La FIFA preguntó a una japonesa que por qué recogen la basura en todos los estadios a los que asisten.

Ella lo explicó: "Es nuestra cultura. Pero también es una señal de respeto hacia el país y estadio que nos acoge y hacia nuestros jugadores. Para nosotros es un honor que nos reciban aquí y no podríamos dejar todo hecho un desastre".

Japoneses TQM 🫶

It's 2030, your portfolio has 30x-50x why?

Becuase you bought these 4 memory stocks and held:

1. $MU — Micron Technology

Target: $5,000 by 2030

AI servers require massive HBM; memory becomes AI's biggest bottleneck.

2. $SNDK — SanDisk

Target: $4,000 by 2030

Every AI model creates exploding storage demand across the world.

3. $WDC — Western Digital

Target: $2,500 by 2030

Data must be stored forever; AI multiplies storage requirements.

4. $DRAM — DRAM ETF

Target: $300 by 2030

Owns the memory ecosystem powering AI compute and storage.

Memory is the new oil. Without memory, AI cannot train, infer, or scale.

Below are $BAC.PRK projections it shows we're still super early.

♻️ RESHARE this post and write 1 comment, I'll DM you my best call option to buy and hold for 1000% (again!)

$NASA ETF core holdings (it owns $SPCX)

$SPCX will easily 100x-200x by 2035:

$SATS 10%

EchoStar satellite operator providing broadband connectivity and video distribution globally.

$RKLB 9%

Rocket Lab — builds Electron rockets and Neutron, launches small satellites to orbit.

$MDA 7%

MDA Space — Canadian satellite manufacturer, builds Canadarm robotics and LEO constellations.

$SPCX 7%

SpaceX — Starship, Falcon 9 launch vehicles, and Starlink global satellite internet constellation.

$ASTS 5%

AST SpaceMobile — building space-based cellular broadband connecting standard smartphones directly.

$LUNR 5%

Intuitive Machines — lunar landers delivering NASA payloads to the Moon's surface.

$PL 5%

Planet Labs — daily Earth imaging constellation; sells satellite imagery and geospatial analytics.Mid holdings (3–4%)

$VSAT 4%

Viasat — satellite broadband networks for commercial aviation, maritime, and government users.

$FLY 4%

Firefly Aerospace — Alpha rocket launches, Blue Ghost Moon lander, lunar logistics provider.

$VNP 4%

5N Plus — produces space-grade high-purity semiconductor materials for satellite solar cells.

$VOYG 4%

Voyager Technologies — space systems integrator serving NASA and defense satellite programs.

$YSS 4%

York Space Systems — manufactures standardized S-class satellite platforms for government constellations.

3491 TTTW 3%

Win Semiconductors (3105/3491) — GaAs compound semiconductor foundry supplying RF chips for satellites.

$IRDM 3%

Iridium — global LEO satellite constellation providing voice and data coverage everywhere on Earth.

$BKSY 3%

BlackSky Technology — real-time Earth intelligence platform using electro-optical satellite imagery.

186A JPJP 3%

Astroscale — Japan's on-orbit space debris removal and satellite life-extension services pioneer.Small holdings (1–2%)

$VPG 2%

Vishay Precision Group — precision sensors and resistors used in satellite and aerospace systems.

$LASR 2%

LIGHT — high-power fiber and semiconductor lasers for directed energy weapons and satellites.

$FTC LNU 2%

Filtronic — UK RF component maker supplying mmWave amplifiers for Starlink and satellite comms.

464A JPJP 2%

QPS Holdings — Japanese SAR satellite constellation for high-frequency Earth observation imaging.

$LPTH 2%

LightPath Technologies — infrared optics and assemblies for space imaging and defense sensors.

9412 JPJP 1%

SKY Perfect JSAT — Japan's leading satellite operator for broadcasting and communications.

$VELO 1%

Velo3D — metal additive manufacturing for rocket engines and complex aerospace flight hardware.

3105 TTTW 1%

Win Semiconductors — world's largest GaAs foundry; RF chips enabling satellite phased-array antennas.

$AVIO 1%

Avio — Italian rocket maker; builds Vega launcher and propulsion systems for European space missions.

290A JPJP 1%

Synspective — Japanese SAR satellite operator providing all-weather Earth observation and analytics.

$NN 1%

NN Inc — precision machined components and assemblies for aerospace and defense satellite programs.

