Nuvama Wealth Management - Swapped Cyclical Income for Recurring — and Bagged an MF Licence

The headline reads dull — revenue +8%, operating PAT +6%. After a +41% revenue year, that's a sharp slowdown.

But the headline hides the real story: FY26 was the year Nuvama changed *what it earns from*.

→ Cyclical out, recurring in. Wealth + Private are now ~55% of firm revenue (was 49%); add Asset Services + Asset Mgmt and ~80% of the firm is recurring/annuity-like (was 74%). MPIS revenue +38%, Private's ARR +32%. The earnings base got more predictable.

→ Two engines, opposite directions. Wealth + Private compounded PBT ~22–24% in a soft market. Capital Markets (IB/IE) went the other way: revenue −19% on weak ECM/QIP. The lone bright spot there — fixed income +34%, now ~half of IB and #1 in public debt issues.

→ Asset Services held the line. Revenue +12%, highest-ever profits, ~15% profit growth despite a rate cut and losing a big client. The "market-infrastructure" leg — sticky, low-vol, not broking.

→ The optionality unlocked. SEBI granted the mutual-fund licence (Jun '26). Asset Mgmt is still tiny (~$6M revenue on $1.4B AUM) but mgmt fees +31%, the private-credit CIO is in, and a SIF — migrating a 5-yr top-quartile long-short — is the next launch.

The other side of the ledger:

• RoE slipped 31.5% → 28.1% (capital build + weak capital markets)

• Cost-to-income ticked up to 56%

• Asset Mgmt is optionality, not earnings yet — even mgmt says "don't rush; one bad year sets you back years"

• New entrants dangling "stratospheric" RM valuations = real cost pressure

Net: a platform trading near-term flash for earnings quality + a long asset-management runway. Whether that AM bet pays is an FY27–28 question, not an FY26 one.

Disc: Educational decode. Not investment advice. No buy/sell calls.

CP Plus / Aditya Infotech — Q4 FY26 Decode

- FY26 Revenue ₹4,221 Cr (+36%)

- EBITDA ₹579 Cr (+124%)

- Adj. PAT ₹368 Cr (+166%)

Q4 alone: Revenue +46%, EBITDA +162%, PAT +208%. Khemka called it a "defining year… regulatory transformation, market consolidation, accelerated localization, AI-led surveillance ecosystems." The numbers back the tone.

1. The real story is market share.

Pre-IPO own-brand share was ~25%. Management's IPO-time guide was ~36% post-STQC. The actual print:

"As of Q3 FY26, our market share reached approximately 45.4%."

STQC didn't just clean up the market. It accelerated consolidation toward the player most prepared — certification, manufacturing, channel, SoC alignment — all locked in before the rules hit.

2. Breadth is the moat.

Many brands are STQC certified. None play across the full stack:

"Nobody out of that plays in all the vertical market segments of home, consumer, small-medium businesses, enterprise, government."

Retail CCTV + government tenders + enterprise + installers + after-sales + R&D. Most competitors are "probably one-tenth of our size at the moment or even lower."

3. The supply-chain crisis helps the leader.

SoC, DDR, flash, sensors — all under pressure into 2027.

"The big get bigger and the smaller tail is the largely affected one."

In a shortage, the largest buyer gets priority. CP Plus is multi-aligned: Ambarella, Qualcomm, Augentix, Innofusion, Novatek, Realtek + sensor partners SmartSens, Sony, SOI. Unsexy. But a quiet market-share moat.

4. Margins reset — but Q4 isn't the base.

EBITDA: 8.3% (FY25) → 13.7% (FY26). Q4 touched ~18% — but management was honest that low-cost inventory, price hikes and SKU mix all helped. Low-cost inventory now exhausted.

"14%-15% should be the new normal."

If that holds after input inflation flows through, earnings power has structurally upgraded. That's where the margin debate now lives.

5. AI = optionality, not yet earnings.

Khemka framed it well: cameras went from viewing → recording → analytics. Now:

"The camera is the sensing device."

Cameras as the eyes, AI as the brain. Qualcomm-led trials, cloud backup, edge AI, SaaS security services. Monetisation: "too early to quantify." Real optionality — just don't model it in current EPS.

FY27 guidance: Revenue ₹6,000–6,500 Cr · EBITDA margin 14–15% · PAT margin 8.5–9.5%. Backward integration moving through housings, lenses, cables + Orient Cables JV. Capacity 2× by FY28.

Kyro Read: CP Plus is interesting because the moat isn't one thing — it's a stack.

