펌프펀은 아직 죽지 않았다

솔라나 밈코인 $PENGUIN 이 바낸 알파로 상장하면서 173밀을 찍고 내려왔네요.

불과 8일만에 일인데, 역시 아직도 졸업자를 만들어주는 장은 밈코인 시장인가요

다음은 무엇이 될지 SOL 밈코를 계속 해봐야 할 것 같습니다.

다들 부~자 되는 26년 만들어봅시다!

🦺 당신의 신원은 정말 안전한가요?

@idOS_network@wallchain

온라인에서 우리는 하루에도 수없이 많은 신원 확인을 거칩니다.

거래소, NFT 마켓, 게임, AI 서비스 등에서 말이죠.

이 때마다 이름, 얼굴, 여권, 신분증 또는 지갑 주소를 제출해야 합니다.

문제는 무엇일까요?

모든 플랫폼은 해당 데이터의 사본을 저장합니다.

단 하나의 서버에서 해킹 당하기라도 한다면

당신의 신원은 수백 곳으로 유출될 수 있습니다.

바로 이 부분에서 idOS가 등장합니다.

idOS는 사용자가 자신의 데이터를 소유하고 암호화할 수 있도록 설계된 웹 3.0 신원 인프라입니다.

✅ 여러 서비스에서 재사용 가능�� 단일 KYC

✅ 언제든지 접근 권한을 부여하거나 취소할 수 있습니다.

✅ 중앙 서버 없이 암호화됩니다.

idOS의 FaceSign을 사용하면 지갑이 실제 신원과 직접 연결되며, 당신의 얼굴이 서명이 됩니다.

누군가 당신의 지갑을 가지고 있더라도, 당신이 직접 가지고 있지 않으면 작동하지 않습니다.

AI가 얼굴을 위조하고 사기가 지갑을 노리는 시대에, 우리가 누구인지 증명하는 방식도 진화해야 합니다.

idOS는 안전한 디지털 신원 확인을 위한 새로운 기준을 제시합니다.

데이터 소유권이 중앙 기관이 아닌, 바로 당신에게 있는 세상입니다.

늦지 않았습니다.

지금이라도 idOS 프로필을 만들고 참여해보세요.

idOS 프로필 만들러 가기

👉 https://t.co/u3oMNvS6xK

We’re Not Here to Defend KYC - We’re Here to Fix It

Let’s be honest: KYC sucks.

And yes - even with @idOS_network, you’ll have to go through it once before we can make it easier.

KYC was written for a different world. The first rules appeared in the early 1990s - before the internet connected everyone, before stablecoins, before open finance. They were designed for local banks, paper forms, and fax machines - and they’re still what we all use today.

The result? A system that penalizes people for where they were born instead of what they do. It blocks entire countries, makes onboarding painful, and still fails to stop crime. Some of our own team members who helped build the app aren’t allowed to fully use it. That makes me both sad and angry.

Fake accounts and stolen IDs are sold on the dark web, while legitimate users face endless friction. Even regulators struggle to process the flood of reports - Germany’s FIU, for example, has faced major backlogs for years.

So yes, KYC is broken. And yet, our industry mostly looks the other way. We preach decentralization, but still store ID copies in centralized silos. We’re decentralized in the streets and centralized in the sheets.

And no - zk doesn’t fix that.

Don’t get me wrong - zero-knowledge proofs are a brilliant technology. But look at the pattern: every few months a new zkKYC startup gets funded - and a few quarters later, its founders and investors discover that this isn’t how KYC actually works. They pivot into some over-marketed centralized “data vault,” or fail to get traction - often both.

If we’re too afraid to dive into the sewage of the existing system and get our hands dirty, we’ll never fix it. zk helps once you have decentralized storage and real data-access guarantees. It doesn’t replace compliance reality - it just makes it amazing once you’ve built the plumbing.

At idOS, we think it’s time to fix it - not ignore it, and not shy away from the hard parts.

We have to meet the system where it is today, and build the bridge to what it should become.

Here’s what we can already do better:

🔁 Reusability: Verify once, reuse your credential across apps - in a compliant way.

👁️ Transparency: Know exactly what data is stored and who you’ve shared it with.

🌍 Inclusion: Support as many countries as the law allows.

🔐 Safety: Avoid duplication and encrypt every record with your personal key - no data honey pots.

