While the rest of crypto is chasing the same 50m users, our ecosystem has built a network with reach to the rest of the world. Sooner or later everyone will realize that distribution is the only durable competitive advantage for a network and that we have a massive lead.

#Stellar $XLM

A lightbulb 💡 moment at Stellar’s Meridian when a representative from Axelar spoke about how Stellar has an Edge on the Defi market because of their remittance business.

Essentially, individuals in the regions that benefit from stellar aid assist and the stellar savings accounts, could be the key ingredient to increasing TVL on the network by an easy “click to earn yield” button, or click for a loan button.

This type of decentralized finance could be built into the application itself, seamless and user-friendly, with educational tutorials on how to engage in defi on stellar network .

Catching up on DTCC news so worth addressing this "nothing burger" comment from "the poor man's coindesk".

Being skeptic about crypto press releases is natural and should be the default. Anyone who has lived through the 2018-19 stream of ripple (actually-nothing-burger) bank integration announcements should know that.

@StellarOrg has been conservative throughout the years and we usually share integration news when they're concrete and ideally launched. In this specific case we're working close enough with DTCC to know that this is real and it's big. You don't have to believe it - keep us accountable and call bullshit if this doesn't launch.

It's true that Stellar won't be the only chain supported by DTCC. They're taking the right approach of supporting leading chains and letting the users decide which ones to use. It will be short list, nowhere close to 50. Why is Stellar so early? We have the institutional track record, the trusted tech and the team has successfully built on Stellar in the past (back when Nadine and Dan were in Securrency)

We did not sponsor any DTCC related content. This is news-worthy, as evidenced by the same team inviting Denelle to talk about it, unsponsored.

Seeing lots of great Stellar news and want to join the community to chat? Here's the top two places to do so:

Official Stellar Dev Discord: https://t.co/5H1ZiR49Vm

Largest community Discord: https://t.co/2kP9fY1y7D

See you there! 🫡 stellar:native

If you're in AI pivot to stellar:native.

Seriously, we are hiring: https://t.co/Xj8RVA8Q5b

Or Build your own thing, we have the best community grant program in the industry:

https://t.co/YeqXbkRfqO

Because of this we are starting the next trading competition

Set up a testnet wallet on Zenex and claim USDC from the faucet

Trade and try to finish with the highest PnL If one account gets cooked, just make a new one and run it back

Links below ⬇️

» @BuildOnStellar may have just had the biggest announcement in its 12-yr history, which is saying a LOT. To understand why it matters, you need the 2026 context of what Stellar has shipped this year first.

@The_DTCC news didn't come out of nowhere.

a 🧵

0/ You cannot simultaneously be permissionless cypherpunk resistance money and also be the mainstream global financial system.

Those are two different things, and they are opposites of each other. You literally cannot do both at once.

Let us actually have this discussion then. Aaron, as a starting point, I find you to be a pretty thoughtful guy on a lot of topics, so your views here are surprising to me. It sounds like you may be hearing only from bank people with a financial interest in protecting their regulator moat. I know a lot of people will think I’m just a crypto person spouting off, however, so let me lay my views out in full.

First, on regulation:

You’re right that stablecoins are not banks. That’s the point. Banks run fractional‑reserve, maturity‑transformation businesses and take significant credit risk and duration risk. This is why ALM has been such a critical issue for banks, because even mark-to-market losses that never materialize into defaults can cause a bank failure if they are also losing deposits. You rightly point out that banks do all these things and stablecoins do not. Properly designed stablecoins are full‑reserve payment instruments backed by short‑term government assets. The correct analogy here would be to government money market funds. In fact, this is the blueprint Genius uses, which it took from the NYDFS (regulating stablecoins with no blow ups from 2018 onwards), which it took from the Boston Fed & the money market reform effort post-crisis, which has led to zero MMF failures after 2008. Regulating them like banks because they’re not banks, which both of us explicitly agree upon, is how you get policy mistakes. It would be very bizarre; a bit like saying that because banks use the internet, we should regulate them like tech companies, which would be a clear category error.

So if the correct analogy is a money market fund, what does regulation there look like? Which demonstrably has worked much, much better than banks as a starting point, given the number of money market fund failures (low single digits, with zero for the government complex in the past 40 years) compared to bank failures (roughly 568 by my count).

