We provide exclusive, independent advice tailored for primary financial institutions. Our Aim is to improve profitability of our clients via tradable advice.

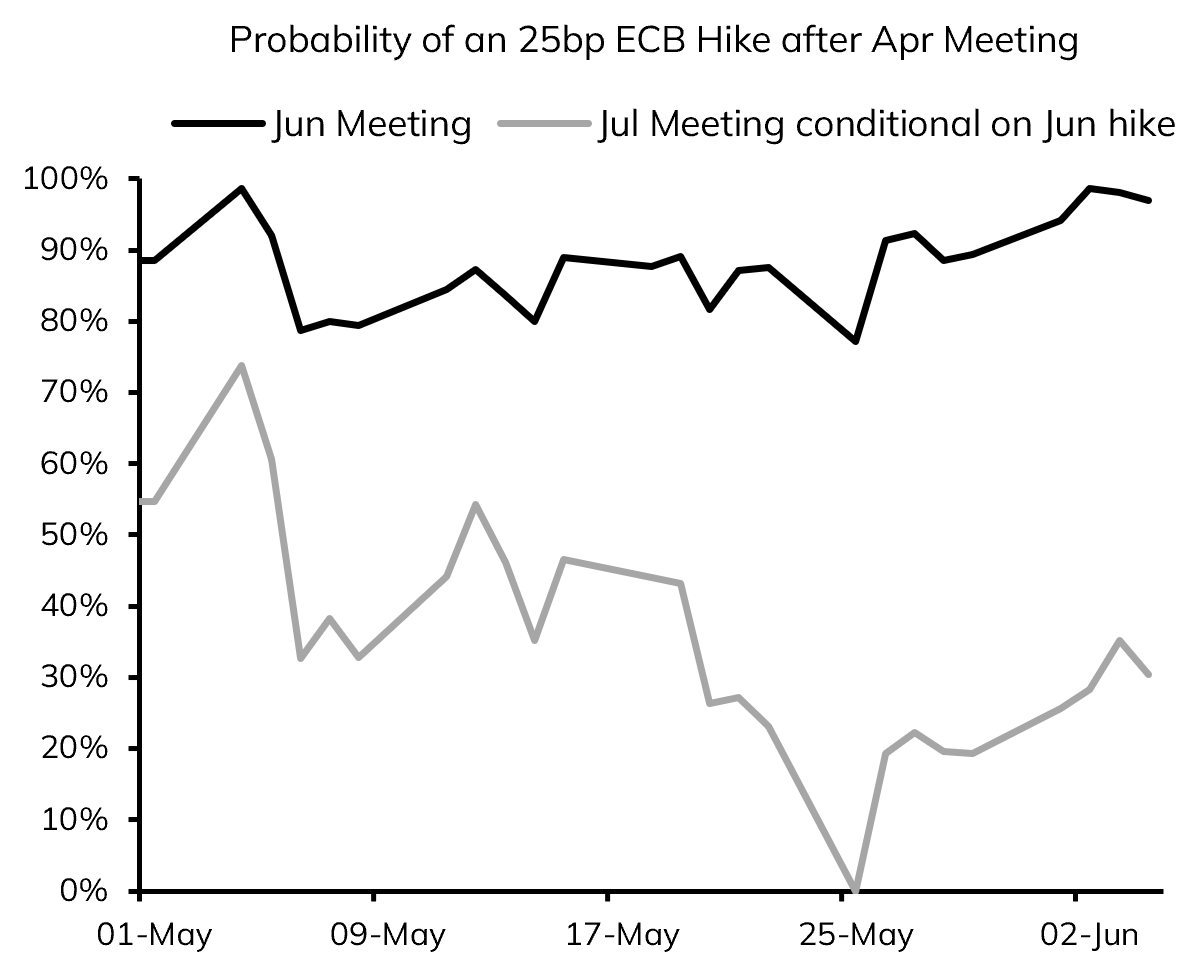

The ECB’s 25bp hike was hawkish, not just “insurance”. Higher core inflation forecasts and upside risks point to more tightening ahead. Lagarde did not pre-commit, but July looks far more likely than markets price.

#LBMACRO#ECB#Inflation

Our latest Weekly previews the Jun ECB meeting as a "Hawkish Hike"

The 25bp is fully discounted, but the tone, risks and projections should skew hawkish, leading markets to read it as the start of a tightening cycle and a back-to-back Jul move still underpriced at 40%.

Our View on the Fed Vindicated

We have long predicted the Fed to hike this year, since the beginning of the energy shock. Today the market has finally priced a full 25 hike by Dec. There is more to come, in our view. This follows today’s very strong May Payroll report, killing once and for all catastrophic views such as “AI is destroying jobs” and thus “the Fed will have to cut rates”.

Markets are turning increasingly hawkish on central banks, as we have been arguing. Pricing of back-to-back ECB hikes has increased, from 0% last week, to 30%. Meanwhile, that of a Sep Fed hike, our modal view, is on the rise, now at 25%. We think both still possess upside.

