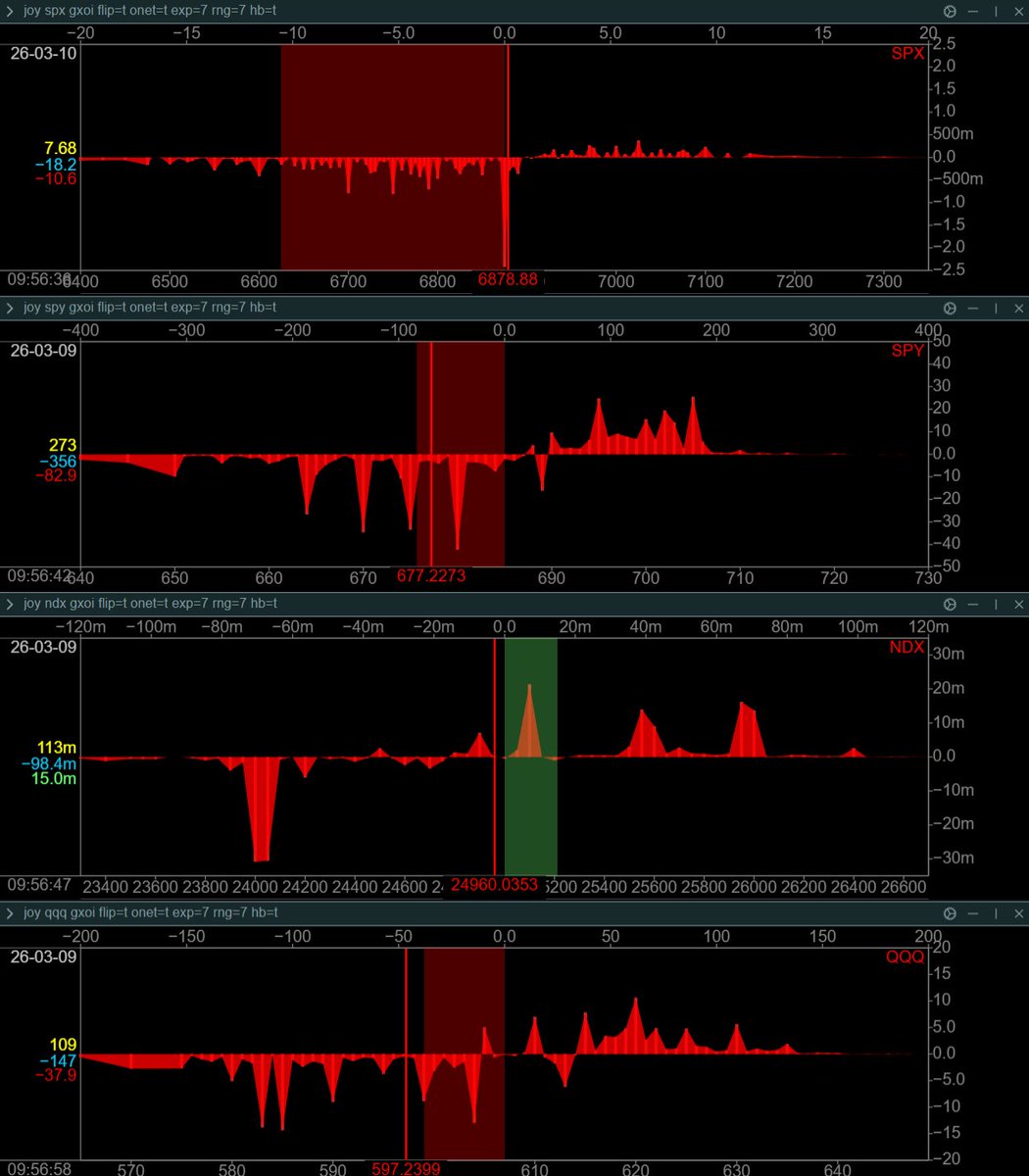

$SPX $ES_F $NQ_F RTH Open

· Premarket slightly down since this morning, tech appears to be the most impacted at -0.5% via $QQQ.

· Futures are following this same pattern while $CL is up 1.78%.

· Yesterday's VIX expiration allowed for a quick rally to 6900 on $ES_F but massive call selling at that level broke the momentum during the last RTH session

· The market remains unstable ahead of Friday's OPEX, significant activity is expected today with Goolsbee/Kashkari and Trump is likely to speak during his visits later today.

$SPX Map

· POLR : 6830 - 6930

· Still in negative gamma with a gamma flip level around 6885

· Call-driven market at 53% with the largest volume strikes at 6900, 6950 & 7000, biggest put strikes at 6850 & 6800

· 0DTE Straddle is much larger than last week at 47 reflecting the instability heading into the end of the week.

