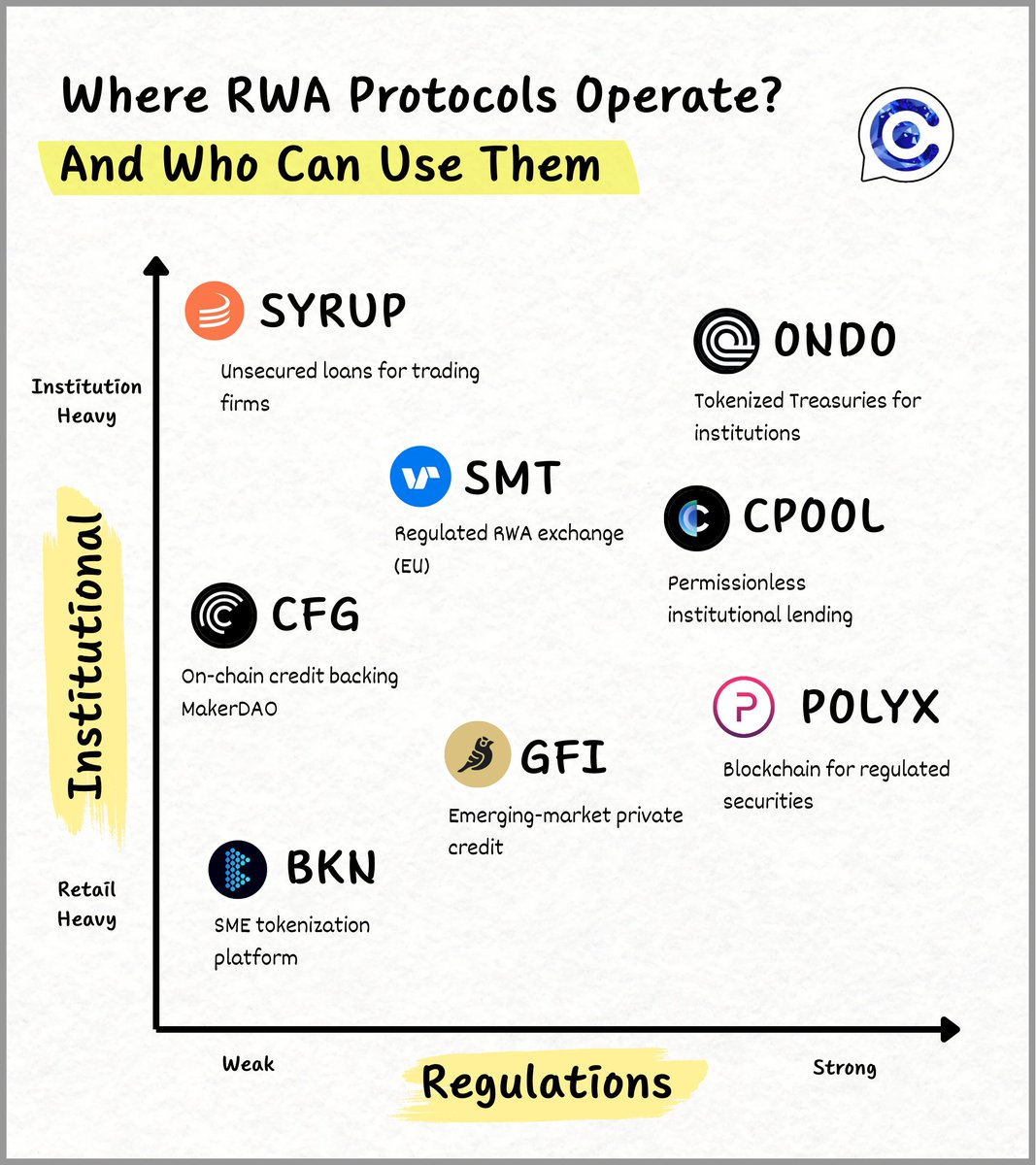

I went deep into the world of RWA protocols.

Everyone says Treasuries, credit & real estate are “on-chain”…

But where, for whom, and at what risk?

→ $ONDO

→ $CFG

→ $SYRUP

→ $GFI

→ $CPOOL

→ $BKN

→ $SMT

→ $POLYX

Here's what I have found 👇

🔵 Ondo Finance ( $ONDO ):

Focus: U.S. Treasuries & yield-bearing stable assets.

Facts & Figures:

• TVL: ~$1.4B locked in Ondo’s USDY and OUSG products (Q3 2025).

