Software stocks will make millionaires in the future. Make sure you buy so we can retire in the next 3 years together.

These are my top software picks moving forward:

1. Palantir $PLTR

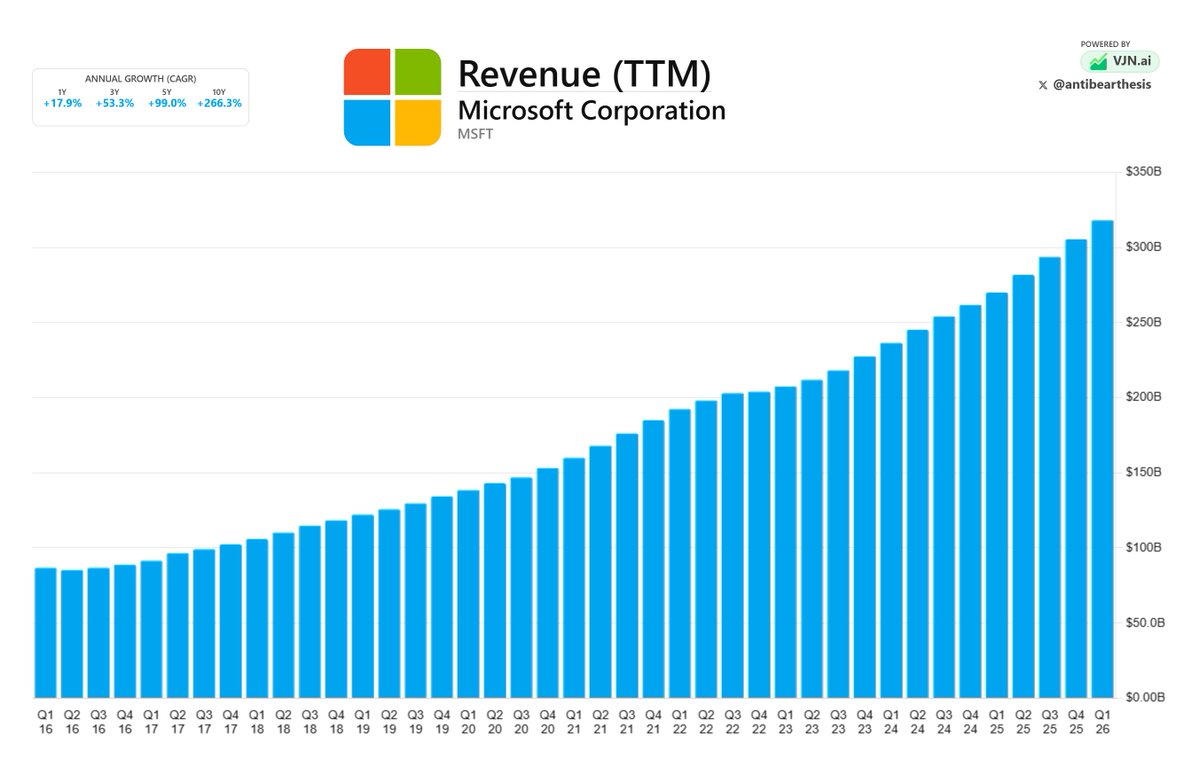

2. Microsoft $MSFT

3. UiPath $PATH

4. ServiceNow $NOW

5. Salesforce $CRM

6. The Trade Desk $TTD

7. Snowflake $SNOW

8. Datadog $DDOG

9. Adobe $ADBE

10. Shopify $SHOP

Software ETF includes $IGV

All my buy and sell signals in Discord @ https://t.co/GaBnArAAKe.

Y si no se cumple? Entonces mi costo de oportunidad fueron esos 20 mil dólares con MSTR siendo la BTCTC más grande del planeta, me voy a cero con gusto,y ESA es la capa de riesgo MSTR no es Bitcoin, Si pierde, pierde por su propia estructura no porque yo haya fallado en la tesis

No estoy equivocado en el fondo; esto dejó de ser económico hace rato y pasó a ser geopolítico, El FOMO que viene va a ser absurdo, 200 acciones de $MSTR hoy son 20 mil dólares si la tesis se cumple, pueden ser 200 mil o más.

Es basicamente esta guerrita en Medio oriente que es la que sostiene el petroleo alto y la inflacion tambien peero eventualmente el conflicto se enfríara y el crudo se normalizara y la Fed sera más dovish y mientras mas se tarde #BTC mas agresivamente subira.

Inflación bajó a 3.5%, mejor de lo esperado y gran parte es el efecto retrasado de la caída del petróleo en junio, Pero ojo, la subyacente sigue en 2.6%, todavía por encima del objetivo de la Fed, así que hablar de deflación extrema como tal es exagerar...