Brand + Channel + STQC + Manufacturing + Supply Chain + AI = Surveillance Platform.

FY26 was the breakout year. The next 2–3 quarters need to prove:

↳ Volume growth without ASP-driven flattering

↳ Margin sustainability post-low-cost-inventory tailwind

↳ Cash conversion at higher receivable base

↳ AI moving from optionality to a measurable line

If 14–15% EBITDA sustains and the share gain holds, this isn't a post-regulation windfall — it's the start of a structurally stronger surveillance platform.

Educational, not investment advice.

— Kyro Ventures Research

Know more about us at https://t.co/E7oSZoMYv3

One of the biggest learnings of my investing career - A theme that falls out of favour can stay out of favour for a very, very long time — longer than most conviction, spreadsheets, or patience can hold.

Indian IT is the textbook case. The market darling of the 2000s — Y2K, the offshoring wave, 30%+ growth — flashed "cheap" all the way down. It's now headed for a fourth straight year of underperformance, its weight in the Nifty 50 at a 17-year low.

The trap is assuming cheap is a catalyst. Often a sector de-rates because the market is finally pricing a real, structural slowdown — softening demand, a business model under question — not because it has made a mistake.

"Out of favour" and "mispriced" are not the same thing. Recognising the difference — and being willing to do nothing for years — is one of the quieter skills in investing.

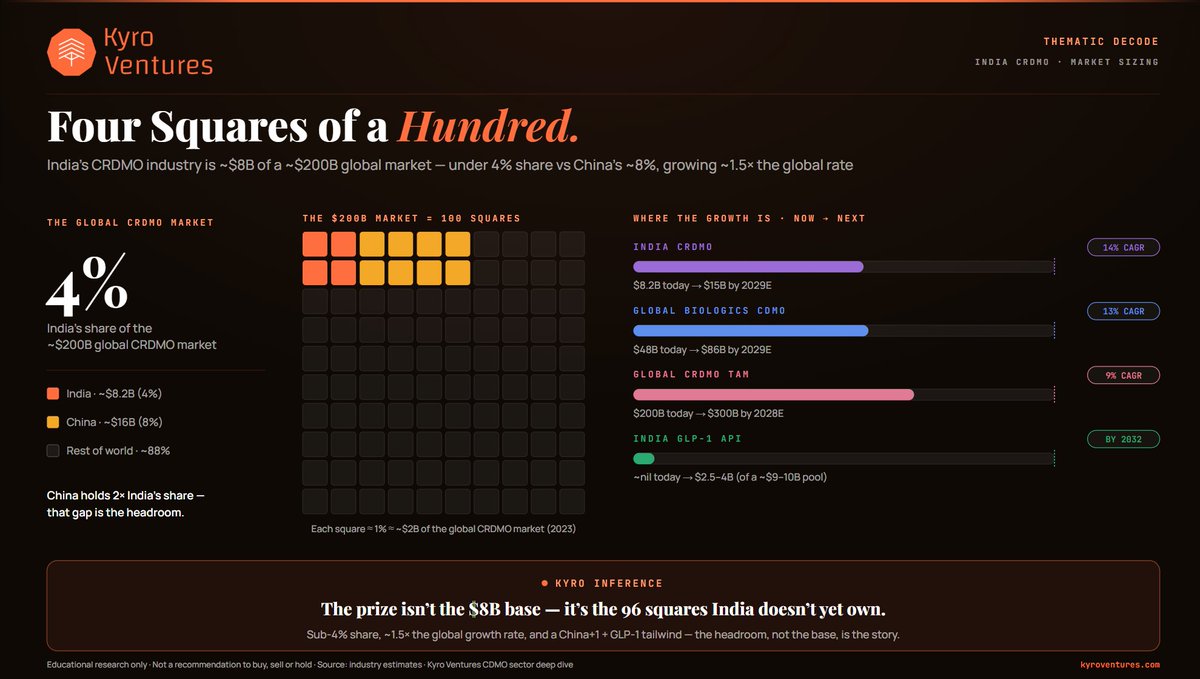

Global CRDMO market

Picture it as 100 squares - India owns 4. China owns 8. The other 88 are still open field.

That 4% is the whole setup. India is already the world's 3rd-largest API maker and supplies ~40% of US generic volumes — but in high-margin contract innovation work, it's barely begun. And it's filling squares ~1.5× faster than the market grows: ~$8B today → ~$15B by 2029E (~14% CAGR), the fastest-growing CRDMO geography on earth.

