8/ KSVC has skin in the game. Three of these six held in TWSE Model 1 since Jan 13:

- Accton (2345): entry NT$1,225, now NT$1,450 (+18.4%)

- Delta (2308): entry NT$1,070, now NT$1,260 (+17.8%)

- Chenbro (8210): entry NT$927, now NT$975 (+5.2%)

The thesis is that AI chips get designed, then they need physical infrastructure. Still early in the 800G/VDC/liquid cooling cycle.

6 Taiwan suppliers just posted January numbers. Power, cooling, networking, racks, test equipment. Record revenues almost across the board.

Everyone's watching who designs the AI chips. The companies building the physical infrastructure around them are printing.

7/ What I keep watching:

- CDU is project-based = lumpy quarterly revenue (see Delta's Jan miss)

- Customer concentration. Accton's Meta/AWS exposure is a feature until it's a risk

- Trainium 3 mass production delayed 1 quarter, upstream 2Q26, downstream 3Q26

- 1H26 demand may be front-loaded (Olympics/World Cup pull-forward in display could affect broader sentiment)

7/ Next real test: March 16 earnings call for 4Q25. That's where management gives the full 2026 outlook. If AI server acceleration shows up in the segment numbers, the re-rating argument gets a lot louder.

Risk side: EV subsidiary Foxtron is doing NT$11mn in January revenue vs NT$708mn a year ago. And if GB200/300 ramp stalls, the bear case at 7x P/E is real.

Don't hold this one. Watching the March call.

Hon Hai down 5% YTD while GB200/300 server racks ramp into hyperscalers. Both MS and GS dropped bull notes the same week — GS put it on the Conviction List at NT$400, MS stayed Overweight at NT$317. 12.4x forward P/E on a name shipping NVIDIA racks.

6/ On valuation: 12.4x forward P/E at the low end of a one-year average (11-15x). GS targets 21x, which is above the historical high end of 20x. They're arguing the shift from pure EMS to AI servers and EVs justifies a structural re-rate.

MS at 18x is more conservative but still wants re-rating from the 7-16x range of the past three years. Bull case NT$444 at 26x. Bear case NT$128 at 7x. Asymmetric if the AI server story plays out.

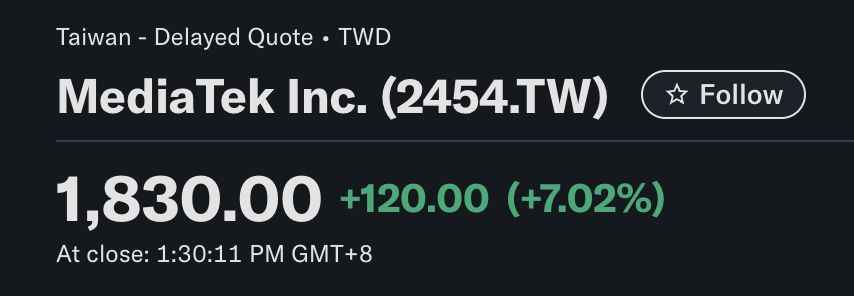

Three broker reports on MediaTek dropped back to back. GS upgraded to BUY, MS reiterated OW, Aletheia at BUY. Nobody's talking about phones anymore. All three are modeling a $7B ASIC business that barely existed 18 months ago.

7/ Three houses, same read: smartphone weakness is noise, ASIC ramp is the story.

ASIC goes from near-zero to 23% of revenue in two years. OpM bottoms in 2026 then expands to 20%+ as ASIC (margin-accretive) scales up.

KSVC holds MTK in TWSE Model 2. Entry NT$1,755, now NT$1,710. Down 2.6% but this is an earnings inflection position, not a swing trade. Watching the 2027 numbers.

Three broker reports on MediaTek dropped back to back. GS upgraded to BUY, MS reiterated OW, Aletheia at BUY. Nobody's talking about phones anymore. All three are modeling a $7B ASIC business that barely existed 18 months ago.