राजस्थानी सिर्फ़ एक बोली नी, म्हारी पहचान, संस्कृति अर इतिहास री आवाज़ है🗣️

जिण धरती नै वीर, लोकदेवता अर लोककला दी,

उण धरती री भाषा नै आज भी मान्यता रो इंतजार है।🙏

If you wanted to do a medium size manufacturing business in india you need to answer this much govt employees ( tekedaras) ;

1.GST

2.Income Tax

3.professional tax

4.FSSAI

5.local municipality (trade license)

6.factories license

7.pollution control board

8. Fire and safety

9.labour license (shops and establishments)

10. Employees professional tax

11. Employer professional tax

12. ESI

13. EPF

14. DGFT in case of import and export

15. Customs

16. Local police for shift

17. ROC in case of company

18. RBI -in fema matter

This is not exhaustive list.

Need to file at least 250 forms

1 earner and there at least 25 people ready to eat whether you make profit or loss that not matters them

वित्त वर्ष 2025-26 की Income Tax Return भरने में जल्दबाज़ी न करें।

चौथी तिमाही के TDS statements तथा बैंकों, कंपनियों, Mutual Funds आदि द्वारा दी जाने वाली Statement of Financial Transactions (SFT) की अंतिम तिथि 31 मई 2026 तक है। इसलिए इस तिथि से पहले आपके AIS, TIS और Form 26AS में सभी आवश्यक सूचनाएँ पूर्ण रूप से दिखाई देना संभव नहीं है।

अतः अपना ITR भरने से पहले, 31 मई 2026 के बाद उपलब्ध updated AIS, TIS और Form 26AS अवश्य डाउनलोड कर मिलान करें। आवश्यकता हो तो portal पर सूचना अपडेट होने के लिए कुछ दिन का समय भी दें।

✅ जल्दबाज़ी से बचें

✅ TDS/TCS और आय का मिलान करें

✅ उसके बाद ही सही एवं पूर्ण ITR दाखिल करें

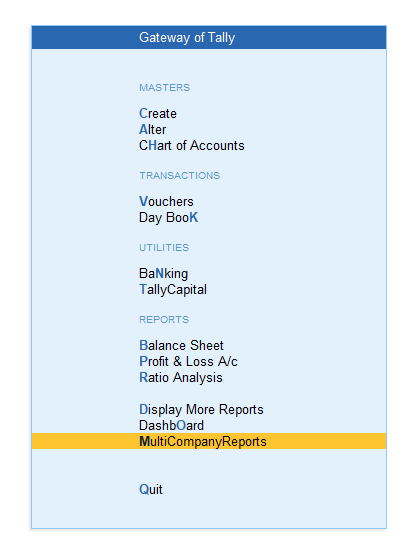

Big Thanks to @nirmal_ghorawat sir for this useful and worthy TDL development for Tally Prime

It Provide Multi Company Report for all Active Company in Single window in Tally Prime, Summary Of Balance Sheet / Profit & Loss Account - for Birds Eye view / Tracking @tallysolutions

Enter in Company Row to move to Tally Prime Balance Sheet / Profit & Loss Account

Should be Useful for CAs / Accountants to Track Activity in Company ~ Sales, Purchase, Stock etc

TDL Link : https://t.co/O8880m16yl

YouTube : https://t.co/xWJ8jjPC9m

प्रधानमंत्री मोदी की अपील :

• जहाँ संभव हो, Work From Home को प्राथमिकता दें।

• एक साल तक सोना खरीदने से बचें।

• पेट्रोल-डीजल की खपत कम करने के लिए मेट्रो से सफर करें, पार्सल रेल से भेजें और कार का कम इस्तेमाल करें।

• खाने के तेल का उपयोग कम करें।

• रासायनिक खाद का इस्तेमाल आधा करें और प्राकृतिक खेती की ओर बढ़ें।

• विदेशी ब्रांडेड उत्पादों का उपयोग कम करें और स्वदेशी को अपनाएँ।

• एक साल तक विदेशों की यात्रा कम करें।

राजस्थान 📍

राजस्थानी लाडू बाटी का आनंद ही कुछ और है। उपलों के जगरो में सिके हुए कत किसको पसंद नहीं??