La estadística muestra a #Bitcoin cerca del final de su fase bajista, combinalo con los potenciales impulsadores bajistas:

🎯Strategy (superado)

🎯Ley de Claridad (por definir en julio)

🎯Macroeconomía (en deterioro)

Principales indicadores de valoración y riesgo-rendimiento dicen; acumular Bitcoin cerca a 60.000 dólares representa una oportunidad, en este análisis profundizo en los motivos👇

https://t.co/UStkBLkJ8g

LISTEN TO ME

You should own at least one of these four FinTech companies.

1. $AFRM - Next target: $160

- BNPL leader, +33% revenue growth, Amazon + Shopify exposure, no late fees, rising Affirm Card adoption

2. $NU - Next target: $31

- 135M+ customers, largest customer base of the group, highly profitable LatAm digital banking

3. $SOFI - Next target: $48

- full-stack fintech bank, +41% adjusted revenue growth, 14.7M members, CEO Anthony Noto buying the dip

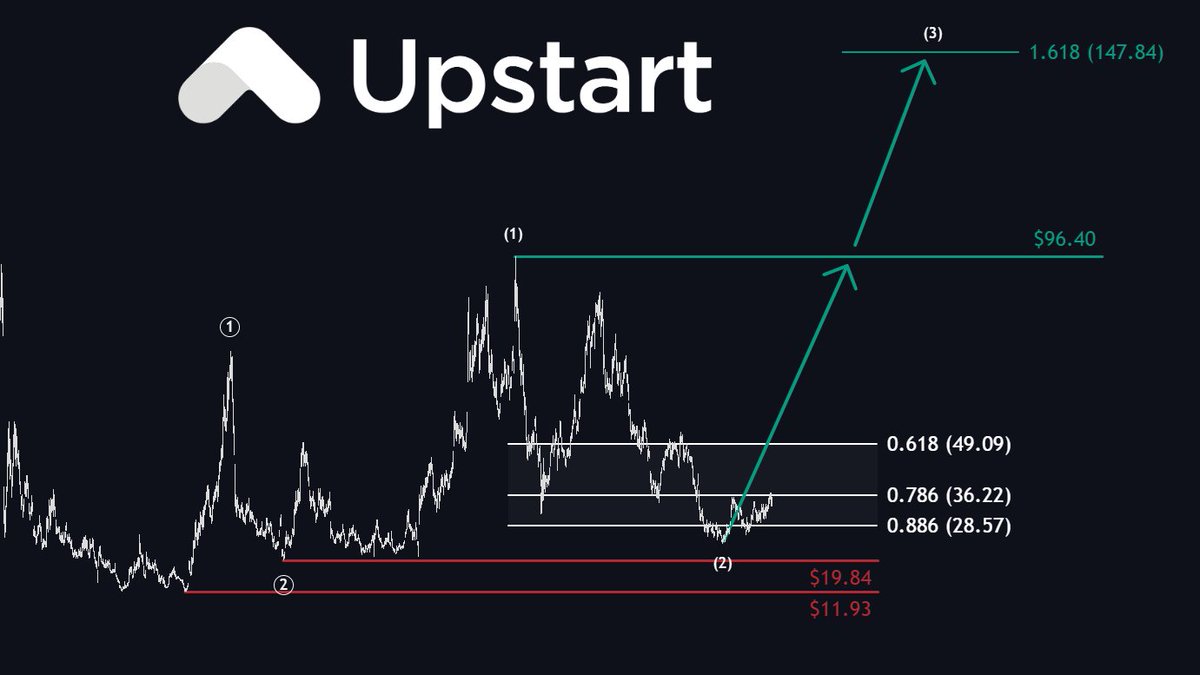

4. $UPST - Next target: $147

- purest AI-lending disruption play, +44% revenue growth, +61% originations, 100+ bank/credit union partners

ASST MOON MATH - ELECTRIC BOOGALOO EDITION

In this projection, Bitcoin goes from $62,653 to $400,000 over 3 years.

BTC multiple: 6.38x. NOT BAD!

But I actually think that ASST could 25x when Bitcoin 6.38x's...

ASST starts today with CEBE NAV/share of $8.03.

At a 1.56x mNAV, that implies a starting price of roughly $12.52.

By the end of the projection, CEBE NAV/share is $178.26.

At a 1.75x mNAV, that implies an ending price of $311.95.

ASST multiple: 24.91x.

So the return stack is:

BTC price: 6.38x

CEBE sats/share: 3.48x

mNAV re-rate: 1.12x

6.38 �� 3.48 × 1.12 = 24.91x

That is the actual moon math.

Bitcoin turns $1 into $6.38.

ASST turns $1 into $24.91.

ASST outperforms Bitcoin by 3.90x on an ending-wealth basis.

Most of the alpha is not the mNAV expansion.

mNAV only moves from 1.56x to 1.75x.

That is a 12.2% uplift.

The real violence is CEBE.

CEBE rises from 12,811 sats/share to 44,564 sats/share.

That is +248% in Bitcoin terms before you even apply Bitcoin’s dollar move.