Three once-in-a-generation tailwinds are landing at once:

→ China+1 / BioSecure — signed into law Dec 2025; WuXi added to the DoD's 1260H list Jun 2026. Jefferies sizes India's incremental prize at ~$2.4B over four years.

→ The patent cliff — ~$190B of branded sales lose exclusivity through 2030 (~69 blockbusters), refilling pipelines and outsourced R&D twice over.

→ The GLP-1 wave — Ozempic/Mounjaro-class sales heading from ~$94B (2025) to ~$130B by 2032. India can plausibly capture $2.5–4B of the ~$9–10B peptide-API + fill-finish pool.

The mix is quietly shifting too: small molecules are still ~72% of the work, but biologics & peptides grow ~2× faster — pulling India toward the complex chemistry (ADCs, sterile fill-finish, fermentation) that earns 30–40% margins.

And the capacity says they believe it: the listed universe is committing a record ~₹150B over three years, almost all in peptides, biologics and complex chemistry. Capex leads revenue by 2–3 years.

The catch — and it's real: top Indian CRDMOs still average just ~$0.4B revenue vs ~$2–4B for global peers, FY26 was lumpy with destocking, and the group trades at ~60–80× earnings. The growth is structural; whether you can grow into that multiple is the open question.

The opportunity was never the $8B base. It's the 96 empty squares.

Disc: Educational only · not a buy/sell/hold recommendation.

Dive deeper into this theme & much more at https://t.co/E7oSZoMqFv

Exicom - The Quarter Tritium Stopped Bleeding

1/10

While the market kept pricing Exicom as a loss-making EV charger play, Q4 quietly flipped the story:

Consolidated EBITDA hit breakeven for the first time since the Tritium acquisition.

Standalone revenue +33% YoY. EV charger revenue ₹88 Cr — its highest ever. Margins at a FY26 peak of 10.6%. Q4 FY26 dropped clues that demand attention. 🧵

Timex — A 170-year-old watch brand just became one of the most exciting compounders on the Indian market.

Timex Group India did ₹800 Cr of revenue in FY26 — up 48%. But revenue isn't the story. Profit is.

EBITDA grew 134%. PBT grew 138%. The margin went from 9.2% to 14.5% in a single year. In Q4 alone, revenue rose 73% and profit nearly tripled (PAT +196%).

That's operating leverage finally switching on. And here's why it switched on 👇

1. Timex stopped being a "cheap watch" company.

It now runs a brand pyramid — Timex at the base, then Guess, Gc, Nautica, adidas, UCB in the middle, and Versace, Ferragamo, Philipp Plein, Ted Baker at the top. Each brand owns a price point. None cannibalises the other.

2. This is a pure-play bet on India's premiumisation wave.

As the Indian consumer trades up, the same watch sale carries a higher price and a fatter margin. Higher ASPs flow straight to the bottom line — exactly what the margin chart is screaming.

3. The channel mix flipped.

E-commerce grew 158% in Q4. Asset-light, high-margin, scalable — no new stores required. New franchises (Signio) and culture-led drops (Timex x NASA, MM6, Elle List) keep the brand relevant to a younger buyer.

4. The quiet catalyst nobody talks about: float.

The promoter cut its stake from 75% to 51% via an OFS. Public float jumped to ~47%, liquidity improved, and institutions could finally build positions. More investable company + inflecting earnings = re-rating fuel.

The honest other side 👇

- The stock isn't cheap. It trades at ~50–65x earnings and ~27x book, near its all-time high (~₹445, +70% in a year). The market is pricing in years of 30%+ compounding.

- And it's a licensed model — Timex doesn't own Guess or Versace. It pays royalties and depends on renewals. The brand owners hold real leverage.

- So the bull case is genuine: premiumisation + brand pyramid + operating leverage + a wider float. The watch-out is equally real: perfection is already in the price.

Disc: Purely educational, not investment advice.

10/10 — The Kyro Frame

Exicom is the rare EV-infrastructure business where:

→ The TAM is a genuine demand supercycle (India 4W EV +109% YoY) plus a global charging + grid-power opportunity

→ The moat is real — full-stack AC/DC value chain, Tritium IP, turnkey deployment, 25+ yrs in critical power

→ The optionality is tangible — exports 2x, US fleet wins, a hyperscaler GRID-FLEX pilot, BESS

→ The balance sheet funds the ambition — Hyderabad capacity in place, rights issue fully deployed

The risk: the consolidated entity isn't profitable yet, and the thesis leans on FY27 execution.

