Look at this photo. Water pooling at the base of the building, right where the downspout dumps it.

That concrete splash block is doing the opposite of its job. Instead of throwing water away from the foundation, it’s holding a puddle and feeding it back toward the wall. And the grade right here isn’t helping. It’s moving water into the building, not away from it. The splash block is the symptom. The drainage is the disease.

This is how you kill a building slowly.

Water against a foundation doesn’t announce itself. It seeps. It wicks up into the wall and the framing, and it sits there through every rain. Give it a season or two and efflorescence blooms on the block, the ground-floor units start to smell, then mold sets up behind the drywall. Give it a few years and the foundation itself starts to go. By the time a tenant complains, the cheap problem already turned expensive.

A lot of times I see owners jump straight to ripping it out and installing new drainage. Start basic instead.

Turn the splash block the right way so it throws water out, not back toward the wall. Slope the soil and the mulch bed down and away. Then go find the drainage boxes, because on an older property nobody has cleaned them in years. They’re packed with leaves and dirt and they haven’t drained since the last management company. Check that every downspout is still connected and the original system actually works.

Half the time, that’s the whole fix. Nothing installed, nothing rebuilt. Just the maintenance somebody skipped for a decade.

If the bones are truly gone, then you go dramatic. Tie the downspout into buried PVC, pitch it right, and run it out to the lot drain.

Turning a block and clearing a drain box costs an afternoon of labor. New PVC to the parking lot is low four figures. Foundation repair runs five to twenty grand, and mold stacks on top, and that’s before the units you can’t rent while it dries out.

Water is the cheapest of problems you’ll ever catch early, and one of the most expensive if you ever neglect it

Show me weeds in the parking lot and I’ll show you a property leaking money.

I walk a lot of properties. The first thing I check isn’t the leasing office or the model unit. It’s the parking lot.

I spotted a beer bottle on the ground at a site once. Came back the next week. Same bottle, same spot. The on-site team had walked past it so many times it had gone invisible to them.

A weed in the asphalt is that beer bottle. It costs nothing to deal with. A guy with a string trimmer clears it in few minutes. The weed is the tell.

A single weed won’t lose you a resident. A property that stopped seeing them will.

Now, the resident isn’t going to call and complain about a weed. They’ll mention the AC or the gate code, never the weed. But the weed, the burnt-out breezeway light, the work order that’s sat for nine days, the trash by the compactor on Sunday, that’s all the same thing. Someone stopped minding the details. Residents feel it long before they can name it, and when the renewal letter lands they don’t argue the rent, they just quietly let the lease run out, and you eat another turn without ever tracing it back to the weed in the lot.

Put a number on it. The NAA found most firms spend $1,500 to $3,500 to turn one unit, and almost one in five spend more. Other industry data pegs the all-in average near $3,900 a door in 2023 (Zego). The weed was free to pull. The move-out it warns you about runs four grand.

This is the management gap. Corporate has standards. Real ones, written down, agreed to in a meeting nobody from the site attended. Then there’s what’s actually on the asphalt. The space between the two is where NOI quietly drains, one ignored detail at a time.

The weed does you a favor. You can’t see a slow work order or a rude phone call from the parking lot, but the weed you can see, and it’s free information you already own and walk right past.

So walk your properties. Too big to walk them all? Pay for an independent audit. Do not send your regionals to inspect their own sites. That’s the fox guarding the henhouse, and the report comes back the same every time: everything looks good, nothing to report.

Imagine that.

G&A Expenses explode for one main reason. The person spending isn't the person paying.

Yesterday, I went line by line through the general ledger on a 176-unit property. Not the summary. The actual ledger. Every recurring charge.

Three stood out.

The property inspection software: $270 a month. Our industry knows the one. Yes, it adds photo logs and audit trails. On one stabilized building, I'm not paying a subscription for that. The same job gets done for a fraction of the cost, or in-house.