$RDW 1%

Redwire — space infrastructure maker; solar arrays, deployable structures, and in-space manufacturing.

$OHB 1%

OHB SE — German space group building satellites, navigation systems, and launcher components.

Satya Nadella just posted something that validates the entire AI buildout thesis from the very top of the stack.

The model is commoditizing. The durable value is the learning loop a company builds on top of the model.

He splits it into two assets:

Human capital -- the knowledge, judgment, relationships, and pattern recognition of your people.

Token capital -- the AI capability the firm builds and owns.

He says the real opportunity is building a learning loop where human capital and token capital compound together.

If the model layer is commoditizing then the durable returns are not in the model makers. They are in the infrastructure that powers every company building its own loop. Compute. Memory. Interconnect. Power.

The full stack underneath the application layer.

The model wars will have winners and losers. The infrastructure underneath gets bought either way.

Bullish the AI buildout.

Every layer. If you want to understand them in detail, check out my Substack.

https://t.co/Wna5UzCOVT

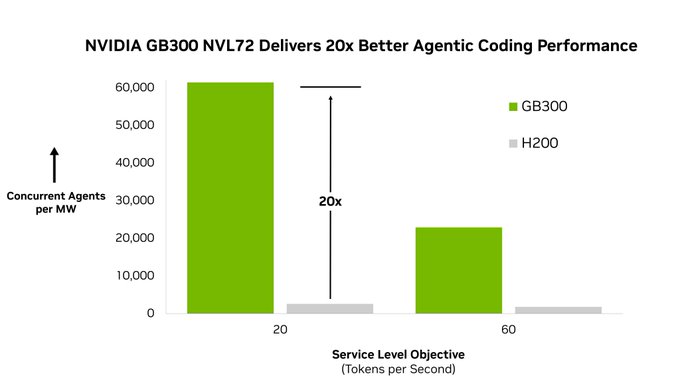

The first agentic AI infrastructure benchmark is here.

An AI agent chains dozens to hundreds of AI model calls together, using tools, gathering context, and iterating until the task is done. Existing benchmarks weren't designed for that.

AgentPerf from @ArtificialAnlys gives developers, enterprises and infrastructure providers a clear way to compare accelerated computing systems for agentic AI.

First round of results highlight that NVIDIA Blackwell delivers 20x more agents per megawatt than NVIDIA Hopper.

$MU $DRAM Unbelievable

$707,000,000,000.

That is the projected 2027 operating profit of 3 memory companies.

Apple + Microsoft + Google + Amazon + Meta + Tesla combined? ~$661 Billion.

The Memory Trio beats the Magnificent 6.

Not revenue. Operating profit.

The big 3 Memory makers are estimated to make more profit than the MAG6 next year, yet trade at a market cap nearly 5x lower.

Still a Huge discount. Rerate inevitable.

Micron 🚀🚀 to $2000 medium term.

