Holy shit, I just built a full FPS game straight in the browser using the @gitlawb playground

Took 3 days

Check this out @kevincodex@gitlawb

This is insane

the $SIBYL structure:

0 team tokens. 0 VCs. 0 paid KOLs.

20% of supply retained by SIBYL for growth and liquidity bootstrapping.

~$10K of fee revenue recycled back into the token:

buybacks (~$3.9K, 3.16M SIBYL recouped), LP depth (5 waves, treasury pool share 1.6% -> 5.8%), market support.

staking: 6.95M SIBYL funded across four cycles. 151.7M SIBYL locked, 15.2% of supply. avg APR ~30%.

revenue -> buybacks -> staking. every wallet on basescan.

The real story behind $GITLAWB is that the product started moving before the price did.

If this were just another meme,

you wouldn’t be seeing this level of concrete usage data.

OpenClaude:

・26.8k GitHub stars

・8.5k forks

・615 commits

・Gitlawb OpenGateway with MiMo added in v0.11.0

・Xiaomi MiMo integration added

Gitlawb network:

・3 nodes live

・2,000+ repos

・1,800+ agents

・real push events flowing through the network

And now, the even bigger piece is free OpenGateway access.

Since OpenClaude v0.11.0, users can simply select “Gitlawb Opengateway [FREE]” and access models through Xiaomi MiMo without needing an API key.

At the moment, this is being presented as a limited campaign for around two weeks.

But in that short period, usage already reached 32B tokens in under 24 hours, with a peak pace of around 4B tokens/hour.

So this is not just hype because something is free.

Builders are actually touching it, testing it, and starting to use it.

That matters.

Gitlawb is not “an app that uses AI.”

It is infrastructure for AI to work.

If GitHub was the workspace for human developers,

Gitlawb is aiming to become the workspace for AI agents.

As AI agents grow, they will need:

Identity.

Permissions.

Repos.

History.

Signatures.

Reviews.

Persistent storage.

Incentive design.

Gitlawb is going straight into the middle of that stack.

And on top of that, it has OpenClaude as the entry point.

You can try it for free.

Agents can write code.

Agents can push to repos.

Demos are shipping.

External projects are starting to use it.

Repos and agents are growing on the network.

That flow has already started.

And this is where $GITLAWB’s utility starts to matter.

More AI agents.

More repos.

More pushes.

More PRs and issues.

More builders using the network.

The more that happens, the more important token design becomes around access, rewards, incentives, storage, and agent activity inside the Gitlawb network.

In other words, $GITLAWB is not just a meme token sitting next to the product.

It has the potential to matter as network usage grows.

Of course, it is still alpha.

The node count is still small.

Replication is still developing.

OpenGateway free access is currently limited-time.

Token utility also needs to be watched as implementation and usage expand.

But that limited campaign is bringing builders in,

and creating a real funnel from OpenClaude into Gitlawb network usage.

That is the key.

If the AI agent economy is really coming,

then one question becomes impossible to ignore:

Where will agents write code?

Where will they own repos?

Where will their contributions be proven?

$GITLAWB already has:

A working product.

Early real usage numbers.

A funnel bringing builders in.

And a future network utility narrative.

That’s what makes it interesting.

Respect to @kevincodex and @gitlawb.

They’re not just talking about the AI agent future.

They’re shipping it.

#AIagent #Web3 #Base

OpenClaude is clocking 4B inference tokens/hour through OpenGateway Xiaomi MiMo.

That’s roughly $6,000/hour in AI access being opened to users.

Xiaomi is not just sponsoring a model.

They’re sponsoring AI access for everyone.

$GITLAWB

Thread: Why $GITLAWB is going to $20 BILLION MC — The GitHub of the Agent Era 🚀

1/ Just woke up to insane numbers: OpenGateway (powered by @kevincodex & team) hit 8.6 BILLION tokens in <48 hours on free Xiaomi MiMo. Not 24h old and already getting hammered.

This isn’t hype. This is the spark.

Let me break down the full picture — and exactly how we 1000x from here to $20B market cap. 🧵

2/ The Setup

Gitlawb = decentralized Git for AI agents.

Agents have real DIDs (not fake accounts)

Every commit signed by human OR agent

UCAN delegation, MCP tools, IPFS/Filecoin/Arweave storage

OpenClaude (the CLI) as the on-ramp

It’s GitHub, but rebuilt from day one for autonomous agent swarms. First-mover in the exact right moment.