• USDY (yield-bearing stablecoin) → backed 1:1 by U.S. Treasuries & bank deposits, offered under Reg S (non-U.S. investors).

• OUSG → provides exposure to BlackRock’s tokenized BUIDL fund (formerly ETF-based).

Regulation:

• Structured under U.S. Reg D/Reg S exemptions.

• Accredited/non-U.S. investors only for most products.

Ondo has basically become the poster child for tokenized U.S. Treasuries.

USDY is pretty interesting, it’s backed 1:1 by U.S. Treasuries & bank deposits, but it’s only offered to non-U.S. investors under Reg S.

OUSG is more of an institutional product that routes into BlackRock’s tokenized fund.

Big names are backing Ondo: Coinbase Ventures, Pantera, Wintermute.

Custody is handled by Coinbase Custody, BitGo, Zodia, Copper.

��� Very institution-heavy right now, but what’s notable is that USDY is starting to show up as collateral in DeFi platforms like Drift on Solana.

🟢 Centrifuge ( $CFG ):

Focus: Tokenizing real-world loans & receivables.

Facts & Figures:

• TVL: ~$1.1B

• Used by MakerDAO → Centrifuge pools (e.g., BlockTower $220M vault) directly backstop DAI.

• Notable borrowers: Trade finance, fintech lenders, real estate financing.

Institutional Involvement:

• Partners with BlockTower Credit, NewSilver (real estate lending), and Anemoy.

Regulation:

• SPV-based (special purpose vehicle) legal wrappers.

• No direct SEC oversight, but structured for institutional participation.

Centrifuge is less about Treasuries and more about tokenizing loans + receivables.

Borrowers include fintech lenders, trade finance companies, even real estate financing.

They use SPVs (special purpose vehicles) for legal structuring not direct SEC oversight, but solid enough to bring in institutional partners.

👉 Institutions, fintech lenders, and DAOs are the ones using it directly.

Retail doesn’t touch it head-on but if you hold DAI, you’re indirectly exposed to Centrifuge assets.

🔴 Maple Finance ( $SYRUP ):

Focus: On-chain loans for trading firms, market makers, and DAOs.

Facts & Figures:

• Total Loans Issued: >$8.4B since launch.

• Notable borrowers: Wintermute, Amber Group, Auros.

• Average yields: 8–15% depending on pool risk.

Institutional Involvement:

• Credit desks and professional trading firms use it for liquidity.

Regulation:

• No SEC registration, operates under offshore structures.

• Relies on “Pool Delegates” to manage borrower due diligence.

Maple built a DeFi-native credit marketplace. Think unsecured loans for trading firms, market makers, and DAOs.

But Maple isn’t regulated, it runs offshore and relies on “Pool Delegates” to handle due diligence.

👉 It’s been powerful for professional lenders and DAOs, but let’s not sugarcoat: the 2022–23 period saw painful defaults that hurt confidence.

Definitely not a retail-friendly playground.

🟣 Goldfinch ( $GFI ):

Focus: Lending to businesses in emerging markets & institutional private credit.

Facts & Figures:

• Loans Issued: ~$200M (2021–2024) via emerging-market lenders.

• Now launching Goldfinch Prime → access to institutional private-credit funds (Ares, Apollo, Golub).

• Yield for lenders: target 9–12% (non-U.S. investors).

Institutional Involvement:

• Partnerships with fintech lenders (PayJoy, Tugende) + institutional funds via Prime.

• Mostly emerging market SMB borrowers historically.

Regulation:

• Weak, no formal SEC or EU framework.

• Relies on off-chain loan agreements.

Goldfinch took a different approach, starting with loans to small businesses in emerging markets, and now moving into institutional private credit.

Now launching Goldfinch Prime → gives accredited/non-U.S. investors access to credit funds from giants like Ares, Apollo, Golub.

The original model was retail-friendly (on-chain lending to SMBs via fintechs like PayJoy, Tugende).

But the pivot is clear: Prime is about institutional players.

👉 Started grassroots with retail, now climbing the ladder to institutional credit.

⚫ Clearpool ( $CPOOL ):

Focus: Unsecured lending to institutions via on-chain credit pools.

Facts & Figures:

• Loans Issued: >$660M since launch.

• Borrowers: Jane Street, Wintermute, CoinShares, Fasanara.

• Average yields: 7–12%.

Institutional Involvement:

• High → trading desks and market makers are key borrowers.