$MU $DRAM $EWY

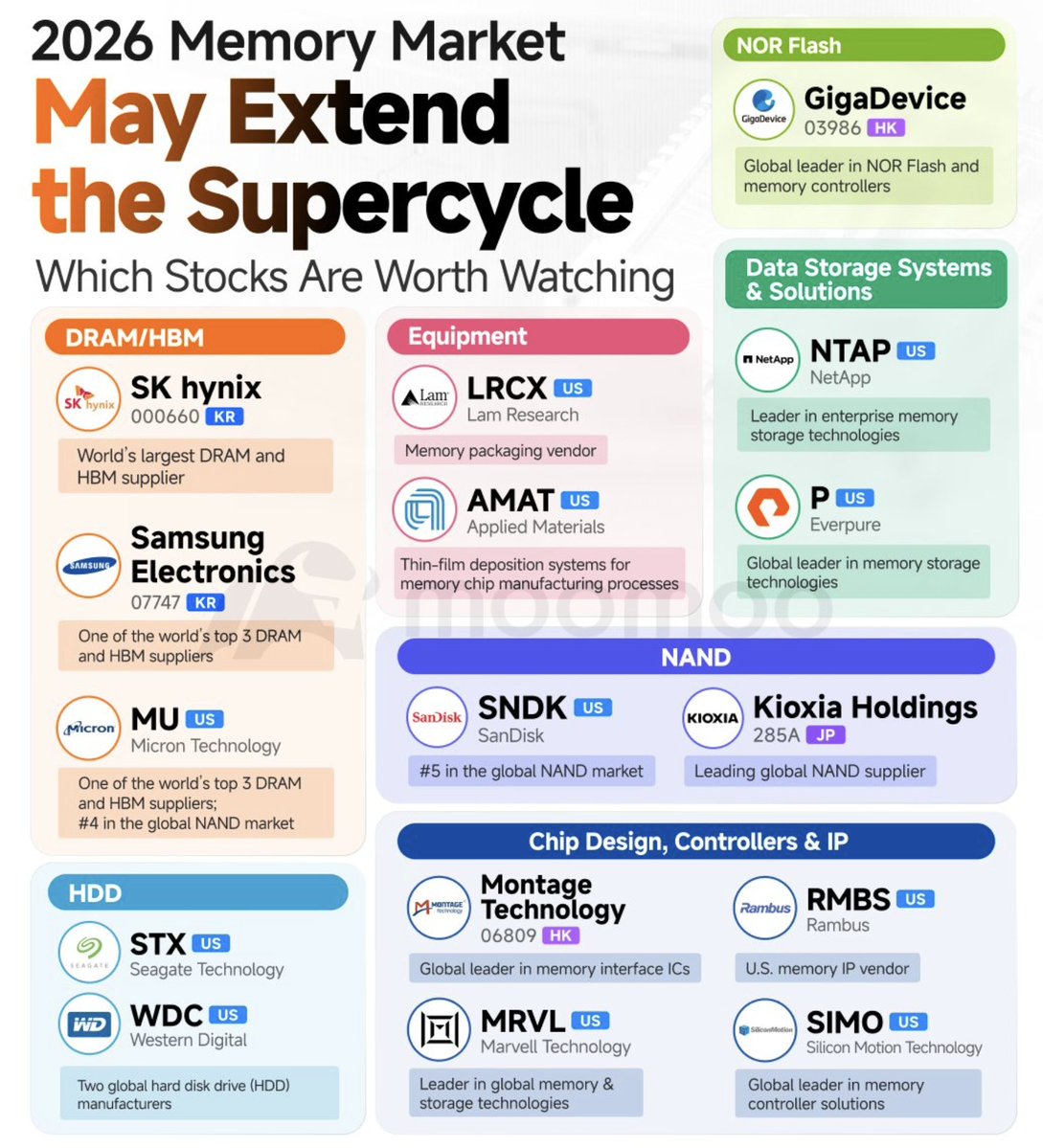

The memory story isn’t over yet.

As AI workloads continue to grow, demand for HBM, DRAM, NAND, and data storage infrastructure could keep the memory supercycle alive well into 2026. While most investors focus on the AI chip makers, the companies supplying memory, storage, controllers, and manufacturing equipment may be some of the biggest beneficiaries.

Names worth watching include $MU Micron, $LRCX Lam Research, $AMAT Applied Materials, $NTAP NetApp, $STX Seagate, $WDC Western Digital, $MRVL Marvell, $RMBS Rambus, and $SIMO Silicon Motion.

If AI is the engine, memory is the fuel. Don’t overlook the companies building the infrastructure behind the boom.

Micron will be a $4,000 stock within the next few years and here is why (Save this).

Let's start with the BofA semiconductor forecast in the chart above.

Bank of America models total semiconductor sales reaching $1.3 trillion in 2026, a 65% year over year jump and growing to $2 trillion by 2030.

But strip out the headline number and look at what is doing the work, it's memory.

Memory sales are forecast to grow 168% in 2026 alone, versus just 25% for core semis ex-memory meaning the entire semiconductor supercycle is essentially a memory supercycle, and it is being driven by one product.

That product is high-bandwidth memory, and BofA projects the HBM market to explode from $35 billion in 2025 to $168 billion by 2030, a 37% compound annual growth rate that makes it one of the fastest growing markets in the history of the semiconductor industry.

Now zoom into Micron specifically.

Micron's entire 2026 HBM output is already contracted under long-term supply agreements.

The company has locked in six major AI and cloud customers at fixed prices, meaning the revenue is largely booked.

And despite that, CEO Sanjay Mehrotra has said Micron can only fulfill 50% to two-thirds of what its key customers actually need in the near term.

The supply crunch is not expected to meaningfully ease until late 2027 at the earliest.

Management guided Q3 to $33.5 billion in revenue with 81% gross margins and if achieved, that single quarter would generate over $27 billion in gross profit.

