@DollarCostAvg $NOK I did same yesterday! The opportunity to buy under the insiders purchase price sounds like a really good idea! I’m very confident for the near future although I keep cash to reinforce more in case or another dump in the coming days/weeks regarding the market trend

I have $NOK price target of $20 since it was $10 few weeks ago.

Here is why i think $NOK has chances of achieving it sooner than most people think.

1. The AI & Cloud Infrastructure Inflection.

The most critical driver of Nokia’s multi-year breakout is its rapid adoption within data centers and hyperscaler networks.

Explosive Growth

In Q1 2026, Nokia's AI & Cloud segment revenue grew 49% year-over-year, now making up roughly 8% of total group sales.

Massive Order Backlog

Nokia booked €1 billion in AI & Cloud orders in a single quarter against €350 million in realized revenue (a book-to-bill ratio of nearly 3x). This builds a massive backlog and offers immense revenue visibility stretching well into 2027.

Hyperscaler CapEx Super-Cycle

Global hyperscaler CapEx projections for 2026 have been massively upwardly revised from an initial $540 billion to over $700 billion. Nokia is capturing a direct slice of this capital allocation as cloud giants aggressively scale backend architecture to handle AI workloads

2. Optical and IP Networking Dominance (The Infinera Tailwind)

Nokia’s Network Infrastructure division is benefiting directly from its acquisition of Infinera, establishing a commanding position in optical and next-generation routing.

Infinera Integration

The integration is running ahead of schedule, driving immediate cost and portfolio synergies. Nokia’s Optical Networks segment alone posted 20% organic growth in Q1, driven heavily by demand for 800G pluggable and associated systems.

Vertical Integration as a Moat

Nokia is aggressively scaling its San José Indium Phosphide (InP) semiconductor fab (Fab 2), targeting production starts later in 2026 with full material impact in 2027. This facility expands Nokia's InP capacity by up to 20x. In a supply-constrained environment, owning its own component manufacturing and optical subsystem supply chain gives Nokia a massive competitive advantage over fabless peers.

IP Routing Breakthroughs

Outside of optical, Nokia is landing critical design wins in IP Networks with multi-rail solutions tailored for AI data center fabrics, diversifying its revenue drivers beyond optical hardware.

Nokia has the edge and is making a comeback. I wouldn’t be surprised if $NOK doubles from its current price before the end of the year.