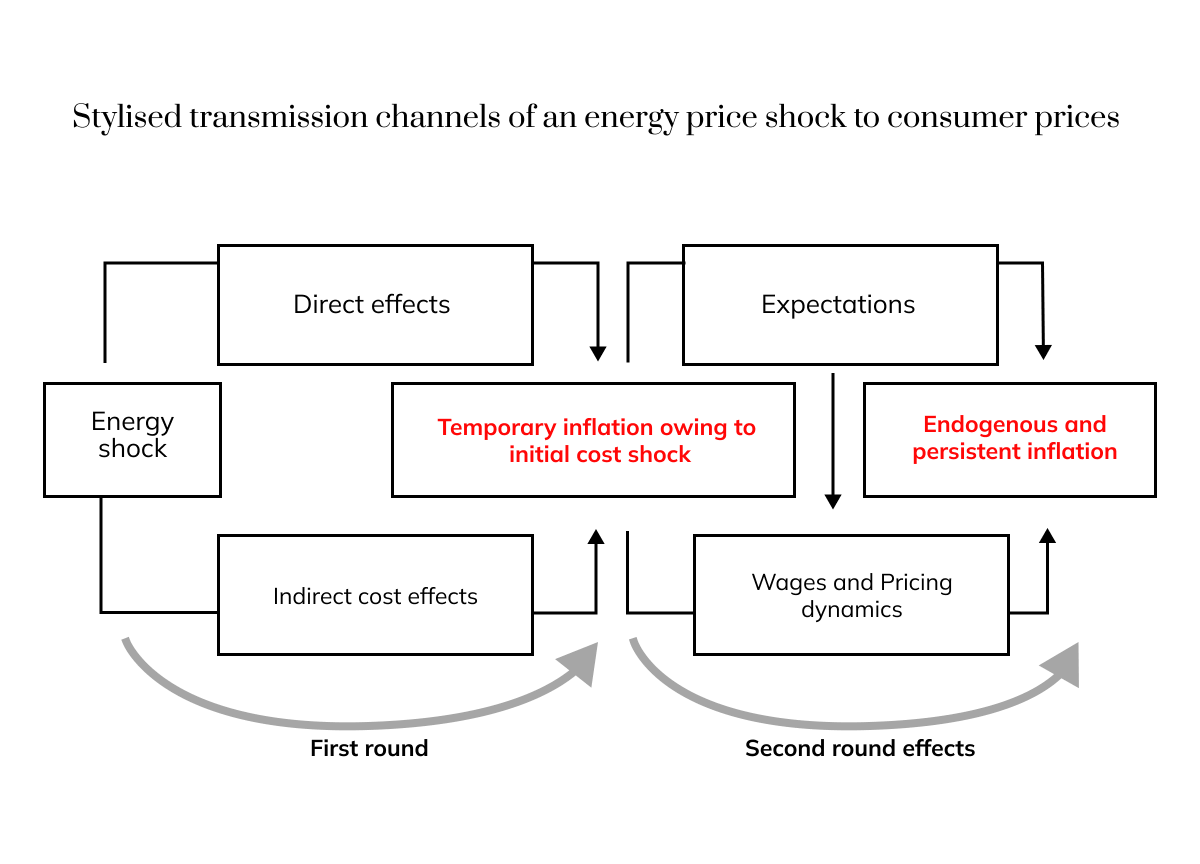

Our Weekly shows that (i) Direct effects (global energy to HICP energy) have already arisen, (ii) the Indirect effects (energy input costs to non-energy goods and services) are working through now, while (iii) Second Round effects have lifted expectations, but wages not yet.

US Equity Bubble? What Bubble?

The US Equity Risk Premium (ERP) – ie the spread between earnings yields and bond yields, a proxy of the return required by investors to be compensated for the extra risk taken in equity investments – has fallen to near zero, i.e. in textbook equity-bubble territory. However, the drop in the US ERP was not due to a fall in earnings yields, which have instead risen alongside an exceptional Q1 earnings season driven by the AI super-cycle. Rather, the ERP has fallen only because of the surge in bond yields, driven by the rise in inflation expectations induced by the energy shock.

Similar considerations to the changes in the ERP apply to its level. Historically, the US ERP has averaged around 2% since 1990, peaking above 7% during the Great Financial Crisis and the early 2010s, when equity prices collapsed. It reached an all-time low at the height of the DotCom bubble in 2000, when it turned negative as the earnings yield fell below 4% while the 10-year bond yield broke above 6.5%. Although today's near-zero reading sits at the lower end of its historical range, this is only due to high bond yields, as equity earnings yields are high alongside record earnings, rather than collapsing under a melt-up in multiples.

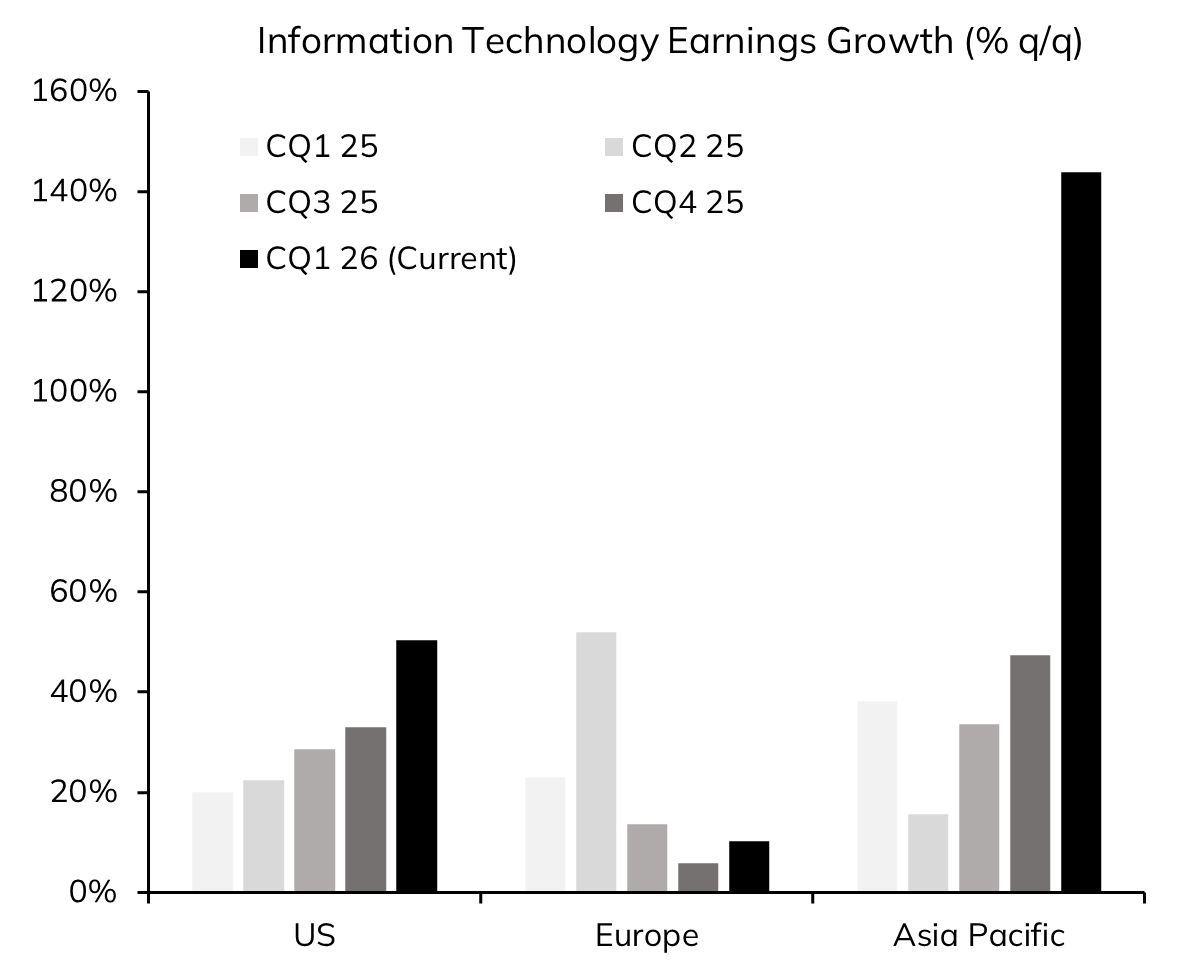

This is especially true for Tech. Tech's intrinsically higher multiples and its dominance in the US economy are the main reason why larger index (S&P 500 etc) valuations have sat at historically high levels since the early 2020s. Yet US Tech, thanks to earnings up around 50% y/y in Q1, currently trades at a relatively low P/E ratio compared to its history, way below the levels reached during the DotCom bubble.

Hence, in our view, the US market is not in bubble territory.

Full breakdown in the first comment.

55 Basis Points and Counting - There's Still Money to be Made on Fed Hikes

Throughout the turbulence of the war and the on-off status of a peace deal, we have consistently argued that the global energy deficit would lift inflation across Developed Market economies, pushing monetary policy in a hawkish direction and yields higher as inflation overpowered concerns around demand destruction.