Money market funds have to hold securities of less than 90 day duration, either in the credit space (prime funds, which are increasingly disfavored) or in the government mmf space (t-bills, agency debt), and both can do collateralized reverse repo.

So what is in a money market fund? Let me quote you: “Genius Act allows uninsured deposits, repo transactions, and 93 day Treasuries, each of which can lose money when fire sale liquidation is needed.”

That’s money market fund instruments! Yes, in theory, t-bills could lose money in a fire sale liquidation, but the point at which the t-bill market stops working is far, far beyond the collapse of the banking sector. T-bills are the safest, cleanest, least capital intensive form of collateral in the world. If our argument is that a collapse of the US treasury itself will destroy stablecoins, then yes, I agree with your assessment. It will also destroy all the banks, and likely the American economy. At some point, the financial system is financially systemic. But it’s nearly impossible to say t-bills themselves are an existential threat, nor the entities holding them. As a reminder, there are $6T of government MMFs and $0.3T of stablecoins, so if stablecoins are such a huge threat, where has been the insane, hair-on-fire panic about government money market funds, zero of which have failed in the past 40 years?

Reverse repo in Genius is also overcollateralized with treasuries and tri-party. Could they fail? Yes. Are they probably inside of pure t-bills? Also yes. Are the big tri-party custodians JPM, State Street, and BNY-Mellon? Yes again. Does that mean we need a banking crisis significantly worse than 2008 for us to have a problem here? One more yes. I will also concede that a banking crisis so large it wipes out our custodian banks will destroy stablecoins; that would also destroy the orderly function of both equity and fixed income markets. Importantly, can stablecoins cause that crisis? No. They would be on the receiving end. The custodians don’t take principal risk to these arrangements, if they fail, it’s not their problem. You need the entity providing the service to fail, otherwise what you would have in extremis (e.g. the fed truly loses control of the long end of the curve, such that we are seeing over 50bps moves intraday) that if stablecoins had a liquidation event in that moment, people could lose a few percentage points on their investment.

That rate environment, as an aside, is typical only of hyperinflation or sovereign default.

Finally we come to uninsured bank deposits: what are we arguing here? We’re arguing that banks are a threat to stablecoins? I actually do believe this. It’s vastly more likely that banks failing where stablecoins held deposits impairs a stablecoin (we’ve seen this happen once already with SVB impairing USDC) than the reverse. If your argument to make things safer is that we should remove bank deposits as an eligible asset for stablecoin reserves, I am 100% fine with this, to be clear. They are in there because of the lobbying of the bank sector and their fears about deposit disintermediation, but I agree that they are vastly more dangerous than the other instruments, so if we want to remove them and further disintermediate banks, I accept that as a financial systemic safety point and it might be a good idea. Food for thought. Uninsured deposits are, after all, vastly, vastly less safe than anything else on this list and banks constantly fail. It raises an uncomfortable question: if uninsured deposits have repeatedly impaired both banks and stablecoins, why are they still treated as ‘safe’ for core payments while structures backed by T‑bills are treated as suspect?

The evidence on that point is conclusive: banks are vastly less safe than stablecoin reserves, excluding bank deposits. If we want to argue for systemic safety, we have to accept that means greatly reducing, not increasing, the role of banks in payments.

Second, on the illegal activity point:

The empirical use case of data is simply not what you claim, and you have the claim backwards.

The ‘illegal randoms’ talking point ignores both the data and the direction of travel. OFAC‑sanctioned addresses are a tiny share of stablecoin volume, and the largest issuers now run real‑time screening and blacklisting that banks can’t match at the account level. We are also much better at targeting them and seizing funds back. How many hundreds of millions of dollars have US banks seized from the Iranian regime since the beginning of our conflict, out of curiosity? On the other hand, we just reached out and grabbed $344mm from them because of USD stablecoins. Can banks take money out of the IRGC’s hands in Iran? No. Are they a funnel sending a large amount of money there? Yes. We have to ask some systemic questions about structure here as well.

There is vastly more crime in the traditional system, because it is opaque and entity stacking obscures the flows as each bank sees only their tiny, tiny fief. A public blockchain lets you see the entire network, and far less of it is anonymous than one might think. To believe that it’s all crime or mostly used for crime, you’d have to believe criminals prefer operating in well-lit areas where everyone can observe vs. in the dark. Banks should be held to the standards of crypto, not the other way around, and if a bank sends any sort of payment and cannot track it at least 5 steps down the chain through other entities, it should be considered a de-facto OFAC and AML violation, if we want to apply equivalent standards. Can any bank in the world measure up to that? No.

