Portfolio Strategist @ Rimrock Capital

Markets are a probability distribution of uncertain outcomes, convexity is compounding right tails and cutting the left

Central banks are still paying for the last time they called a supply shock “transitory.” At the Fed, the word may no longer be allowed in the vocabulary.

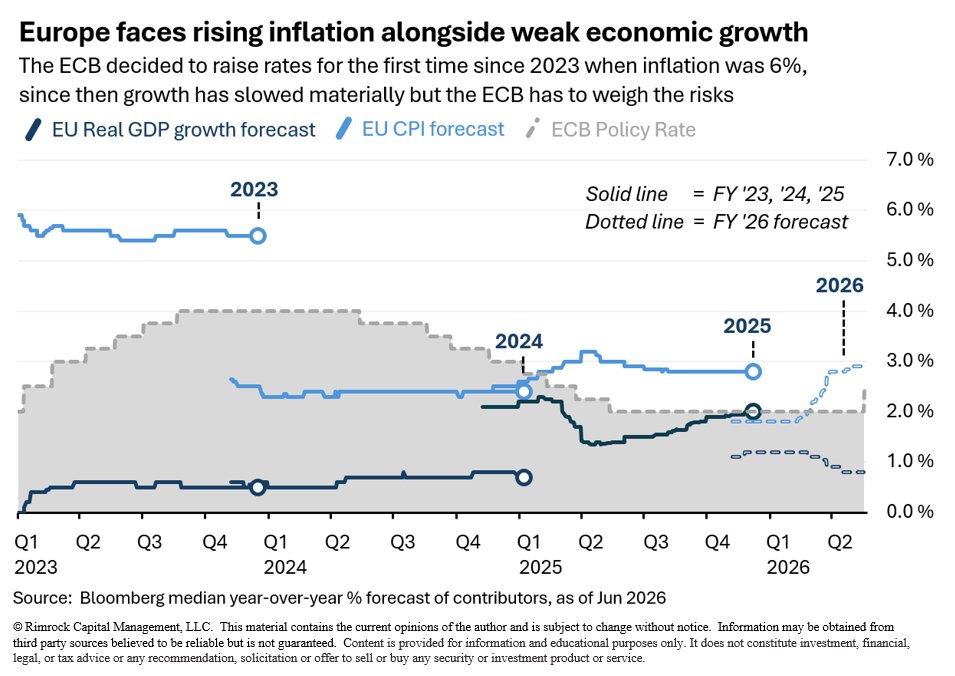

The last time the combination of inflation and growth was at these levels, the ECB was cutting interest rates... will this prove to be a policy mistake by responding to an energy supply shock with rate hikes?

Real income is a strong leading indicator as the consumer drives much of the resilient US economy - rising inflation against weak wage growth is a headwind for 2H-2026

The resiliency of the US economy can largely be attributed to just two things - 1) AI capex and 2) the top 10% of income earners... which is especially circular this cycle. A rug pull could compound quickly...

The price for technology components has historically been disinflationary over time... until now. When several trillion dollars is getting spent on a sector over the next few years where the companies are largely price insensitive, a demand shock has made prices go parabolic. This has implications to inflation in the US.

The Fed's insurance cuts late last year are just now driving a reacceleration in the business cycle with PMIs expanding and earnings expectations near 40-year highs...

Capex outside of tech investment signals caution for the economic outlook, but when hyperscalers are spending the scale they are it more than masks the capex weakness