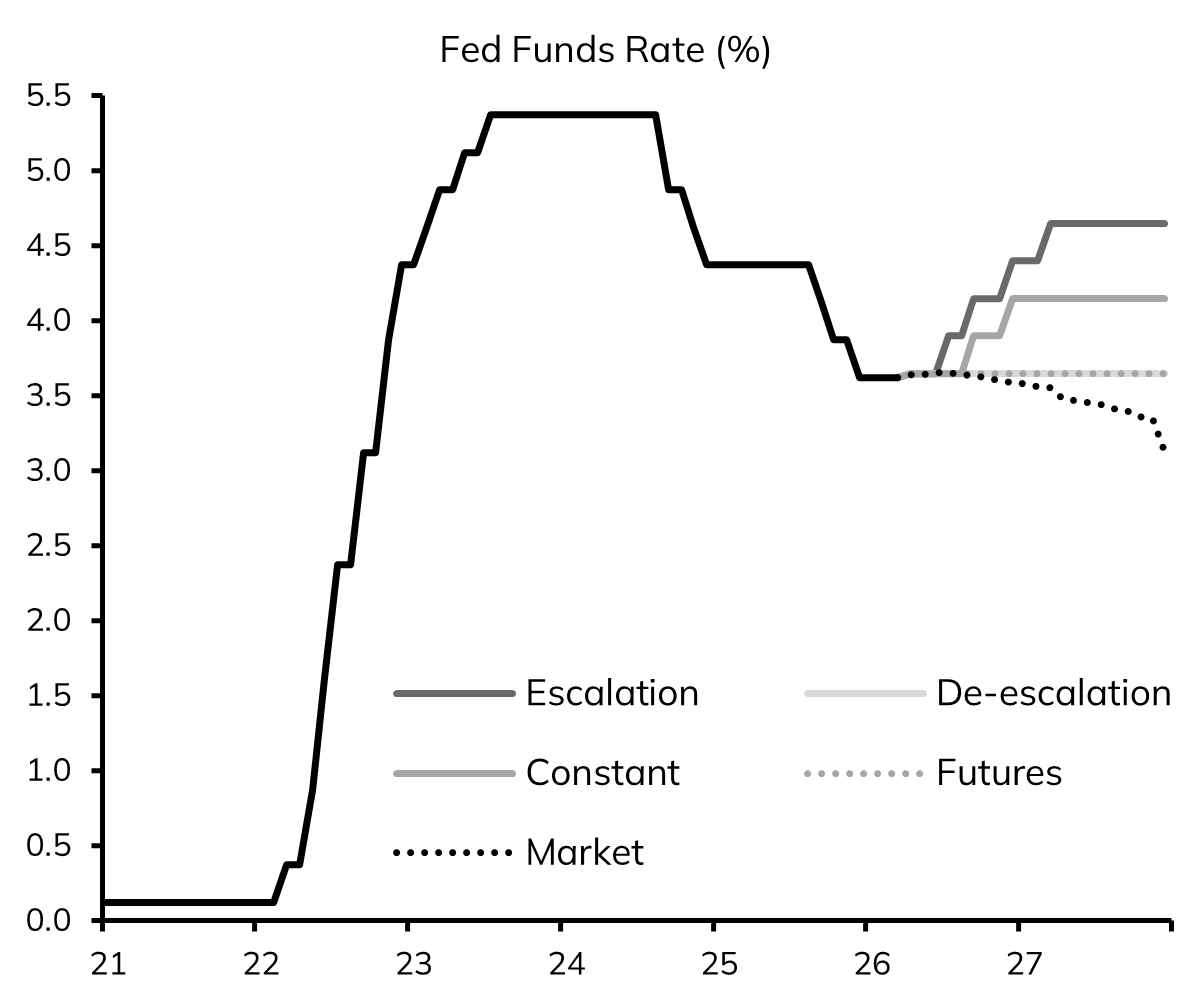

While markets were quick to buy into our view in the Eurozone and UK, there was reluctance to price out rate cuts in the US. This is now changing, with a nearly 70% probability of a Fed hike by Jan 2027 and almost 100% by Mar 2027. This marks a 55bps swing in swap pricing for this year since we posted the analysis below – i.e. those who bet on our views made money – with 22bps of that coming in the past three weeks alone as US data showed, consistent with our long-held views: (i) the labour market in balance, (ii) strong underlying growth, and (iii) rising upstream inflation pressures, set to push US inflation above 4%.

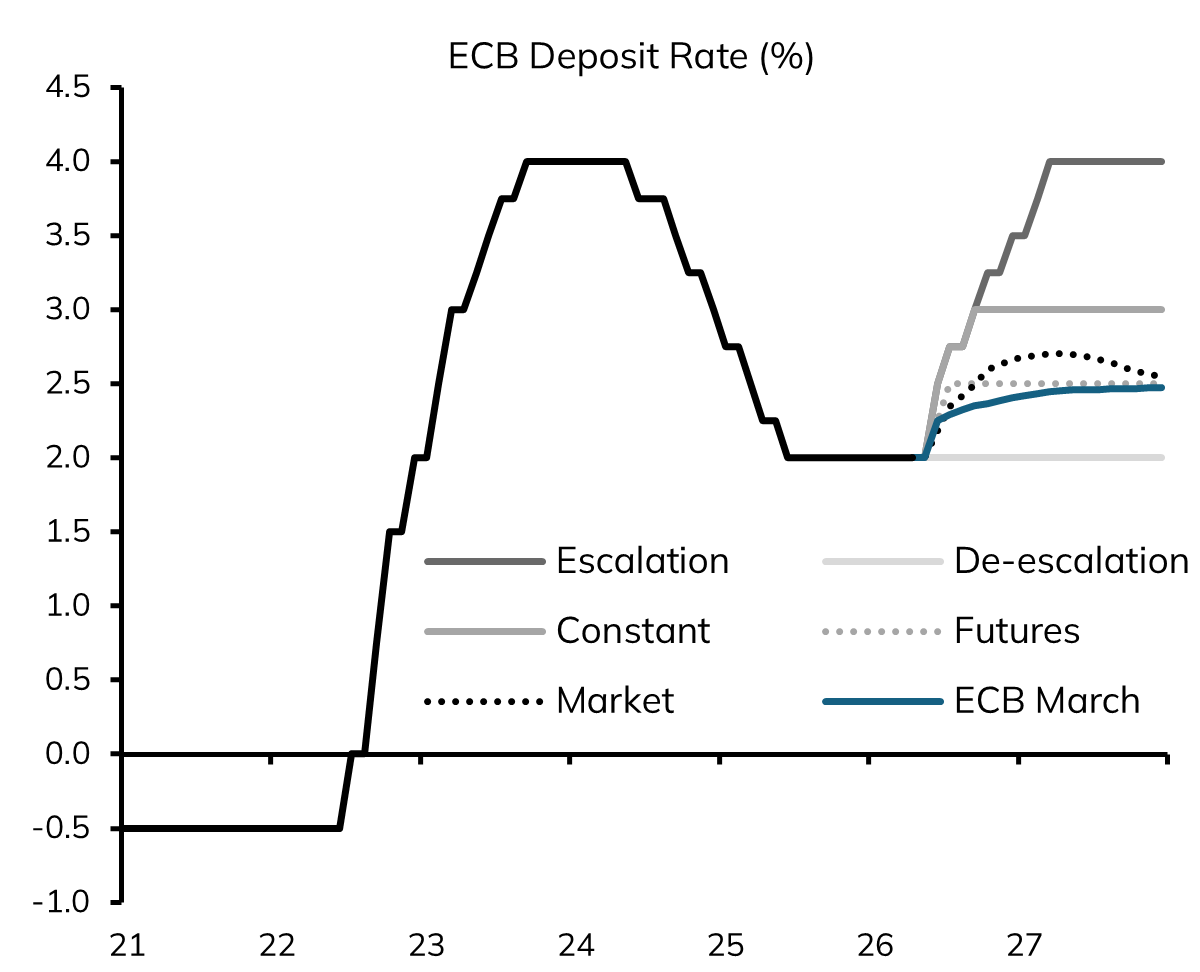

Our latest analysis suggests that pricing for the Fed remains the most dislocated compared with the ECB and BoE despite this convergence. Indeed, under our "Constant" scenario, we see the Fed hiking 25bps in Sep, delivering 50bps of hikes this year. When we posted our view in early Mar, the market was pricing in almost two cuts by year-end. Currently, a Sep hike is 15% priced, with a single hike this year priced at 55%.