When you look at on‑chain flows, the overwhelming use of dollar stablecoins is for dollar clearing across exchanges, OTC desks, and increasingly non‑crypto businesses, not dark‑web markets. This is also an empirical fact. You can look at the flows, or are you telling me that Redot Pay, MiniPay, the entire Visa crypto settlement system, or PayPal are vast international criminal enterprises buying… sandwiches and mobile phone service at scale? This is a 2016 talking point, but if Visa and PayPal are using these rails, do we truly believe they are flagrantly violating their BSA obligations? Should banks still be allowed to issue cards through Visa if so?

Thirdly, on Fed bailouts:

As you know, I’m strongly opposed to bailouts in general (even the 2008-era ones) that do anything other than protect depositors. I’m on record as having said way more executives, equity holders, and bond holders should have lost money than did on some of these things. I think JPM overpaid for Bear Stearns at $2, and I think the bailouts of many of these firms should not have happened without zeroing comp and clawbacks for almost all the rainmakers at these places.

So I’m also equally opposed to bailouts for stablecoins. However, what would a bailout of that sort look like? There’s really only two cases where the stablecoin is failing, as we discussed above:

One, banks are failing and they had uninsured deposits, so what we are talking about is once again bank bailouts. I remain opposed! I also think this strengthens your inadvertent point that maybe stablecoins should be banned from having deposits at banks; an entirely parallel system built purely on treasury collateral so users of payments who aren’t intending to lend money to a real estate billionaire just for the privilege of buying a coffee might be a good thing.

Two, the treasury market itself is exploding. Well, here I concede we’re going to have a bailout, even if I don’t think we should. Will it work? Probably not without causing a huge amount of inflation (separate issue), but I’m not going to pretend the US gov’t is just going to be like “nah fuck it” if the debt stack catches fire. If stablecoins are part of that (along with banks and insurance companies, which are huge holders of treasuries), I will shake my head that we didn’t take the debt problem seriously, but also find it totally unexpected. This is a sovereign bailout / default, not a stablecoin-specific issue. The US treasury market is many, many, many trillions, of which stablecoins hold hundreds of billions. They are the tail on a vast, sprawling, extremely fat dog.

Three, I suppose there is the case of theft / fraud where someone just found a way to straight up steal the money. That… would be very bad? There should not be a bailout for that. There should be criminal liability and someone should end up in jail for a very, very long time. But that’s regular way financial fraud: see also Madoff, Barings, etc. which is possible at any regulated financial entity, and has happened repeatedly right under our nose. We just need to do better at supervision.

Finally and fundamentally this is not a banks vs. crypto issue, this is a “how do we structure the payments system issue”. I will explain that by asking the following question: should you be forced to lend money to a real estate billionaire at 0% to buy a coffee?

If your answer to that is not yes, do you find the current banking system unjust?

Why? That’s what banks are doing on the back-end while forcing everyone to subsidize them with bailouts and well-below market rates. Electronic payments are now a majority of the system, where they used to be a tiny minority before the creeping expansion of the internet. We gave banks a monopoly here through deposits that was never intended. Is it a bad thing to allow competition and a parallel system? I think we have been unwilling to stop and look at this core assumption, but there’s no avoiding it after Genius.

We have to answer the question: should the average American be forced to lend money to billionaires at 0%, and then the government bail out the banks and bankers’ bonuses when it goes wrong?

Banks will scream that this restricts lending, but a huge expansion of lending in the system over the past five years is BNPL, brokerage margin accounts, hedge fund leverage, and private credit. Are any of those unambiguously a social good that we should be subsidizing and paying bankers huge bonuses for?

If our response to that is to instead do it harder, then the crisis that will eventually show up is going to look a lot more like 1929 than 2008. It’s going to be hugely damaging to the average American. It’s not going to lead to a rejuvenation of financial regulation, it’s going to lead people to tear it all down.