· $VIX has also switched into negative gamma with a flip at 21.50, heavy strikes at 23/25 show a clear pricing of volatility.

Interpretations are mine | Datas from @ConvexValue & @QuantData

En tant que trader d'orderflow sur $ES & $NQ, mon carnet d'ordres et mes tapes sont mes seuls yeux sur le marché. Longtemps je pensais que le flux suffisait mais j'ai réalisé qu'il me manquait une dimension essentielle : l'exposition gamma (GEX)

Premier thread simple pour comprendre comment je combine ça pour ne plus trader à l'aveugle via @ConvexValue 🧵👇

$SPX $ES_F $NQ_F Open RTH

La demande réelle est visible via l'alignement des ratios sur le $SPX. L'argent entre activement sur le marché, bien que le Delta du SPX soit négatif (-49,5K, ventes de Calls), les ratios de flux sur $SPY et $QQQ (≈ >1.1) signalent une pression acheteuse sous-jacente.

Même si le delta $SPX affiche un rouge vif (-71.8K), c'est potentiellement une signature de "vente de prime" institutionnelle et non une pression vendeuse directionnelle.

$SPX Map

POLR : 6960

La zone noire centrale montre une trajectoire stable dérivant vers 6960, une zone de résistance faible pour le prix qui semble confirmer un slow grind haussier.

Gamma positif (Long Gamma) avec un VIX stabilisé pour l'instant sur les 15 encourageant un slow grind, une compression de la volatilité est notable.

Implied Probability 0DTE :

$SPX Straddle (ATM) : 46.32 / [6900.00 - 6980.00]

$ES_F (SPX Spot: 6945.57)

Straddle (ATM) : 46.61 (0.67%)

C70% : 7033.71 | IV : 12.21%

C50% : 7023.65 | IV : 13.05%

P50% : 6943.15 | IV : 19.61%

P70% : 6902.89 | IV : 22.78%

$NQ_F (NDX Spot: 25675.23)

$NQ Straddle (ATM) : 153.79 (0.60%)

C70% : 25976.35 | IV : 13.15%

C50% : 25916.08 | IV : 13.47%

P50% : 25644.87 | IV : 16.17%

P70% : 25554.46 | IV : 17.39%

Interpretations are mine | Datas from @ConvexValue

![lonelyRaph's tweet photo. $SPX $ES_F $NQ_F Open RTH

La demande réelle est visible via l'alignement des ratios sur le $SPX. L'argent entre activement sur le marché, bien que le Delta du SPX soit négatif (-49,5K, ventes de Calls), les ratios de flux sur $SPY et $QQQ (≈ >1.1) signalent une pression acheteuse sous-jacente.

Même si le delta $SPX affiche un rouge vif (-71.8K), c'est potentiellement une signature de "vente de prime" institutionnelle et non une pression vendeuse directionnelle.

$SPX Map

POLR : 6960

La zone noire centrale montre une trajectoire stable dérivant vers 6960, une zone de résistance faible pour le prix qui semble confirmer un slow grind haussier.

Gamma positif (Long Gamma) avec un VIX stabilisé pour l'instant sur les 15 encourageant un slow grind, une compression de la volatilité est notable.

Implied Probability 0DTE :

$SPX Straddle (ATM) : 46.32 / [6900.00 - 6980.00]

$ES_F (SPX Spot: 6945.57)

Straddle (ATM) : 46.61 (0.67%)

C70% : 7033.71 | IV : 12.21%

C50% : 7023.65 | IV : 13.05%

P50% : 6943.15 | IV : 19.61%

P70% : 6902.89 | IV : 22.78%

$NQ_F (NDX Spot: 25675.23)

$NQ Straddle (ATM) : 153.79 (0.60%)

C70% : 25976.35 | IV : 13.15%

C50% : 25916.08 | IV : 13.47%

P50% : 25644.87 | IV : 16.17%

P70% : 25554.46 | IV : 17.39%

Interpretations are mine | Datas from @ConvexValue](https://pbs.twimg.com/media/G-Ef00-W4AA0OR4.jpg)

![lonelyRaph's tweet photo. $SPX $ES_F $NQ_F Open RTH

La demande réelle est visible via l'alignement des ratios sur le $SPX. L'argent entre activement sur le marché, bien que le Delta du SPX soit négatif (-49,5K, ventes de Calls), les ratios de flux sur $SPY et $QQQ (≈ >1.1) signalent une pression acheteuse sous-jacente.

Même si le delta $SPX affiche un rouge vif (-71.8K), c'est potentiellement une signature de "vente de prime" institutionnelle et non une pression vendeuse directionnelle.