You can get full access to our Scenarios and other analysis of this kind either on Substack, or directly via our Emporium App which includes auxiliary notes.

Links are in the comments.

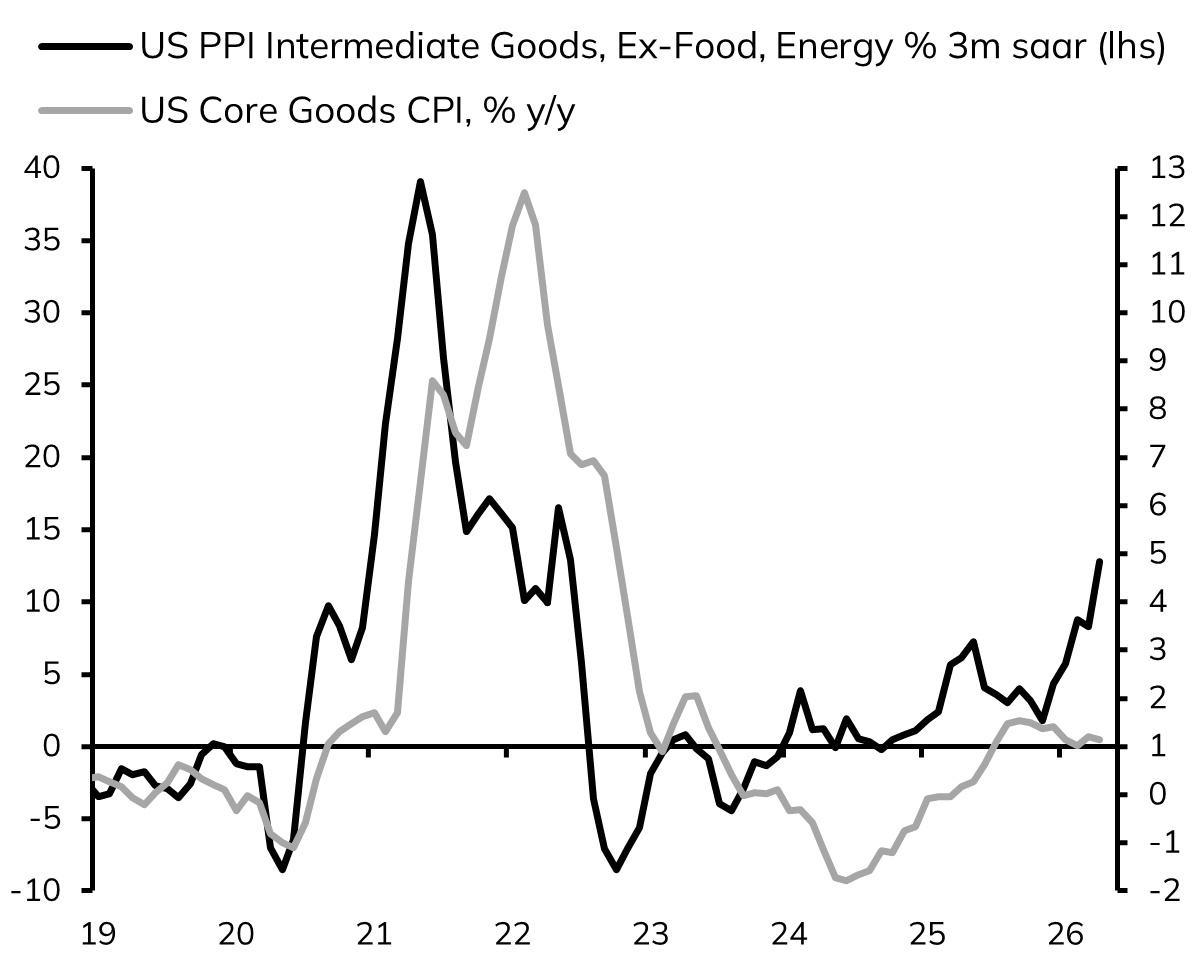

The pass-through from the supply-shock to inflation is happening, leaving Central Banks no other option but to hike.

The leading signals of the pass-through were already visible in the PMI Prices and Supplier Delivery Times components, which surged in both March and April. The confirmation came, in the US, from the April PPI, showing Intermediate Core Goods prices jumping to 12.9% on a 3-month annualised basis, the highest since May 2022. In Germany, from April Wholesale Prices of Core Goods, accelerating sharply tracking the pattern that front-ran the 2022 episode. Globally, the GSCI Agriculture & Livestock commodity index has risen to its highest level since June 2022.

In 2022, the supply-shock dynamics were dismissed as "transitory" by central banks, the Fed in particular, until they (very much) weren't, and the catch-up in monetary policy came at twice the cost. We think the mistake won’t be repeated, and central banks will be quicker to hike, the Fed included.

Comparing the Labour Markets in the US (the Winner), EMU (the Middleman) and UK (the Loser)

