@shubham1492 And one needs to check the capability of leader vs next line of players

For eg Raghav and Mono have big gap in terms of product quality, moat, tech etc and one can’t simply do relative valuation to justify buying no2 player

That’s the lesson I have learnt

Disc: One can go through latest concall/ PPT to have more info. Just sharing what I find interesting in Special sits, no recommendation to buy or sell. Always do your due diligence.

#SpecialSituation#Indoborax Promoter change

From capital misallocation to prudent deployment, a tale captured in two images

Image 1: Cash generated in the business used for buying a residential property worth 42 crores instead of growing the business or returning the cash to shareholders while company had 70 cr Mcap

They have guided for 250 cr topline in FY27 with future growth in high double digits along with some margin expansion, forward integration, new chemistry/products, execution is yet to be seen.

An interesting company to track with new energy, experienced team and prudent capital allocation at play.

NVIDIA IS BUYING ITS OWN CHIPS AND CALLING IT REVENUE

And your retirement account is secretly holding the bag.

This scheme is literally straight out of the Enron playbook...

In January 2026, a special purpose vehicle called Valor Compute Infrastructure was created with one purpose:

Buy Nvidia's chips so Nvidia could book the sale as revenue.

Valor raised $5.4 billion and purchased over 100,000 of Nvidia's GB200 GPUs.

But $1.9 billion of that money came FROM Nvidia itself.

Nvidia invested $1.9 billion into the shell company, then sold that same shell company $5.4 billion worth of its own chips and booked every dollar as revenue.

It's the Girl Scout whose dad bought all the cookies and then she wins the sales contest because Dad was the customer. Except this Girl Scout is a trillion-dollar company and the cookie sale is $5.4 billion.

But it gets MUCH worse:

The remaining $3.5 billion in financing came from Apollo Global Management. Apollo structured the debt, packaged it into securities, and then sold those securities to Athene.

And guess who Athene is? Apollo's OWN insurance subsidiary. The one that sells fixed annuities to American retirees as safe, conservative retirement products.

Follow the chain:

Nvidia funds a shell company with $1.9 billion. The shell company buys $5.4 billion in Nvidia chips. Apollo finances the remaining $3.5 billion. Apollo sells the debt to its own insurance arm. That insurance arm packages it into annuity products and sells them to retirees who think they're buying something safe.

The retirees have no idea that their retirement savings are now backed by 100,000 computer chips sitting in some data center that will be worth pennies on the dollar in three years.

Now look at what's happening inside Athene:

$74.2 billion in US reserves but $217 billion in assets have been shifted to a Bermuda-based captive insurer, outside normal US regulatory oversight.

$103 billion of that portfolio (roughly 35%) is classified as Level 3 assets. That means there is no observable market price.

These assets are valued by internal models, not by actual markets.

And sitting on top of all those unpriced assets? 16.6x leverage.

If you're getting flashbacks to 2008, you should be.

Back then it was mortgages bundled into securities that nobody understood, sold to investors who had no idea what they were holding, rated as safe by agencies that never looked under the hood.

Today it's GPU-backed securities. Computer chips bundled into structured credit instruments, routed through an offshore insurance subsidiary, and sold to you as a retirement product.

The collateral is 100,000 GPUs leased to a single customer through an xAI subsidiary. If xAI stops making lease payments for any reason - financial distress, a pivot in strategy, anything - the entire structure unravels.

And Nvidia releases new architectures every year, so each generation delivers dramatically more compute per watt. A 5 year lease on technology that's obsolete in 2 years creates a mismatch that should terrify every annuity holder in America.

Every single step in this chain is technically legal. The SPV is legal, the lease is legal, Nvidia's equity stake is legal, the securitization is legal, and the Bermuda transfer is legal.

But legality and legitimacy are not the same thing.

I've seen every trick Wall Street has ever pulled in my 45 years of doing this.

And what I'm looking at right now is a pipeline that takes AI infrastructure risk, launders it through 8 layers of financial engineering, and deposits it in the retirement accounts of Americans who never agreed to fund Elon Musk's data centers.

In 2008 it was mortgage-backed securities.

In 2026 it's GPU-backed securities.

Different asset. Same greed. With the same ending.

George Soros taught Ron Baron one lesson that made him $20 billion

"if you have identified and done the work on a business that can grow tremendously - you can't own enough of the greatest idea you've ever had"

Baron put $400 million into Tesla and made $7 billion - then put $2 billion into SpaceX and made $13 billion - 54% compounded per year for 9 years

he just placed a $1 billion order at the SpaceX IPO - "I'm 83 years old - I can't imagine ever selling a single share in my lifetime"

bookmark and watch it today ↓

@ishmohit1 People with 50-60% hit rate have done very well in beating the index, their %gains > % losses, basically letting winner positions run lead to phenomenal outcomes.

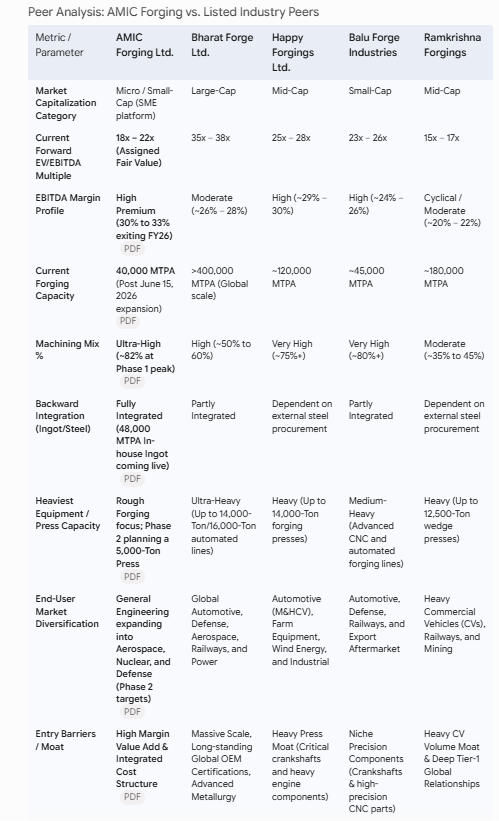

#amicforging

New capacity(Phase-1) coming live in next 15 days

Phase-2 funding is already secured and will add significantly to the capabilities and supply to niche industries

Marquee name in pref allotment and stock is coming out of 2 years of consolidation.

*Expecting earnings to go up by 5x here*

Interesting company to study.