घी-गुड और सूखे मेवो से निर्मित देशी चूरमा लाडू ना केवल स्वादिष्ट अपितु स्वास्थवर्धक भी होते है।

लेकिन यदि आपको उपलों का अभाव तो शहरी क्षेत्र में यह विधि भी उपयुक्त.. 🙌

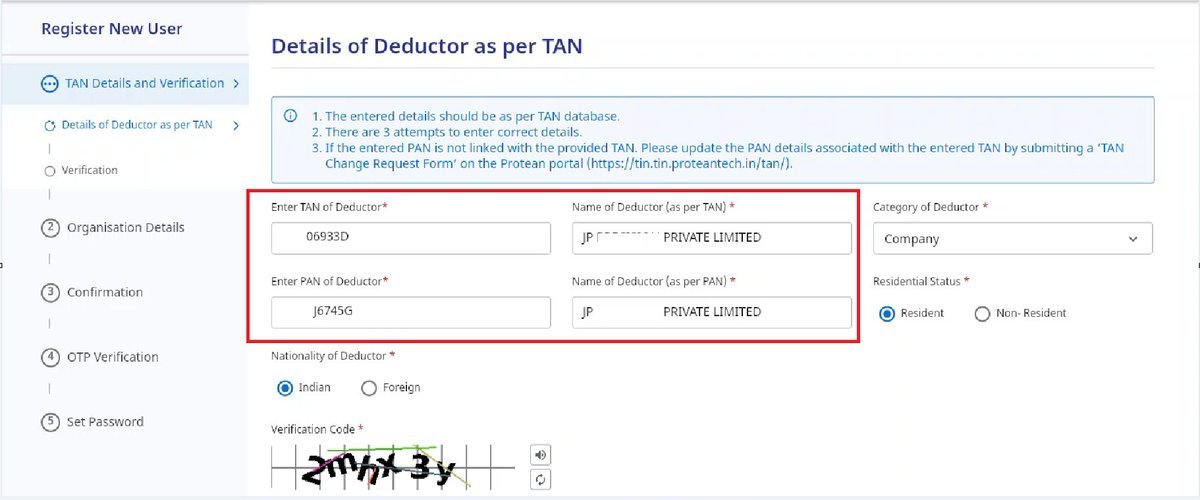

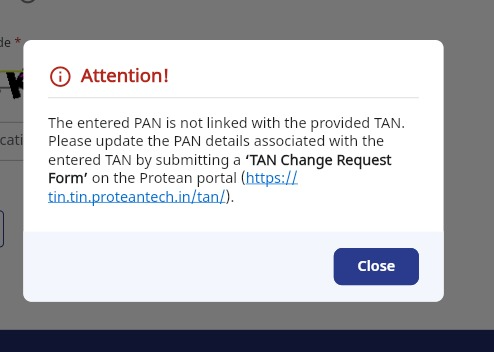

Taxpayers/professionals are currently facing several technical/practical issues with revamped TRACES Portal.

Please comment with the issue you are facing right now on TRACES along with screen shot

I will collate all genuine issues & submit them to CA @pankajgshah - Vice-Chairman @dtc_icai , for taking them up with the Department at Central Level

I will start with the first one - TAN/PAN mismatch in case of LLP/Company registration.

While registering TAN of a Company/LLP, the system is asking to link TAN with PAN through the TAN change Request form. While Incorporation, both PAN and TAN are allotted by the Dept. & mentioned on the same Certificate of Incorporation.

No seperate linking required!!