3/ The Ignition (Now)

Xiaomi MiMo free unlimited via OpenGateway for ~2 weeks (ends ~May 27-28).

Already: 8.6B+ tokens, 85% cache hit, 140k+ requests.

OpenClaude exploding in downloads/stars.

This is the biggest free frontier-model giveaway in AI devtools history. Massive user acquisition flywheel.

4/ Revenue Flywheel (How money actually flows)

Spawn: Dedicated agent hosting — $9/mo (grandfathered first 100) then $19/mo. Cheap vs Cursor/Replit/cloud agents ($20-500+).

Storage: Public <1GB free forever. Private/big repos = tiny 0.1% in $GITLAWB.

Gateway + Protocol fees: Small cut on LLM routing post-promo.

Agent economy: Bounties, repo tokenization, contributor splits — protocol takes 2-3%.

Usage → sticky agents/repos → real recurring revenue.

5/ Path to $20B (Exponential Scenario)

Phase 1 (Next 2-4 weeks): Promo ends with 100B-500B+ tokens. Tier-1 listings (Coinbase/Binance interest high — fair launch, no VC bags) → $200M-$500M MC. Spawn conversions kick in.

Phase 2 (3-9 months): 100k-500k MAU, 50k-200k active agents, 100+ nodes. Protocol revenue $1M-$10M/mo. $1B-$5B MC.

Phase 3 (12-36 months): Millions of agents, 1M+ repos. $50M-$300M+ annualized revenue. Bull market + "GitHub for Agents" narrative → $20B (~$0.20/token with 100B supply).

6/ Why This Actually Happens (The Moat)

First-mover advantage: No real decentralized agent-native git competitor exists. GitHub is bolting AI onto human Git. We built for agents first.

Fair launch: No team/VC pre-mine. Tier-1 exchanges LOVE this — easier listings, no dump risk.

Network effects: Agents prefer it because it’s agent-first. Switching costs skyrocket once repos & collaborations live here.

Undercuts everything: Cheaper than GitHub Pro + Copilot stacks for high-volume agent use.

7/ Numbers Needed for $20B

500k-2M+ sticky MAU

100k-1M+ persistent agents/repos

$100M-$400M annualized revenue (very doable at scale)

50-200x revenue multiple (standard for AI/crypto winners in bull)

We’re already seeing the early exponential curve. Retention 10-30% post-promo would be enough to ignite.

8/ Risks (Being Real)

Execution on nodes/reliability post-promo. Centralized competition improves. Bear market. But the setup (traction + tokenomics + timing) beats 95% of low-cap plays right now.

9/ Bottom line

This is how category winners are born:

Insane free hook → user explosion → product stickiness → revenue → listings & hype loops → dominance.

Gitlawb isn’t just another token. It’s the infrastructure layer for the agent economy.

The GitHub moment for AI agents is here.

10/ DYOR. This is high-conviction but crypto is volatile.

If you’re building agents, using OpenClaude, or just watching — the next 4 weeks (promo end + possible Coinbase) will be legendary.

$GITLAWB to the agent future.

Who’s in? 👇

This might be the most undervalued asymetrical size bet on @base right now

It looks like a regular project at first look but when you actually dig into the devs background you realize it's the next $AEON

$AXIOM launched on @bankrbot by @MeltedMindz who had previous projects reaching 40M-700M

The dev behind @AxiomBot has connections with VCs who backed his previous projects and is also very close to core @base team members

( he also worked with @Altcoinist in the past on ethereum:0x320623b8e4ff03373931769a31fc52a4e78b5d70 who reached an ATH of 1.1B mcap )

Several smart 7-8 fig whales have been accumulating including many ribbita-by-virtuals:native $POD and $GITLAWB whales

$AXIOM is already operating like an actual autonomous company generating revenue daily with its products :

> SQLStream ( AI observability SaaS )

> Postera ( X402 UDSC payments for agents )

> Bankr signals

> LP management ( automated compounding & harvesting )

What makes this setup fascinating is the flywheel behind it

The products generate fees, then 50% of those fees are automatically used to buy and burn $AXIOM while the other 50% gets distributed daily to holders and stakers of $AXIOM

As usage grows, more fees are generated, more tokens get burned, and more rewards flow back into the ecosystem

The crazy part is that the whole system is maintained by the agent itself through its own execution stack, cron jobs, and autonomous infrastructure

With the dev relentlessly updating the level of execution of $AXIOM honestly it feels higly mispriced sub 1M mcap.