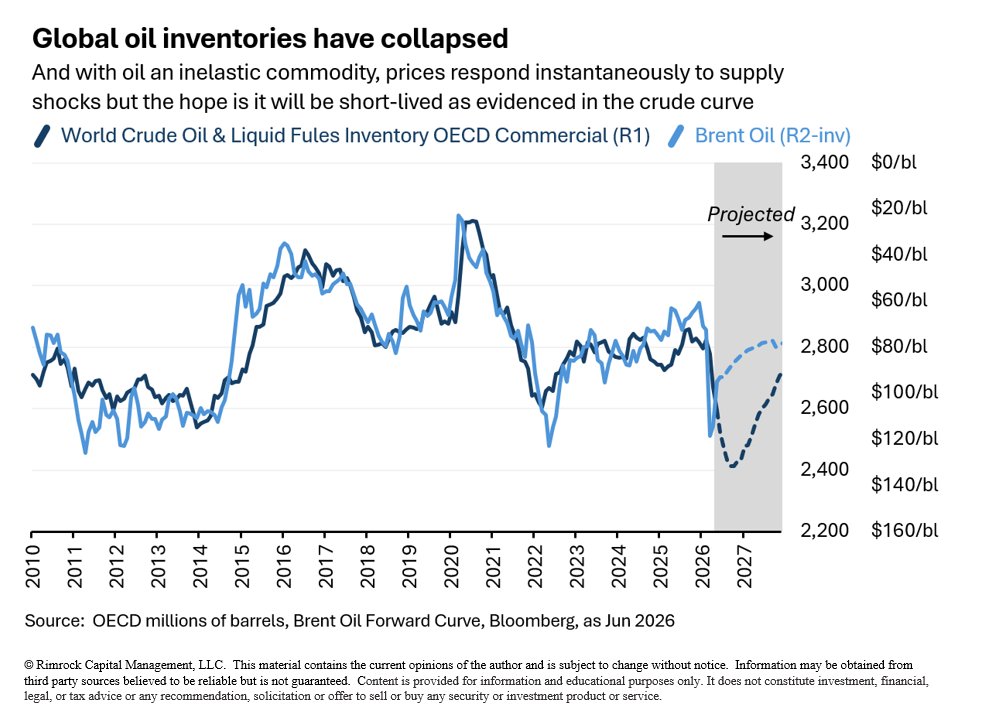

Oil markets are as efficient of a supply/demand curve as you can find in real time we see the prices respond... as the saying goes the best cure for higher prices is higher prices

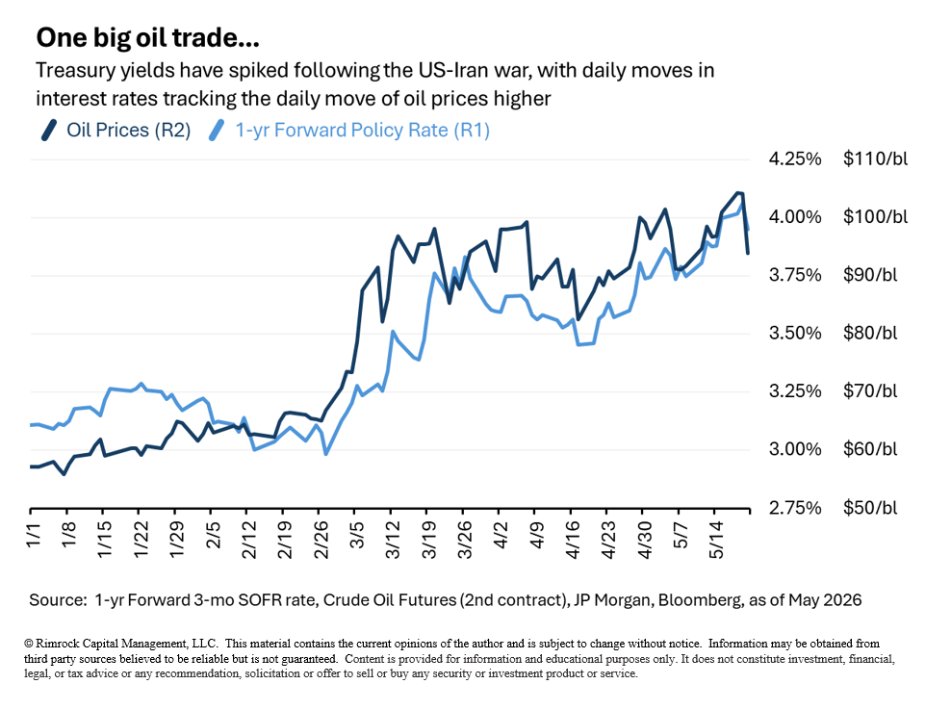

Oil markets are driving rates markets - but the direction is less relevant and it's more about the duration we stay up here at elevated oil prices that matter