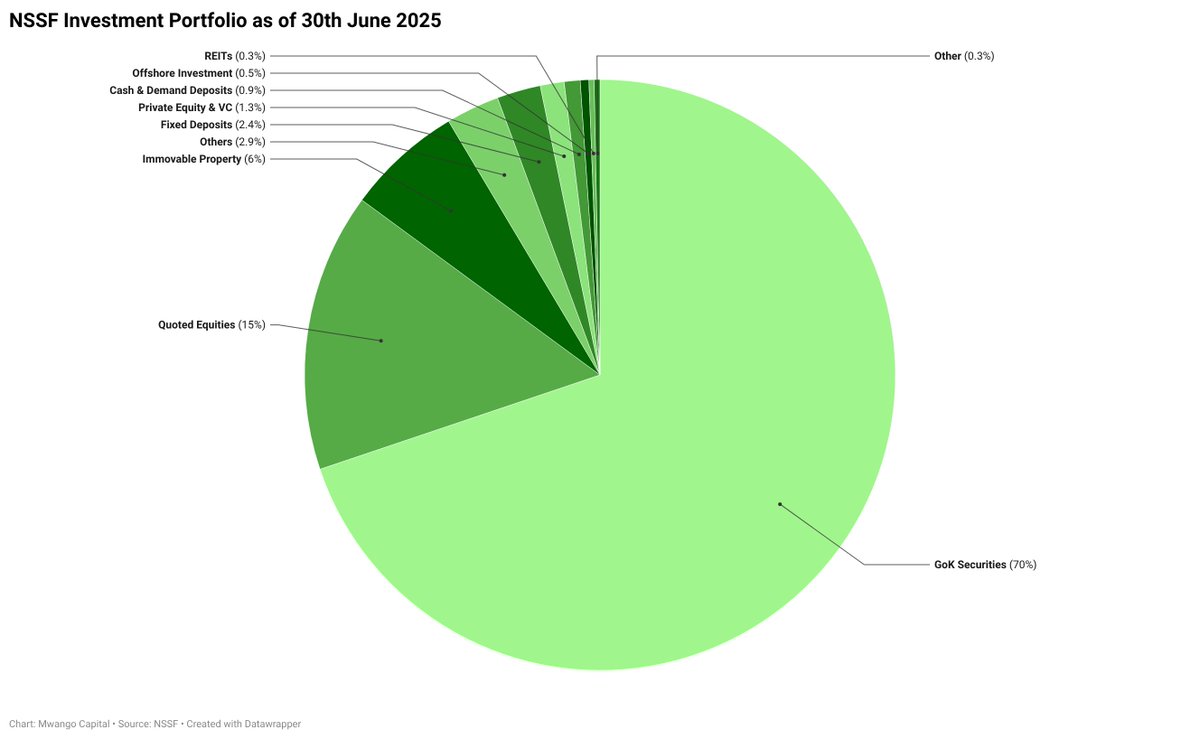

NSSF has allocated about 70% of its assets to Government securities, 15% to quoted equities, and 6% to immovable property, with fixed deposits at 2% and private equity & VC at just 1%.

The portfolio looks tilted towards low-risk, income-generating investments.