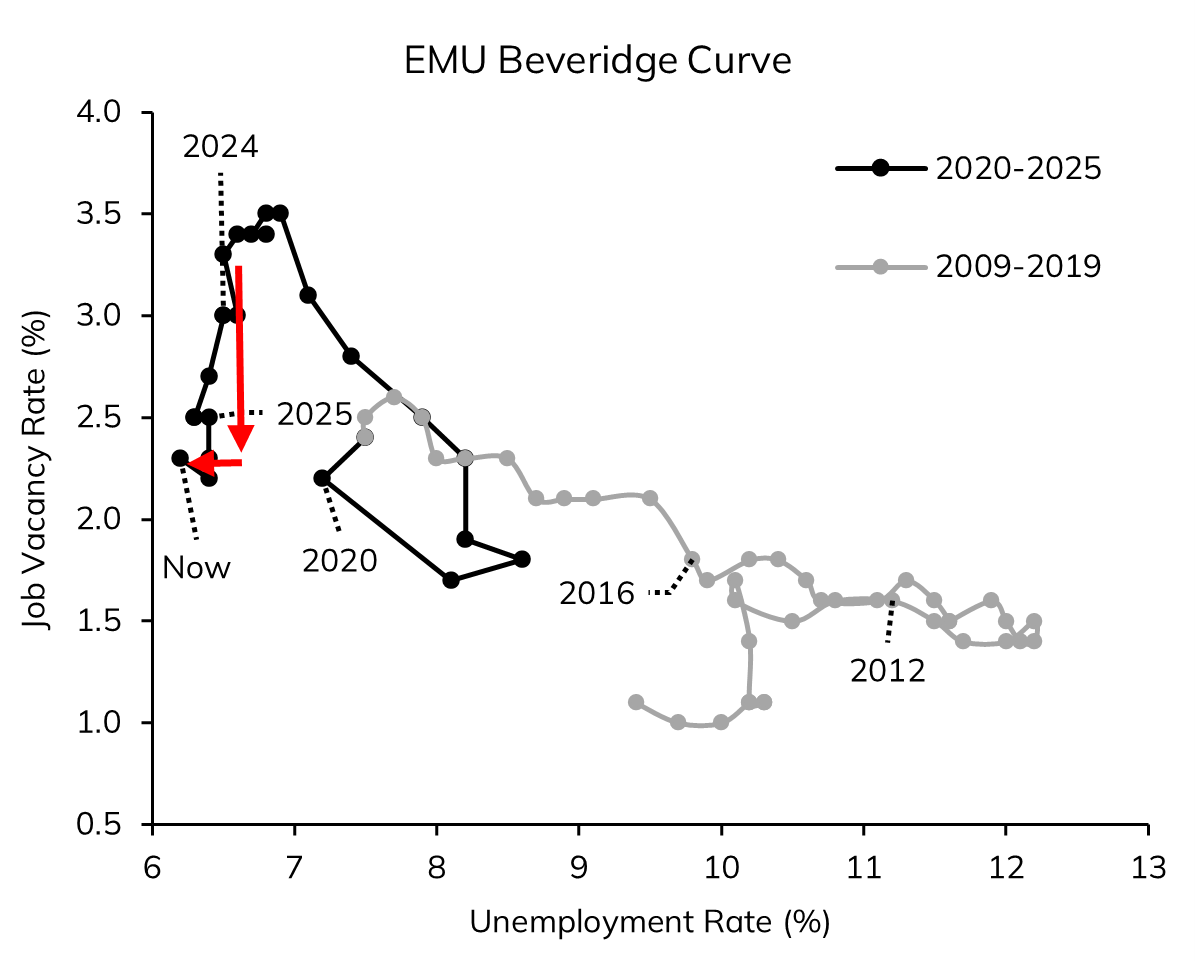

In our analysis, G3 labour markets tell the truth. The US is the winner, as while labour productivity surge, driven by the AI boom, the labour market efficiency is highest, as shown by its low Natural Rate of Unemployment (NRU) and well-behaved Beveridge Curve (i.e. the relationship between job vacancies and unemployment). The EMU is the middleman, as although productivity is weakening, the labour market is getting more efficient, as shown by the ongoing leftward shift of the Beveridge Curve. The UK is the loser, as due to wrong government policies, not only is productivity falling, but also the NRU is rising.

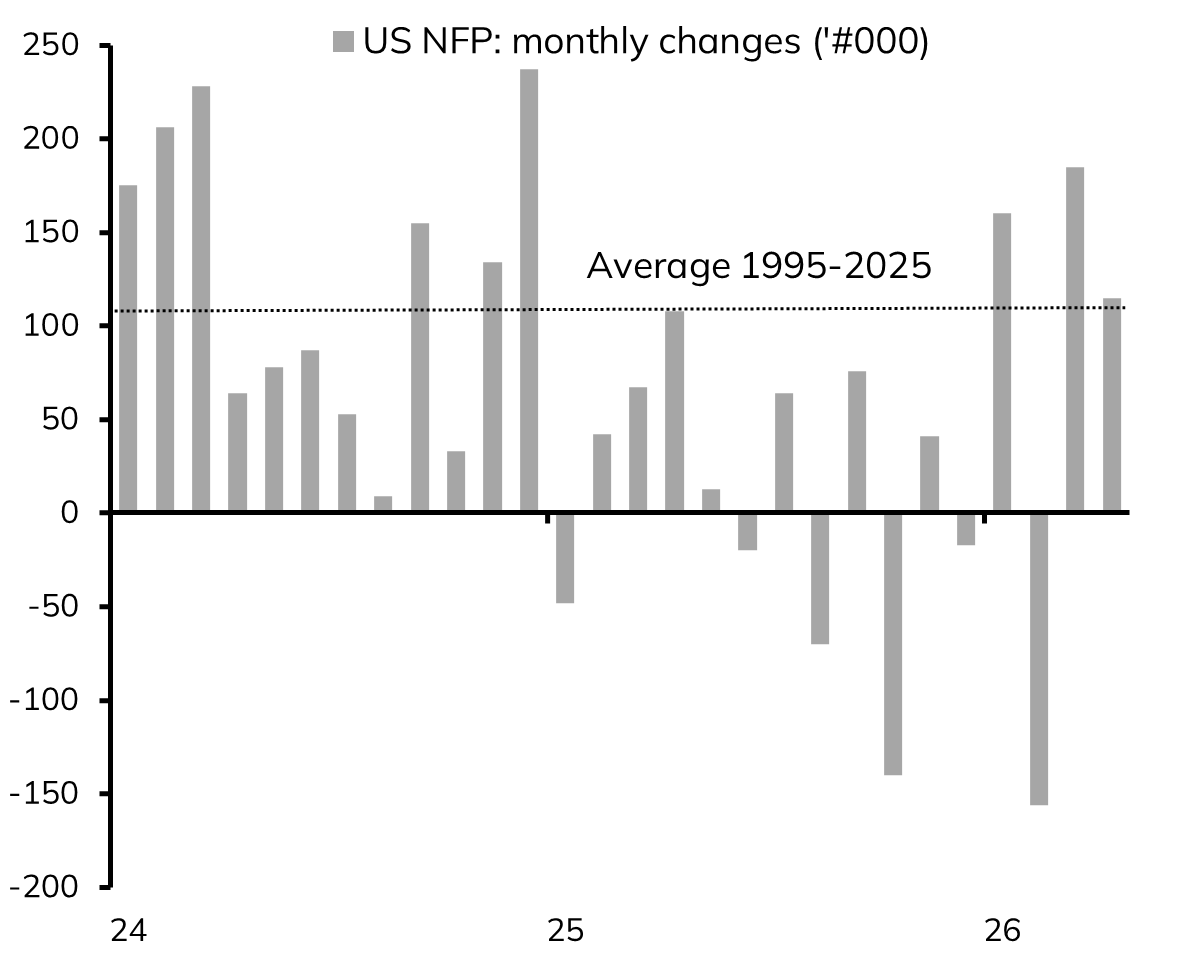

Labour Market Falling Apart? Certainly not in the US!

The April US labour market report supports our long-standing view that at the onset of the ongoing energy-led supply-side shock the US labour market was in good shape. This view is at odds with those envisaging jobs demand falling apart, also because of AI, and thus calling for Fed cuts. Indeed, in the last two months, Non-Farm Payrolls (NFP) average 150k, well above its 113k average since 1995. Moreover, the ongoing drop in labour supply – the Labour Force contracted by another -92k – contributes to keep the labour market in balance, if not tight: at 4.3%, the Unemployment rate is way below its average since 1995 and any measure of the neutral rate.

Hence, no drama, no need to ease monetary conditions from the labour market side of the Fed mandate. On the contrary, inflation is clearly deviating from the Fed’s mandate, way exceeding its 2% target on any possible metric, and things can only get worse in the coming months, with gas at the pump sailing towards their all-time highs. Hence, red light to Fed cuts, regardless of Trump and Warsh desires, but increasingly green light to hikes, should the energy-led inflation shock endures.

“Hope Is Not a Good Strategy”: From Surging Energy Prices to Rationed Quantities

https://t.co/0mrCOtWKwS

The energy crisis is extending from prices, already severe, to quantities. Hormuz has been closed for longer than the 2-month transit lag to Europe and Asia, meaning the last cargoes already arrived around 20 Apr. Hence the backwardation in oil futures, with long-dated contracts well below the front, looks dangerously optimistic. The clearest signal comes from jet fuel: rationing in Europe could begin as early as this month, or June at the latest, with potentially thousands of flight cancellations. Europe is most exposed. The US less so, but not immune. We hope this bleak outlook does not materialize, but as we say in finance: “Hope is not a good strategy”.