Regulation:

• Moderate → permissioned KYC pools launched in 2023 (Clearpool Prime).

• No SEC registration, but stronger compliance than Maple.

Clearpool is another unsecured lending platform, often compared to Maple but it leans more on compliance.

They launched “Clearpool Prime” in 2023, which introduced permissioned/KYC pools a step Maple hasn’t taken as far.

👉 Institutions like it, pros use it, and for retail lenders it’s… risky but accessible. Think of it as “Maple with more compliance layers.”

🟠 Brickken ( $BKN ):

Focus: SaaS platform to tokenize equity, debt, and RWAs for SMEs & enterprises.

Facts & Figures:

• Assets tokenized: >$250M across 14 countries since 2023.

• Reached EBITDA positive in 2024.

• Raised $2.5M seed (Jan 2025) to expand into EU, US, Asia.

Institutional Involvement:

• Low → SMEs & corporates, less institutional finance than Ondo/Swarm.

Regulation:

• Compliance depends on issuer jurisdiction.

• Platform provides legal & tech framework; BKN token as governance/utility.

Brickken is totally different from the others here.

It’s not about Treasuries or credit desks.

It’s a SaaS platform that helps SMEs tokenize equity, debt, and RWAs.

�� Great for startups and enterprises issuing tokenized shares/bonds. Investor access depends on where the issuer is based.

🟡 Swarm Markets ( $SMT ):

Focus: Tokenized securities & regulated DeFi.

Facts & Figures:

• Licensed by BaFin (German financial regulator).

• Offers tokenized U.S. Treasuries, bonds, stocks.

Institutional Involvement:

• High → targeted at European institutional investors.

• Provides regulated KYC DeFi access.

Regulation:

• Strong → fully licensed under MiFID II (EU securities framework).

Swarm is one of the few fully regulated RWA platforms.

Offers tokenized Treasuries, corporate bonds, even stocks.

Everything is done under MiFID II (the EU’s securities framework).

👉 This is squarely for institutions and accredited investors.

If you’re retail, you’re not trading here but institutions love the regulatory clarity.

🔵 Polymesh ( $POLYX ):

Focus: Purpose-built L1 blockchain for regulated digital securities.

Facts & Figures:

• Validator set controlled by KYC/AML verified participants.

• Native POLYX staking requires identity verification.

• Ecosystem includes custody providers & regulated brokers.

Institutional Involvement:

• High → designed for capital markets.

Regulation:

• Strong → compliance baked at protocol level.

• Only verified entities/individuals can issue/transfer securities.

Polymesh isn’t a protocol sitting on Ethereum it’s a whole blockchain built specifically for regulated securities.

Validator set = all KYC/AML verified.

Ecosystem includes custody providers + regulated brokers.

👉 It’s compliance baked right into the chain.

Very much for banks, asset managers, and regulated entities not for your average degen.

🔚 Conclusion: The RWA Divide

Institutional Corner: Ondo, Swarm, Polymesh → compliant, built for big money.

Credit Innovators: Maple, Centrifuge → institutional borrowers, but regulatory gaps.

Retail Edge: Clearpool, Goldfinch, Brickken → expand access to everyday investors, though exposure comes with a bit of legal and credit risk.

@SebasP49474734 What's your opinion on the Stoch RSI on the monthly on the Kucoin chart? It's in the completely overbought territory at value 94 of 100. I couldn't find another crypto that is overbought on the monthly Stoch RSI, only $QNT is.

@MindCrypto_ Please note that the amount of addresses that hold at least 1 QNT is 112000. That means 40000 addresses are not that meaningful. This puts this rankings in another perspective. You can check the holdings of all wallets at etherscan. At page 1103 begins the addresses with 1 QNT.

@ChartNerdTA What do you think about the upcoming token unlocks? Only around 30% is in circulation and in september 2.00B tokens will be unlocked according to https://t.co/QroEsJB9wm Does it concern you?

@SebasP49474734 No bed, no roof and even no food. All is in $QNT now. But sometimes after closing hours I'm allowed to enter the local slaughterhouse, where they allow me to eat the scrappings of the abatoir floor.

@SebasP49474734 ,,Willen jullie meer, of minder Quantstradamus?"

-,,Minder, minder, minder!!"

Listening to his voicechanging videos is a home remedie for premature ejaculation.

There's no formal measurement for cringe, but after watching his videos I can assure you: IT'S OVER 9000!