The reward: a standalone-profitable core compounding while Tritium swings from drag to driver.

Q4 didn't just beat — it changed what kind of company Exicom is.

📌 Educational thread. No buy/sell calls. Discuss; don't act on tweets.

Explore more about us at https://t.co/E7oSZoMYv3

Exicom - The Quarter Tritium Stopped Bleeding

1/10

While the market kept pricing Exicom as a loss-making EV charger play, Q4 quietly flipped the story:

Consolidated EBITDA hit breakeven for the first time since the Tritium acquisition.

Standalone revenue +33% YoY. EV charger revenue ₹88 Cr — its highest ever. Margins at a FY26 peak of 10.6%. Q4 FY26 dropped clues that demand attention. 🧵

9/10 — What bulls underweight:

⚠️ Consolidated still loss-making. FY26 PAT loss ₹274 Cr; group profitability hinges on Tritium hitting breakeven in Q4 FY27.

⚠️ Tritium is still small. ~$9.7 Mn/quarter — the turnaround is early and unproven across a full cycle.

⚠️ Critical Power in a soft cycle. Telecom tower rollout grew just ~3.7% YoY; FY27 recovery is a forecast, not a fact.

⚠️ Depreciation drag. The new ₹216 Cr plant lifts fixed costs — standalone PAT already fell YoY despite EBITDA up 77%.

⚠️ Macro & FX exposure. Management itself flagged geopolitical, supply-chain, currency and commodity volatility.

Honest research weighs both sides.

Timex — A 170-year-old watch brand just became one of the most exciting compounders on the Indian market.

Timex Group India did ₹800 Cr of revenue in FY26 — up 48%. But revenue isn't the story. Profit is.

EBITDA grew 134%. PBT grew 138%. The margin went from 9.2% to 14.5% in a single year. In Q4 alone, revenue rose 73% and profit nearly tripled (PAT +196%).

That's operating leverage finally switching on. And here's why it switched on 👇

1. Timex stopped being a "cheap watch" company.

It now runs a brand pyramid — Timex at the base, then Guess, Gc, Nautica, adidas, UCB in the middle, and Versace, Ferragamo, Philipp Plein, Ted Baker at the top. Each brand owns a price point. None cannibalises the other.

2. This is a pure-play bet on India's premiumisation wave.

As the Indian consumer trades up, the same watch sale carries a higher price and a fatter margin. Higher ASPs flow straight to the bottom line — exactly what the margin chart is screaming.

3. The channel mix flipped.

E-commerce grew 158% in Q4. Asset-light, high-margin, scalable — no new stores required. New franchises (Signio) and culture-led drops (Timex x NASA, MM6, Elle List) keep the brand relevant to a younger buyer.

4. The quiet catalyst nobody talks about: float.

The promoter cut its stake from 75% to 51% via an OFS. Public float jumped to ~47%, liquidity improved, and institutions could finally build positions. More investable company + inflecting earnings = re-rating fuel.

The honest other side 👇

- The stock isn't cheap. It trades at ~50–65x earnings and ~27x book, near its all-time high (~₹445, +70% in a year). The market is pricing in years of 30%+ compounding.

- And it's a licensed model — Timex doesn't own Guess or Versace. It pays royalties and depends on renewals. The brand owners hold real leverage.

- So the bull case is genuine: premiumisation + brand pyramid + operating leverage + a wider float. The watch-out is equally real: perfection is already in the price.

Disc: Purely educational, not investment advice.

India's CRDMO industry is an ~$8 billion business sitting inside a ~$200 billion global market.

That gap is the entire thesis.

It grows ~1.5× the global rate, holds under 4% share against China's ~8%, and sits at the receiving end of a global supply realignment. The headroom — not the base — is the story.

We've torn the whole sector down, end to end:

* The market math — $8.2B today → ~$15B by 2029E (~14% CAGR), and where the GLP-1 API and biologics pools open up

* The molecule mix — small molecules still ~72%, but biologics & peptides compounding at ~2× the rate

* The value chain — why margin concentrates at the two ends (discovery IP + complex commercial chemistry earn 30–40%) while commodity mid-chain API deflates

* Who actually plays each link — Syngene, Divi's, Laurus, Gland, Piramal, Blue Jet, Cohance and more, mapped stage by stage

24 molecules. 13 CDMOs. One complete picture.

📖 Read the full report at https://t.co/E7oSZoMYv3 — our most comprehensive sector teardown yet.