Such a supply shock, sending inflation through the roof while rationing quantities, risks triggering a non-linear "Rece-flation" outlook, analogous to the 1970s. A combination that standard central bank price-based modelling, ours included, struggles to capture. The message seems unambiguous: risks around inflation and policy rates are skewed to the upside. At the next policy meeting, in June, we expect the ECB to hike by 50bps and the BoE by 25bps, barring either an unlikely total de-escalation or a catastrophic economic meltdown. For the Fed, markets finally seem to converge towards our call, but only starting to price-in a tightening bias by end-2026.

Surging Oil and Sky-Rocketing Eurozone Inflation Expectations add pressure on the ECB to hike

Our view ahead of the ECB policy meeting on 30 Apr, has been consistently for a “Hawkish Hold”, with rising probabilities of a rate hike, way higher than the mere 10% priced in by the market.

Indeed, inflation prospects have increasingly deteriorated since Lagarde’s speech on 20 Apr, which encouraged market expectations of unchanged ECB rates in Apr.

Since then, front-end Brent prices have increased by a huge $20, thus almost reaching the ECB “Adverse” scenario, and business surveys, from the PMI to the ECB SAFE, have highlighted mounting price pressures.

(a couple of days ago we posted a comment on the PMI)

Yesterday, the ECB survey of consumers’ Inflation Expectations, conducted between 5 and 30 March, added another nail in the coffin of dovish views, supporting our hawkish views.

Indeed, the survey showed inflation expectations moving up sharply: on a 12-month-ahead horizon, from 2.5% to 4% if measured by the median, and from 4.4% to 6.8% if measured by the mean.

Moreover, and most importantly from a monetary policy standpoint, expectations on a 3-year horizon jumped from 2.5% to 3.0%, very close to the peak recorded during the last inflation crisis, in Q4 2022, signalling a de-anchoring particularly worrisome for the credibility of the 2% ECB inflation target.

All this will put the ECB Council in big trouble at tomorrow's meeting.

Should they decide not to hike - we envisage chances of hold-hike almost even, contrary to the mere 10% market probability of a 25bps hike – and energy prices persist, we would expect the ECB to hike by 50bps in Jun, as by then inflation expectations would be even more disanchored.