The AI leasing tool: $703 a month. And I love AI. I build with it daily and I think it remakes this business. The vendor will tell you one extra lease pays for the year. Fair. So I checked what it actually closed. The math wasn't there.

Not yet. That gap is the whole reason AI is hard to sell right now. Hold it against the hard numbers, and it often folds.

The marketing design templates: $95 a month. Templates I can make in two minutes with ChatGPT or Gemini for free. Canceled.

Entrata and Yardi both bundle their own inspections, AI leasing, and marketing tools. Built in. So there's a real chance you're paying a third party for something your platform already does. Or paying for both and using neither well.

I asked my team why they couldn't use the built-in tools. The answer: the reporting was lacking.

Both platforms have deep custom report builders. Yardi runs YSR and custom SQL. Entrata lets you configure a report down to the field. Learn the tool and you can build any report you want. The data is already sitting in the system.

So the reporting wasn't lacking. The skill to pull it was. And I paid a third party to cover for a skill gap on my own team.

Now the deeper problem. It's older than any software.

Multifamily runs on a two-party payer system. The owner pays. Someone else does the spending.

You feel the cut. Of course you do. It's your money. But it's buried in a budget line you approved once and stopped reading. Invisible by design.

And yeah, I approved every one of these at some point. The system is built so you approve once and forget. The person clicking "subscribe" isn't the person signing the check.

So the costs mushroom. Pull your G&A from a few years back and set it next to today. The jump will surprise you. It crept in one $95 subscription at a time.

Is this whack-a-mole? Yes. You kill three, and two show up next quarter.

Do this. Get the financial statement. Then go past it, into the general ledger. Read every recurring charge on the property. One question per line.

Not "can I defend this?"

"Can they?"

Make the people spending your money justify every dollar. The ones who can't go away.

The ledger tells the truth. The budget often hides it. Go find those small leaks; they add up.