Micron is ramping HBM4 at twice the speed of its HBM3E ramp, the first HBM4E chip is scheduled for introduction in 2027 and the company has committed approximately $200 billion in planned capacity expansion to meet what it describes as a historic memory supply crunch.

A company generating $130+ billion annualized revenue by 2027, with 80%+ gross margins, sold-out capacity, a 20%+ HBM market share in a $168 billion market, and a geopolitical moat as the only American HBM supplier and that is how you get to $4,000.

Our milk road subscribers are already up Massively on Micron, come join Milk Road Pro for our full breakdown, our complete Micron valuation model and our full AI trade thesis.

Link below!

this is f*cking gold

How to build your first AI agent (Full guide)

if I had this a year ago, I would've shipped my first agent in a day instead of 2 weeks

in the right hands, this changes everything:

You don't need to buy $SPCX to 10x your portfolio.

You can buy $NASA ETF which owns:

1. SpaceX $SPCX — 12.70%

Rockets, spacecraft, Starlink satellite internet

2. Rocket Lab $RKLB — 6.99%

Small satellite launches, spacecraft components

3. Lockheed Martin $LMT — 6.66%

Satellites, spacecraft, defense, NASA contractor

4. RTX Corporation $RTX — 6.22%

Satellite systems, sensors, propulsion, defense tech

5. Airbus SE $AIR.PA — 5.08%

Satellites, space modules, launch infrastructure

6. Boeing $BA — 4.81%

Spacecraft, satellites, Starliner program for NASA

7. Maxar Technologies $MAXR — 4.35%

High-res satellite imagery, space infrastructure

8. Northrop Grumman $NOC — 3.92%

Satellites, space vehicles, mission systems

9. L3Harris Technologies $LHX — 3.38%

Comms systems, space hardware, defense tech

10. Planet Labs $PL — 2.93%

Fleet of imaging satellites, daily Earth observation

Remember, $SOXL which owns $NVDA is up 1200% from $22 to $280 so far. $NASA could be the same.

♻️ RESHARE this post and write 1 comment, I'll share my top 3 ETF to add for 10x (and safer).

$NVDA Vera Rubin & $GOOGL next-gen AI data centers are pulling 800V DC adoption ahead of schedule with shipments expected in Q3 2026.

The shift to 800V becomes a forced upgrade as AI racks move toward megawatt-scale power increasing power-semiconductor content in every rack.

Micron is going to be a $4,000 stock and the CEO just told you exactly why in one interview (Save this).

Micron is no longer a chip company but rather a America's monopoly on the most strategically critical material in the AI buildout.

It's the only western company manufacturing memory at advanced nodes, sitting on $200 billion in committed domestic capex, with every unit of its highest value product already sold.

let's start with the supply reality, Mehrotra said Micron can currently meet only 50% to two thirds of the demand from its key customers.

That shortage will last well beyond 2027, and meaningful new supply from anyone in the industry does not arrive until 2028 at the earliest.

Two more years of demand outpacing supply in a market growing 168% year over year and that is the floor on the bull case.

Now layer on what makes this cycle structurally different from every one before it.

Micron is the only American memory manufacturer on earth, Samsung and SK Hynix are South Korean.

In a world where AI infrastructure has become a declared national security priority where Commerce Secretary Lutnick and Trade Ambassador Greer personally showed up to a fab dedication in Manassas, Virginia being the only US memory company is not just a competitive advantage.

It is a government backed structural monopoly on the most critical input to the US AI buildout, backed by $6.2 billion in CHIPS Act subsidies across Idaho, New York, and Virginia.

The $200 billion buildout spans Manassas for DDR4 defense and industrial memory, Boise for leading-edge DRAM with first wafers out mid 2027, a second Boise HBM fab with first wafers by end of 2028, and the Syracuse megafab, the largest semiconductor facility in US history, breaking ground January 2026 with up to four fabs over time.

Combined, these sites take Micron's domestic production from 10% of its total output today to 40% over the next decade, and create 90,000 jobs in the process.

The business model transformation is the real story.

Come join Milk Road Pro for our full breakdown, our complete Micron valuation model incorporating the $200 billion domestic buildout and our entire AI thesis.

Link below.

$NVDA is trading near its cheapest valuation in a decade.

You’re paying a market multiple for the core compute engine of the entire AI economy powering the largest infrastructure buildout in history.