🔥Global NAND Memory Market Surges to a Record $46B in Q1 2026 as AI Demand Drives Massive Growth 🔥

📈NAND Memory revenues surged a massive 3.5x annually mirroring the dramatic DRAM growth

📈NAND prices driven by the expanding AI demand are pushing up the revenue every quarter.

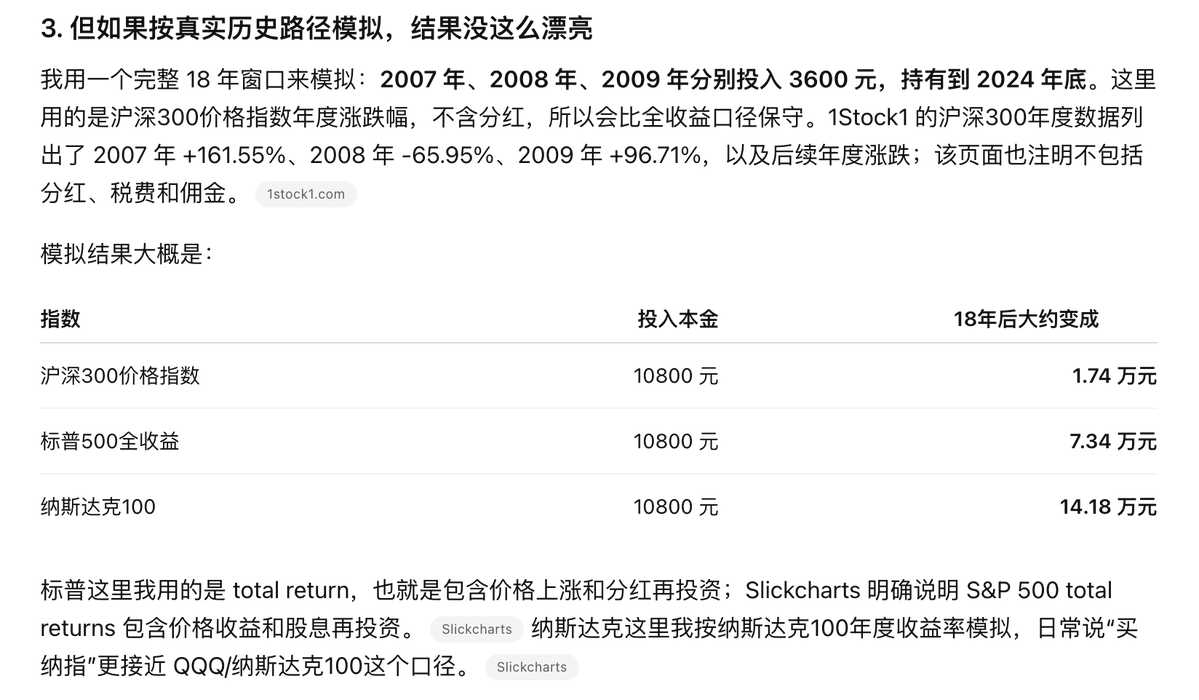

▪️@Samsung is the solid No.1 with a 29% share, followed by SK Hynix and Kioxia.

▪️China’s #YMTC continues its rapid growth, expanding its share to 13%, closing the gap with @SanDisk and @MicronTech

Analysis:

The global NAND flash memory market reached a massive $46 billion in revenues in Q1 2026, fuelled by growing demand for AI infrastructure. According to @CounterPointTR ’s latest NAND Memory Market Tracker, the industry saw the market almost 📈2x sequentially and a staggering 📈3.5x compared to Q1 2025, mirroring the dramatic price hikes previously seen in the DRAM sector.

Key Market Takeaways:

✨The AI Tailwind:

Artificial intelligence infrastructure roll out and move to Agentic AI continues to be the primary growth engine. Server-oriented enterprise SSDs (eSSDs) accounted for 43% of the total NAND market in Q1 2026 and are projected to cross 60% by the end of the year. For perspective, Q1 2026 NAND revenues was greater than the full year 2023 revenues.