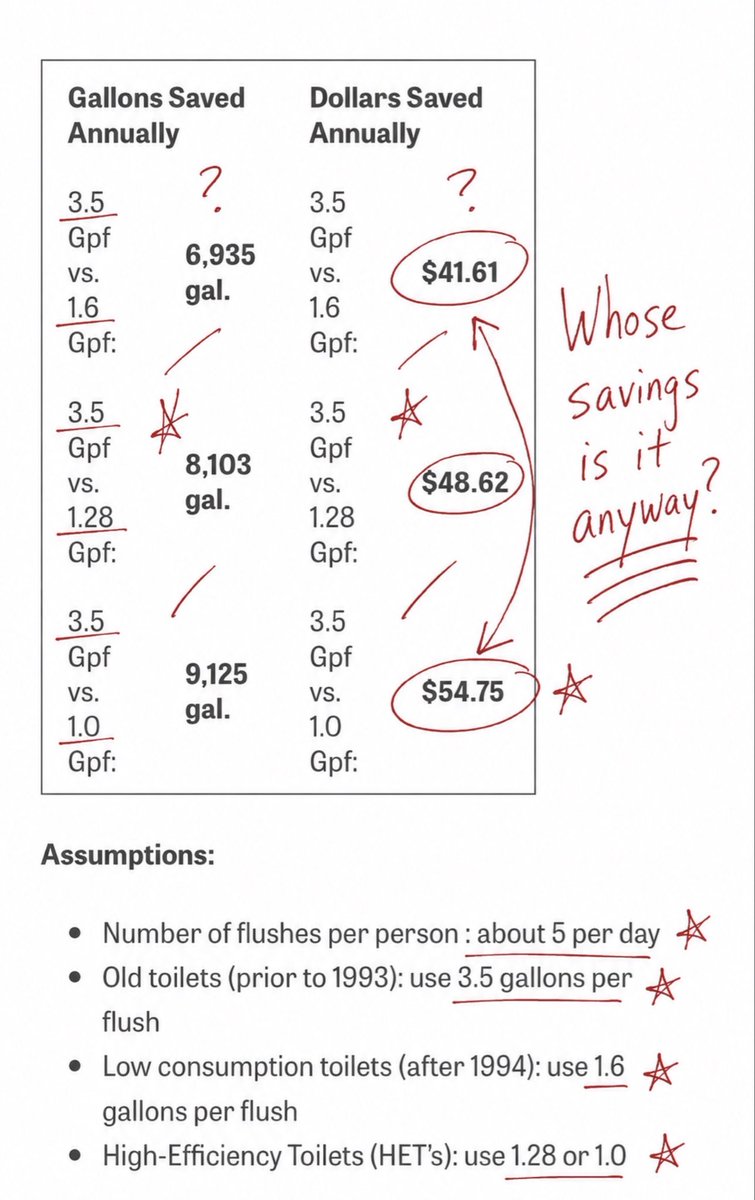

Your green upgrade cut the bill 20%. So why did you keep only a quarter of the savings?

Years ago I went deep on net zero. Studied how the Germans built Passivhaus, sat in a LEED course genuinely fired up about it.

Then I started arguing with the instructor.

I said, my bank doesn’t lend against a carbon offset. He looked at me like I was crazy. But it was a fair question. Show me where the savings or my green projects don’t work.

I’ll give you a great example. I had a property with Georgia Power poles on it and a common area electric bill that made me wince. So I backed into what those poles actually cost me, every dollar, the materials rental and the power. Their pole program was charging me an implied 36% IRR.

Thirty six.

I tore the poles out, mounted LED fixtures on the buildings, ran them off the existing meters. The bill dropped and the job paid for itself in less than 16 months. Easy to measure, easy to defend to a lender.

So why not run the same play inside the units?

Because the second you walk through the apartment door, the meter changes names. It belongs to the resident now. Same bulb, same physics, but the return walked out with the meter.

And no, you can’t just charge more for the efficient unit. The renter shops base rent and meets the utility bill after he signs, if he ever runs the math.

Now run the water math, because the vendor’s deck quietly skips this part. Your building water bill is $100k and low flow devices cut usage 20%. If you pay the whole bill, you bank $20k, clean. But if you bill 80% back to residents, you keep $4k and they keep $16k. Same device. Your return just fell 80%, and the brochure still shows the twenty grand.

And yes, the bank pays now. Fannie and Freddie knocked 10 basis points off my rate for documented energy and water savings, plus more loan proceeds. Real money. But that’s the workaround, by the way. It took Fannie putting cash on my side of the table to make my residents’ savings worth my time.

Fannie even underwrites the split. They credit me for 75% of my projected savings and 25% of my residents’. The lender knows exactly who keeps the money. Measured dollars, never carbon for carbon’s sake.

I’m not against the science. I wanted it to work, and the technology works fine. Green pays cleanest when you hold the meter. Split the savings with your resident and the math goes fuzzy, no matter how good the pitch sounds.

Show me whose name is on the meter and I’ll tell you whether it ever gets installed

Most of your operating costs were decided at the closing table.

Real estate is a lobster pot. Easy to swim into, hard to back out of. The upside is the bait. You chase it in, the door shuts behind you, and now you own whatever it costs to run the place.

I read a Bisnow panel of Houston operators this week. Insurance, labor, taxes, all turned into deal killers, they said. True. But watch how they talk about it. The cost shows up, and then they go to work. Renovate. Trim R&M and payroll. Survive to next year. I'm old enough to remember the whole industry yelling "survive till '95." Some things don't change.

That's the back half of the story. The front half happened before they owned the building.

Take labor. Buy a 98-unit deal, and you still have to staff it, a manager and a tech for 98 doors. Buy 212 units in the same town, with a much lower payroll number to run it. One deal drags a heavy payroll line for as long as you own it. The other runs lean from day one. Same work. The math was set before you leased a single unit.