$SPX Map

POLR : 6960

La zone noire centrale montre une trajectoire stable dérivant vers 6960, une zone de résistance faible pour le prix qui semble confirmer un slow grind haussier.

Gamma positif (Long Gamma) avec un VIX stabilisé pour l'instant sur les 15 encourageant un slow grind, une compression de la volatilité est notable.

Implied Probability 0DTE :

$SPX Straddle (ATM) : 46.32 / [6900.00 - 6980.00]

$ES_F (SPX Spot: 6945.57)

Straddle (ATM) : 46.61 (0.67%)

C70% : 7033.71 | IV : 12.21%

C50% : 7023.65 | IV : 13.05%

P50% : 6943.15 | IV : 19.61%

P70% : 6902.89 | IV : 22.78%

$NQ_F (NDX Spot: 25675.23)

$NQ Straddle (ATM) : 153.79 (0.60%)

C70% : 25976.35 | IV : 13.15%

C50% : 25916.08 | IV : 13.47%

P50% : 25644.87 | IV : 16.17%

P70% : 25554.46 | IV : 17.39%

Interpretations are mine | Datas from @ConvexValue](https://pbs.twimg.com/media/G-Ef0zlWYAA5V9Z.png)

![lonelyRaph's tweet photo. $SPX $ES_F $NQ_F Open RTH

La demande réelle est visible via l'alignement des ratios sur le $SPX. L'argent entre activement sur le marché, bien que le Delta du SPX soit négatif (-49,5K, ventes de Calls), les ratios de flux sur $SPY et $QQQ (≈ >1.1) signalent une pression acheteuse sous-jacente.

Même si le delta $SPX affiche un rouge vif (-71.8K), c'est potentiellement une signature de "vente de prime" institutionnelle et non une pression vendeuse directionnelle.

$SPX Map

POLR : 6960

La zone noire centrale montre une trajectoire stable dérivant vers 6960, une zone de résistance faible pour le prix qui semble confirmer un slow grind haussier.

Gamma positif (Long Gamma) avec un VIX stabilisé pour l'instant sur les 15 encourageant un slow grind, une compression de la volatilité est notable.

Implied Probability 0DTE :

$SPX Straddle (ATM) : 46.32 / [6900.00 - 6980.00]

$ES_F (SPX Spot: 6945.57)

Straddle (ATM) : 46.61 (0.67%)

C70% : 7033.71 | IV : 12.21%

C50% : 7023.65 | IV : 13.05%

P50% : 6943.15 | IV : 19.61%

P70% : 6902.89 | IV : 22.78%

$NQ_F (NDX Spot: 25675.23)

$NQ Straddle (ATM) : 153.79 (0.60%)

C70% : 25976.35 | IV : 13.15%

C50% : 25916.08 | IV : 13.47%

P50% : 25644.87 | IV : 16.17%

P70% : 25554.46 | IV : 17.39%

Interpretations are mine | Datas from @ConvexValue](https://pbs.twimg.com/media/G-Ef0zQW8AA5lmH.jpg)

![lonelyRaph's tweet photo. $SPX $ES_F $NQ_F Open RTH

La demande réelle est visible via l'alignement des ratios sur le $SPX. L'argent entre activement sur le marché, bien que le Delta du SPX soit négatif (-49,5K, ventes de Calls), les ratios de flux sur $SPY et $QQQ (≈ >1.1) signalent une pression acheteuse sous-jacente.

Même si le delta $SPX affiche un rouge vif (-71.8K), c'est potentiellement une signature de "vente de prime" institutionnelle et non une pression vendeuse directionnelle.

$SPX Map

POLR : 6960

La zone noire centrale montre une trajectoire stable dérivant vers 6960, une zone de résistance faible pour le prix qui semble confirmer un slow grind haussier.

Gamma positif (Long Gamma) avec un VIX stabilisé pour l'instant sur les 15 encourageant un slow grind, une compression de la volatilité est notable.

Implied Probability 0DTE :

$SPX Straddle (ATM) : 46.32 / [6900.00 - 6980.00]

$ES_F (SPX Spot: 6945.57)

Straddle (ATM) : 46.61 (0.67%)

C70% : 7033.71 | IV : 12.21%

C50% : 7023.65 | IV : 13.05%

P50% : 6943.15 | IV : 19.61%

P70% : 6902.89 | IV : 22.78%

$NQ_F (NDX Spot: 25675.23)

$NQ Straddle (ATM) : 153.79 (0.60%)

C70% : 25976.35 | IV : 13.15%

C50% : 25916.08 | IV : 13.47%

P50% : 25644.87 | IV : 16.17%

P70% : 25554.46 | IV : 17.39%

Interpretations are mine | Datas from @ConvexValue](https://pbs.twimg.com/media/G-Ef01RWAAA8sPM.jpg)