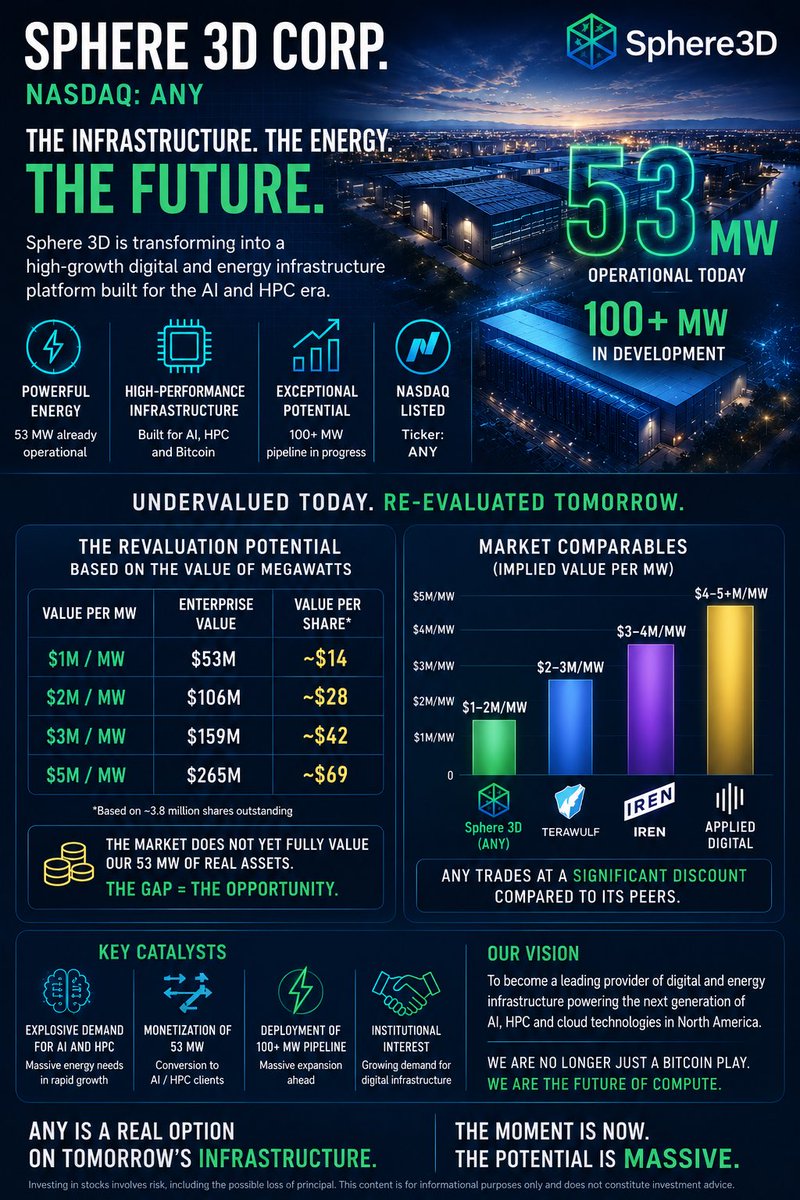

$ANY is still the most undervalued AI data center play on the market, green on a red day, their current CEO after their recent merger with Cathedra is ex HUT8 CFO, next target is $7

Asked Claude to find me a data center company that is valued below $1M per MW ($MarketCap/MW) that is not severely distressed or heavily indebted. Lol.

The timing of the HPC market coming to smaller clusters with hash price near all time lows is insane.

Re-Rate Cometh.

$ANY just wait until the other data centers are done with their pull backs (the big boys). Once those start running again, thats when this will go parabolic too.

For now, its so undervalued, thats its still slowly creeping up while rest are pulling back

$NOK is STILL my next 1000% play – New price target $25 🎯

Since I dropped that post on April 29, the market has finally started catching on.

$NOK has ripped another ~20%+ higher, hitting fresh 16-year highs around $16.60 while most “AI pure-plays” are getting choppy. But we’re still early.

Nokia isn’t the flip-phone company anymore. It’s quietly becoming the picks-and-shovels backbone of the entire AI infrastructure boom, and the momentum is accelerating.

Here’s the updated thesis:

• AI-RAN + NVIDIA partnership is live and scaling

Nokia’s co-development with NVIDIA is already deployed with BT, Elisa, NTT DOCOMO, Vodafone and others. This isn’t future hype, it’s the bridge to AI-native 6G, and Nokia is years ahead of Ericsson and everyone else.

• Optical & data center explosion is just getting started

Q1 2026 already delivered +49% AI + cloud revenue. They raised their addressable AI fiber/hyperscale market to a 27% CAGR through 2028. The Infinera acquisition is paying off big time, hyperscalers are spending like crazy on optical networking for AI clusters, and Nokia is one of the few players that can actually deliver at scale.

• Earnings momentum keeps getting stronger

Beat Q1 estimates, operating profit +54%, gross margins expanding, full-year guidance reaffirmed and raised. Just this week they launched a new AI networking lab to accelerate co-innovation with partners. The flywheel is spinning.

• Valuation still has massive rocket fuel left

Even after the run, $NOK trades at a fraction of pure AI networking peers. A modest rerating to where those names sit (20-30x forward) puts us at $25+ per share in the next 12-18 months, before 6G really kicks in. From here, that’s another 50%+ leg higher, with multiple legs possible over the full cycle.

This isn’t a meme stock. This is real execution, real revenue inflection, and real AI tailwinds that the market is still underpricing.

I’m still loading the boat on every dip.

New price target: $25

(As always, this is my opinion, not financial advice. Do your own research.)

I’ve taken a 1% allocation in $ANY

$24M market cap. 53MW of live, energized data center infrastructure. In a market where power is the scarcest asset in tech.

Either this gets a hosting tenant signed and re-rates 30-100x, or I lose a small bet. That’s the trade.