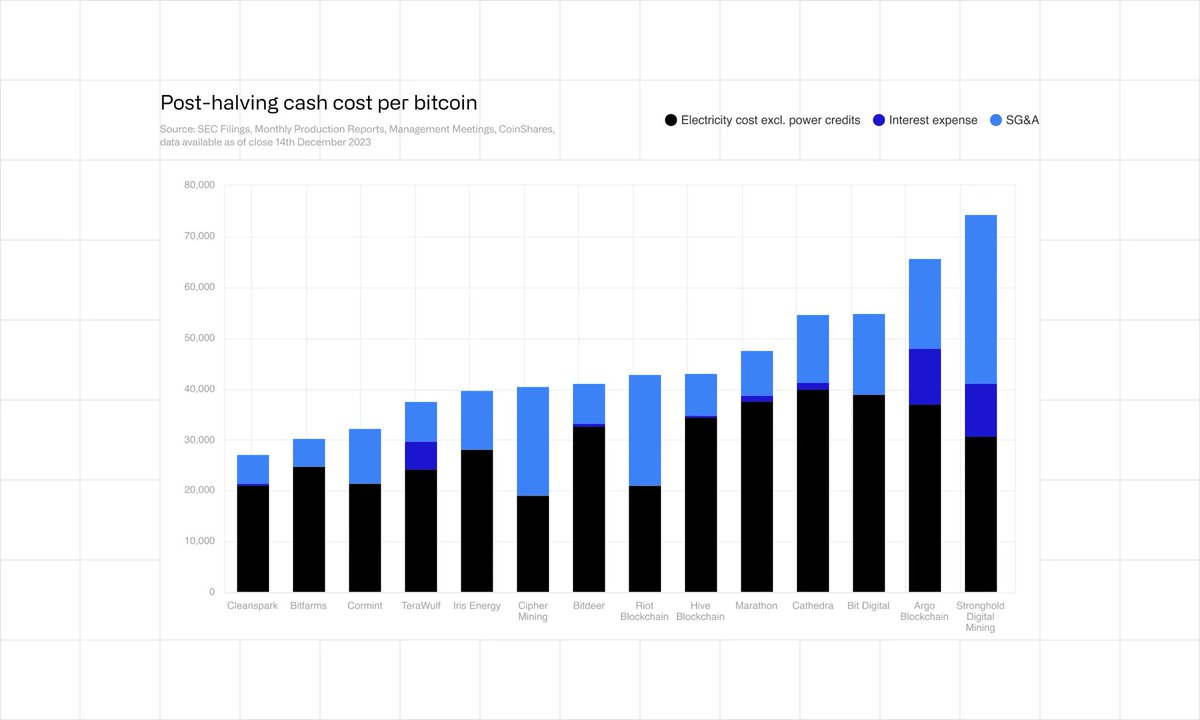

@DeFi_Made_Here If you don’t pay dividends, it doesn’t mean you don’t generate revenue

For lending tvl is bs metric as its growing doesn’t mean your net interest income grows

For trading liquidity used to be the operational metric to watch before univ3, you can see it in the table

@sonyasunkim@artemis__xyz * it only works in the regime when the fees generated and broader fundamentals are interlinked with the price, which is not the case for the crypto atm. Here it is just simple that inflation vs. inflows, that's it

to have inflows = f(fundamentals incl. rev growth) takes time

@0xsudogm @_kaitoai How does it feel to shill a saas that you invested 5.3 mil?:)) kek and comments are from: founder kaito, colleague at dragonfly, kaito official and (?) angel in kaito

no hate, kaito is gud, just funny

@pablo_veyrat@ethena making it tokenized thus publicly available also enhances the health of the futures market, which has been long-skewed, making leverage expensive. Now, with @ethena as a significant long-term short seller, the volatility and skew of rates should decrease

On stETH as collateral: recently CEXs have introduced 3rd-party custody, so for the big institutional clients like @ethena I suppose all exchanges mentioned in the docs gave the opportunity to use it as collateral with small haircut

On risks: agree with @EvgenyGaevoy most of the risk is in execution of the team (margin management, leverage management) + premium on the smart contract risk of LST protocols. Market risk is offset between margin and position

Lots of the teams were doing Basis trading: short perps long spot collecting funding rates (note margin is used to cover funding rates + pnl also). But ethena did it at scale and public and I consider 600m move from Maker as an investment into this strategy and treasury management. Looks like it is a smart decision for 33% roi vs. 5.25% on UST through brokerage account not controllable by MakerDAO :))

We have been living in the market regime long skewed so the funding rates cumulative were positive :

https://t.co/v3sGD802sd

We will see the performance when the regime will change, however anything up to 10bn USDe marketcap can bee easily opened and unwinded, further harder to imagine as it will be 50%+ of the futures market

Binance and Bybit account for 51%+ of the futures perpetual market in terms of Open Interest. Interestingly the cumulative funding rate for $BTC is not only positive, meaning that the market is bullish-skewed, but also positively stable with only 3 months out 53 for @binance (4/47 for @Bybit_Official ) closing in negative zone during black swans of Luna case and FTX.

Then, delta-neutral basis trade (Long BTC spot + Short BTCUSDT perp) is simple and good for nominal yields and for risk-adjusted Sharpe as well.

@gleng2041 @ramahluwalia You don’t care so much that spent an hour typing 5 posts why the young guy has not “made” it. Looks like your ego is so sensitive ahah. I was also there, would have rather traded memecoins instead

@amtwo_eth@yugacohler technically yes, but in reality it is almost impossible, you either need your own capital to bootstrap or at least some sort of injections, because barrier to enter is still high (which makes the opportunity big though)

3/N Despite high interest rates and a hawkish monetary policy, US liquidity has been increasing since hitting a bottom in Q4 2022. This indicates a local bottom for equities as well as the absolute bottom for BTC at 16k and the broader crypto market. This chart illustrates this, by @LynAldenContact