@IncomeTaxIndia

Income Tax Section 194T - कल तक partners Interest और remuneration पर करोड़ों रुपये TDS के रूप में जमा हुए हैं जो छोटी और मझौली firms के अधिकांश मामलों में Partners को Refund होगा ।

भविष्य के लिए इस प्रावधान पर तार्किक विचार कर उचित परिवर्तन किया जाना उचित होगा ।

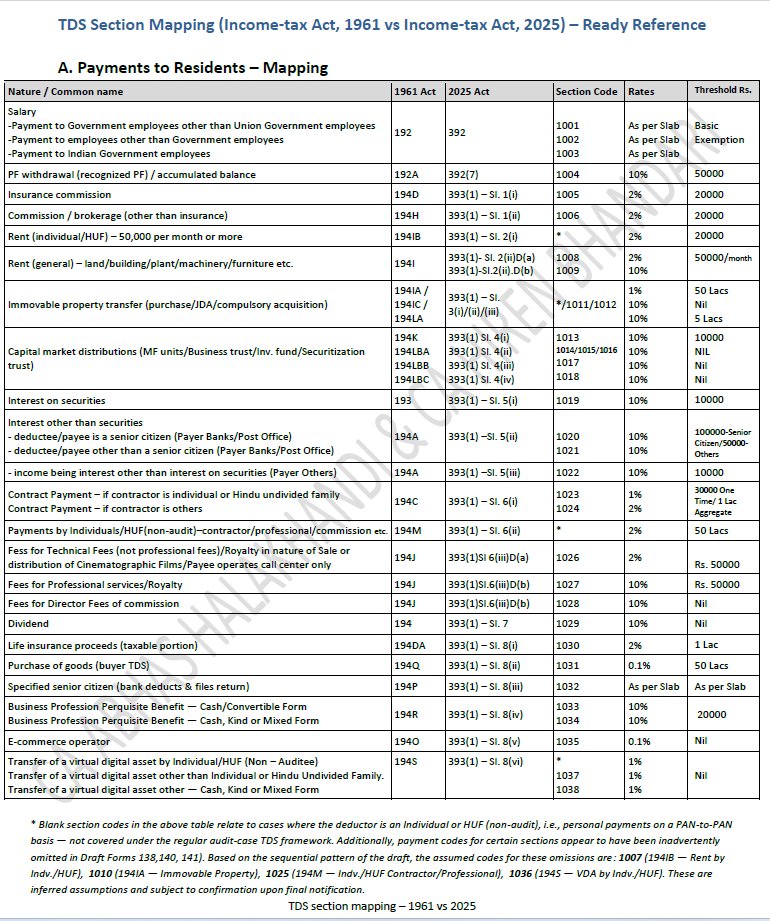

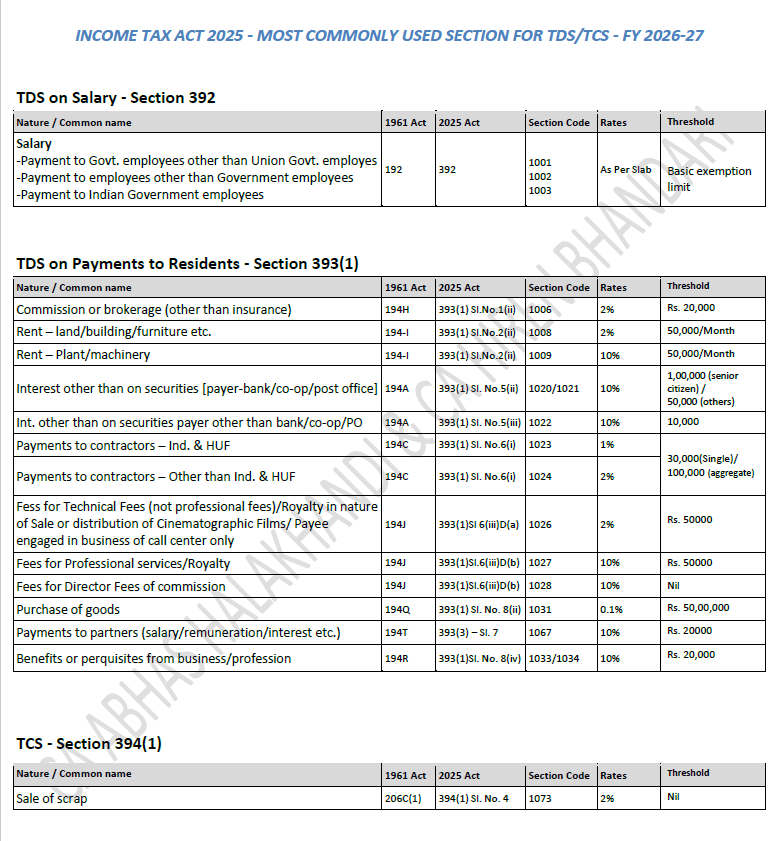

Most Comprehensive One pager for TDS/TCS Sections, Codes and Threshold under New Income Tax Act 2025

✅ Comprehensive one-page sheet for all new TDS/TCS sections, codes,thresholds

https://t.co/wJ2lecCh5T

✅Most common TDS/TCS sections used by MSMEs

https://t.co/KQ0MhTKXAk

Payment for Apr 2026 begins from May 1st under New Act!!

If you handle TDS/TCS…

SAVE THIS.

This single tool covers:

✔ Smart search across all sections

✔ Filter by nature / type (TDS vs TCS)

✔ Old vs updated section mapping

✔ Rate + threshold + form visibility in one view

✔ Built-in calculator for quick working

✔ Dashboard insights for better understanding

✔ Clean, structured interface for instant lookup

No need to open multiple tabs again.

Link 🔗 https://t.co/Yr9LZUZ87o

Some TAN Application were pending for processing

@IncomeTaxIndia some TDS Payment were pending as application for TAN was not processed

Kindly extend due date for payment by 7 days

Partners के interest/remuneration पर TDS का नया provision छोटे-मध्यम partnership firms के लिए अनावश्यक cash flow stress पैदा करेगा।