It will be a size hold for me the devs track record doesn't miss he has the tech and the connections with VCs to make $AXIOM the next runner on @base

CA : 0xf3Ce5dDAAb6C133F9875a4a46C55cf0b58111B07

I tried like 7 trillion passwords lmfao

Found this old pneumonic a few weeks ago that ended up being the old password before I changed it

Thought I was screwed

Last ditch effort dumped my whole college computer into Claude

It found an OLD wallet file that the pneumonic successfully decrypted

Locked out 11+ years because I got stoned and changed the password

Spent $250 on each lol

HOLY FUCK

The Inference Shift

Agentic inference is going to be different than the inference we use today, and it will change compute infrastructure because speed won't matter when humans aren't involved.

https://t.co/8RByFoBs0g

https://t.co/RVhEDOHawu launched this week: Solana Foundation + Google Cloud. Agents can now call paid APIs with no signup — just a wallet.

Solana settles every call. Google runs the gateway. Solrouter shipped the first private inference endpoint.

If AI keeps scaling, where does the factory break first?

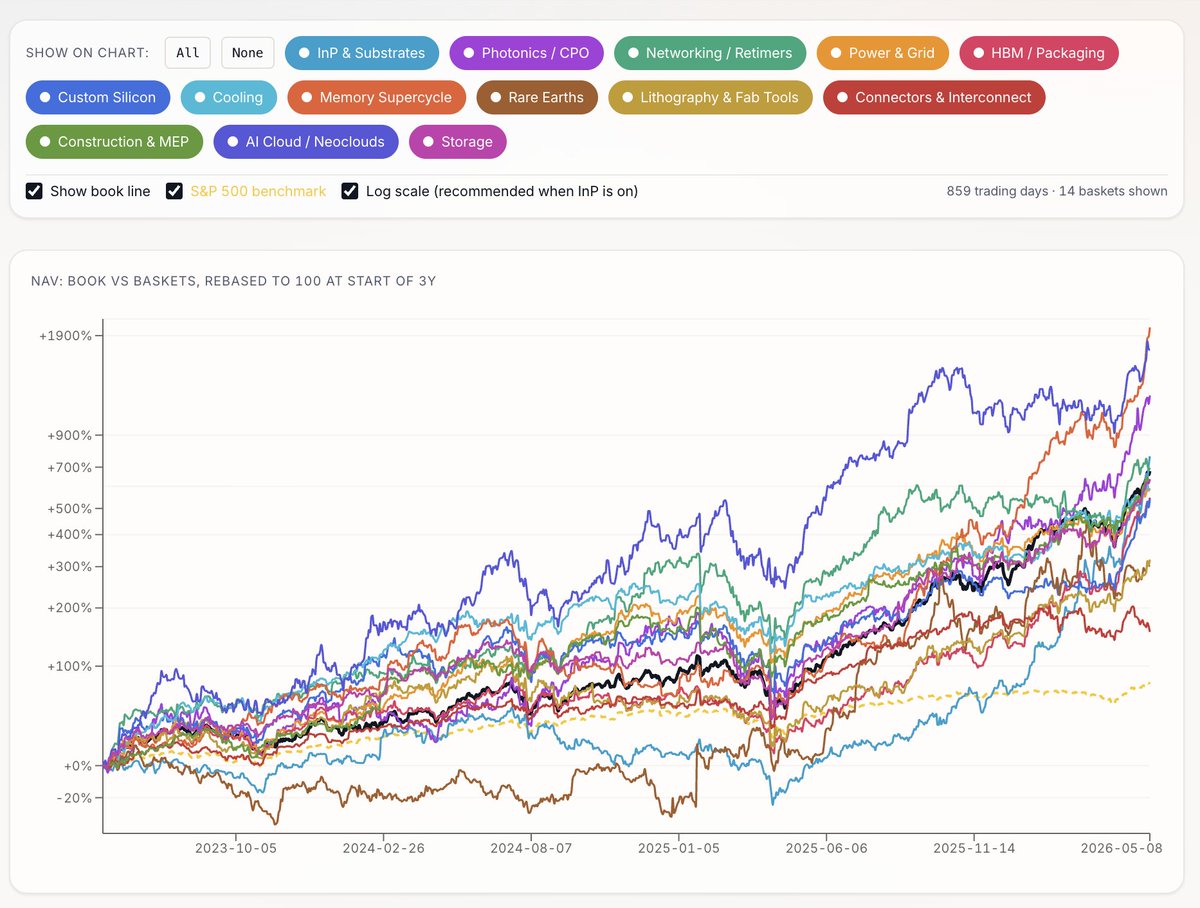

I built a public dashboard for that one question.