Our Scenarios and Central Bank Previews

https://t.co/Y3yU3Blid2

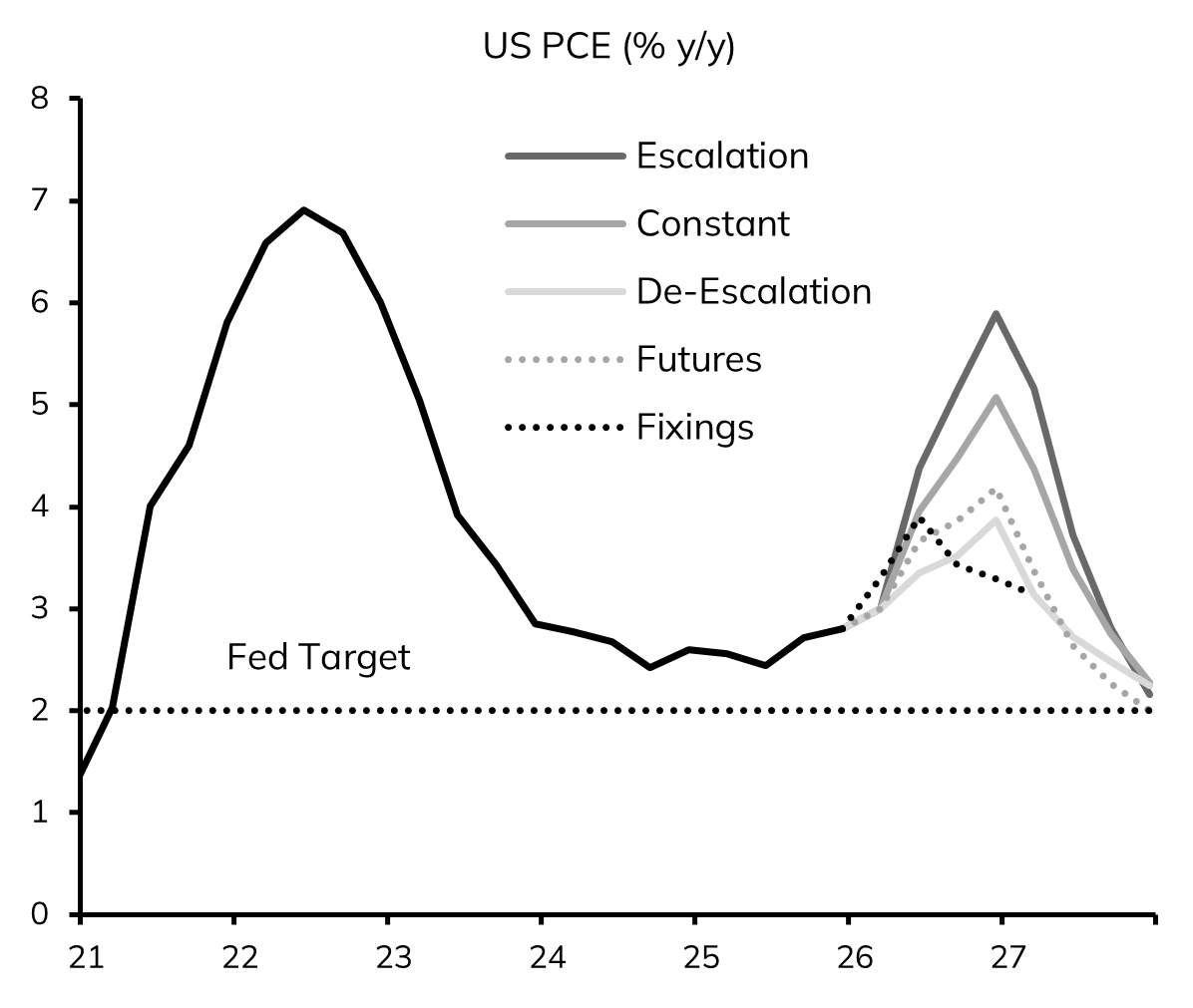

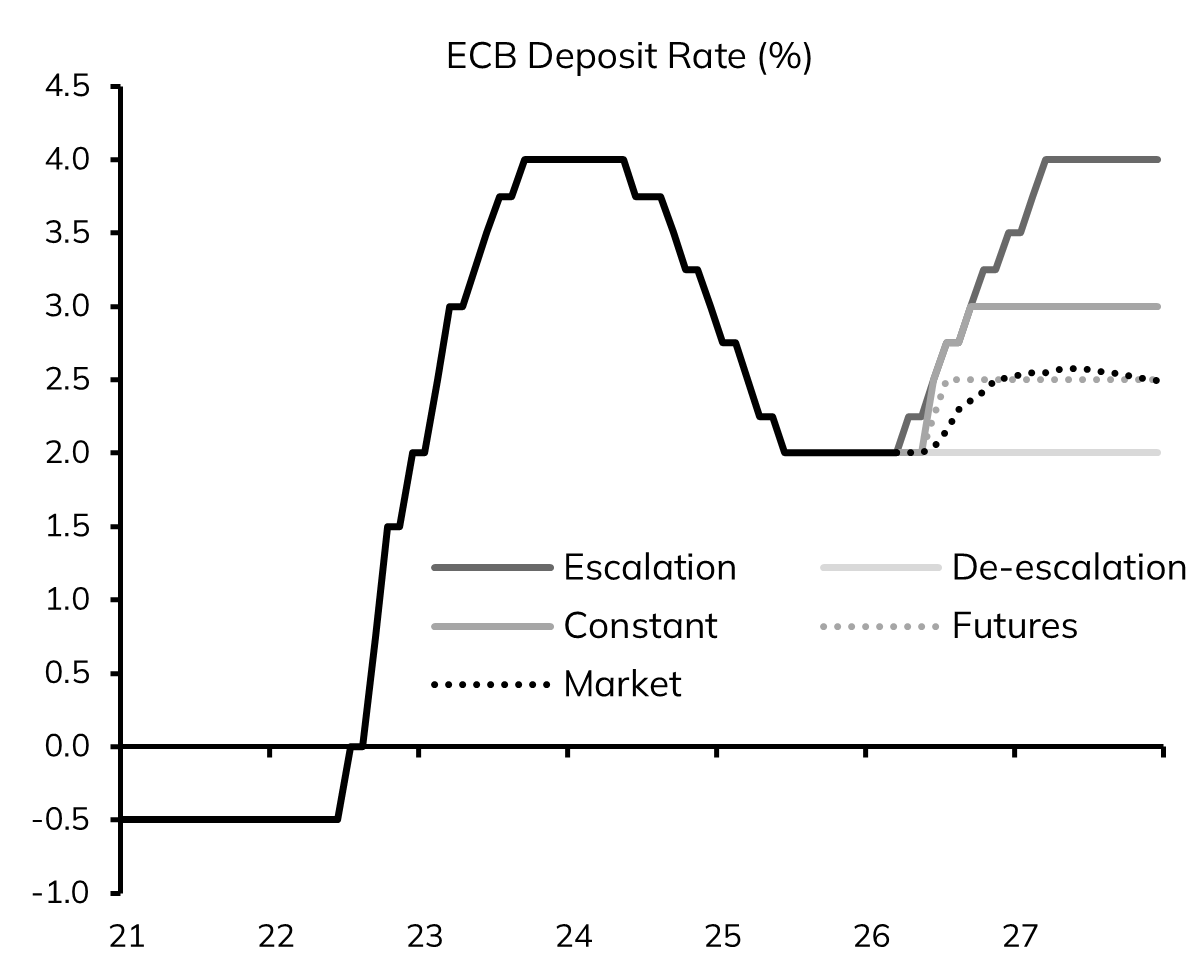

In our latest Weekly we update our scenario analysis that we adopted to model macro and central bank uncertainty since the beginning of the US-Iran war.

Since last week, following the steep rebound of energy prices, our scenarios have hardened.

They now embed monetary policy tightening by both the ECB and the BOE even under our optimistic 'Futures' scenario, showing pronounced 'backwardation', consistent with a reopening of Hormuz in the not-too-distant future.

The tightening is more pronounced under our 'Constant' scenario, with spot energy prices remaining constant at their current levels. Under this scenario, even the Fed would eventually hike rates.

This week we envisage a 'hawkish hold' by the ECB, the BoE as well as the BoJ, with the Fed still in 'wait and see'. Risks of a rate hike for the ECB and the BoE, while still low, are not negligible, contingent on the surge in oil prices. Even so, the hiking would be just postponed for the first three central banks, with material risks of a 50 bp hike in June.

Inflation, Not Unemployment is the Main Headache for the Fed

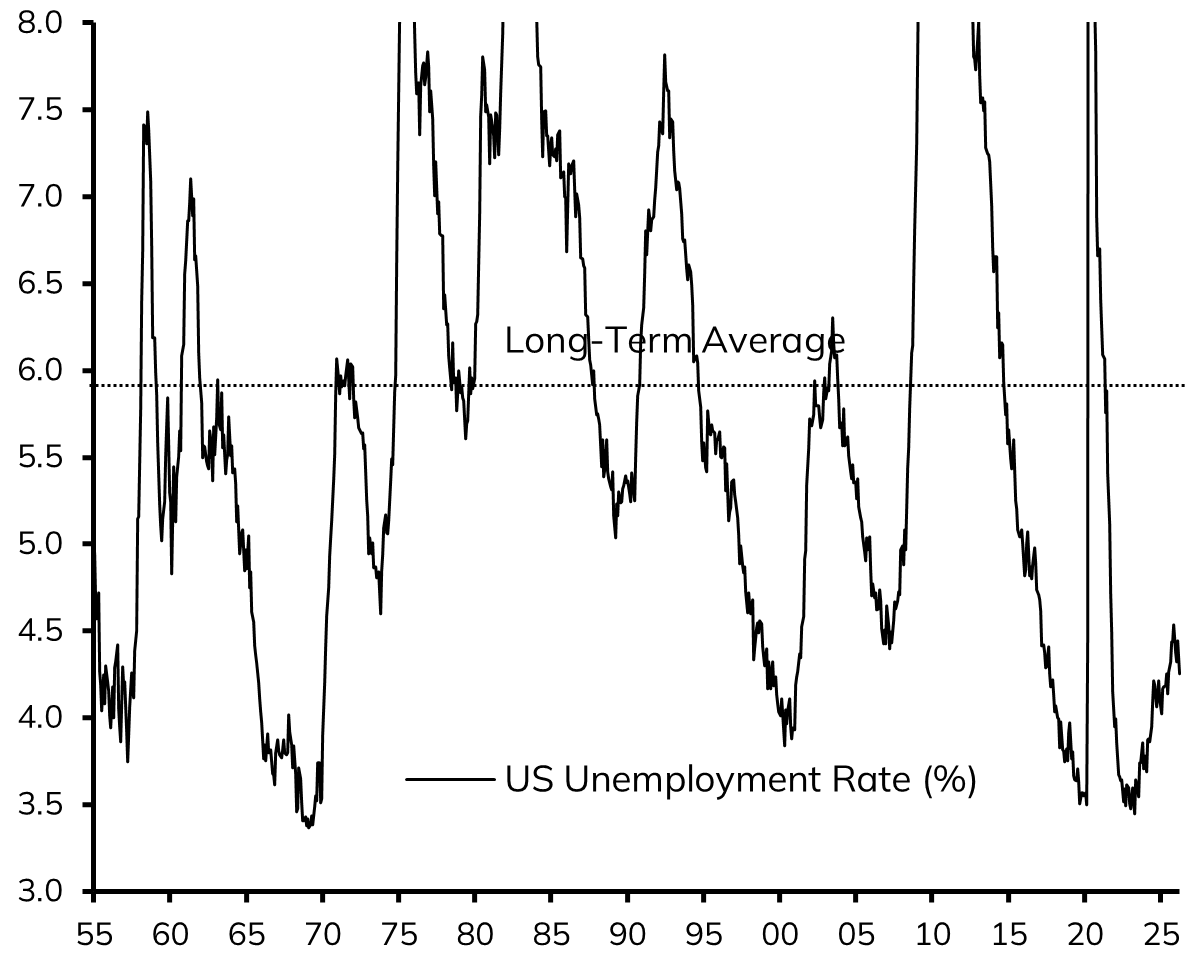

On net, the US March Labour Market report was a firmer than expected. Seeing through monthly volatility, cumulated revisions to Non-Farm Payrolls (NFP) in Jan-Feb were negligible, while the upside surprise in March was meaningful at 186k net jobs creation versus 78k expected by the Consensus.