We’re plumbers, not politicians. We can’t rewrite global law, but we can design better rails around it.

Here’s what we can’t change today (yet):

🚫 The FATF and EU “high-risk” lists restrict service to users in certain countries. That’s not our rule - it’s the one our financial partners must follow.

🗂️ Regulated providers must retain KYC data for a few years by law. With idOS, they can keep secure access without downloading it, and data is automatically deleted when the retention period ends.

🧩 Some partners still rely on their existing centralized KYC providers for data storage. We’re meeting clients where they are today, so our system works now - and can upgrade them later.

And here’s what’s possible with idOS already:

Once the initial check is done, KYC providers delete your data. It stays only with the regulated entity that needs it - not with the verification vendor. That’s how we remove unnecessary copies while staying compliant.

It’s early days, and there’s plenty of work ahead - but this is a start.

And it can only get better from here.

idOS is open-source, public-good infrastructure. You can inspect it, criticize it, or help improve it. Community members are already contributing to better privacy, storage, and UX through encryption and MPC.

So please - don’t shoot the messenger.

We’re not defending a broken system.

We’re the ones going into the drainage to clean it up.

KYC still sucks - join us in making it better.

그냥 열심히만 하면 다 보상 받는다고?

@RiverdotInc@River4fun

최근 넷플릭스에 공개된 드라마

"서울자가에 대기업 다니는 김부장 이야기" 를 보셨나요?

대기업에서 20년 이상 근속하며

누구보다 성실하게 일했지만

그러나 상무 승진을 하지 못하고 있는 김부장

김부장이 승진하려면 어떻게 해야 했을까요?

직장인으로서 느낀점도 있지만

리버와 리버단의 반응도 함께 생각이 들었습니다.

1일 1리버과 몇 백개의 댓글을 달면서

누구보다 성실하게 활동하며

몇 백에서 몇 천점까지 포인트를 기대하지만

현. 실. 은. 그렇지 않다는 것입니다.

리버 포인트를 얻기 위한 것도 마찬가지라고 생각합니다.

리버의 알고리즘을 추측만 할뿐이지만

보다 나은 전략을 세우고 열심히 만 하는게 아니라

잘 하는 게 필요한 것 같습니다.

정리하면,

$RIVER 의 ��똑한 Smart Vault 시스템처럼

Omni-CDP 스테이블 코인 satUSD의 수익을 창출하는게 필요하지 않나 생각해봅니다.

#RIVER #RiverPts

사실..리버 소재가 떨어져서 그냥 써봤습니다.

긴 글 읽어주셔서 감사합니다.

오늘 조회수가 왜이래? 🧐

@RiverdotInc@River4fun

혹시 트위터 조회수가 잘나오게 하는 방법 아시나요?

저도 잘 몰랐는데~

@TGuleumppang 님께서 알려주신 고급 정보가 있습니다 !

X(트위터)의 노출의 70%는 글을 게시한 시점부터

1시간 안에 결정된다는 것인데요.

알고리즘에 따라 잘 노출되고, 활성화되려면

10분안에 해당 글이 다양한 상호작용이 있으면 좋다는 ��입니다.

그러니까~ 글 게시 전/후로 열심히 소통하면서

내 글이 보다 높은 확률노 노출되게 하는 것도 필요하죠!