अधिकांश मामलों में partners को यही TDS refund के रूप में वापस मिलेगा।

पहले tax काटो, फिर refund दो — यह व्यर्थ compliance है।

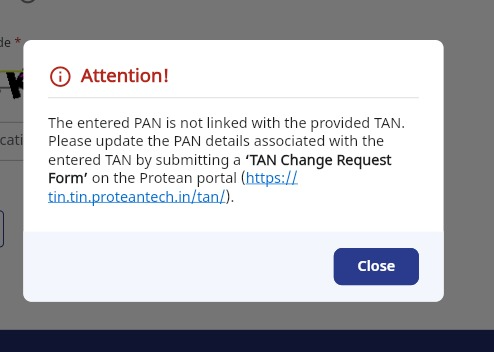

TRACES portal has been revamped, but every revamp should not come at the cost of mental harassment of taxpayers and professionals!!

While registering TAN of a Company/LLP, the system is asking to link TAN with PAN through the TAN change Request form.

While Incorporation, both PAN and TAN are allotted by the Dept. & mentioned on the same Certificate of Incorporation. No seperate linking was required earlier.

Due to this technical issue on the revamped portal, TAN registration and account login are not possible from last 10 days.

Request @IncomeTaxIndia to urgently resolve this issue.

Request professionals to please rt & comment if facing same issue🙏

अगर आपको Stage V chronic kidney disease, तो भी GST Returns time से भरिये ..!!

अगर health issues की वजह से, आपका business बंद है , तो भी physical verification में अपने business premises में मिलिए , वार्ना आपका registration cancel हो जायेगा !!

Hello Friends,

This is not a joke, but brief facts of the case before the Honourable Bombay High Court.

The Assessee was a proprietary concern engaged in collecting used plastic PET bottles and supplying them in bulk for recycling. It had obtained GST registration effective from 16.03.2023 and had been discharging tax obligations.