👑Samsung Holds the Crown:

Samsung comfortably maintained its number-one position, capturing a 29% market share.

3️⃣ Close Race for Third Spot:

@KioxiaAPAC , Micron, SanDisk and YMTC are pretty close competing fiercely for the third spot with solid demand all across.

🎯YMTC’s Meteoric Rise:

China’s Yangtze Memory Technologies Corp (YMTC) is the market's standout performer. Driven by heavy demand from domestic Chinese manufacturers and price increases driven by supply shortages, YMTC grew almost 445% annually as its market share rose from 8% a year ago to 13% this quarter.

Looking ahead, YMTC is aiming for an Initial Public Offering (IPO) in the Chinese stock market, following a path similar to CXMT. A successful listing is expected to grant the company substantial capital injection and market credibility.

Under this scenario, we expect YMTC to surpass both Kioxia and Micron, widen its lead to emerge as the world’s No. 3 NAND player.

Competitive Landscape: Global Revenue Share (Q1 2025 – Q1 2026)

Based on Counterpoint's latest tracker, the market growth and share breakdown for Q1 2026 stands as follows:

$SNDK $MU $AMAT $LRCX #NAND

June risks checklist:

Fake Risk #1: SpaceX IPO drains liquidity

Everyone is treating this like a black hole for capital. I don’t buy it. The float will likely be tiny relative to the valuation, and market liquidity remains abundant. I think any liquidity shock would be just intraday.

Fake Risk #2: Waller + QT

I highly doubt Waller tries to crash markets with a QT scare in his first meeting. Even if the left hand shrinks the balance sheet, the right hand is pushing financial deregulation and bank balance sheet expansion.

Fake Risk #3: Middle East escalation

My base case remains that this is a price negotiation, not a state negotiation. Escalation is very unlikely.

The real risks:

1. Funds selling because they believe the fake risks. Positioning matters more than narratives.

2. June OPEX.

Call/put IV skew is already heavily tilted toward calls. The closer to OPEX, the vanna/charm flow from OTM call options will force MM to sell.

The uncertainties:

1. Will Waller be much less transparent than JPow? Markets hate uncertainty.

2. Will oil prices resurge as inventories near bottoms? How much of the oil spike leaks into May CPI/PCE?

3. Will BOJ hike 25bps in June?

My plan:

Start reducing leverage and exposure to high-beta names from the first week of June. I will not add any new positions except small monthly call lottery tickets, but will buy dips if SMH/SPX reaches the 21d EMA in the OPEX week, as I expect another bull run post-OPEX.

What's happening in the MLCC market

First off, MLCC as a whole is a $15B market. MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers)

The AI server MLCC market is growing at 80%+ CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)

We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27.

Humanoids are another future high-growth market for MLCCs

Book-to-bill ratio for most MLCC suppliers is over 1 now

Reasons for price hikes-

High Nickel & Silver are affecting all segments

There is a supply-demand mismatch in the high-end (high capacitance, high voltage) segment, which is used in autos & servers

High-end MLCC lead time is over 20 weeks

Spot/distributor prices have increased by 20%-40% for low capacitance & consumer device MLCCs due to hoarding and double booking, especially in China

OEM contracts have not seen large price hikes yet

What's happening now:

Rapid capacity expansion happening across the industry

Murata expects blended ASP prices to remain flat (ASP going down in consumer electronics, expansion in AI server market)

Tier 1 players like Murata, Taiyo Yuden, SEMCO building capacity to serve AI server MLCC market

This will create opportunities for Tier 2/3 and Chinese suppliers to expand in the mid to low end market (Macronix effect)

Future:

MLCC production equiment & raw materials suppliers will be the biggest beneficiary of this CAPEX boom

MLCC producer stocks have performed well, and it is finally spilling to raw material/equipment producers

I expect them to outperform MLCC producers now