Relative to BTC, ASST’s outperformance is:

3.48x from CEBE accretion

1.12x from mNAV expansion

3.48 × 1.12 = 3.90x BTC outperformance

On a log-return basis, roughly 92% of the BTC-relative alpha comes from CEBE growth.

Only about 8% comes from the mNAV re-rate.

Now the deeper part:

The claim ratio is the key variable.

Claim ratio = senior claims in BTC / total BTC.

In this model, senior claims are basically the preferred stack net of cash, translated into BTC.

My input to senior claims being issued? An average of $125 million in SATA issuance for THREE STRAIGHT YEARS on a climb to $400k BTC. This might sound like a lot, but by the end of this Bitcoin price run they are actually considerably less amplified than MSTR today.

So when the claim ratio is high, the common is more levered to the residual Bitcoin equity.

When the claim ratio falls, the common gets safer, but the amplification starts fading.

Claim ratio starts at 46.6%.

It peaks around month 5 at 53.4%.

By month 12, it is already back down to 48.9%.

By month 24, it falls to 36.1%.

By month 36, it is down to 24.9%.

That is the hidden curve.

Early in the model, the SATA issuance is extremely powerful because the Bitcoin balance sheet is still relatively small.

A $150M/month preferred issuance program is a sledgehammer against a $1B–$5B Bitcoin NAV.

But by year 3, the BTC stack is enormous.

At month 0:

Net senior claims: $580M

BTC NAV: $1.25B

Claim ratio: 46.6%

At month 12:

Net senior claims: $2.38B

BTC NAV: $4.87B

Claim ratio: 48.9%

At month 36:

Net senior claims: $5.98B

BTC NAV: $24.04B

Claim ratio: 24.9%

The preferred stack grew massively. But the Bitcoin balance sheet outgrew it. That is why the leverage bleeds out of the structure over time.

And you can see it directly in the CEBE growth rate:

Year 1 CEBE/share growth: +81.9%

Year 2 CEBE/share growth: +50.7%

Year 3 CEBE/share growth: +26.9%

Still absurd.

But the amplifier decays. The reason is brutally simple:

SATA is issued in dollars.

Bitcoin is compounding in dollars.

And every month, the same $150M buys fewer BTC.

Month 1 BTC bought: 2,394 BTC

Month 12 BTC bought: 1,359 BTC

Month 24 BTC bought: 732 BTC

Month 36 BTC bought: 395 BTC

Same dollar hammer.

Much larger Bitcoin wall. That is why the claim ratio falls, and that is why the CEBE growth rate cools.

That is why ASST would need to issue a lot more SATA to keep the amplification juiced.

Using the model’s month-12 claim ratio of 48.9%, keeping that ratio through month 36 would require roughly $12.0B of preferred balance by the end.

The model ends with $6.18B.

That is a ~$5.78B gap.

On a simple end-state basis, from month 12 to month 36, that means the issuance pace would need to be closer to ~$391M/month instead of $150M/month.

Roughly 2.6x the modeled issuance pace.

And if you solve it dynamically, it gets even more aggressive, because every new dollar of SATA also buys BTC and expands the asset base.

$150M/month can keep growing CEBE, but it cannot preserve the early leverage intensity once the Bitcoin NAV gets huge.

To keep the machine in full demon mode, SATA issuance has to scale with the size of the Bitcoin balance sheet.

Sooo.... not financial advice, but in my HUMBLE OPINION, that means the best opportunity is NOW :)

Mag 7's will continue to make you rich. I am a buyer every single month rain or shine.

Here's what to expect moving forward and when to buy:

1. NVIDIA $NVDA

2. Amazon $AMZN

3. Microsoft $MSFT

4. Meta Platforms $META

5. Apple $AAPL

6. Tesla $TSLA

7. Google $GOOGL

8. RoundHill Magnificent 7 ETF $MAGS

All my buy and sell signals in Discord @ https://t.co/GaBnArAAKe.

Bitcoin and the crypto sector is a buy now and lower.

Robinhood $HOOD has been doing very well, so this can be a leading indicator for the rest of crypto to do well.

1. $BTC - Bitcoin

2. $MSTR - Strategy&

3. $COIN - Coinbase

4. $HOOD - Robinhood

All my buy and sell signals in Discord @ https://t.co/GaBnArAAKe.

$HIMS

One of the cleanest long-term setups in the market, but the fundamentals still need to prove themselves.

Guidance has been raised repeatedly, yet the company hasn't grown significantly over the last months, while margins collapsed.

But if this plays out, this stock has insane upside potential.

$130 are easily possible in this cycle, from a technical perspective.

Bitcoin metrics used to cost thousands per year.

BlockHorizon just opened everything up, 100% FREE data & charts:

✅ All metrics, daily updates

✅ Full historic data

✅ Unlimited alerts

✅ CSV+XLS+JSON downloads

Same data as other providers. No paywall

👉 https://t.co/KEK5tp3wT9