A month ago, it would have taken little to rally the market. Now it would take little to provoke a correction.

The AI value chain is being priced as if every link holds: labs scale, hyperscalers spend, GPUs stay scarce, power arrives, pricing sticks, financing flows, revenue lands before depreciation bites.

The real risk isn't that AI capex collapses. It's that 2026 marks the peak rate of acceleration before monetisation is proven. Expectations only need to stop rising.

SOX ~60% above its 200-day. Put/call at 2022 lows. HY spreads not confirming equity highs. VIX higher than at recent tops. No historical precedent outside a 40-day window in early 2000.

Long book cut to ~1/3 of target, partially hedged, waiting for model confirmation to press shorts.

Full letter ↓

https://t.co/ErwE4sVbXi

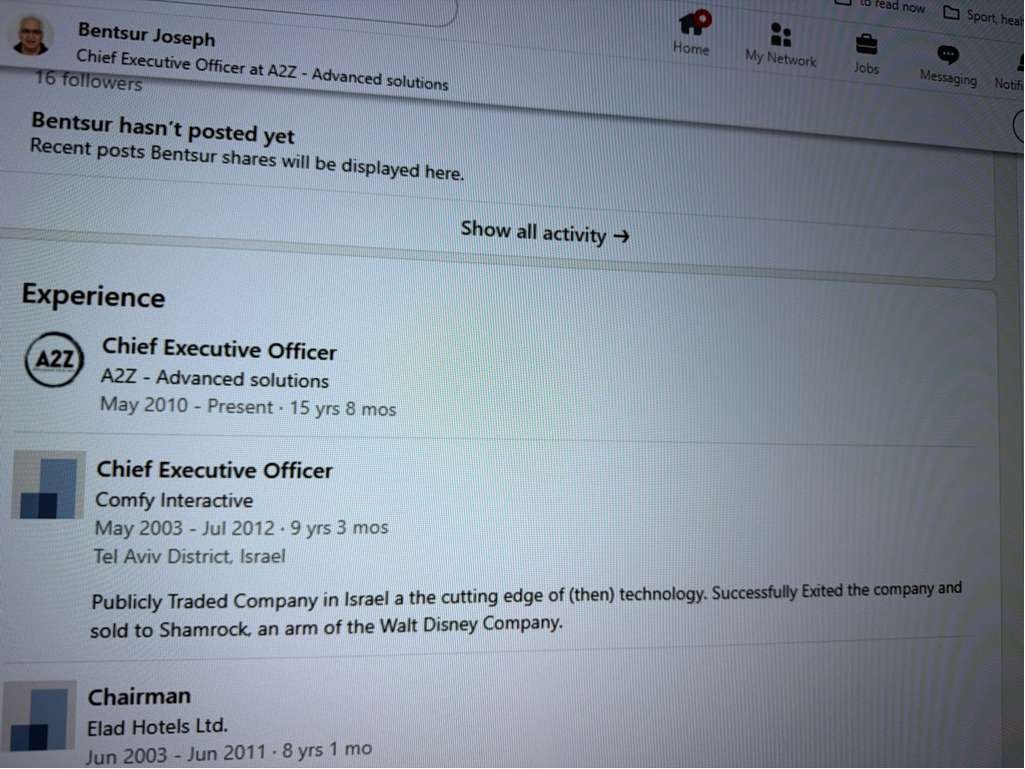

@Pelicanwayre But fair enough — one of the profiles, the one with a single follower, does contain the error you pointed out, so I apologise for saying the picture was fabricated; it is real.

@Pelicanwayre This profile has only one connection and may even have been created automatically by Google or some other software. In any case, the section below correctly states the same information about Comfy. It’s clearly not an attempt to mislead anyone.

My base case: we still need more downside work for a durable, broad rally – a weak rally from here is possible but probably be weak and narrow. October lows + the 100dma sit just below. Sooner or later, I’d expect a break and another around 2–3% to around 6,300–6,400 SPX cash. Worst case: a 200dma test just under around 6,200. Either way, any further leg down is a buy - the rebound should be violent. Even if this is a topping process pre-bear, the first 1–2 corrections (5–10%) are typically bought, and nothing yet (bank crisis / liquidity crunch) argues this time must be different.

6/6

The late-Oct warning signs - weak breadth / Hindenburg Omen, vol divergence, and extreme positioning - ultimately swamped what’s usually supportive seasonality. As I write: S&P 500 >-5% and accelerating lower; Nasdaq 100 around -8%; Russell 2000 around -9%.

1/6

Bottom line: even if seasonality “wins,” the next couple of months are likely to be more volatile, with 5–10% drawdowns more likely-and possibly soon. Good luck with trading.

12/12

Seasonality is the counterpoint. November–December—and November–May more broadly-are typically positive. However, the S&P is already >40% off April lows with six straight up months; the Nasdaq-100 is up seven months in a row and nearly +60% from April.

11/12