I think it’s important we stop to ask about the current configuration of the system before just taking the talking points from the same people making huge bonuses off stuffing the system with BNPL loans and margin debt. After all, if FDIC insurance is the be-all and end-all, how can we square the bank failure vs. MMF failure data? What is the solution for anyone who needs over $250k in an account, which is a huge number of small to medium high turnover, low margin businesses? Do we need massive FDIC reform and to bring back Glass-Steagall and vastly more punitive rules around bank failures for execs and employees? I’m open to that discussion, but there’s no framing where the current system works fine to address these concerns. There's probably also no framing where treasury-backed narrow payments instruments are bad for payments stability (and if they are bad for lending, we can always just lower rates).

So, in short: banks are demonstrably the systemic threat to the payments system, to American financial markets, and to social cohesion. Have we forgotten 2008 so quickly? If stablecoins are such a threat that banks cannot survive them, my answer to that is simple: time to reform the banks.

Circle CCTP is NOW LIVE on Stellar! 🚀

Native USDC moving across 23 chains through @circle’s burn and mint infra!

BIG unlock for builders, payments, treasury flows, and crosschain DeFi on Stellar

There were a lot of people, investors, funds who recognized the casino phase of the blockchain in its evolution who created a lot of noise by investing in casino-era technology to mass extract.

They succeeded and max extracted.

Now that the technology and ecosystem has matured into doing things that are actually useful and sustainable, they no longer believe in it.

We move on.

👋🏻

In the latest episode of the Gen C podcast from @CoinDesk with @SamEwen, our CMO @jasonkarsh discusses his journey in the industry, the state of marketing in crypto, and what's cooking at Stellar.

https://t.co/7atHGhl62F

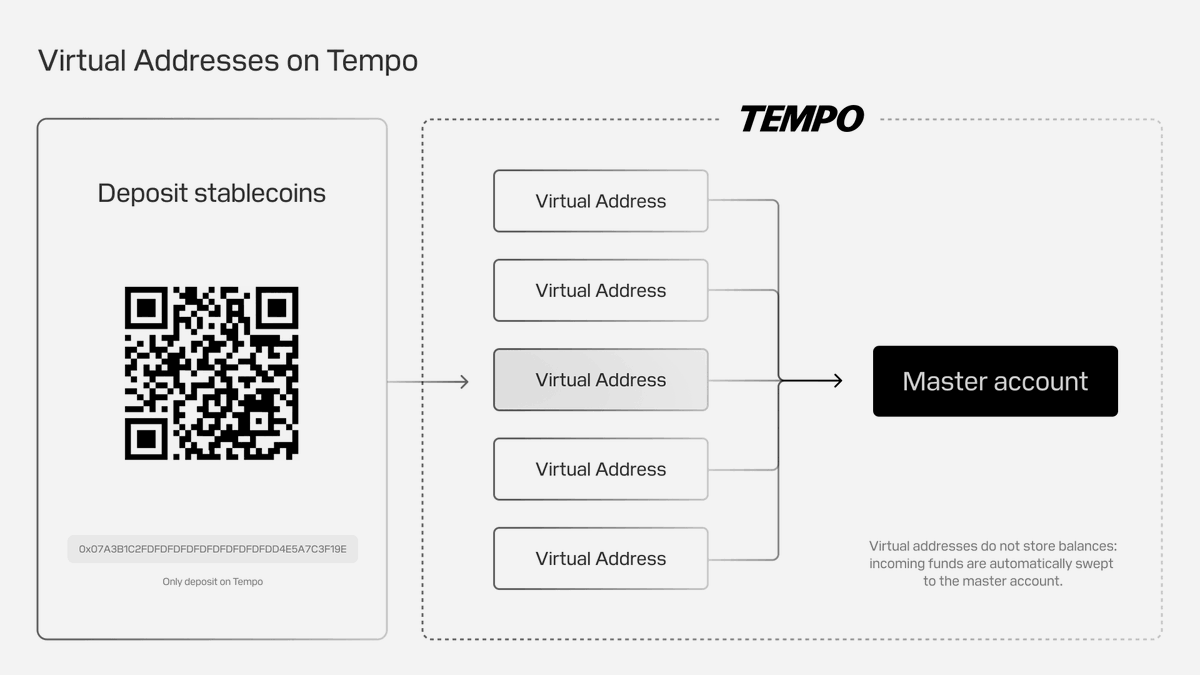

Per-customer deposit addresses are live on Tempo.

On most chains, giving every customer a unique deposit address means initializing, monitoring, and sweeping a real onchain wallet for each.

With virtual addresses, funds credit directly to a master wallet at the protocol layer.