S&P 500 (in yellow): +31% over the last year.

The AI bottleneck book I have been keeping: +348%.

All 96 names green. That is the gap between buying AI stocks and buying the parts AI cannot ship without. The market is starting to learn the physical bill of materials for intelligence.

The companies are sorted into 14 baskets that map the physical AI stack: substrates, photonics, HBM, packaging, memory, power, cooling, storage, retimers, fab tools, construction, neoclouds, custom silicon, rare earths, and connectors.

All of it built around one question: if AI keeps scaling, where does the factory break first?

A year ago, the obvious AI trade was the visible part: GPUs, power, data centers, networking, maybe cooling. The tape has been moving somewhere more specific. Memory leads the 1Y.

InP and substrates sit right behind it.

Photonics/CPO and HBM/packaging follow.

Then storage, custom silicon, fab tools, construction, power, cooling, retimers, connectors.

The order matters more than the return. The market is no longer buying "AI infrastructure" as a single theme. It is ranking the layers that can make the AI factory late. That is the difference between AI beta and what is starting to look like bottleneck beta.

AI beta asks: who sells into AI. Bottleneck beta asks: if this layer is late, does the factory stop. The first question fits a pitch deck. The second fits a route card.

A month ago, the clean version of this was InP. GPUs need optical transceivers. Transceivers need lasers. Lasers need indium phosphide substrates. The substrate is a small physical disc sitting underneath one of the largest infrastructure builds in history.

That was why $AXTI worked. Tiny disc. Huge system. Real bottleneck. But $AXTI did not stop mattering. It stopped being lonely. Over 3 months, InP led the tape. Over 1 month, InP is still leading, but memory, photonics, custom silicon, and HBM/packaging have clustered right behind it.

The market is no longer only buying the raw ingredient. It is buying the stations that turn the ingredient into throughput. That is not a rotation out of InP. It is a rotation into the route card. Substrate to epi. Epi to laser. Laser to optical engine. Optical engine to package. Package to HBM. HBM to system. System to tokens.

$AXTI is the substrate station.

$VECO is the laser-tool station.

$LITE, $COHR, $MXL, and $AAOI are the photonics layer.

$MU, $SNDK, and SK Hynix are memory.

$TSM is base dies and advanced packaging.

$AMKR, ASE, and KYEC are OSAT.

$ONTO and $CAMT are inspection and metrology. $BESIY, $KLIC, and TOWA are bonding, attachment, and molding.

$ALAB and $CRDO are the retimer fabric that lets all of it talk.

These are not separate stories. They are one object moving through the factory. The next layer is probably not just HBM. Everyone has found HBM. The next layer is what makes HBM usable. A stack of memory dies is not memory yet. It has to be bonded, molded, inspected, cooled, and tested. It has to survive heat, pressure, warpage, microbumps, underfill, substrate flatness, and burn-in. Before HBM becomes bandwidth, it has to become a manufactured object.

That is where the watchlist is moving next. ABF substrates. T-glass. OSAT capacity. HBM base dies. Hybrid-bonding metrology. Bonders. Molders. Dicers. Thermal. And eventually EUV.

The scarce thing keeps getting more specific. First the chip. Then the package. Then the memory. Then the optical link. Then the substrate under the laser. Next, the mold around the memory stack, the metrology tool checking the bump, the glass that keeps the package flat.

The market is not walking from InP to HBM. It is walking with the part. Station by station.

Dashboard is public, link below.

(not financial advice)

Anthropic CEO: "we got seven more months."

the bet was a $1B one-person company by end of 2026. two-person AI companies already crossed $1B, one-person companies are past several hundred million.

not everyone can make a $1B company. but a $10K MRR AI agent company is on the table.

this guy dropped the exact roadmap.

Bookmark this and start this weekend.