The neater indication on the state of the US Labour Market stems from the Unemployment rate, which fell from 4.44% to 4.26%, its lowest since last June and a level signalling a balanced, if not firm situation, being well below it 5.8% long-term average (see the chart below).

In the first quarter of the year, NFP increased on average by 68k per month, which is quite satisfactory given: (i) the negative legacy from the government shutdown; (ii) extremely adverse weather conditions; (iii) the large contraction in Labour Supply (-396k only in March); and very early negative effects from the war to Iran.

Overall, we maintain that pre-war the US economic situation was solid and rising underlying inflation, evident in Core PCE dynamics, was the main problem. This asymmetry in favour of inflation deviating from the Fed target way more than unemployment is poised to be exacerbated by the war, given the upside pressures stemming from energy prices, eventually passing through other sectors.

Hence, we maintain that, on the one hand, the Fed won’t be in the position to cut rates, despite illiterate political pressures to do so, and on the other hand, should the supply shock endure, the FOMC will eventually need to shift its focus towards the need start hiking rates. Surely, Powell was cautious in his last appearance, but things will change should energy prices stay where they are, let alone if they go up further.

Moving Towards The "Escalation" Scenario

https://t.co/W8bI1CAGeX

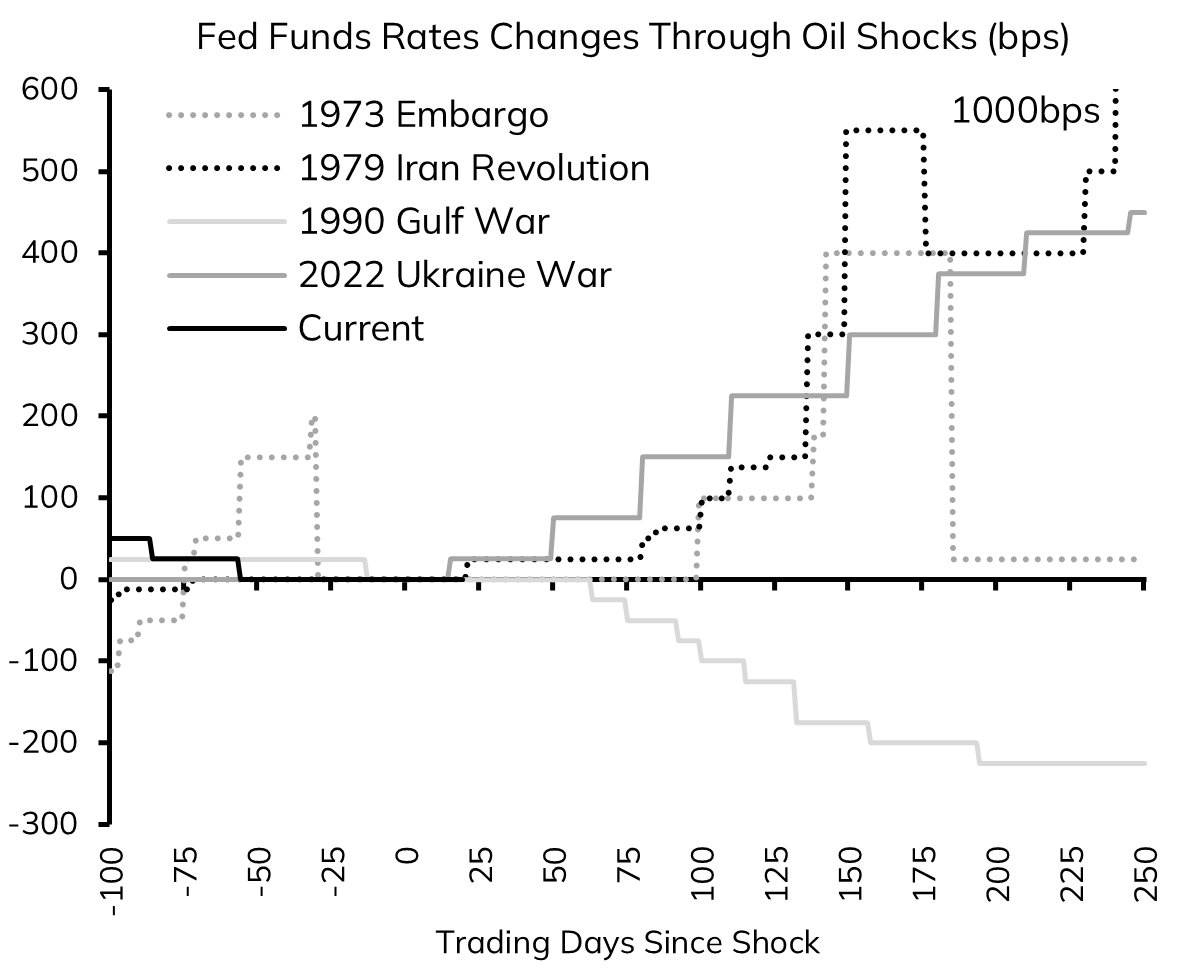

In our latest Weekly, we compared the four major oil shocks in history, ranking the current one as the second most severe after the 1973 embargo at this stage of the shock, ie one month into it (Chart 1). Today's Oil price action only reinforces this assessment, with the base case shifting alarmingly towards what we termed "Escalation” in our Inflation and Policy Rates scenarios.

The message from history is unambiguous, as the Fed hiked in every major oil shock, with the sole exception of 1990 (Chart 2). That exception is instructive, as it was not a pure energy shock, but a poisonous mix with the Savings & Loans crisis. Should the current shock remain primarily energy-driven, central banks will hike. Should it instead trigger a financial crisis, say from Private Credit insolvencies, the playbook changes.

Equities and bonds are falling in tandem, as in every supply shock. The drawdown so far is multiple derating, consistent with the repricing in rates, while earnings have not yet been downgraded. Past episodes suggest the next leg lower comes from there.

Risks continue to move as we envisaged. Inflation targeters are priming to hike in Apr, the Fed will follow, and "De-escalation" looks increasingly like the tail, not the mean.

Inflation and Policy Rates Scenarios For Fed, ECB and BoE

https://t.co/i8huFPj1yk

When, at the onset of the war, we were envisaging the ECB hiking rates by 100bps and the Fed raising rates rather than cutting, we were seen as almost lunatic by the consensus. Needless to say, uncertainty is still king, but the more the supply shock goes on, the more this scenario becomes likely. Indeed, the market is converging to our knee-jerk view and is now pricing in close to 75bps of rate hikes for the ECB, while taking off the table the cuts envisaged for the Fed, after having priced-in a hike yesterday. Should oil prices stay at current levels, however, this would be far from enough. Moreover, in an escalation scenario, where oil climbs steadily say to $125, we think the ECB will have to hike by 200bps and the Fed by 75-100bps. Should the Fed not do it, due to political pressures, the market will do the job and the yield curve would bear steepen aggressively. We shall see: as said, uncertainty is king, and yesterday's TACO episode is a case in point, but the more the supply shock goes on, the more the bearish scenarios become reality.