It runs down every line. A 1965 building costs more to keep standing than a 2015 build, year after year. Coastal address and your insurance is on another planet. Student housing, you're hiring extra leasing staff. Small market with no employers nearby, try recruiting a maintenance tech without overpaying.

A property landscaped in Phoenix rock costs less than one wrapped in grass. Interior hallways and elevators eat money you will never get back.

You can't manage your way out of any of it. You bought it that way.

And don't assume the heavier cost load comes with the rent to carry it. Sometimes it does. Plenty of times it doesn't. A coastal address can rent for less than an inland one, sitting next to a college or a busy downtown. Cost and rent don't always travel together. Assume they do, and the market corrects you.

Once you own it, you get a few levers. The controllable decisions you make, within each expense line, drive most of the results. The rest you just feed. I've fed the expensive kind. You learn it the slow way.

Now, we all underwrite the expense line. I'm not saying they don't. The real question is whether you see how the variables are hardwired against you before you sign. You pull up the IRR, and it passes your hurdle rate. But not all IRRs are created equal. Every deal has an expense DNA, and it gets set the day you buy. It's the vintage, the coast, the unit count, the construction, all the things that decide how high your costs start and how hard they swing. Some deals are wired lean. Some are wired heavy and jumpy from day one. Two of them can hand you the very same return. The number won't tell you which. The expense side will. Read it going in.

https://t.co/7LWn3AisUO

A CPA fed twelve months of bank statements into Claude. Not exports. Image scans. 6,700 transactions. Seven minutes later, the balance sheet footed.

My first thought was the right one. No way that's real.

It was. He ran a 40-person firm and sat there drinking his coffee while the thing classified 6,700 lines and flagged its own guesses.

Cool trick. But it hands you a finished balance sheet and won't tell you how it got there. Which transaction went where, and why. A black box that foots. Try defending that number to your bank. Or the IRS.

So he bolted on one piece. Beancount. A plain text file that holds real double-entry books. Open source since 2007. Free.

Now every number on that statement traces back to a line you can read. Plain text, so it drops into Git and every change is logged, what moved and when. It even checks itself: tell it an account should hit a number on a date, and it flags the mismatch. You stop taking the machine's word for it. You check its work. And it's a real file you can share or reopen later.

Almost twenty years it mostly sat there. Filling it and classifying it took a human or a subscription. That cost just went to almost nothing.

Here's where it stopped being a party trick for me.

Every deal we get under contract, I get the seller's bank statements and their T12. The question: is the income they're selling me the income that exists?

Pad it, and I pay for the padding in the price.

So me or my analyst pulls it apart by hand. Export the transactions. Retype the amounts. Back out the reserves, the draw requests, the non-cash junk. Then tie what they claim they made to what actually hit the bank. Hours of it. Every deal.

On the next deal, that pull and tie-out is the machine's job, not my analyst's. It leaves a file I can check.

Now the part the hype videos skip. A bank statement shows cash moved. It doesn't tell you whether the story is honest. It won't catch collections yanked forward to pad the trailing twelve. The reconciliation gets me to the real question faster. It doesn't answer it. That still takes a person who's been lied to before.

Someone will build the real AI ledger. I'd bet on it. And it won't look like QuickBooks, which is a database with a form on the front of it. The next one reads a roof invoice, a tenant text, a bank feed, even a voice memo, and books all of it, then lets you ask your books a question instead of clicking through them.

That's the destination. This isn't it.

This is a free text file and a model that already exists, doing the boring, expensive part today while somebody builds the real thing. A bridge. I'll take the bridge.

Credit to Jason at Jason On Firms, he put me onto this. His video and the repo are in the comments. If you underwrite deals or do this type of work, point your model at the repo and go.

Here is the prompt for the Google Review Mining of your property you can use to build out your Claude or Code Skills. It will at least give you a framework. https://t.co/7mrbJU90Od