퇴근하고 1일 1리버 하는 것도 힘들지만

시간을 쪼개 하는만큼 성과가 안나오면 재미도 반감되니까요~

대댓글로 소통하는 것도 좋지만

새로운 글에도 먼저 답글을 달아주고

내가 먼저 다가가는 상호작용을 활발히 해보면 좋겠습니다~

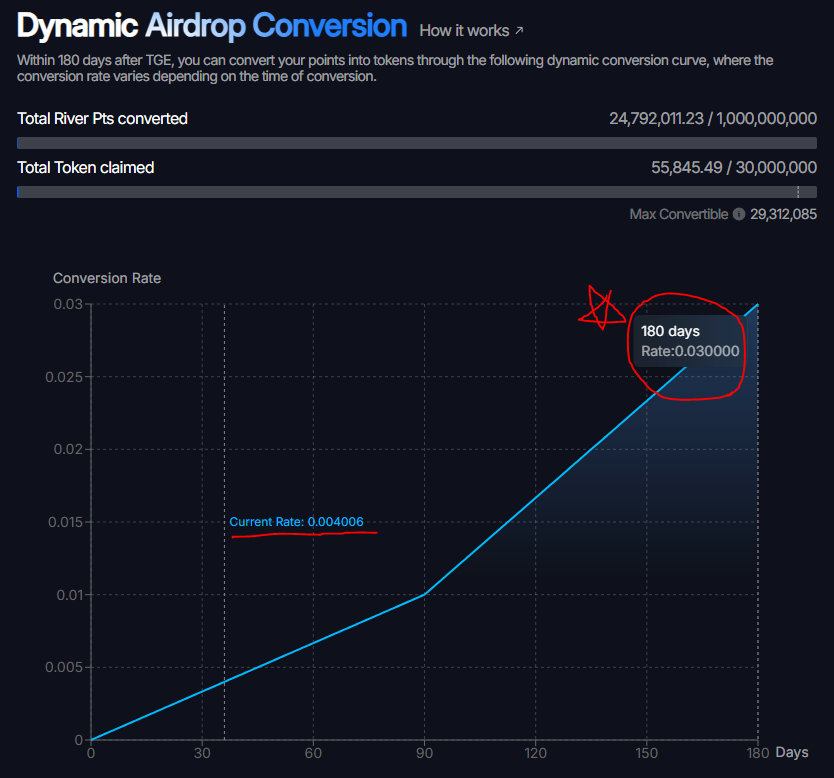

$RIVER 의 Dynamic Airdrop Conversion 처럼

우리 소통의 전환률도 올라가면 좋겠네요!

추운 날씨 건강 조심하세요!

팔로워 (곧) 1000명 -☕️ 카페인 충전 이벤트 !

@RiverdotInc@River4fun

야핑을 시작하고 거의 한 달정도 시간이 되었네요.

다른 분들에 비해서는 다소 느리지만...

제 템포대로 해오면서 이제 팔로워 1000명을 앞두고 있습니다.

큰 힘이 되어주신 리버단 여러분들과 월체인 분들께 감사드립니다.

감사의 마음을 담아 소소하게 이벤트를 준비했습니다.

- 참여방법 - 댓글 남기기만 해도 자동참여 !

- 기간 : 2025. 10. 26.(일) ~ 2025. 10. 29.(수) 23:59 까지

- 상품 : 컴포즈커피 쿠폰 (20장, 1명 1장씩 20명)

- 추첨방식 : 핀볼 랜덤 뽑기 게임

팔로워 분들과 상호작용 해주신 모든 분들께 다시 한 번 감사드립니다!

앞으로도 잘 부탁드립니다. 🙇♂️

🌊$River 핵심 키워드

: 체인 추상화, Omni-CDP, satUSD/satUSD+, Cross-chain Liquidity, River4Fun and 리버단

![KrrBtc's tweet photo. ☕️ 지친 리버단을 위한 카페인 충전 이벤트 결과 공개

@RiverdotInc @River4fun

팔로워 1,000명 달성과 함께 리버단 분들에게 감사한 마음을 전하고자 진행했던 커피 이벤트 결과를 공개합니다!

어제 야근으로 늦고 그대로 뻗어버려서...

12시 땡하고 공개하지 못했네요 🥲

당첨되신 분들 축하드립니다!

- 당첨자 명단 아래 참고 👇

※ 당첨되신 분들은 저에게 별도 DM 부탁드립니다.

다음에 기회가 되면 다른 이벤트를 준비해보겠습니다 🎁

날이 추워졌는데 건강 조심하세요.

시즌3 끝까지 행복하게 상호작용과 소통하시길 바랍니다.

[당첨자 명단]

@dasd15asdf

@GildongBot

@nky1209

@sPp5FcK0pH74702

@newhavendiepp

@dmte00

@Crypto_S3th

@dat150201

@Jyky31133851

@jjibi2025

@woo_jun_space

@Yari_kiru

@chun_453

@nyuknyuk66

@gaengji7512

@Zzaeyg

@dibidibidip_zz

@SUITOBER

@kindmceo

@pantera_park

🌊 $RIVER 핵심 키워드

- 체인 추상화, Omni-CDP, satUSD/satUSD+

- Dynamic Airdrop Conversion, Smart Vault](https://pbs.twimg.com/media/G4gnQPQaEAAGKjC.png)