In March 2024, the proprietor was diagnosed with Stage V chronic kidney disease, because of which the business became temporarily non-operational, though returns continued to be filed through the consultant. On 29.05.2024, the Department conducted a field visit and found the business non-operational. On 11.06.2024, a show cause notice was issued under Rule 21(a) alleging that no business was being carried on from the declared place of business, and the registration was suspended from the same date. On 26.06.2024, the Assessee filed a detailed reply manually, and on 27.06.2024, the representative personally appeared and explained that the stoppage was temporary due to the proprietor’s illness. Despite this, the Department passed the cancellation order on 22.08.2024 under Section 29(a) read with Rule 21(a). Thereafter, the Assessee applied for revocation, but another show cause notice dated 27.09.2024 was issued proposing rejection, and an ex parte order dated 10.10.2024 rejected the revocation application on the ground that no reply had been filed.

Whether cancellation of GST registration under Section 29(a) read with Rule 21(a), when the business was temporarily non-operational due to the proprietor’s serious illness, could be sustained when the show cause notices and impugned orders did not contain reasons or deal with the Assessee’s reply.

The Bombay High Court held that this was a genuine case where the proprietor’s serious ill-health had led to the temporary discontinuance of business, but the Department failed to consider that explanation at all. The Court found that neither the show cause notices nor the impugned orders contained any discussion, reasoning, or findings on the Assessee’s reply, and therefore the action was mechanical, standardised, arbitrary and without authority of law. Accordingly, the Court quashed the show cause notices dated 11.06.2024 and 27.09.2024, set aside the cancellation order dated 22.08.2024 and the revocation rejection order dated 10.10.2024, and directed that the setting aside of these orders should result in restoration of the Assessee’s registration. Liberty was, however, given to the Department to initiate fresh proceedings in accordance with law, with proper reasons and a hearing.

G.B. Traders v. Union of India - Bombay High Court

Writ Petition No. 8990 of 2025 | 01-Apr-2026

Support this & amplify the issue — Retweet now

अप्रैल बीत गया… लेकिन IncomeTax की तरफ से अब तक एक भी ITR utility जारी नहीं

और ये तब है जब इस मुद्दे पर अदालतें बार-बार साफ निर्देश दे चुकी हैं — फिर भी वही ढिलाई, वही खामोशी

जब नियम बनाने वाले ही नियमों को हल्के में लेने लगें,

तो करदाता कानून का सम्मान क्यों और कैसे करे?

ये सिर्फ देरी नहीं… सिस्टम पर भरोसे की परीक्षा है।

Ram Bajaj

8696424223

For GST Update, Join this Group

https://t.co/ARE0hYIeoV

Dear Friends,

In numerous FORM GST DRC - 01A, the proper officer takes shelter of Section 61 for the issuance of the same.

The Moot Question is: Can FORM GST DRC - 01A be issued invoking the provisions of Section 61 of the CGST/SGST Act or not?

Section 61(1):

The proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform him of the discrepancies noticed, if any, in such manner as may be prescribed and seek his explanation thereto.

Rule 99(1):

Where any return furnished by a registered person is selected for scrutiny, the proper officer shall scrutinize the same in accordance with the provisions of section 61 with reference to the information available with him, and in case of any discrepancy, he shall issue a notice to the said person in FORM GST ASMT-10, informing him of such discrepancy and seeking his explanation thereto within such time, not exceeding thirty days from the date of service of the notice or such further period as may be permitted by him and also, where possible, quantifying the amount of tax, interest and any other amount payable in relation to such discrepancy.

Rule 142(1A):

The proper officer may, before service of Notice to the person chargeable with tax, interest and penalty, under sub-section (1) of Section 73 or sub-section (1) of Section 74 or sub-section (1) of section 74A, as the case may be, communicate the details of any tax, interest and penalty as ascertained by the said officer, in Part A of FORM GST DRC-01A

Even from a conservative reading, it is amply clear that whether a FORM GST ASMT - 10 is issued or NOT, the issuance of FORM GST DRC-01A DOES NOT derive its power from Section 61.

When you get instances like this, please evaluate whether this is a fishing or a roving inquiry rather than searching a case law which may or may not have the required requisities.

Pro Tip: Please stick to the Act and Rules for pointing out the anamoly

@GSTwithNihal

#gst #gstwithnihal #litigation #caselaw #law #rules